|

시장보고서

상품코드

1939093

음향 센서 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Acoustic Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

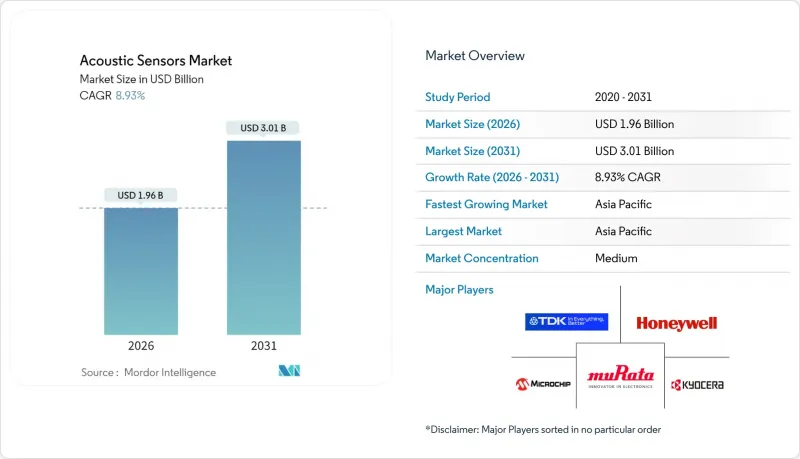

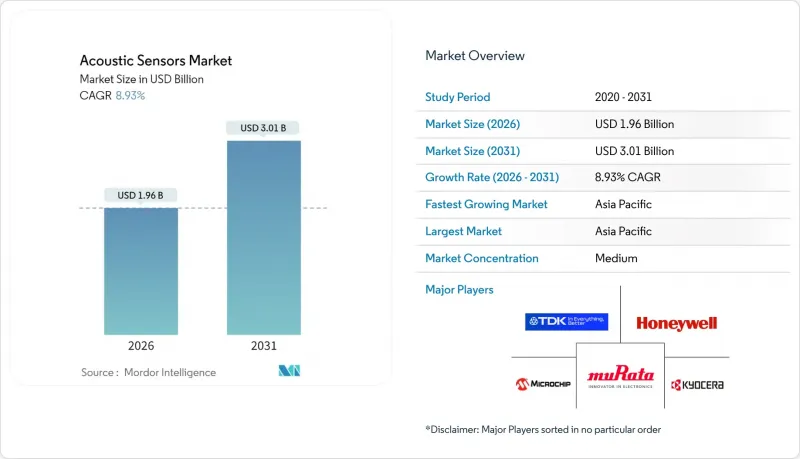

음향 센서 시장 규모는 2026년에는 19억 6,000만 달러로 추정되며, 2025년 18억 달러에서 성장이 전망됩니다.

2031년까지 30억 1,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 8.93%로 확대될 것으로 전망됩니다.

이러한 확대는 5G 및 Wi-Fi 7을 위한 고주파 필터 수요의 급증, 운송 분야의 전동화, 산업용 사물인터넷(IIoT)의 급속한 확산, 지속적인 소형화 노력에 의해 촉진되고 있습니다. 통신 인프라의 업그레이드가 벌크 음향파(BAW) 필터의 판매를 주도하는 한편, 표면 탄성파(SAW) 디바이스는 3GHz 미만의 애플리케이션 분야에서 성장을 유지하고 있습니다. 전기자동차(EV) 및 첨단 운전자 보조 시스템(ADAS)은 하네스 무게를 줄이고 강력한 전자기 간섭에 대한 내성을 구현하기 위해 배터리가 필요 없는 무선 센싱이 요구되고 있습니다. IIoT 사용자들은 현재 예지보전을 위해 엣지형 음향 센서를 선호하고 있으며, 인쇄 가능한 압전 필름은 구조적 건전성 모니터링 및 의료용 일회용 제품에 초저비용으로 적용될 수 있습니다. 경쟁 환경에서는 반도체 대기업의 진입으로 혁신 주기가 가속화되는 반면, 압전 기판 공급 부족과 지정학적 리스크가 공급망에 나타나고 있습니다.

세계 음향 센서 시장 동향 및 인사이트

5G 및 Wi-Fi 7 인프라의 급속한 확산으로 고주파 필터 수요 증가

5G 및 Wi-Fi 7로 업그레이드를 추진하는 통신사업자는 3GHz 이상의 주파수 대역에서 작동하는 필터가 필요합니다. 이 대역에서는 전자식 대체품이 한계에 도달하지만, SAW(표면탄성파) 소자, 특히 BAW(체적탄성파) 소자는 요구되는 가파른 롤오프 특성과 낮은 삽입손실을 실현합니다. 무라타제작소의 2024년 생산능력 증설은 6GHz 대역의 Wi-Fi 7을 지원하는 스마트폰 주문과 직접적으로 연동되어 있습니다.

자동차 전동화, 무선 센싱의 채택을 가속화하다

EV 플랫폼에서는 진동과 RF 에너지를 회수하는 가볍고 배터리가 필요 없는 센서가 선호됩니다. 콘티넨탈이 2024년에 출시한 무선 음향 타이어 공기압 장치는 ISO 26262의 기능 안전 요건을 충족하는 동시에 높은 전자기 간섭 하에서 신뢰성을 입증했습니다.

온도 드리프트 및 혹독한 환경용 패키징의 제약 조건

석영 기반 디바이스는 20-50 ppm/℃의 온도 드리프트가 발생하며, 고가의 보상 회로 또는 밀폐형 밀봉이 필수적입니다. -55℃-+125℃의 항공우주 설계에서는 상용 유닛보다 300-500% 더 높은 비용이 발생할 수 있으며, 진동 스트레스로 인해 재교정의 필요성이 높아집니다.

부문 분석

유선 장치로 인한 음향 센서 시장 규모는 2025년 11억 9,000만 달러에 달할 것으로 예상됩니다. 공정 산업에서는 안정적인 전력 공급과 데이터 전송을 위해 유선 형식이 여전히 선호되고 있습니다. 그러나 6억 1,000만 달러로 평가되는 무선 솔루션은 개조 경제성과 EV 수요로 인해 더 빠른 성장세를 보이고 있습니다. 무선 솔루션의 CAGR 10.74%는 유지보수 주기를 연장하는 에너지 수확 기술의 발전을 반영합니다. IEC 61508에 기반한 표준화와 이중화된 RF 프로토콜로 인해 미션 크리티컬 시스템에서 채택이 확대되고 있습니다.

풍력발전 분야의 설치 업체들은 센사타의 배터리 불필요 노드로 인해 10년 이상의 수명 연장을 보고하고 있습니다. 배선 비용 절감과 도입 기간 단축이 초기 장치의 높은 가격을 상쇄하고, 무선 도입은 음향 센서 시장의 주요 성장 축으로 자리매김하고 있습니다.

SAW 디바이스는 2025년 12억 4,000만 달러(음향 센서 시장 점유율 69.10%)를 차지할 것으로 예상되며, 3GHz 이하 애플리케이션과 성숙하고 경제적인 수정 가공 기술에서 우위를 점하고 있습니다. 그러나 통신 분야의 주파수 상승에 따라 3GHz 이상에서 성능 우위를 보이는 BAW에 5억 6,000만 달러의 시장 기회가 열리고 있습니다. TDK의 1억 달러 규모의 일본 국내 라인은 Wi-Fi 7 및 5G 단말기를 대상으로 하고 있으며, BAW의 두 자릿수 성장을 뒷받침하고 있습니다.

SAW는 산업 및 소비자 부문에서 폭넓은 채택을 유지하고 있지만, 물리 기반 주파수 제한으로 인해 고 대역폭 요구사항이 지배적인 분야에서는 BAW가 지속적으로 우위를 점할 수 있습니다.

지역별 분석

아시아태평양은 6억 7,000만 달러(2025년 매출의 37.20%, CAGR 9.81%)를 창출할 것으로 예상됩니다. 중국의 제조 거점 확대와 일본의 소재 기술 우위가 지역적 우위를 뒷받침하고 있습니다. 한국의 급속한 5G 보급과 EV 수출이 이 지역의 음향 센서 시장 규모를 더욱 확대.

북미는 5억 1,000만 달러로 그 뒤를 이었으며, IIoT(산업용 IoT) 개조와 항공우주 분야의 엄격한 신뢰성 요구사항에 힘입어 그 뒤를 이었습니다. 극초음속 항공기 감시를 지원하는 연방정부 프로그램이 국방 분야 도입에 박차를 가하고 있습니다. 유럽은 4억 3,000만 달러로, 지속가능성과 근로자 안전을 중시하는 EV 의무화 규제와 인프라 모니터링 규제의 혜택을 받고 있습니다.

중동, 아프리카 및 남미는 아직 개발 중이지만, 무선 및 배터리 불필요 노드가 원격지 및 위험 지역에 적합한 석유 및 가스, 광업, 스마트 시티 프로젝트에서 시범 도입이 진행되고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09Acoustic sensor market size in 2026 is estimated at USD 1.96 billion, growing from 2025 value of USD 1.8 billion with 2031 projections showing USD 3.01 billion, growing at 8.93% CAGR over 2026-2031.

The expansion is fueled by soaring high-frequency filtering demand for 5G and Wi-Fi 7, electrification in transportation, rapid industrial Internet of Things (IIoT) adoption, and continuing miniaturization initiatives. Telecommunications infrastructure upgrades are propelling bulk acoustic wave (BAW) filter sales, while surface acoustic wave (SAW) devices sustain growth in sub-3 GHz applications. Electric vehicles (EVs) and advanced driver assistance systems (ADAS) require battery-free wireless sensing to cut harness weight and withstand strong electromagnetic interference. IIoT users now favor edge-enabled acoustic sensors for predictive maintenance, and printed piezoelectric films promise ultra-low-cost deployments across structural health and medical disposables. Competitive dynamics reflect semiconductor majors entering the space, intensifying innovation cycles but exposing the supply chain to piezoelectric substrate shortages and geopolitical risks.

Global Acoustic Sensors Market Trends and Insights

Rapid 5G and Wi-Fi 7 Infrastructure Driving High-Frequency Filter Demand

Telecommunications providers upgrading to 5G and Wi-Fi 7 need filters operating above 3 GHz, a range where electronic alternatives falter. SAW and especially BAW devices deliver the required steep roll-off and low insertion loss. Murata's 2024 capacity expansion directly aligns with smartphone orders targeting the 6 GHz Wi-Fi 7 band.

Automotive Electrification Accelerating Wireless Sensing Adoption

EV platforms favor lightweight, battery-free sensors that harvest vibration or RF energy. Continental's 2024 launch of wireless acoustic tire-pressure units illustrates reliability under high electromagnetic interference while meeting ISO 26262 functional-safety demands.

Temperature Drift and Harsh-Environment Packaging Limitations

Quartz-based devices drift 20-50 ppm / °C, forcing costly compensation or hermetic sealing. Aerospace designs spanning -55 °C to +125 °C may cost 300-500% more than commercial units, and vibration stresses accelerate recalibration needs.

Other drivers and restraints analyzed in the detailed report include:

- Growth of IIoT and Predictive-Maintenance Programs

- Printed and Flexible Piezoelectric Films Enabling Ultra-Low-Cost Sensing

- Semiconductor Supply-Chain Volatility Impacting Material Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The acoustic sensor market size attributed to wired devices reached USD 1.19 billion in 2025. Wired formats remain favored for reliable power and data in process industries. However, wireless solutions, valued at USD 0.61 billion, are growing faster due to retrofit economics and EV demand. Wireless solutions' 10.74% CAGR reflects energy-harvesting breakthroughs that extend maintenance intervals. Standardization under IEC 61508 and redundant RF protocols improves acceptance in mission-critical systems.

Installers in wind energy report service-life gains exceeding 10 years from Sensata's battery-free nodes. Lower cabling costs and accelerated deployment offset initial device premiums, positioning wireless deployments as a primary growth vector in the acoustic sensor market.

SAW devices contributed USD 1.24 billion, equal to 69.10% acoustic sensor market share in 2025, favored for sub-3 GHz applications and mature, economical quartz processing. Yet ascending frequencies in telecom open USD 0.56 billion BAW opportunities with performance advantages above 3 GHz. TDK's USD 100 million Japanese line targets Wi-Fi 7 and 5G handsets, validating BAW's double-digit expansion.

While SAW maintains broad adoption across industrial and consumer segments, physics-based frequency ceilings ensure BAW's sustained outperformance wherever high-band requirements dominate.

The Acoustic Sensor Market Report is Segmented by Type (Wired, Wireless), Wave Type (Surface Acoustic Wave, Bulk Acoustic Wave), Sensing Parameter (Temperature, Pressure, Torque, Humidity, Mass, Viscosity), Application (Automotive, Aerospace and Defense, Consumer Electronics, Healthcare, Industrial, Environmental Monitoring, Other Applications), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific provided USD 0.67 billion, commanding 37.20% 2025 revenue and pacing at 9.81% CAGR. China's fab expansions and Japan's materials leadership buttress regional advantages. South Korea's rapid 5G roll-out and EV exports further enlarge the regional acoustic sensor market size.

North America followed with USD 0.51 billion, sustained by IIoT retrofits and stringent aerospace reliability requirements. Federal programs funding hypersonic vehicle monitoring accelerate defense uptake. Europe delivered USD 0.43 billion, benefiting from EV mandates and infrastructure monitoring regulations emphasizing sustainability and worker safety.

Middle East and Africa and South America remain nascent yet attract pilot deployments for oil-and-gas, mining, and smart-city projects where wireless battery-free nodes suit remote or hazardous locales.

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- KYOCERA Corporation

- Honeywell International Inc.

- Microchip Technology Inc. (Vectron International)

- Transense Technologies plc

- Pro-micron GmbH & Co. KG

- CTS Corporation

- IFM Electronic GmbH

- Dytran Instruments, Inc.

- Campbell Scientific, Inc.

- API Technologies Corp.

- SENSeOR SAS

- CeramTec GmbH

- Boston Piezo-Optics Inc.

- Teledyne Microwave Solutions

- Raltron Electronics Corporation

- Taiyo Yuden Co., Ltd.

- AVX Corporation

- Althen GmbH Mess- und Sensortechnik

- Sensor Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 5G and Wi-Fi 7 roll-outs raising demand for high-frequency SAW/BAW filters

- 4.2.2 Automotive shift to EVs and ADAS accelerating wireless, battery-free sensor adoption

- 4.2.3 Growth of Industrial IoT and predictive-maintenance programs

- 4.2.4 Printed and flexible piezoelectric films enabling ultra-low-cost sensing surfaces

- 4.2.5 Miniaturized MEMS microphones powering voice-UI proliferation in wearables and hearables

- 4.2.6 Government regulations mandating real-time environmental and infrastructure monitoring

- 4.3 Market Restraints

- 4.3.1 Temperature-drift and packaging challenges in harsh environments

- 4.3.2 Competition from optical and capacitive alternatives in high-precision niches

- 4.3.3 Semiconductor supply-chain volatility pushing lead-times and input costs higher

- 4.3.4 Fragmented material standards hindering cross-platform interoperability

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape and Standards

- 4.6 Technological Outlook (Edge and AI analytics)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Wired

- 5.1.2 Wireless

- 5.2 By Wave Type

- 5.2.1 Surface Acoustic Wave (SAW)

- 5.2.1.1 Rayleigh Surface Wave

- 5.2.2 Bulk Acoustic Wave (BAW)

- 5.2.1 Surface Acoustic Wave (SAW)

- 5.3 By Sensing Parameter

- 5.3.1 Temperature

- 5.3.2 Pressure

- 5.3.3 Torque

- 5.3.4 Humidity

- 5.3.5 Mass

- 5.3.6 Viscosity

- 5.4 By Application

- 5.4.1 Automotive

- 5.4.2 Aerospace and Defense

- 5.4.3 Consumer Electronics

- 5.4.4 Healthcare

- 5.4.5 Industrial

- 5.4.6 Environmental Monitoring

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 TDK Corporation

- 6.4.3 KYOCERA Corporation

- 6.4.4 Honeywell International Inc.

- 6.4.5 Microchip Technology Inc. (Vectron International)

- 6.4.6 Transense Technologies plc

- 6.4.7 Pro-micron GmbH & Co. KG

- 6.4.8 CTS Corporation

- 6.4.9 IFM Electronic GmbH

- 6.4.10 Dytran Instruments, Inc.

- 6.4.11 Campbell Scientific, Inc.

- 6.4.12 API Technologies Corp.

- 6.4.13 SENSeOR SAS

- 6.4.14 CeramTec GmbH

- 6.4.15 Boston Piezo-Optics Inc.

- 6.4.16 Teledyne Microwave Solutions

- 6.4.17 Raltron Electronics Corporation

- 6.4.18 Taiyo Yuden Co., Ltd.

- 6.4.19 AVX Corporation

- 6.4.20 Althen GmbH Mess- und Sensortechnik

- 6.4.21 Sensor Technology Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment