|

시장보고서

상품코드

1939096

X-by-wire 시스템 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)X-by-wire System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

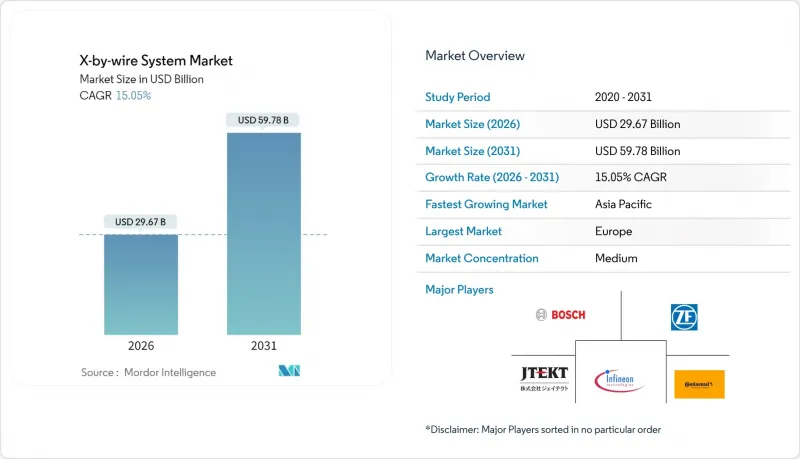

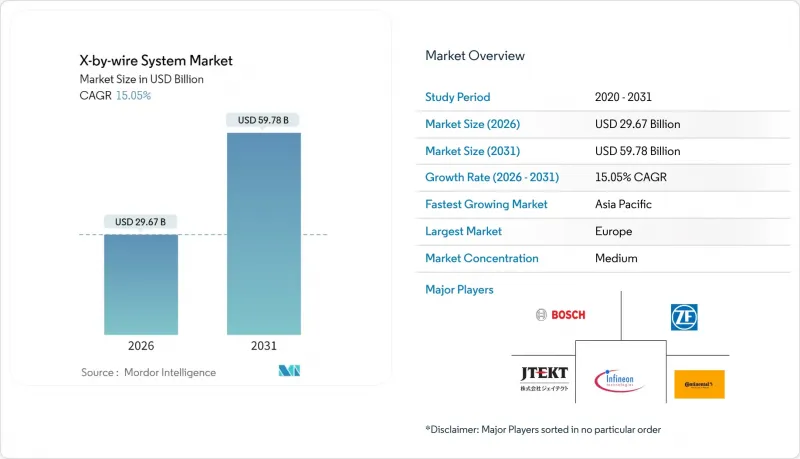

2026년 X-by-wire 시스템 시장 규모는 296억 7,000만 달러로 추정되며, 2025년 257억 9,000만 달러에서 성장하여 2031년에는 597억 8,000만 달러에 달할 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 15.05%에 달할 것으로 예상됩니다.

가속화되는 전동화 의무화, 소프트웨어 정의 차량으로의 전환, 자동 운전 요구 사항과 함께 스로틀, 브레이크, 조향, 주차, 변속 기능에서 기계식 연동 메커니즘이 프로그래밍 가능한 전자 제어로 대체되고 있습니다. 배터리 전기자동차(BEV)는 전기 인프라와 스케이트보드 플랫폼으로 물리적 배선 제약을 해소하고 무게를 줄일 수 있어 이미 도입을 주도하고 있습니다. 기계적 백업이 필요 없는 Steer-by-wire를 허용하는 개정된 ECE R 79.01과 같은 규제적 이정표로 인해 남은 승인 병목현상이 해소되고 있습니다. 조향, 제동 및 구동 시스템을 소형의 무선 조정 가능한 유닛에 통합하는 코너 모듈 아키텍처 제공 경쟁이 치열해지면서 기능 안전 및 사이버 보안 규정 준수가 여전히 장벽으로 작용하고 있습니다.

세계 X-by-wire 시스템 시장 동향 및 인사이트

첨단운전지원시스템과 자율주행 추진

자동운전 수준이 고도화됨에 따라 전자시스템만이 구현할 수 있는 즉각적이고 반복적인 제어 실행이 요구되고 있습니다. 주요 배터리 픽업 트럭에 탑재된 Steer-by-wire 시스템은 기계식 컬럼을 능가하는 성능 향상을 인정받아 저명한 기술상을 수상했습니다. 레벨 4-5 자동 운전의 계산 부하가 1,000 TOPS를 넘어 마이크로초 단위의 액추에이터 응답이 필수적입니다. 새로운 차량의 센서 제품군은 수백 개의 데이터 스트림을 수집하며, 이를 정밀한 동역학으로 변환하기 위해서는 바이와이어 인터페이스가 필요합니다. 기능 안전 및 사이버 보안 규정(ISO 26262 및 ISO/SAE 21434)은 명확한 적합성 경로를 확립하고 있지만, 개발 주기를 연장하고 있습니다.

세계 안전 규제와 CO2 규제는 전자화를 촉진합니다.

EU의 2025-2034년 평균 배출가스 규제는 사실상 전기화를 의무화하고, 에너지 관리를 최적화하는 전자 제어 서브시스템의 도입을 촉진할 것입니다. ECE R 79.01은 완전 전자식 조향 시스템을 정식으로 승인하고, 기계식 백업 요건을 폐지했습니다. 이는 규제 당국이 이중화된 전자 안전 채널을 신뢰하고 있음을 보여줍니다. 의무화된 첨단 비상 브레이크 시스템과 사각지대 모니터링 시스템도 마찬가지로 바이와이어의 정확성에 의존하고 있으며, OEM 제조업체들이 유압식 및 케이블식으로부터의 전환을 가속화하고 있습니다.

기능안전 인증의 장벽

X-by-wire 시스템에서 ISO 26262 기능 안전 인증을 획득하는 것은 복잡성을 수반하며, 상당한 시간과 비용의 장벽이 될 수 있습니다. 바이와이어 시스템에 대한 자동차 안전 무결성 수준(ASIL) 요건은 일반적으로 ASIL-C 또는 ASIL-D 평가를 요구하며, 기존 기계식 시스템에 비해 개발 기간이 18-24개월 연장될 수 있는 광범위한 검증 프로세스가 필요합니다. AI 및 머신러닝 알고리즘의 통합은 ISO PAS 8800에 기반한 추가적인 인증 과제를 수반합니다. X-by-wire 시스템의 종합적인 ASIL-D 인증을 위한 시험 및 검증 비용은 5,000만 달러가 넘을 수 있으며, 특히 중소규모의 OEM 및 Tier 1 공급업체에게는 재정적 장벽이 되고 있습니다.

부문 분석

Brake-by-wire는 2025년 X-by-wire 시스템 시장에서 39.42%의 점유율을 차지할 것으로 예상됩니다. 이는 ADAS의 제동거리 보장 및 회생 제동 최적화에 있어 이 시스템의 중요성을 반영합니다. 전기자동차의 보급 확대와 에너지 회수 전략이 전기 브레이크 작동에 의존함에 따라 브레이크 분야의 X-by-wire 시스템 시장 규모는 크게 확대될 것으로 예상됩니다. Steer-by-wire는 규제 대응과 자율주행 프로그램의 발전으로 인해 16.23%의 CAGR로 가장 빠른 성장세를 보이고 있습니다. 스로틀, 주차, 변속 등의 기능도 케이블 및 유압 시스템 교체가 꾸준히 진행되고 있지만, 상대적 가치 기여도는 여전히 낮은 수준입니다.

계약 체결 사례를 보면 규모의 경제가 분명하게 드러납니다. 북미의 한 자동차 제조사가 500만대 분량의 Brake-by-wire를 조달하고, 비용 균형을 맞추기 위해 전자식 리어 브레이크와 유압식 프론트 브레이크를 결합했습니다. Steer-by-wire 시스템 분야에서는 중국의 고급 세단이 완전 전자식 조향장치에 대한 정부 승인을 획득하여 타사가 따라올 수 있는 선례를 만들었습니다. 공급업체의 로드맵은 현재 Steer-by-wire System과 Brake-by-wire를 밀폐형 유닛에 통합하는 코너 모듈로 수렴하고 있으며, 조립 시간을 단축하고 인증 절차를 간소화하는 데 초점을 맞추고 있습니다.

2025년 X-by-wire 시스템 출하량에서 승용차가 73.65%를 차지하여 전체 경차의 수요 추세를 반영하고 있습니다. 그러나 중대형 트럭은 17.78%의 CAGR로 성장을 가속화하고 있으며, 이는 차량 전동화 의무화와 상업용 애플리케이션에서 X-by-wire 시스템의 운영상의 이점에 힘입어 성장세를 보이고 있습니다. 상용 트럭용 X-by-wire 시스템 시장 규모는 2031년까지 브레이크 회생 및 유지보수 절감에 연동된 가동 주기에 따른 투자 회수 계산을 배경으로 큰 폭의 성장이 예상됩니다.

차량 관리자들은 전자식 작동 기술로 가능한 무선 진단(OTA 진단)과 예지보전을 높이 평가하고 있습니다. 초기 파일럿에서는 Steer-by-wire 기술을 통해 트레일러의 자동 위치 결정을 실현하여 야드 내 작업 시간을 약 40% 단축했습니다. 소형 상용차(LCV)는 완만한 성장세를 보이고 있으며, 라스트 마일 배송 애플리케이션에서 통합 바이와이어 제어가 가능한 전기 플랫폼이 점점 더 선호되고 있습니다. 그 대표적인 예가 자율 배송 업무를 위해 코너 모듈 아키텍처를 채택한 REE 오토모티브의 '레오파드 EV'입니다.

지역별 분석

유럽은 엄격한 CO2 배출 목표와 종합적인 안전 규제로 인해 기존 기계식 대체품보다 전자 제어 시스템을 체계적으로 우선시하고 있어 2025년에도 35.20%의 점유율로 선두를 유지했습니다. 독일과 프랑스 자동차 제조사들은 우선 고급 전기자동차에 와이어 제어를 도입하고, 비용 곡선이 낮아지는 단계에서 대량 생산 부문으로 확대할 것입니다. 이 지역의 공급업체들은 수세기에 걸친 섀시 기술 노하우를 활용하면서 도메인 컨트롤러 소프트웨어 전문 지식으로 전환하고 있습니다. ECE R 79.01에 구현된 규제의 확실성은 기존 기업과 신규 진입 기업 모두에게 투자에 대한 확신을 주고 있습니다.

아시아태평양은 성장 동력으로 2031년까지 CAGR 18.06%를 유지할 것입니다. 중국의 급속한 BEV 보급과 Steer-by-wire 양산차의 조기 인가가 지역 도입의 청사진이 되었습니다. 이 지역은 이미 확립된 전자제품 제조 역량과 공급망을 활용하여 X 바이와이어 시스템의 복잡한 센서 액추에이터 요구사항을 경쟁력 있는 비용으로 지원합니다. 일본과 한국은 고정밀 액추에이터와 통합형 코너 모듈 시제품을 제공하고 있으며, 이들은 이미 로보택시에서 실지 테스트가 진행되고 있습니다.

북미에서는 자율주행 기술에 대한 대규모 투자와 상용차 전동화 의무화로 인해 꾸준한 성장세를 보이고 있습니다. 테슬라에 대한 브레이크 바이 와이어의 대규모 주문은 확장의 모멘텀을 보여주고 있습니다. 미국의 반도체 생산능력은 첨단 도메인 컨트롤러를 지원하며, 사이버 보안 프레임워크는 국제 ISO 표준을 준수하도록 진화하고 있습니다. 픽업 트럭과 SUV 플랫폼이 스케이트보드형 EV 아키텍처로 전환하고, 전자식 액추에이션을 위한 패키징 공간이 확보되면서 보급이 가속화되고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09X-by-wire systems market size in 2026 is estimated at USD 29.67 billion, growing from 2025 value of USD 25.79 billion with 2031 projections showing USD 59.78 billion, growing at 15.05% CAGR over 2026-2031.

Accelerated electrification mandates, the software-defined-vehicle shift, and autonomy requirements are converging to displace mechanical linkages with programmable electronic control across throttle, brake, steer, park, and shift functions. Battery-electric vehicles (BEVs) already dominate adoption because their electrical infrastructure and skateboard platforms eliminate physical routing constraints while lowering weight. Regulatory milestones, such as the revised ECE R 79.01 that now permits steer-by-wire without a mechanical backup, are removing remaining approval bottlenecks. Competitive intensity is climbing as suppliers race to deliver corner-module architectures that bundle steering, braking, and drive systems into compact, over-the-air-tunable units, while functional-safety and cybersecurity compliance remain gating factors.

Global X-by-wire System Market Trends and Insights

Advanced-driver-assistance and Autonomy Push

Growing levels of automated driving demand instantaneous, repeatable control execution that only electronic systems can provide. A steer-by-wire implementation on a leading battery pickup recently earned a high-profile technology award, highlighting the performance leap over mechanical columns. Computing loads for Level 4-5 autonomy exceed 1,000 TOPS, making micro-second-scale actuator response mandatory. Sensor suites in new vehicles now collect hundreds of data streams; translating them into precise dynamics requires by-wire interfaces. Functional-safety and cybersecurity regulations (ISO 26262 and ISO/SAE 21434) establish clear compliance paths but lengthen development cycles.

Global Safety and CO2 Rules Favour Electronics

The EU's 2025-2034 fleet-average emissions limits effectively compel electrification, and by extension, electronic control subsystems that optimize energy management. ECE R 79.01 now formally allows full electronic steering systems, eliminating the mechanical fallback requirement and signaling regulators' trust in redundant electronic safety channels. Mandated advanced emergency braking and blind-spot monitoring systems similarly rely on by-wire precision, accelerating OEM migration away from hydraulics and cables.

Functional-safety Certification Hurdles

The complexity of achieving ISO 26262 functional safety certification for X-by-wire systems presents significant time and cost barriers. Automotive Safety Integrity Level (ASIL) requirements for by-wire systems typically demand ASIL-C or ASIL-D ratings, necessitating extensive validation processes that can extend development timelines by 18-24 months compared to traditional mechanical systems. The integration of AI and machine learning algorithms introduces additional certification challenges under ISO PAS 8800. Testing and validation costs for X-by-wire systems can exceed USD 50 million for comprehensive ASIL-D certification, creating financial barriers particularly challenging for smaller OEMs and tier-1 suppliers.

Other drivers and restraints analyzed in the detailed report include:

- EV Packaging and Weight-saving Benefits

- Digital Chassis Cost-saving Platforms

- High Integration Cost for Legacy Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brake-by-wire secured a 39.42% X-by-wire systems market share in 2025, reflecting the system's centrality to ADAS stop-distance guarantees and regenerative-braking optimization. The X-by-wire systems market size for braking is projected to expand significantly as EV penetration rises and energy-recuperation strategies depend on electric brake actuation. Steer-by-wire shows the fastest upswing at 16.23% CAGR, enabled by regulatory acceptance and autonomy programs. Other functions like throttle, park, and shift continue to replace cables and hydraulics steadily, but their relative value content remains lower.

Contract awards reveal scale economies: a single North American OEM sourced brake-by-wire for 5 million units, combining electronic rear brakes with hydraulic fronts to balance cost. In steer-by-wire, a Chinese flagship sedan won government approval for full electronic steering, setting a precedent others will follow. Supplier roadmaps now converge on corner modules merging steer and brake-by-wire into sealed units, slashing assembly time and simplifying homologation.

Passenger cars represented 73.65% of the X-by-wire systems market 2025 shipments, mirroring overall light-vehicle demand. Nevertheless, medium and heavy trucks are accelerating at an 17.78% CAGR, driven by fleet electrification mandates and the operational advantages that X-by-wire systems provide in commercial applications. The X-by-wire systems market size for commercial trucks is expected to grow significantly by 2031, underpinned by duty-cycle-driven payback calculations linked to brake regeneration and reduced maintenance.

Fleet managers value over-the-air diagnostics and predictive maintenance unlocked by electronic actuation. Early pilots show steer-by-wire enabling automated trailer positioning, cutting yard maneuver time by approximately 40%. Light Commercial Vehicles experience moderate growth as last-mile delivery applications increasingly favor electric platforms with integrated by-wire controls, exemplified by REE Automotive's Leopard EV, which utilizes corner-module architecture for autonomous delivery operations.

The X-By-Wire Systems Market Report is Segmented by Type (Throttle-By-Wire, Brake-By-Wire, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component (Sensors and Pedal Modules, Actuators, and ECUs), Propulsion Type (Internal-Combustion Engine, Hybrid, and Battery-Electric), and Geography (North America, South America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retained leadership at 35.20% share in 2025 owing to stringent CO2 emission targets and comprehensive safety regulations that systematically favor electronic control systems over traditional mechanical alternatives. German and French OEMs deploy by wire on premium EVs first, then cascade to mass segments once cost curves dip. Regional suppliers exploit centuries of chassis know-how while pivoting to domain-controller software expertise. Regulatory certainty, embodied in ECE R 79.01, gives investment confidence to both incumbents and new entrants.

Asia-Pacific is the growth engine with an 18.06% CAGR through 2031. China's rapid BEV uptake and early approval of steer-by-wire production vehicles have created the blueprint for regional adoption. The area benefits from established electronics manufacturing capabilities and supply chains supporting X-by-wire systems' complex sensor and actuator requirements at competitive costs. Japan and South Korea contribute high-precision actuators and integrated corner-module prototypes that are already being field-tested on the robotaxis.

North America posts steady gains, supported by significant investments in autonomous driving technologies and commercial vehicle electrification mandates. A high-volume brake-by-wire award to Tesla underlines scaling momentum. U.S. semiconductor capacity supports advanced domain controllers, while cybersecurity frameworks evolve to align with global ISO standards. Uptake accelerates as pickup-truck and SUV platforms transition to skateboard EV architectures, freeing packaging for electronic actuation.

- Continental AG

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- JTEKT Corporation

- Nexteer Automotive

- Infineon Technologies AG

- Nissan Motor Corporation

- Tesla Inc.

- Audi AG

- Toyota Motor Corporation

- Hitachi Astemo Ltd.

- Denso Corporation

- Curtiss-Wright Corporation

- CTS Corporation

- Valeo SA

- Orscheln Products LLC

- Torc Robotics

- Jaguar Land Rover

- REE Automotive

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advanced-driver-assistance and Autonomy Push

- 4.2.2 Global Safety and CO2 Rules Favour Electronics

- 4.2.3 EV Packaging and Weight-saving Benefits

- 4.2.4 Digital Chassis Cost-saving Platforms

- 4.2.5 OTA-tunable Software-defined Chassis

- 4.2.6 Corner-module EV Skateboards for Fleets

- 4.3 Market Restraints

- 4.3.1 Functional-safety Certification Hurdles

- 4.3.2 High Integration Cost for Legacy Platforms

- 4.3.3 In-vehicle-network Cyber-security Gaps

- 4.3.4 Supply Crunch of Redundancy-grade Sensors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook - X-by-wire Control Architectures

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Type

- 5.1.1 Throttle-by-wire System

- 5.1.2 Brake-by-wire System

- 5.1.3 Steer-by-wire System

- 5.1.4 Park-by-wire System

- 5.1.5 Shift-by-wire System

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.3 By Component

- 5.3.1 Sensors and Pedal Modules

- 5.3.2 Actuators

- 5.3.3 Electronic Control Units (ECUs)

- 5.4 By Propulsion Type

- 5.4.1 Internal-Combustion Engine Vehicles

- 5.4.2 Hybrid Vehicles

- 5.4.3 Battery-Electric Vehicles

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 ZF Friedrichshafen AG

- 6.4.3 Robert Bosch GmbH

- 6.4.4 JTEKT Corporation

- 6.4.5 Nexteer Automotive

- 6.4.6 Infineon Technologies AG

- 6.4.7 Nissan Motor Corporation

- 6.4.8 Tesla Inc.

- 6.4.9 Audi AG

- 6.4.10 Toyota Motor Corporation

- 6.4.11 Hitachi Astemo Ltd.

- 6.4.12 Denso Corporation

- 6.4.13 Curtiss-Wright Corporation

- 6.4.14 CTS Corporation

- 6.4.15 Valeo SA

- 6.4.16 Orscheln Products LLC

- 6.4.17 Torc Robotics

- 6.4.18 Jaguar Land Rover

- 6.4.19 REE Automotive

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment