|

시장보고서

상품코드

1939098

블루투스 스피커 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Bluetooth Speaker - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

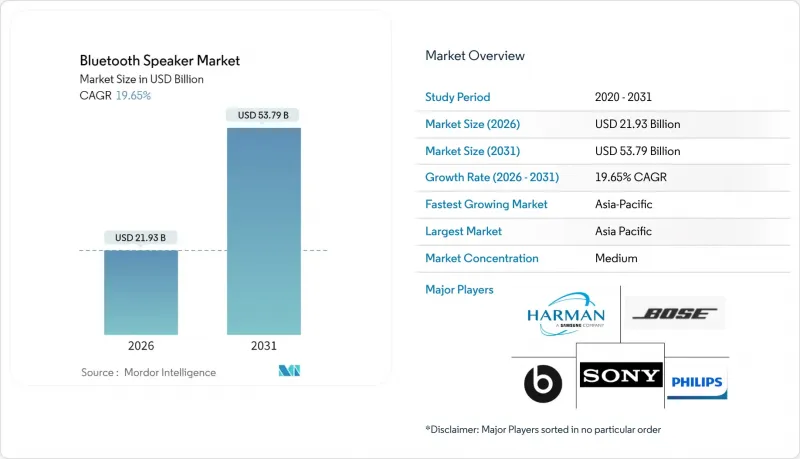

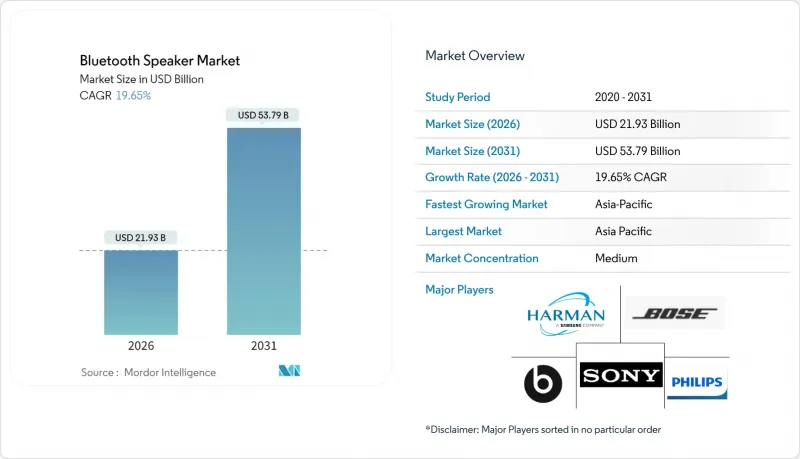

블루투스 스피커 시장은 2025년에 183억 2,000만 달러로 평가되며, 2026년 219억 3,000만 달러에서 2031년까지 537억 9,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2031년)의 CAGR은 19.65%로 전망됩니다.

견고한 수요는 스마트홈의 보급, 음악 스트리밍의 대중화, 배터리 비용의 하락, Bluetooth LE Audio의 상용화에 기인하며, 각각 대상 사용자층을 확대하는 동시에 교체 주기를 단축시키고 있습니다. 아시아태평양은 경쟁력 있는 제조거점과 빠르게 성장하는 중산층으로 인해 현재 판매량을 주도하고 있습니다. 반면 북미와 유럽은 스마트홈의 조기 보급을 배경으로 프리미엄 평균판매가격(ASP)을 실현하고 있습니다. 음성 비서 지원 모델은 가장 빠르게 성장하는 카테고리이지만, 블루투스 전용 스피커는 Wi-Fi에 의존하지 않는 단순하고 지연이 적은 경험을 제공하므로 여전히 가장 큰 하위 부문을 차지하고 있습니다. 경쟁 환경은 통합으로 전환되고 있으며, 기존 브랜드가 특허 기술과 브랜드 가치를 확보하기 위해 고급 오디오 제조업체를 인수하고 있으며, 이로 인해 상품 기업의 진입장벽이 높아지고 있습니다.

세계 블루투스 스피커 시장 동향 및 인사이트

스마트홈 생태계의 급속한 확산

Matter 표준을 통한 원활한 상호운용성을 통해 블루투스 스피커는 단일 엔터테인먼트 기기에서 다기능 스마트홈 허브로 진화하고 있습니다. 아마존의 2025년형 에코 쇼(Echo Show) 시리즈는 Fire TV 서비스 내장, 자동 프레이밍 기능을 갖춘 비디오 통신, 그리고 Matter, Zigbee, Thread에 대한 완벽한 지원을 단일 장치에 통합함으로써 이러한 변화를 구현하고 있습니다. 브랜드 간 호환성 향상으로 전환 비용이 절감되고, 음성 인식 스피커를 통해 조명, 공조, 보안 제어를 통합하는 가정에서는 프리미엄 제품 교체 수요가 촉진될 것입니다. LegatoXP와 같은 중국 ODM 플랫폼은 제품 개발 주기를 단축하고, 중견 브랜드가 제한된 기술 예산으로 스마트홈 시장에 진입할 수 있도록 지원합니다. 이러한 요인들이 결합되어 가정용 보급이 가속화되고 브랜드 경쟁이 치열해지면서 블루투스 스피커 시장의 총 수요가 확대될 것입니다.

음악 스트리밍 서비스 확대

음악 스트리밍 서비스 유료 가입자 수는 2024년 7억 5,000만 명을 돌파할 것으로 예상되며, 고해상도 및 공간 오디오 재생 지원하드웨어에 대한 수요가 증가하고 있습니다. LC3, LDAC, aptX Lossless 등 코덱 기술이 성숙해짐에 따라 사용자들은 기존 장치와 차세대 스피커의 청각적 품질 차이를 인식하고 교체 수요를 불러일으키고 있습니다. 구독 플랫폼에서는 그룹 청취를 기본적으로 지원하는 멀티 디바이스 플랜도 권장하고 있으며, 이로 인해 단일 스피커 구성보다 멀티룸 스피커를 선호하는 경향이 있습니다. 스트리밍의 지속적인 매출 모델은 프로모션 번들링을 촉진하고, 할인 스피커는 고객 확보 수단으로 작용하여 예측 기간 중 하드웨어 판매량을 더욱 자극할 수 있습니다.

만연한 모조품과 해적판

무허가 공장에 의한 인기 디자인 복제가 만연하고, 저품질 모조품이 EC 채널에 넘쳐나고 있습니다. 정품 브랜드를 가격적으로 압박하고, 소비자 신뢰를 훼손하는 사태가 발생하고 있습니다. 위조품은 안전회로를 생략하는 경우가 많아 배터리 화재 위험을 높이고, 인증 기술, 블록체인 라벨, 법적 조치 등 브랜드 보호 비용 증가를 초래하고 있습니다. 고급 제조업체는 보안 홀로그램과 공급망 추적을 도입하는 반면, 중소업체는 대규모 모니터링에 대한 자금 부족으로 인해 매출 유출과 평판 훼손의 위험에 노출되어 있습니다.

부문 분석

2025년 기준 블루투스 스피커 시장 점유율은 68.75%로, TV 및 멀티룸 플랫폼과 원활하게 연동되는 전원 공급 시스템에 대한 소비자 선호도가 높아짐에 따라 고정형 및 벽걸이형 유닛이 68.75%를 차지할 것으로 예측됩니다. 이 부문의 안정적인 매출 기반은 스마트홈 리노베이션 프로젝트와 연동된 예측 가능한 업그레이드 주기를 제조업체에 제공합니다. 한편, 휴대용 스피커는 도심 속 야외활동과 원격근무의 이동 수요를 배경으로 21.95%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다.

고정형 솔루션은 고음질, 저음 응답성, 음성비서 제어를 중시하며, 이는 평균판매가격(ASP)의 상승과 스트리밍 서비스와의 번들 판매를 촉진하는 특성입니다. 한편, 휴대용 디자인, 견고한 구조, 경량화, 장시간 배터리 작동에 최적화되어 신흥 시장의 새로운 구매자를 끌어들이고 있습니다. 따라서 이 두 가지 하위 부문은 서로를 잠식하지 않고 병행하여 성장하고 있으며, 블루투스 스피커 시장 전체에 다양한 매출 구조를 가져다주고 있습니다.

2025년 기준, 주거용 설치 환경은 블루투스 스피커 시장 규모의 60.55%를 차지하며 21.85%의 가장 빠른 CAGR을 유지할 것으로 예측됩니다. 이는 COVID-19로 인한 봉쇄 기간 중 형성된 가정 중심의 엔터테인먼트 습관이 정착되었음을 보여줍니다. 스마트홈의 지속적인 업그레이드로 인해 교체 주기가 4년 미만으로 줄어들어 기존 하이파이 장비의 평균 교체 주기를 크게 밑돌고 있습니다.

상업용 수요(레스토랑, 호텔, 소규모 사무실)는 프리미엄 설치형 시스템에서 여전히 중요하지만, 조달 프로세스의 장기화와 자본 예산의 긴축에 직면해 있습니다. 음성비서가 성숙함에 따라 가정용 스피커는 조명 및 공조 제어의 허브 역할을 강화하고, 기능과 엔터테인먼트 활용을 결합하여 블루투스 스피커 시장의 장기 수요 예측에서 주도적인 위치를 확고히 하고 있습니다.

지역별 분석

아시아태평양은 2025년 블루투스 스피커 시장 점유율의 31.45%를 차지할 것으로 예상되며, 제조 규모, 젊은 층의 소비, 스마트폰의 급속한 보급을 배경으로 2031년까지 연평균 복합 성장률(CAGR) 21.15%를 나타낼 것으로 예측됩니다. 중국 OEM 업체들은 PCB 및 배터리 공급망과의 지역적 근접성을 활용하여 리드타임을 단축하고, 2030년까지 5조 8,000억 위안이 넘을 것으로 예상되는 국내 전문가용 AV 기기 수요를 포착하고 있습니다. IoT 생태계에 대한 정부의 우대 정책은 스마트 스피커의 보급을 더욱 가속화하고 있으며, 수량과 혁신 측면에서 지역내 선도적 위치를 확고히 하고 있습니다.

북미는 판매량에서는 뒤처지지만, 평균판매가격(ASP)은 세계 최고 수준을 유지하고 있습니다. 스마트홈의 조기 도입과 음성비서 통합에 대한 소비자의 지불 의향이 이 지역의 매출총이익률을 세계 평균보다 높게 유지하고 있습니다. 국립공원에서의 캠핑부터 도심의 옥상 모임에 이르기까지 아웃도어 레크리에이션의 동향은 다중 장치 연결 기능을 갖춘 견고한 모델에 대한 수요를 불러일으키고 있습니다. 브랜드 충성도가 높은 소노스와 같은 카테고리 리더는 가격 경쟁 속에서도 프리미엄 판매 공간을 유지할 수 있습니다.

유럽에서는 15%대 초반의 견고한 성장세를 유지했습니다. 엄격한 품질 및 사이버 보안 기준은 기존 브랜드의 우위를 점하고, 2024년 8월부터 시행되는 개정 무선기기 지침(RED)은 보안 부팅 및 네트워크 보호를 의무화하여 컴플라이언스 예산이 없는 저가 수입품은 사실상 퇴출됩니다. 소비자는 컴플라이언스 준수 여부를 프리미엄 가격으로 구매로 평가하므로 국내외 제조업체들은 조기 인증 획득과 CE 마크를 차별화 요소로 활용하고 있습니다. 이를 통해 세계 블루투스 스피커 시장 매출에 대한 가치 중심의 기여가 지속되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The Bluetooth Speaker Market was valued at USD 18.32 billion in 2025 and estimated to grow from USD 21.93 billion in 2026 to reach USD 53.79 billion by 2031, at a CAGR of 19.65% during the forecast period (2026-2031).

Robust demand stems from smart-home adoption, mass music-streaming uptake, battery cost declines, and the commercialization of Bluetooth LE Audio, each widening the addressable user base while shortening replacement cycles. Asia-Pacific leads current unit volumes thanks to competitive manufacturing clusters and a rapidly expanding middle class, while North America and Europe deliver premium average selling prices (ASPs) on the back of early smart-home penetration. Voice-assistant-enabled models are the fastest-growing category, yet Bluetooth-only speakers still represent the largest sub-segment because they deliver a simple, low-latency experience that does not rely on Wi-Fi. Competitive dynamics are shifting toward consolidation as established brands purchase luxury audio houses to secure patented technologies and brand cachet, thereby raising entry barriers for commodity players.

Global Bluetooth Speaker Market Trends and Insights

Rapid Adoption of Smart-Home Ecosystems

Seamless interoperability delivered by the Matter standard elevates Bluetooth speakers from stand-alone entertainment devices to multifunction smart-home hubs. Amazon's 2025 Echo Show range illustrates the shift by embedding Fire TV services, auto-framing video communications, and full Matter, Zigbee, and Thread support in a single unit. Inter-brand compatibility lowers switching costs and drives premium replacement demand as households unify lighting, HVAC, and security control via voice-enabled speakers. Chinese ODM platforms such as LegatoXP shorten product development cycles, letting second-tier brands enter the smart-home space with smaller engineering budgets. Collectively, these forces accelerate household penetration, intensify brand competition, and enlarge the total volume opportunity for the Bluetooth speaker market.

Expansion of Music-Streaming Subscriptions

Music-streaming services surpassed 750 million paid subscribers in 2024, boosting demand for hardware capable of high-resolution and spatial-audio playback. As codecs such as LC3, LDAC, and aptX Lossless mature, users recognize audible quality deltas between legacy devices and next-generation speakers, prompting replacement purchases. Subscription platforms also encourage multi-device plans that natively support group listening, thereby favoring multi-room speakers over single-speaker setups. Streaming's recurring revenue model fosters promotional bundling, where discounted speakers act as customer-acquisition vehicles, further stimulating hardware volumes throughout the forecast window.

Rampant Counterfeiting and Piracy

Unauthorized factories replicate popular designs, flooding e-commerce channels with low-quality imitations that undercut legitimate brands on price and erode consumer trust. Counterfeits often omit essential safety circuits, raising the risk of battery fires and accelerating brand-protection expenditures for authentication technologies, blockchain labeling, and legal enforcement. While premium players deploy security holograms and supply-chain tracing, smaller vendors lack capital for large-scale monitoring, exposing them to revenue leaks and reputational damage.

Other drivers and restraints analyzed in the detailed report include:

- Bluetooth LE Audio and Auracast Roll-out

- Outdoor Recreation and Van-Life Boom

- Safety Recalls Tied to Battery Fires

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed and wall-mounted units accounted for 68.75% of the Bluetooth speaker market share in 2025, illustrating consumers' preference for power-fed systems that integrate seamlessly with televisions and multi-room platforms. This segment's steady revenue base gives manufacturers predictable upgrade cycles tied to smart-home renovation projects. Portable speakers, however, post a 21.95% CAGR, gaining from urban outdoor activities and remote-work mobility.

Fixed solutions emphasize audio fidelity, bass response, and voice-assistant control, traits that favor higher ASPs and bundling with streaming services. Portable designs optimize for rugged builds, lighter weight, and prolonged battery life, attracting first-time buyers in emerging markets. The two sub-segments, therefore, expand in parallel rather than cannibalize, yielding a diversified revenue structure for the overall Bluetooth speaker market.

Residential settings delivered 60.55% of the Bluetooth speaker market size in 2025 and also hold the fastest 21.85% CAGR, underscoring the permanence of home-centric entertainment habits formed during pandemic lockdowns. Continuous smart-home upgrades keep the replacement cycle under four years, far shorter than the historical averages for legacy hi-fi components.

Commercial demand, restaurants, hotels, and small offices, remains important for premium installed systems but faces elongated procurement processes and tighter capital budgets. As voice assistants mature, residential speakers increasingly serve as hubs for lighting and HVAC control, blending functional utility with leisure use and cementing their primacy in long-term demand projections for the Bluetooth speaker market.

The Global Bluetooth Speaker Market Report is Segmented by Portability (Portable, Fixed/Wall-Mounted), Application (Residential, Commercial), Connectivity Technology (Bluetooth-Only, and More), Distribution Channel (Online-Only Retailers, and More), Price Range (Economy Less Than USD 50, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 31.45% of the Bluetooth speaker market share in 2025, generating a 21.15% CAGR to 2031 on the back of manufacturing scale, youth-oriented consumption, and rapid smartphone proliferation. Chinese OEMs leverage proximity to printed-circuit and battery supply chains to compress lead times and capitalize on domestic demand, which is forecast to surpass CNY 5.8 trillion for professional AV equipment by 2030. Government incentives for IoT ecosystems further accelerate the adoption of smart speakers, solidifying regional leadership in both volume and innovation.

North America trails in unit volumes yet achieves the highest ASPs. Early smart-home adoption and consumer willingness to pay for voice-assistant integration keep the region's gross margins above global averages. Outdoor recreation trends-from national park camping to city rooftop gatherings- stimulate demand for ruggedized models with multi-device pairing. Brand loyalty is strong, allowing category leaders such as Sonos to maintain premium shelf space even amid price-based competition.

Europe posts steady mid-teen growth, backed by stringent quality and cybersecurity standards that favor established brands. The updated Radio Equipment Directive effective August 2024 mandates secure boot and network safeguards, effectively filtering out low-end imports lacking compliance budgets. Consumers reward compliance with premium pricing, prompting local and international manufacturers to certify early and use CE markings as marketing differentiators, sustaining a value-heavy contribution to global Bluetooth speaker market revenues.

- Sony Group Corporation

- Samsung Electronics Co., Ltd. (Harman International Industries, Inc.)

- Panasonic Holdings Corporation

- Bose Corporation

- Beats Electronics LLC (Apple Inc.)

- Koninklijke Philips N.V.

- LG Electronics Inc.

- Logitech International S.A.

- Sonos, Inc.

- Bang & Olufsen A/S

- Yamaha Corporation

- Altec Lansing LLC

- JVCKENWOOD Corporation

- Anker Innovations Technology Co., Ltd.

- Ultimate Ears (Logitech)

- Tribit Audio (Thesy Technology Co., Ltd.)

- Onkyo Home Entertainment Corporation

- Zebronics India Pvt. Ltd.

- AOMAIS Audio (Shenzhen Jin Wen Hua)

- SoundBot Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of smart-home ecosystems

- 4.2.2 Expansion of music-streaming subscriptions

- 4.2.3 Falling ASPs of lithium-ion batteries

- 4.2.4 Outdoor recreation and van-life boom

- 4.2.5 Bluetooth LE Audio and Auracast roll-out

- 4.2.6 Growing demand for immersive classroom audio

- 4.3 Market Restraints

- 4.3.1 Rampant counterfeiting and piracy

- 4.3.2 Margin erosion from price wars

- 4.3.3 Safety recalls tied to battery fires

- 4.3.4 Stricter EU EMI limits for more than 30 W speakers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Portability

- 5.1.1 Portable

- 5.1.2 Fixed / Wall-Mounted

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 By Connectivity Technology

- 5.3.1 Bluetooth-only

- 5.3.2 Bluetooth + Wi-Fi (Multi-room)

- 5.3.3 Smart Speakers w/ Voice Assistant

- 5.4 By Distribution Channel

- 5.4.1 Online-Only Retailers

- 5.4.2 Omnichannel Consumer-Electronics Stores

- 5.5 By Price Range

- 5.5.1 Economy (Less than USD 50)

- 5.5.2 Mid-range (USD 50-199)

- 5.5.3 Premium (More than USD 200)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sony Group Corporation

- 6.4.2 Samsung Electronics Co., Ltd. (Harman International Industries, Inc.)

- 6.4.3 Panasonic Holdings Corporation

- 6.4.4 Bose Corporation

- 6.4.5 Beats Electronics LLC (Apple Inc.)

- 6.4.6 Koninklijke Philips N.V.

- 6.4.7 LG Electronics Inc.

- 6.4.8 Logitech International S.A.

- 6.4.9 Sonos, Inc.

- 6.4.10 Bang & Olufsen A/S

- 6.4.11 Yamaha Corporation

- 6.4.12 Altec Lansing LLC

- 6.4.13 JVCKENWOOD Corporation

- 6.4.14 Anker Innovations Technology Co., Ltd.

- 6.4.15 Ultimate Ears (Logitech)

- 6.4.16 Tribit Audio (Thesy Technology Co., Ltd.)

- 6.4.17 Onkyo Home Entertainment Corporation

- 6.4.18 Zebronics India Pvt. Ltd.

- 6.4.19 AOMAIS Audio (Shenzhen Jin Wen Hua)

- 6.4.20 SoundBot Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment