|

시장보고서

상품코드

1939050

스마트 라벨 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Smart Label - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

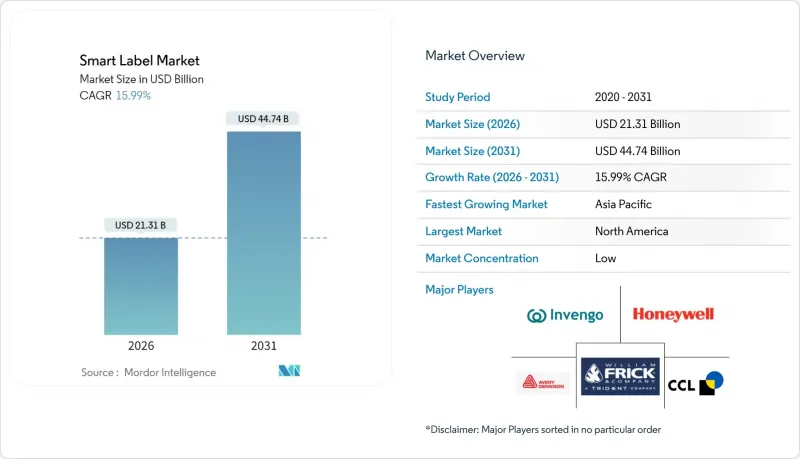

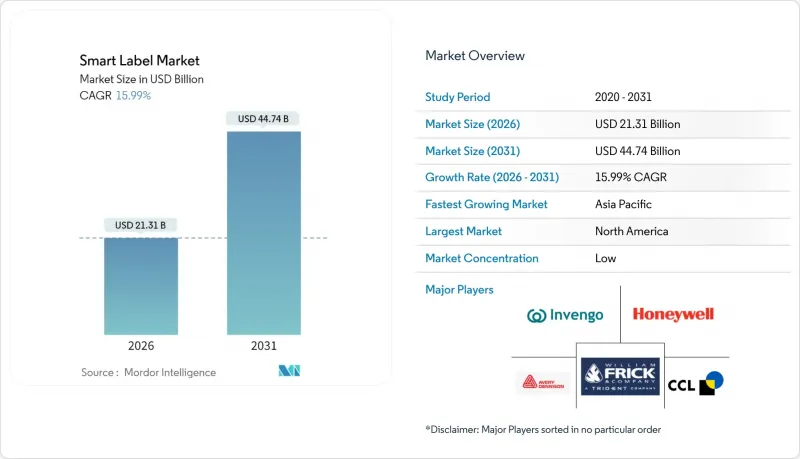

스마트 라벨 시장 규모는 2026년에는 213억 1,000만 달러로 추정되고 있으며, 2025년 183억 8,000만 달러에서 성장하고 있습니다. 2031년의 예측에서는 447억 4,000만 달러에 달하며, 2026-2031년에 CAGR 15.99%로 성장할 것으로 전망되고 있습니다.

이러한 성장은 규제 요건, 무선 주파수 식별(RFID) 및 근거리 무선통신(NFC) 기술의 발전, 엔드투엔드 공급망 투명성에 대한 수요 증가와 함께 이루어지고 있습니다. FDA의 의약품 공급망 보안법에 따른 의약품 직렬화, 디지털 제품 여권 개념을 도입한 EU의 포장 및 포장 폐기물 규정(PPWR), 월마트와 같은 소매업체가 주도하는 RFID 프로그램 등이 결합되어 필수적인 규정 준수 표준이 확립되었습니다. 이에 따라 각 업체들은 클라우드 분석, 블록체인 인증, 수동형 라벨을 데이터가 풍부한 자산으로 변환하는 환경 IoT 센서를 통합하여 실시간 재고 가시성, 동적 가격 책정, 산업 전반의 상태 모니터링을 실현하고 있습니다.

세계 스마트 라벨 시장 동향 및 인사이트

재고 가시화를 위한 RFID 도입 확대

월마트가 수천 개의 재고 관리 단위(SKU)에 초고주파(UHF) RFID 태그 장착을 의무화하면서 공급업체들은 생산라인을 개조해야 했고, 업계 전반에 걸쳐 RAIN RFID 인코딩 솔루션에 대한 투자를 촉진했습니다. 공급업체는 제조 실행 시스템과 직접 연동되는 영구적인 재고 가시성을 확보하여 자재 부족을 줄이고 디지털 트윈을 통한 스케줄링 효율을 향상시킬 수 있습니다. 퀄컴이 스마트폰에 RAIN RFID를 내장할 계획인 만큼, 조만간 모든 소비자용 기기에 리더 기능이 탑재되어 고정형 스캐너 인프라가 필요 없어져 소규모 소매업체들의 도입이 가속화될 것으로 보입니다. 한편, 안테나의 소형화로 3미터의 판독 범위를 실현하여 고객 경험을 향상시키는 원활한 체크아웃 구역을 구현할 수 있습니다.

의약품 공급망에서 위조 방지 수요 증가

2024년 11월 DSCSA가 전면 시행됨에 따라 거래 파트너는 제품 인도 전에 일련화된 식별자 검증을 의무적으로 수행해야 합니다. 이를 통해 위변조 방지 및 투약 정보 표시를 위한 NFC 칩, 블록체인 암호화, 전자 종이 디스플레이를 통합한 라벨의 업그레이드를 촉진하고 있습니다. 예를 들어 Ynvisible의 ConnectedLabel은 연간 100만개 이상의 의약품 패키지에서 거의 실시간 온도 추적을 지원하고 있습니다. 미국 외의 국가로는 인도에서 인기 의약품에 QR코드 표시를 의무화하고 있으며, 이는 일련번호 표시가 단순한 컴플라이언스 대응에서 환자 안전의 차별화 요소로 전환되고 있음을 보여줍니다.

소규모 소매업체에 대한 높은 초기 하드웨어 통합 비용

전자식 선반 태그(ESL)는 태그당 11-12달러의 고가이며, 수천 개의 SKU에 배포할 경우 많은 자본 투자가 필요합니다. 소규모 소매업체들은 POS(Point of Sale) 시스템 업데이트와 직원 교육에 대한 예산도 확보해야 하므로 노동력 절감의 가능성에도 불구하고 도입이 늦어지고 있습니다. 구독 모델도 등장하고 있지만, 아직은 개발 단계에 머물러 있습니다.

부문 분석

2025년 기준 RFID는 스마트 라벨 시장 점유율의 37.86%를 차지할 것으로 예상되며, 소매 및 물류 분야에서 입증된 확장성을 기반으로 하고 있습니다. NFC는 현재 규모는 작지만, 스마트폰의 전 세계적 보급을 활용한 '탭으로 인증' 경험으로 19.52%의 연평균 복합 성장률(CAGR)이 예상됩니다. 따라서 NFC 관련 스마트 라벨 시장 규모는 특히 블록체인 통합을 통한 위변조 방지 기능을 갖춘 고급품 인증 분야에서 절대 금액 기준으로 가장 가파른 성장세를 보이고 있습니다. 전자 상품 모니터링(EAS)은 안정적으로 유지되는 반면, 센싱 라벨은 콜드체인 및 환경 규제 대응 이용 사례에서 성장세를 보이고 있습니다. 전체적으로 기술 전환은 수동적 식별에서 다기능 센서 및 참여 툴로 이동하고 있습니다.

ST마이크로일렉트로닉스의 ST25Connect 프로그램을 통해 소비자와의 양방향성이 더욱 확대되고 있습니다. 의료기기, 와인, 화장품에 NFC 태그를 내장하여 개인화된 컨텐츠를 제공하는 동시에 참여도 분석 데이터를 수집할 수 있습니다. 인레이에 저비용 센서를 통합함으로써 추적, 상태 모니터링, 고객 커뮤니케이션의 경계가 더욱 모호해지면서 RFID와 NFC는 융합된 혁신의 길을 걷고 있습니다.

소매업은 2025년 기준 30.48%의 매출 점유율을 유지하고 있으며, 이는 매장 전체 RFID 프로그램의 조기 도입과 전자가격표시기(ESL)의 보급 확대를 반영하고 있습니다. 그러나 의료 및 제약 분야 관련 스마트 라벨 시장 규모는 업계 전체에서 가장 빠른 19.08%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 일련번호와 온도 관리 물류의 필요성으로 인해 병원, 약국, 수탁제조업체들은 엔드 투 엔드 추적성을 위해 스마트 라벨을 도입하고 있습니다. 물류 사업자와 3자 물류(3PL)도 하이브리드형 셀룰러 BLE 라벨을 도입하여 인수인계 서류의 실시간 자동화를 실현하고 있습니다.

프레제니우스 카비의 데이터 매트릭스+RFID 도입 사례는 급성기 병원 환경에서 약물 확인이 인적 오류를 줄일 수 있는 실례를 보여줍니다. 임상시험용 디지털 라벨은 언어 변경에 따른 수동 재부착이 필요 없어 환자의 컴플라이언스 향상과 규제 감사를 간소화할 수 있습니다. 이러한 움직임은 FDA의 FSMA 204 추적성 의무화에 대비한 식품 및 음료 업계에도 확산되고 있습니다.

스마트 라벨 시장 보고서는 기술별(RFID, EAS, NFC, 센싱 라벨, ESL 등), 최종사용자별(소매, 의료, 물류, 제조 등), 구성부품별(IC, 배터리, 안테나 등), 용도별(추적, 보안, 콜드체인, 가격표시 등), 형태별(스티커, 태그 등), 지역별(북미, 유럽, 아시아태평양, 중동, 아프리카, 남미, 유럽, 아시아태평양 등)로 구분하여 조사했습니다. 스티커, 태그 등), 지역(북미, 유럽, 아시아태평양, 중동/아프리카, 남미) 별로 분류되어 있습니다. 시장 예측은 금액 기준(USD)으로 제시됩니다.

지역별 분석

북미는 2025년 전 세계 매출의 37.12%를 차지할 것으로 예상되며, 이는 미국 소매 업계의 RFID 조기 도입과 법적 구속력이 있는 DSCSA 시리얼라이제이션 로드맵의 기반이 되고 있습니다. 2030년까지 국내 반도체 생산량을 3배로 확대하는 연방정부의 지속적인 투자로 최근 도입 일정을 지연시켰던 칩 부족 현상이 완화될 전망입니다. 캐나다와 멕시코는 니어쇼어링의 발전에 따른 통합된 국경 간 상업의 혜택을 누리고 있습니다. 또한 에이버리데니슨이 1억 달러를 투자한 케레타로 공장은 지역내 스마트 라벨 수요 증가에 대응할 예정입니다.

유럽은 지속가능성을 중시하는 규제에 힘입어 제2의 지역 블록을 형성하고 있습니다. 곧 시행될 PPWR(플라스틱 포장 규정)은 재활용 가능성 평가를 위한 디지털 식별자를 의무화하고, 독일의 전기자동차 배터리 패스포트 시범 운영은 자동차 밸류체인에서 RFID의 정착을 촉진할 것입니다. 코니카미놀타의 예측에 따르면 유럽 RFID 라벨 시장은 2027년까지 25억 유로(28억 달러)에 달할 것으로 예상되며, 이는 소비재, 의료 및 산업 분야의 광범위한 채택을 반영할 것으로 보입니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 18.21%로 가장 빠르게 성장하는 지역입니다. 중국의 7,000개 식품 생산업체에 대한 2D 바코드 도입, 인도의 플라스틱 폐기물 QR코드 추적 시스템, 일본의 인더스트리 5.0 추진책이 결합되어 특히 큰 모멘텀을 창출하고 있습니다. 확장되는 5G 및 계획 중인 6G 네트워크는 환경 IoT의 기반을 제공하고, 배터리가 필요 없는 센서의 대규모 도입을 지원합니다. 대만과 한국에 집중된 반도체 제조는 공급 측면에서 우위를 가져다 주지만, 지정학적 리스크는 여전히 변수로 작용할 수 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05Smart label market size in 2026 is estimated at USD 21.31 billion, growing from 2025 value of USD 18.38 billion with 2031 projections showing USD 44.74 billion, growing at 15.99% CAGR over 2026-2031.

This growth reflects the intersection of regulatory mandates, advances in radio-frequency identification (RFID) and near-field communication (NFC) technologies, and rising demand for end-to-end supply-chain transparency. Pharmaceutical serialization under the FDA's Drug Supply Chain Security Act, the European Union's Packaging and Packaging Waste Regulation (PPWR) that embeds digital-product-passport concepts, and retailer-driven RFID programs such as Walmart's have together created a non-negotiable compliance baseline. Companies are responding by integrating cloud analytics, blockchain authentication, and ambient IoT sensors that convert passive labels into data-rich assets, enabling real-time inventory visibility, dynamic pricing, and condition monitoring across industries.

Global Smart Label Market Trends and Insights

Growing RFID Adoption for Inventory Visibility

Walmart's mandate for ultra-high-frequency (UHF) RFID tags on thousands of stock-keeping units has pushed suppliers to retrofit production lines, catalyzing sector-wide investment in RAIN RFID encoding solutions. Suppliers gain perpetual stock visibility that feeds directly into manufacturing execution systems, reducing material shortages and unlocking digital-twin scheduling efficiencies. Qualcomm's plan to embed RAIN RFID in smartphones will soon turn every consumer device into a reader, eliminating the need for fixed scanner infrastructure and accelerating small-retailer adoption. Meanwhile, antenna miniaturization now supports 10-foot read ranges, enabling frictionless checkout zones that elevate customer experience.

Rising Demand for Anti-Counterfeiting in Pharma Supply Chains

Full enforcement of the DSCSA in November 2024 requires trading partners to verify serialized identifiers before product hand-off, prompting label upgrades that combine NFC chips, blockchain encryption, and e-paper displays for tamper evidence and dosage information. Ynvisible's ConnectedLabel, for instance, supports near real-time temperature tracking on over 1 million pharma packs annually. Outside the United States, India has ordered QR codes on the top-selling medicines, illustrating how serialization is moving from compliance exercise to patient-safety differentiator.

High Initial Hardware and Integration Costs for Small Retailers

ESLs cost USD 11-12 per tag, creating steep capital requirements when rolled out across thousands of SKUs. Smaller retailers must also budget for point-of-sale upgrades and staff training, delaying adoption despite labor-saving potential. Subscription models are emerging but remain nascent.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Omnichannel Retail Requiring Real-Time Pricing

- Increasing Penetration of IoT-Enabled Logistics

- Semiconductor Supply Constraints Delaying UHF RFID IC Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

RFID accounted for 37.86% of the smart label market share in 2025, underpinned by proven scalability in retail and logistics. NFC, though smaller today, is projected for 19.52% CAGR because it exploits the global ubiquity of smartphones for tap-to-verify experiences. The smart label market size tied to NFC therefore shows the steepest absolute dollar expansion, especially in luxury authentication where blockchain integration delivers tamper-evident provenance. Electronic article surveillance remains steady, whereas sensing labels gain momentum through cold-chain and environmental compliance use cases. Overall, technology migration is moving from passive identification toward multifunction sensors and engagement tools.

Greater consumer interactivity is being unlocked by STMicroelectronics' ST25Connect program, enabling NFC tags in medical devices, wine, and cosmetics to deliver personalized content while capturing engagement analytics. Integrating low-cost sensors within inlays further blurs lines between tracking, condition monitoring, and customer communication, placing RFID and NFC on convergent innovation paths.

Retail retained 30.48% revenue share in 2025, reflecting early adoption of store-wide RFID programs and growing ESL footprints. However, the smart label market size linked to healthcare and pharmaceuticals is set to grow at 19.08% CAGR, the fastest across industries. Serialization deadlines and the need for temperature-controlled logistics drive hospitals, pharmacies, and contract manufacturers to embed smart labels for end-to-end traceability. Logistics providers and 3PLs also deploy hybrid cellular-BLE labels to automate hand-off documentation in real time.

Fresenius Kabi's Data Matrix plus RFID initiative illustrates how medication verification cuts human error in high-acuity hospital environments. Digital display labels for clinical trials eliminate manual relabeling across language variants, improving patient compliance and simplifying regulatory audits. Similar dynamics extend to food and beverage players gearing up for the FDA's FSMA 204 traceability mandates.

The Smart Label Market Report is Segmented by Technology (RFID, EAS, NFC, Sensing Labels, ESL, and More), End-User (Retail, Healthcare, Logistics, Manufacturing, and More), Component (ICs, Batteries, Antennas, and More), Application (Tracking, Security, Cold-Chain, Pricing, and More), Form Factor (Stickers, Tags, and More), and Geography (North America, Europe, APAC, MEA, South America). Market Forecasts in Value (USD).

Geography Analysis

North America held 37.12% of global revenue in 2025, anchored by the United States' early adoption of RFID in retail and the legally binding DSCSA serialization roadmap. Continued federal investment aimed at tripling domestic semiconductor output by 2030 will reduce chip shortages that have recently slowed deployment schedules. Canada and Mexico benefit from integrated cross-border commerce as near-shoring picks up, while Avery Dennison's USD 100 million Queretaro facility is set to meet rising regional demand for smart labels.

Europe represents the second-largest regional block, buoyed by sustainability-centric regulation. The forthcoming PPWR mandates digital identifiers for recyclability scoring, and Germany's battery-passport pilot for electric vehicles solidifies RFID within automotive value chains. Konica Minolta forecasts the European RFID label market to reach EUR 2.5 billion (USD 2.8 billion) by 2027, reflecting widespread adoption in consumer goods, healthcare, and industrial sectors.

Asia-Pacific is the fastest-growing geography with an 18.21% CAGR through 2031. China's 2D-barcode rollout across 7,000 food producers, India's QR-code traceability for plastic waste, and Japan's industry-5.0 incentives together generate outsized momentum. Growing 5G and planned 6G coverage provides the network backbone for ambient IoT, supporting large-volume adoption of battery-free sensors. Chip manufacturing concentration in Taiwan and South Korea offers supply advantages, although geopolitical risk remains a variable.

- Avery Dennison Corporation

- CCL Industries Inc.

- Zebra Technologies Corp.

- Honeywell International Inc.

- SATO Holdings Corp.

- William Frick & Company

- Invengo Information Technology Co. Ltd.

- Scanbuy Inc.

- Alien Technology LLC

- Roambee Corporation

- Smartrac (NXP)

- SES-imagotag SA

- Pricer AB

- Thinfilm Electronics ASA

- Digimarc Corporation

- Tapwow LLC

- Stora Enso Oyj

- Identiv Inc.

- Impinj Inc.

- Checkpoint Systems Inc.

- Confidex Ltd.

- NXP Semiconductors N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing RFID adoption for inventory visibility

- 4.2.2 Rising demand for anti-counterfeiting in pharma supply chains

- 4.2.3 Expansion of omnichannel retail requiring real-time pricing

- 4.2.4 Increasing penetration of IoT-enabled logistics

- 4.2.5 Emergence of printed battery-free sensor labels for cold-chain integrity

- 4.2.6 EU ESG packaging mandates (PPWR 2026) accelerating smart-label integration

- 4.3 Market Restraints

- 4.3.1 High initial hardware and integration costs for small retailers

- 4.3.2 Lack of universal interoperability standards

- 4.3.3 Semiconductor supply constraints delaying UHF RFID IC availability

- 4.3.4 Data-privacy regulations limiting NFC consumer-engagement analytics

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 RFID

- 5.1.2 Electronic Article Surveillance (EAS)

- 5.1.3 Near Field Communication (NFC)

- 5.1.4 Sensing Labels (Temp, Gas, etc.)

- 5.1.5 Electronic Shelf Label (ESL)

- 5.1.6 Other Emerging (QR, BLE)

- 5.2 By End-user Industry

- 5.2.1 Retail

- 5.2.2 Healthcare and Pharmaceuticals

- 5.2.3 Logistics and Transportation

- 5.2.4 Manufacturing and Industrial

- 5.2.5 Food and Beverage

- 5.2.6 Other End-user Industry

- 5.3 By Component

- 5.3.1 Micro-controllers / ICs

- 5.3.2 Batteries and Power Units

- 5.3.3 Antennas and Transceivers

- 5.3.4 Sensors

- 5.3.5 Software and Middleware

- 5.3.6 Substrate and Protective Materials

- 5.4 By Application

- 5.4.1 Asset and Inventory Tracking

- 5.4.2 Anti-theft and Security

- 5.4.3 Cold-chain Monitoring

- 5.4.4 Dynamic Pricing and Promotion

- 5.4.5 Brand Authentication and Consumer Engagement

- 5.4.6 Work-in-Process Management

- 5.5 By Label Form Factor

- 5.5.1 Wet-inlay / Sticker Labels

- 5.5.2 Hang Tags

- 5.5.3 In-mold Labels

- 5.5.4 Textile and Apparel Labels

- 5.5.5 Printable Flexible Sensor Labels

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 CCL Industries Inc.

- 6.4.3 Zebra Technologies Corp.

- 6.4.4 Honeywell International Inc.

- 6.4.5 SATO Holdings Corp.

- 6.4.6 William Frick & Company

- 6.4.7 Invengo Information Technology Co. Ltd.

- 6.4.8 Scanbuy Inc.

- 6.4.9 Alien Technology LLC

- 6.4.10 Roambee Corporation

- 6.4.11 Smartrac (NXP)

- 6.4.12 SES-imagotag SA

- 6.4.13 Pricer AB

- 6.4.14 Thinfilm Electronics ASA

- 6.4.15 Digimarc Corporation

- 6.4.16 Tapwow LLC

- 6.4.17 Stora Enso Oyj

- 6.4.18 Identiv Inc.

- 6.4.19 Impinj Inc.

- 6.4.20 Checkpoint Systems Inc.

- 6.4.21 Confidex Ltd.

- 6.4.22 NXP Semiconductors N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment