|

시장보고서

상품코드

1939097

아시아태평양의 열화상 시스템 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Thermal Imaging Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

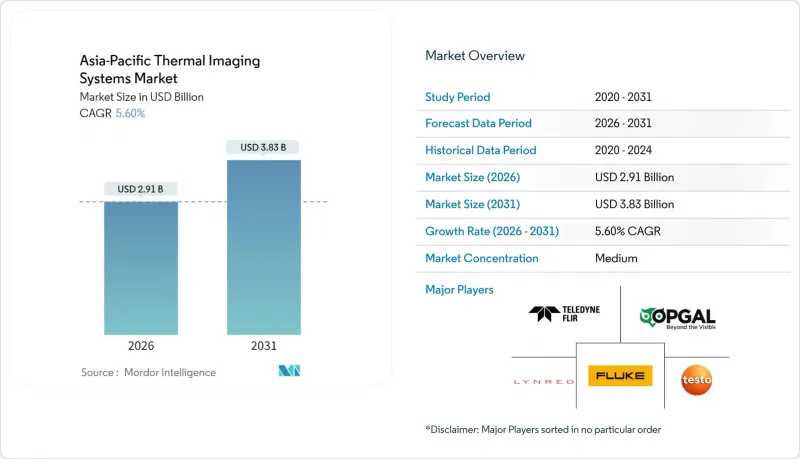

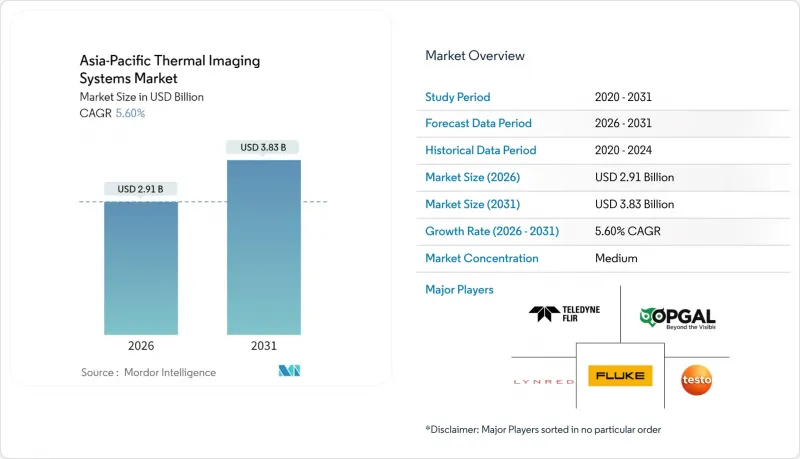

아시아태평양의 열화상 시스템 시장은 2025년 27억 6,000만 달러에서 2026년에는 29억 1,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 5.60%를 기록하며 2031년에는 38억 3,000만 달러에 달할 것으로 예측됩니다.

국방부의 국경 감시 시스템 업데이트 자금 지원, 산업체들의 예지보전 프로그램 도입, 소비자 기기에 소형 열화상 코어의 통합이 진행되면서 채택이 가속화되고 있습니다. 비냉각식 마이크로볼로미터의 가격이 연평균 15-20%씩 하락하고 있어, 건물 검사 및 스마트폰 액세서리 분야에서 중저가 시장 기회가 열리고 있습니다. 중국, 일본, 한국 정부의 축산 바이오 보안 규제와 공장 자동화의 진전으로 인해 기존 보안 구매자를 넘어 잠재 고객층이 확대되고 있습니다. 냉각식 중파 적외선 카메라의 라이선스 마찰과 웨이퍼급 VOx 소자의 공급 불안정성은 여전히 주요 비용 및 일정 리스크입니다. 개발사들은 아시아태평양 열화상 시스템 시장의 미래 성장 경로를 확보하기 위해 멀티 스펙트럼 단파 적외선 솔루션, 칼코게나이드 광학소자, 엣지 AI 분석 기술을 우선적으로 도입하고 있습니다.

아시아태평양의 열화상 시스템 시장 동향 및 인사이트

비냉각식 마이크로볼로미터 센서 비용 절감

중국 팹의 급속한 대량 생산 확대로 인해 VOx 마이크로볼로미터의 가격은 연간 15-20% 하락했고, 휴대용 열화상 장치의 소매 가격은 500달러 이하로 떨어졌습니다. 이를 통해 건설업체와 주택 검사관은 스마트폰용 열화상 애드온의 도입을 정당화할 수 있게 되었고, 중산층 시장에서의 사용자 수를 확대할 수 있게 되었습니다. 산업 전기 기술자는 고가의 고장이 발생하기 전에 배전반의 핫스팟을 감지하기 위해 핸드헬드 뷰어를 채택하여 총 소유 비용을 절감하는 효과를 누리고 있습니다. 판매량 증가는 수익률 압박을 가져오고, 벤더들은 부가가치가 높은 클라우드 소프트웨어와 분석 구독 서비스에 집중하고 있습니다. 이처럼 센싱 기술의 보급이 아시아태평양 열화상 시스템 시장의 지속적인 성장을 뒷받침하고 있습니다.

아시아태평양의 국방 및 국경 보안 비용 증가

남중국해와 히말라야 지역에서의 영토 분쟁의 긴장이 고조되는 가운데, 국방 예산은 증가 추세에 있습니다. 미국은 2016년 이후 아시아태평양의 해양 영역 인식(MDA)에 4억 7,500만 달러(약 5,000억 원)를 투자했습니다. 해안 레이더, 차량 탑재형 ISR 포드, 소형 드론의 주야간 추적이 가능한 대 UAS(무인항공기) 배터리에는 열화상 장비가 장착되어 있습니다. 호주는 적외선 장비가 장착된 P-8 포세이돈 항공기를 조달했고, 싱가포르는 항만 감시망에 열 감지 카메라를 다층적으로 배치했습니다. 조달 주기에서는 운영자의 대응을 가속화하는 AI 분류 툴을 통합하기 위한 개방형 아키텍처에 중점을 두고 있습니다. 이러한 장기 조달 파이프라인은 다년간의 납품을 보장하며, 아시아태평양의 열화상 시스템 시장을 뒷받침하고 있습니다.

냉각식 카메라의 높은 초기 비용과 수출 허가 제한 사항

ITAR 및 EAR 규정에 따라 중파장 적외선(MWIR) 시스템은 미국의 승인을 받아야 하며, 수개월에 걸친 서류 절차가 발생하여 중국 및 러시아 구매자를 제한하고 있습니다. 또한, 극저온 냉각장치는 라이프사이클 비용을 증가시켜 국방 및 연구 분야 외의 시장성을 제한하고 있습니다. 그 결과, 기관들은 종종 감지 범위가 좁아짐에도 불구하고 비냉각식 대체품으로 타협해야 하는 경우가 많아 아시아태평양의 열화상 시스템 시장의 상한선을 낮추고 있습니다.

부문 분석

열화상 카메라는 2025년 10억 2,000만 달러의 시장 규모를 형성하며 아시아태평양의 열화상 시스템 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이는 일본, 한국, 중국 연안 지역의 공장 검사 및 건물 진단이 주도하고 있습니다. UAS 프로그램은 현재 규모가 작지만, 2031년까지 CAGR 5.93%로 확대될 것으로 예상됩니다. 분쟁 지역에서 드론의 확산에 따라 국방 분석 분야에서 아시아태평양의 열화상 시스템 시장 점유율이 확대될 것으로 예상됩니다.

열화상 카메라가 선도적인 지위를 유지하고 있는 배경에는 예지보전을 통한 투자 회수가 즉각적으로 이뤄지는 점, 건축기준에서 적외선 감사가 규정되는 사례가 증가하고 있는 점을 들 수 있습니다. 소방기관에서는 연기를 투과하여 열원을 식별하는 견고한 이미저를 채택하여 산업 화재 시 대응 시간을 단축하고 있습니다. 해상-연안 감시 시스템은 레이더에 열화상 이미지를 중첩하여 24시간 365일 상황 인식을 실현하고, 해군이 불법 조업과 밀수를 차단할 수 있도록 지원하고 있습니다. NEC의 산불 감지 그리드는 태풍 다발 지역인 일본에서 열화상 기술이 재해 대책에 얼마나 중요한지 보여주고 있습니다. 의료 및 수색 구조팀은 시야가 좋지 않을 때 생존자 위치 파악을 위해 드론 탑재 시스템을 채택하고 있으며, 이는 사용 사례를 더욱 확대하여 아시아태평양의 열화상 시스템 시장 성장을 뒷받침하고 있습니다.

2025년에도 열화상 카메라는 매출의 54.10%를 차지했지만, 모듈 출하량은 2031년까지 6.22%의 가장 높은 CAGR을 기록할 것으로 예상되며, OEM 제조업체의 전환으로 아시아태평양의 열화상 시스템 시장 규모에서 모듈 점유율이 확대될 것으로 예상됩니다. 모듈 점유율이 확대되고 있음을 보여줍니다. 스마트폰용 어태치먼트 키트나 자동차용 야간투시 패키지에서는 광학 어셈블리를 추가하지 않고 기존 기판에 통합할 수 있는 모듈을 선호하여 설계의 유연성을 높이고 있습니다.

산업 및 공공안전 프로젝트에서는 견고한 인클로저, 분석 기능 및 네트워크가 통합된 완제품 카메라가 여전히 주류를 이루고 있습니다. 그러나 Teledyne FLIR의 Hadron X는 250g 미만의 드론 프레임에 대응하여 소형화가 양산 고객을 끌어들이는 사례를 보여주고 있습니다. 모듈 벤더들은 열화상 카메라에 익숙하지 않은 통합업체를 위해 시장 출시 시간을 단축하기 위해 SDK와 AI 가속화를 번들로 제공하고 있습니다. 따라서 모듈 보급률 증가는 수익원 다각화를 가져오고, 아시아태평양의 열화상 시스템 시장에서 OEM과의 협력을 강화할 수 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The Asia-Pacific thermal imaging systems market is expected to grow from USD 2.76 billion in 2025 to USD 2.91 billion in 2026 and is forecast to reach USD 3.83 billion by 2031 at 5.60% CAGR over 2026-2031.

Adoption accelerates as defense ministries fund border-surveillance upgrades, industrial firms deploy predictive-maintenance programs, and consumer devices integrate compact thermal cores. Declining uncooled micro-bolometer prices, averaging 15-20% annual reductions, open mid-tier opportunities in building inspection and smartphone accessories. Government livestock bio-security mandates and rising factory automation in China, Japan, and South Korea broaden the addressable base beyond traditional security buyers. Export-licensing friction for cooled MWIR cameras and wafer-grade VOx supply fragility remain primary cost and schedule risks. Developers are therefore prioritizing multispectral SWIR solutions, chalcogenide optics, and edge-AI analytics to safeguard future growth paths in the Asia-Pacific thermal imaging systems market.

Asia-Pacific Thermal Imaging Systems Market Trends and Insights

Declining Cost of Uncooled Micro-Bolometer Sensors

Rapid scale-up at Chinese fabs brought 15-20% annual price declines in VOx micro-bolometers, pulling portable thermal devices below USD 500 retail. Builders and home inspectors can now justify thermal add-ons for smartphones, expanding user counts in middle-income markets. Industrial electricians adopt handheld viewers to spot hot spots in switchgear before costly failures, benefiting from lower total cost of ownership. Volume gains widen though margins compress, pushing vendors toward value-added cloud software and analytics subscriptions. The democratization of sensing thus underpins a durable upswing in the Asia-Pacific thermal imaging systems market.

Rising Defense and Border-Security Spending in APAC

Territorial tensions in the South China Sea and along the Himalayas keep defense budgets rising, with USD 475 million earmarked by the U.S. for APAC maritime domain awareness since 2016. Thermal imagers equip coastal radars, vehicle-mounted ISR pods, and counter-UAS batteries capable of tracking small drones day and night. Australia procures thermal-equipped P-8 Poseidon aircraft, while Singapore layers heat-sensing cameras onto harbor surveillance grids. Procurement cycles emphasize open architectures to insert AI classification tools that accelerate operator response. Long-lead acquisition pipelines thus assure multi-year deliveries that buoy the Asia-Pacific thermal imaging systems market.

High Upfront Cost and Export-Licence Constraints for Cooled Cameras

ITAR and EAR regulations mandate U.S. sign-off for MWIR systems, adding months of paperwork and constraining Chinese and Russian buyers. Cryogenic coolers also lift lifetime costs, limiting marketability outside defense and research. Consequently, agencies often settle for uncooled alternatives despite reduced range, trimming the ceiling of the Asia-Pacific thermal imaging systems market.

Other drivers and restraints analyzed in the detailed report include:

- Industrial Predictive-Maintenance Adoption

- Smartphone, Drone and ADAS Integration of Thermal Cores

- Semiconductor-Grade VOx / InSb Wafer Supply Fragility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermography generated USD 1.02 billion in 2025, the single largest slice of the Asia-Pacific thermal imaging systems market size, anchored by factory inspection and building diagnostics in Japan, South Korea, and coastal China. Counter-UAS programs, though smaller today, are projected to log a 5.93% CAGR to 2031, expanding the Asia-Pacific thermal imaging systems market share for defense analytics as drones proliferate across contested borders.

Thermography retains leadership because predictive-maintenance ROI is immediate, and building codes increasingly specify infrared audits. Firefighting agencies employ rugged imagers that penetrate smoke and pinpoint hot spots, reducing response times during industrial blazes. Maritime and coastal surveillance packages layer thermal onto radars for 24/7 situational awareness, helping navies deter illegal fishing and smuggling. NEC's forest-fire detection grids illustrate thermal's value in disaster preparedness across typhoon-prone Japan. Medical and search-and-rescue teams adopt drone-mounted systems to locate survivors in low-visibility conditions, further broadening use cases and supporting growth within the Asia-Pacific thermal imaging systems market.

Thermal cameras continued to capture 54.10% of revenue in 2025, yet module shipments are on track for the strongest 6.22% CAGR through 2031, highlighting an OEM pivot that elevates module share of the Asia-Pacific thermal imaging systems market size. Smartphone attach-kits and automotive night-vision packages prefer modules that slot into existing boards without adding optical assemblies, boosting design flexibility.

Complete cameras still anchor industrial and public-safety projects where rugged housings, analytics, and networking come pre-integrated. Nonetheless, Teledyne FLIR's Hadron X aligns with drone frames weighing under 250 g, showing how miniaturization attracts volume customers. Module vendors bundle SDKs and AI acceleration to reduce time-to-market for integrators unfamiliar with thermography. Rising module penetration, therefore, diversifies revenue streams and cements OEM ties inside the Asia-Pacific thermal imaging systems market.

The Asia-Pacific Thermal Imaging Systems Market Report is Segmented by Application (Thermography, Maritime and Coastal Surveillance, and More), Product (Thermal Cameras, Thermal Scopes/Sights, and More), Technology (Uncooled LWIR, and More), End-User Vertical (Aerospace and Defence, Law-Enforcement and Public Safety, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Teledyne FLIR LLC

- Wuhan Guide Infrared Co., Ltd.

- Lynred

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Fluke Corporation

- Opgal Optronic Industries Ltd.

- Testo SE and Co. KGaA

- Trijicon, Inc.

- Dongguan Xintai Instrument Co., Ltd.

- Thermoteknix Systems Ltd.

- Raytron Technology Co., Ltd.

- Zhejiang Dali Technology Co., Ltd.

- Meridian Innovation Ltd.

- Nippon Avionics Co., Ltd.

- NEC Avio Infrared Technologies Co., Ltd.

- Shenzhen SAT Infrared Technology Co., Ltd.

- Leonardo S.p.A.

- L3Harris Technologies, Inc.

- BAE Systems plc

- Axis Communications AB

- Seek Thermal, Inc.

- InfraTec GmbH

- Infrared Cameras Inc.

- Tien-Yuan Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining cost of uncooled micro-bolometer sensors

- 4.2.2 Rising defence and border-security spending in Asia-Pacific

- 4.2.3 Industrial predictive-maintenance adoption

- 4.2.4 Smartphone, drone and ADAS integration of thermal cores

- 4.2.5 Livestock bio-security mandates using AI-thermal analytics

- 4.2.6 Chalcogenide optics easing germanium supply risk

- 4.3 Market Restraints

- 4.3.1 High upfront cost and export-licence constraints for cooled cameras

- 4.3.2 Scarcity of certified thermography service providers

- 4.3.3 Semiconductor-grade VOx / InSb wafer supply fragility

- 4.3.4 Smart-city privacy rules limiting thermal surveillance

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Thermography

- 5.1.2 Maritime and Coastal Surveillance

- 5.1.3 Border Surveillance

- 5.1.4 Counter-UAS / Drones

- 5.1.5 Critical Infrastructure Security

- 5.1.6 Others (Fire-fighting, Smartphones, Medical, PVS)

- 5.2 By Product

- 5.2.1 Thermal Cameras

- 5.2.2 Thermal Scopes / Sights

- 5.2.3 Thermal Modules / Cores

- 5.3 By Technology

- 5.3.1 Uncooled LWIR (VOx / a-Si)

- 5.3.2 Cooled MWIR and LWIR (InSb, MCT)

- 5.3.3 SWIR and Multispectral

- 5.4 By End-User Vertical

- 5.4.1 Aerospace and Defence

- 5.4.2 Law-Enforcement and Public Safety

- 5.4.3 Healthcare and Veterinary

- 5.4.4 Automotive and Mobility

- 5.4.5 Oil and Gas and Process Industries

- 5.4.6 Manufacturing and Utilities

- 5.4.7 Other End-User Verticals

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Southeast Asia

- 5.5.5 South Korea

- 5.5.6 Australia and New Zealand

- 5.5.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Teledyne FLIR LLC

- 6.4.2 Wuhan Guide Infrared Co., Ltd.

- 6.4.3 Lynred

- 6.4.4 Hangzhou Hikvision Digital Technology Co., Ltd.

- 6.4.5 Fluke Corporation

- 6.4.6 Opgal Optronic Industries Ltd.

- 6.4.7 Testo SE and Co. KGaA

- 6.4.8 Trijicon, Inc.

- 6.4.9 Dongguan Xintai Instrument Co., Ltd.

- 6.4.10 Thermoteknix Systems Ltd.

- 6.4.11 Raytron Technology Co., Ltd.

- 6.4.12 Zhejiang Dali Technology Co., Ltd.

- 6.4.13 Meridian Innovation Ltd.

- 6.4.14 Nippon Avionics Co., Ltd.

- 6.4.15 NEC Avio Infrared Technologies Co., Ltd.

- 6.4.16 Shenzhen SAT Infrared Technology Co., Ltd.

- 6.4.17 Leonardo S.p.A.

- 6.4.18 L3Harris Technologies, Inc.

- 6.4.19 BAE Systems plc

- 6.4.20 Axis Communications AB

- 6.4.21 Seek Thermal, Inc.

- 6.4.22 InfraTec GmbH

- 6.4.23 Infrared Cameras Inc.

- 6.4.24 Tien-Yuan Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment