|

시장보고서

상품코드

1939069

베트남의 플라스틱 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vietnam Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

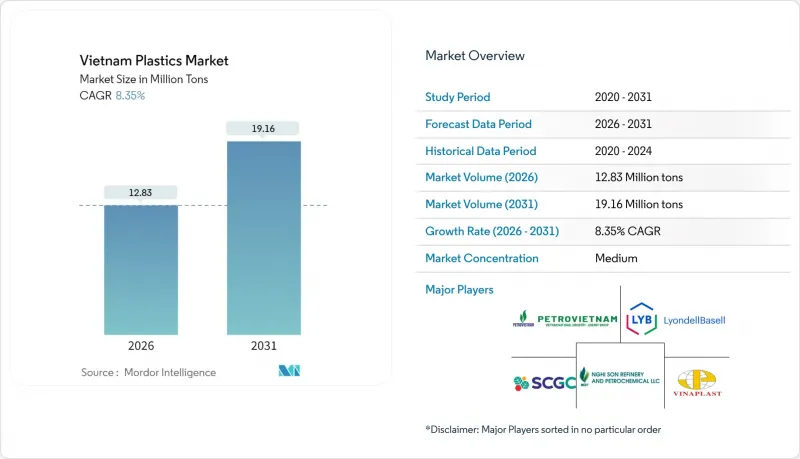

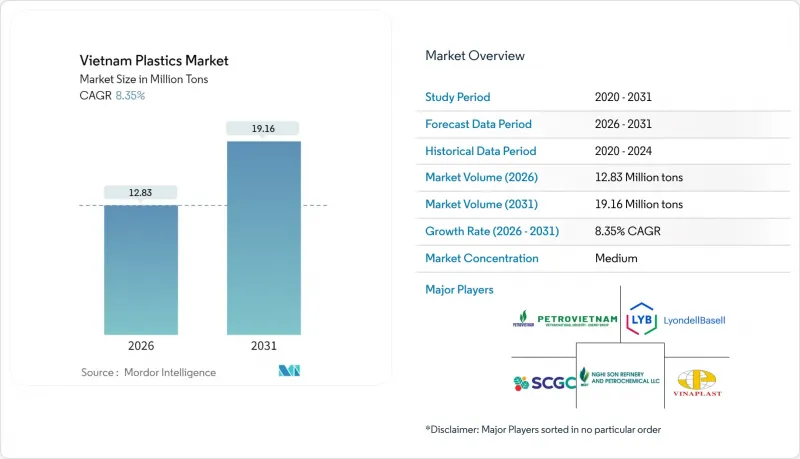

2026년 베트남 플라스틱 시장 규모는 1,283만 톤으로 추정되며, 2025년 1,184만 톤으로부터 성장이 전망됩니다. 2031년까지의 예측에서는 1,916만 톤에 달하며, 2026-2031년에 CAGR 8.35%로 확대할 전망입니다.

베트남은 탄탄한 외국인 직접 투자, 적극적인 인프라 투자, 그리고 단호한 규제 현대화가 결합되어 동남아시아에서 가장 빠르게 성장하는 플라스틱 산업의 거점으로 자리매김하고 있습니다. 중국으로부터의 제조업 이전은 다운스트림 소비를 지속적으로 확대하고 있으며, 건설 투자(2025년 상반기 전년 대비 40% 증가)는 파이프, 프로파일, 단열재에 대한 안정적인 수요를 창출하고 있습니다. 현지 가공업체들은 실험보다 생산량을 우선시하며, 급증하는 주문에 대응하기 위해 압출 라인의 규모 확대를 추진하고 있습니다. 동시에, 지속가능성에 대한 요구는 바이오플라스틱의 채택을 가속화하고 있으며, 수지 공급업체들은 원료의 다양화와 재활용 소재의 채택을 추진하고 있습니다. 그러나 수입 나프타와 프로파일렌은 여전히 비용에 민감한 원료입니다.

베트남 플라스틱 시장 동향 및 전망

국내 건설 프로젝트의 견고한 성장

인프라 지출은 자금 집행 기간이 몇 주에서 1-3일로 단축됨에 따라 2025년 상반기에 전년 대비 40% 증가했습니다. PVC 파이프, 단열 보드, 난연 케이블 트레이에 대한 수요가 급증하고 있으며, 이는 베트남이 싱가포르보다 60-65% 낮은 비용 경쟁력을 갖춘 건설 거점임을 반영하고 있습니다. 공장 건설보다 데이터센터 프로젝트가 증가함에 따라 무할로겐 화합물 및 내열성 엔지니어링 수지에 대한 수요가 증가하고 있습니다. 통첩 10/2024/TT-BXD에 따라 수입 건축자재에 대한 품질검사가 의무화되어 적합성을 증명할 수 있는 현지 컨버터에게 유리한 정책으로 바뀌었습니다. 이러한 추세는 베트남 플라스틱 시장에 수량과 금액 모두에서 성장을 가져오고 있습니다.

식품 등급 및 E-Commerce 포장 수요의 급격한 확대

2024년 베트남의 식품 가공 생산액은 793억 달러(전년 대비 7.4% 증가)에 달할 것이며, 도시 지역에서는 E-Commerce의 보급이 급속히 확대될 것입니다. 이에 따라 가공업체는 보관 기간을 연장하는 배리어 필름과 운송 비용을 절감하는 경량 우편봉투라는 두 가지 요구를 동시에 충족시켜야 합니다. 전자기기용 보호 완충재(2025년 3월까지 부품 수입량 29.3% 증가)는 완충용 폼과 성형 인서트 수요를 더욱 증가시키고 있습니다. 국내 제조 포장재에 대한 정부의 우대 정책은 국내 공급업체에 대한 조달을 유도하고, 인쇄, 라미네이팅, 다층 압출 라인에 대한 설비투자를 촉진하는 효과를 가져왔습니다.

수입 나프타-프로파일렌에 대한 높은 의존도

베트남은 2025년 1-7월 기간 중 550만 톤 이상의 플라스틱 원료를 수입했으며, 대부분 중국, 한국, 대만에서 수입했습니다. SCG의 론슨 콤플렉스는 2025년 8월에 가동을 시작해 140만 톤의 생산능력을 갖췄지만, 아직 국내 수요의 일부만 충족할 수 있는 수준입니다. 원재료비는 생산원가의 60-70%를 차지하며, 유가 변동에 따라 계속 영향을 받기 때문에 유가가 급등하면 가격 경쟁력이 약화됩니다. 계획 중인 7억 달러 규모의 에탄 업그레이드를 통해 격차는 줄어들 것으로 예상되지만, 가스 우위를 점하고 있는 걸프만 생산자와의 가격 경쟁력 확보는 여전히 어려운 상황입니다.

부문 분석

2025년 기준, 베트남 플라스틱 시장에서 기존형 플라스틱의 점유율은 51.10%를 유지할 것으로 예측됩니다. 일상적인 포장재, 파이프, 성형 부품에 사용되는 폴리에틸렌 및 폴리프로필렌 등급이 핵심입니다. 이들 제품은 성숙한 공급망과 낮은 단가의 이점을 활용하여 지속적인 물량 우위를 확보하고 있습니다. 폴리카보네이트와 폴리아미드를 포함한 엔지니어링 플라스틱은 고휘도 OLED(유기발광다이오드) 디스플레이와 광학 모듈을 운반하는 전자기기 라인에서 수요가 증가하고 있습니다. 폴리우레탄은 건설 붐에 힘입어 샌드위치 패널과 가구용 쿠션재로 활용되고 있습니다.

바이오플라스틱은 여전히 틈새 시장이지만, 브랜드 소유주가 지속가능성 목표를 추구하고 새로운 규제로 인해 수요가 증가함에 따라 2031년까지 연평균 12.55%의 성장률을 보일 것으로 예측됩니다. 농업잔재물은 잠재적인 전분 원료를 공급하지만, 인증 장벽과 프리미엄 가격 설정으로 인해 규모 확대가 여전히 어렵습니다. 그러나 국제적인 의류 그룹이 주도하는 파일럿 프로그램은 베트남이 미래의 바이오폴리머 생산 기지가 될 가능성을 보여줌으로써 2027년 이후 전환점을 시사하고 있습니다.

베트남 플라스틱 시장 보고서는 유형별(기존형 플라스틱, 엔지니어링 플라스틱, 바이오플라스틱), 기술별(블로우 성형, 압출 성형, 사출성형, 기타 기술), 용도별(포장, 전기 및 전자기기, 건축 및 건설, 자동차-운송기기, 생활용품, 가구-침구, 기타 용도)로 분류됩니다. 용도)로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05Vietnam Plastics Market size in 2026 is estimated at 12.83 million tons, growing from 2025 value of 11.84 million tons with 2031 projections showing 19.16 million tons, growing at 8.35% CAGR over 2026-2031.

Robust foreign direct investment, aggressive infrastructure outlays, and decisive regulatory modernization converge to position Vietnam as Southeast Asia's fastest-growing plastics hub. Manufacturing relocation from China continues to swell downstream consumption, while construction investments-up 40% year over year in H1 2025-channel steady demand for pipes, profiles, and insulation materials. Local converters prioritize throughput over experimentation, scaling extrusion lines to meet surging orders. Simultaneously, sustainability mandates accelerate bioplastics adoption, nudging resin suppliers to diversify feedstocks and recycle content even as imported naphtha and propylene remain cost-sensitive inputs.

Vietnam Plastics Market Trends and Insights

Robust Growth in Domestic Construction Projects

Infrastructure spending climbed 40% year over year in H1 2025 after disbursement timelines were cut from weeks to 1-3 days. Demand for PVC pipes, insulation boards, and flame-retardant cable trays has soared, reflecting Vietnam's status as a cost-competitive construction center with costs still 60%-65% below Singapore levels. Data center projects outpace factory builds, elevating requirements for halogen-free compounds and heat-resistant engineered resins. Circular 10/2024/TT-BXD mandates quality checks on imported building materials, a policy that favors local converters able to document compliance. Together, these trends funnel volume and value growth into the Vietnam plastics market.

Booming Food-grade & E-commerce Packaging Demand

Vietnam's food processing output reached USD 79.3 billion in 2024, up 7.4%, just as e-commerce adoption leapt across urban centers. As a result, converters face parallel requirements for barrier films that prolong shelf life and lightweight mailers that cut shipping costs. Protective cushioning for electronics-imports of components rose 29.3% through March 2025-adds further pull for cushioning foams and molded inserts. Government preference programs that spotlight locally made packaging tilt procurement toward domestic suppliers, encouraging capital upgrades in printing, lamination, and multilayer extrusion lines.

Heavy Dependence on Imported Naphtha and Propylene

Vietnam imported more than 5.5 million tons of plastic feedstock in the first 7 months of 2025, largely from China, South Korea, and Taiwan. SCG's Long Son complex came online in August 2025 with a 1.4 million tons capacity, yet it still covers only a slice of domestic demand. Feedstock expenses, 60%-70% of output cost, remain tethered to global oil swings, eroding price competitiveness when crude spikes. Planned ethane upgrades worth USD 700 million will narrow the gap, but cost parity with gas-advantaged Gulf producers remains elusive.

Other drivers and restraints analyzed in the detailed report include:

- Rising Foreign Direct Investment in Downstream Resin Conversion

- Surge in Automotive & Electronics Relocation to Vietnam

- Escalating Environmental Activism Against Single-use Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional plastics retained 51.10% of the Vietnam Plastics market share in 2025, anchored by polyethylene and polypropylene grades used in everyday packaging, pipes, and molded parts. These products benefit from mature supply chains and low unit costs, ensuring continued volume leadership. Engineering plastics, including polycarbonate and polyamide, are gaining traction in electronics lines that ship high-brightness OLED(Organic Light Emitting Diode) displays and optical modules. Polyurethanes ride the construction boom, serving sandwich panels and furniture cushioning.

Bioplastics, though still a niche, are set to grow at a 12.55% CAGR through 2031 as brand owners chase sustainability targets and new regulations unlock demand. Agricultural residues supply potential starch inputs, yet scaling remains hindered by certification hurdles and premium pricing. Still, pilot programs led by international apparel groups showcase Vietnam as a future biopolymer production site, signaling a possible inflection after 2027.

The Vietnam Plastics Market Report is Segmented by Type (Traditional Plastics, Engineering Plastics, and Bioplastics), Technology (Blow Molding, Extrusion, Injection Molding, and Other Technologies), Application (Packaging, Electrical and Electronics, Building and Construction, Automotive and Transportation, Housewares, Furniture and Bedding, and Other Applications). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- AGC Inc.

- Billion Industrial Holding Limited

- Far Eastern New Century Corporation

- Hyosung Chemical

- LyondellBasell Industries Holdings B.V.

- NAN YA PLASTICS CORPORATION

- NSRP LLC

- SCG Chemicals Public Company Limited

- SKC

- Toray Industries Inc.

- Vietnam Oil and Gas Group

- Vietnam Polystyrene Co. Ltd

- Vinaplast

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust Growth in Domestic Construction Projects

- 4.2.2 Booming Food-grade & E-commerce Packaging Demand

- 4.2.3 Rising Foreign Direct Investment in Downstream Resin Conversion

- 4.2.4 Surge in Automotive & Electronics Relocation to Vietnam

- 4.2.5 Government Incentives for Recycled-content Resins

- 4.3 Market Restraints

- 4.3.1 Heavy Dependence on Imported Naphtha and Propylene

- 4.3.2 Escalating Environmental Activism Against Single-use Plastics

- 4.3.3 Rising Competition from Bio-based Substitutes in FMCG

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products & Services

- 4.5.5 Degree of Competition

- 4.6 Raw Material Analysis

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Traditional Plastics

- 5.1.1.1 Polyethylene

- 5.1.1.2 Polypropylene

- 5.1.1.3 Polystyrene

- 5.1.1.4 Poly Vinyl Chloride

- 5.1.2 Engineering Plastics

- 5.1.2.1 Polyurethanes

- 5.1.2.2 Fluoropolymers

- 5.1.2.3 Polyamides

- 5.1.2.4 Polycarbonates

- 5.1.2.5 Styrene Copolymers (ABS and SAN)

- 5.1.2.6 Thermoplastic Polyesters

- 5.1.2.7 Other Engineering Plastics

- 5.1.3 Bioplastics

- 5.1.1 Traditional Plastics

- 5.2 By Technology

- 5.2.1 Blow Molding

- 5.2.2 Extrusion

- 5.2.3 Injection Molding

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Electrical and Electronics

- 5.3.3 Building and Construction

- 5.3.4 Automotive and Transportation

- 5.3.5 Housewares

- 5.3.6 Furniture and Bedding

- 5.3.7 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 Billion Industrial Holding Limited

- 6.4.3 Far Eastern New Century Corporation

- 6.4.4 Hyosung Chemical

- 6.4.5 LyondellBasell Industries Holdings B.V.

- 6.4.6 NAN YA PLASTICS CORPORATION

- 6.4.7 NSRP LLC

- 6.4.8 SCG Chemicals Public Company Limited

- 6.4.9 SKC

- 6.4.10 Toray Industries Inc.

- 6.4.11 Vietnam Oil and Gas Group

- 6.4.12 Vietnam Polystyrene Co. Ltd

- 6.4.13 Vinaplast

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment