|

시장보고서

상품코드

1939104

에너지 관리 시스템(EMS) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Energy Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

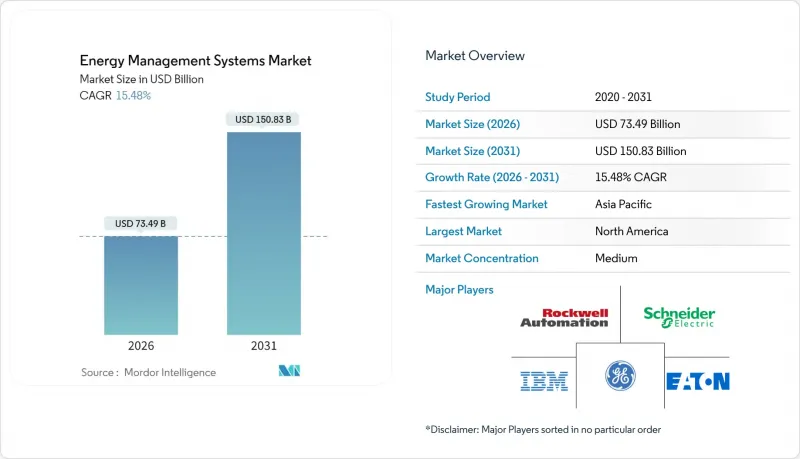

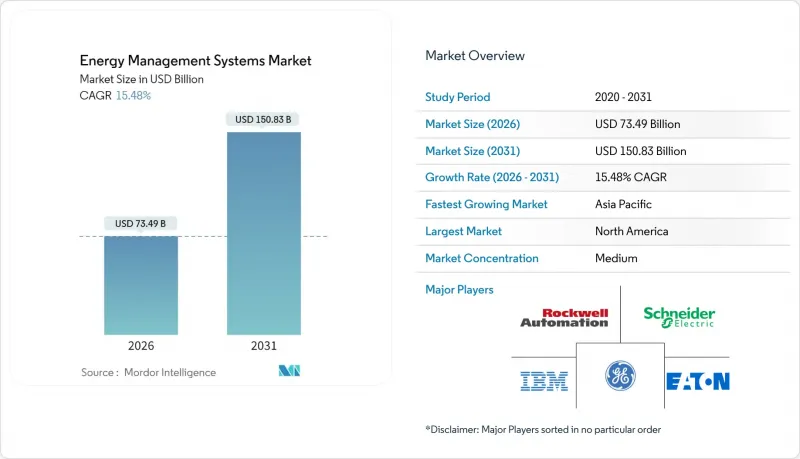

에너지 관리 시스템(EMS) 시장은 2025년에 636억 4,000만 달러로 평가되었으며, 2026년 734억 9,000만 달러에서 2031년까지 1,508억 3,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2031년) 동안 CAGR은 15.48%로 예상됩니다.

이러한 급격한 성장은 탈탄소화 규제 강화, 스마트 그리드의 급속한 확산, 기업의 넷제로 목표가 높아짐에 따라 실시간 에너지 최적화가 선택에서 필수로 전환되고 있음을 반영합니다. 전력회사들은 대규모로 AMI(Advanced Metering Infrastructure)를 도입하고 있으며, 이를 통해 사업자는 상세한 데이터를 확보할 수 있고, AI 기반 분석과 결합하여 자가 복구형 그리드 기능을 실현하고 운영 비용을 절감하고 있습니다. 상업용 부동산 소유주들은 2026년부터 의무화되는 넷제로 건축 기준에 직면해 있으며, 이로 인해 커넥티드 HVAC(냉난방 환기), 조명, 제어 플랫폼에 대한 수요가 급증할 것으로 예상됩니다. 한편, 대규모 재생에너지 구매 계약을 체결하는 기업들은 시간 단위 추적, 인증서 관리, 탄소 회계가 가능한 통합 시스템을 필요로 합니다. 기후 정책과 더불어 변동하는 상품 가격과 탄소 비용의 상승은 에너지 관리 시스템(EMS) 시장의 경제적 합리성을 더욱 높이고 있으며, 기업들은 두 자릿수 비용 절감과 공급측 충격에 대한 내성을 추구하고 있습니다.

세계 에너지 관리 시스템(EMS) 시장 동향 및 인사이트

첨단 계량 인프라의 급속한 보급으로 전력망 지능화 추진

성숙한 경제권의 유틸리티 사업자들은 2024년까지 AMI 프로그램을 가속화하여 클라우드 분석 엔진에 간격 데이터를 전송하는 수백만 개의 스마트 미터를 설치했습니다. 에버소스는 매사추세츠와 코네티컷 주에 걸쳐 130만 대의 프로젝트를 완료했고, 내셔널 그리드는 북동부 지역에서 340만 개의 엔드포인트를 연결했습니다. 이 데이터 피드는 자동화된 수요 대응, 정전 자가 복구, 예측 부하 예측과 같은 현대 에너지 관리 시스템(EMS) 시장 플랫폼의 핵심 모듈을 지원합니다. AI 알고리즘이 몇 초 만에 전력 경로를 변경하여 복구 시간을 단축하고 배전 손실을 줄입니다. 배전 사업자가 그리드 서비스를 수익화하고 재생에너지에 대응하는 과정에서 AMI는 현장 자산과 클라우드 기반 최적화를 연결하는 필수적인 계층을 형성하고 있습니다.

의무화된 넷제로 건축 표준으로 상업용 EMS 도입 가속화

뉴욕시, 워싱턴주, 캘리포니아주 등의 관할권에서는 2026년을 조기 시작 시점으로 대규모 건축물의 넷제로 운영을 촉진하는 규정을 제정했습니다. 뉴욕시 조례 97호는 25,000평방피트(약 2,323평방미터) 이상의 시설에 대해 2030년까지 배출량 40% 감축을 의무화하고, 위반 시 고액의 벌금을 부과합니다. 캘리포니아주 Title 24 개정으로 고급 제어 및 계측이 규정되어 에너지 관리 시스템(EMS)의 시장 도입이 임의적 업그레이드에서 규제 대응을 위한 필수 요건으로 바뀌었습니다. 캐나다와 EU에도 유사한 규제가 적용되어 통합형 HVAC, 조명, 재생에너지 대응 플랫폼에 대한 잠재적 수요가 확대되고 있습니다.

높은 초기 도입 비용으로 중소기업 시장 침투를 제약하는 요인

종합적인 도입에는 여전히 5만-50만 달러가 필요하며, 자금에 제약이 있는 시설의 경우 장벽이 될 수 있습니다. 하드웨어, 통합, 교육으로 인해 투자 회수 기간이 18-36개월로 길어져 중소기업의 도입이 늦어지고 있습니다. EaaS(Energy-as-a-Service) 구독으로 설비투자(CapEx)가 운영비용(OpEx)으로 전환되어 진입장벽이 낮아지고 있습니다. 아이리스 오하이마(Iris Ohima)가 2025년에 발표한 클라우드 스위트 'ENEverse'는 센서, 분석, 원격 제어를 하드웨어가 필요 없는 모델로 통합한 이 전환을 상징적으로 보여주는 사례입니다.

부문 분석

빌딩 에너지 관리 시스템(EMS)은 2025년 전체 에너지 관리 시스템(EMS) 시장의 45.62%를 차지하며 가장 큰 점유율을 차지할 것으로 예상됩니다. 규제 강화, 임차인을 위한 지속가능성 보고, 건강한 실내 환경에 대한 요구가 증가함에 따라 상업용 건물은 유틸리티 비용을 25-40% 절감할 수 있는 첨단 제어 시스템에 대한 투자를 지속하고 있습니다. 가정용 솔루션은 가장 빠른 성장세를 보이고 있으며, 전기요금 상승, 스마트 가전 보급, 전력 수요 대응 인센티브, 음성 제어 온도 조절기 및 자동 EV 충전 스케줄 관리의 보급으로 CAGR 16.85%로 확대되고 있습니다. 통합 플랫폼은 현재 재실 센서, 태양광발전 인버터, 배터리 제어를 융합하여 자기 조절형 나노 그리드를 구축하고 있습니다. 벤더마다 아키텍처(엣지 허브 대 클라우드 퍼스트)는 다르지만, 모두 데이터를 AI 엔진에 통합하여 실시간 최적화를 실현합니다. 이에 따라 에너지 관리 시스템(EMS)의 시장 대상 기반이 확대되고 있습니다.

최근 몇 년간의 발전은 규칙 기반 자동화에서 예측적 오케스트레이션으로의 전환을 보여주고 있습니다. C3.ai의 모델은 물리 기반 설비 라이브러리와 머신러닝을 결합하여 부하 피크를 예측하고 HVAC를 사전 조정하여 에너지 강도를 최소화합니다. 캐리어의 블루엣지 커맨드 센터는 냉각기 수준의 데이터를 원격 엔지니어에게 스트리밍하여 몇 분 안에 설정값을 조정합니다. 현지 직원 없이도 두 자릿수 비용을 절감할 수 있습니다. 이를 통해 피드백 루프를 형성하고, 입증된 절감 효과가 추가 리노베이션 자금으로 전환되어 벤더 수익의 기반이 되는 장기 서비스 계약을 확고히 합니다.

제조시설은 에너지 비용이 운영비의 20%에 달하는 것이 일반화되어 있어 2025년 에너지 관리 시스템(EMS) 시장 점유율의 31.05%를 차지할 것으로 예상됩니다. 시멘트, 철강, 화학 등의 분야에서는 고속 센서와 디지털 트윈을 활용하여 용광로, 압축기, 공정라인을 조정하여 생산성 향상에 전력을 다하고 있습니다. 그러나 의료 분야는 16.02%의 CAGR로 성장하고 있습니다. 병원은 24시간 365일 가동되고 엄격한 습도 및 온도 관리가 필요하기 때문에 AI를 통한 공조 및 보일러 제어 최적화에 최적의 환경입니다. 아폴로병원에서는 의료기기 가동 스케줄과 코제너레이션 제어를 통합한 클라우드형 EMS 도입 후 30%의 광열비 절감을 달성한 것으로 보고되고 있습니다.

두 번째 주요 최종사용자인 전력 사업자는 수요 예측 및 재생에너지 통합을 위해 EMS 모듈에 의존하고 있습니다. IT 및 통신 사업자들은 냉각 부하가 총 전력 소비의 40%에 육박하는 데이터센터 내에서 유사한 논리를 적용하고 있습니다. AI 워크로드에 따른 서버 밀도가 급증함에 따라 고급 기류 모델링과 액체 냉각 최적화가 시설의 주류 로드맵에 포함되고 있습니다. 주거 및 상업용 복합시설은 순계량제 정책과 옥상 태양광발전의 수익화 요구에 힘입어 수요를 보완하고 있습니다.

에너지 관리 시스템(EMS) 시장 보고서는 EMS 유형(BEMS, IEMS, HEMS), 최종사용자(제조업, 전력/에너지, IT/통신, 의료, 주거/상업), 용도(에너지 생성, 에너지 전송, 에너지 모니터링), 구성요소(하드웨어, 소프트웨어, 서비스), 지역별로 분류되어 있습니다. 서비스), 지역별로 분류되어 있습니다.

지역별 분석

북미는 2025년에도 에너지 관리 시스템(EMS) 시장 매출의 35.18%를 차지하며 선두를 유지할 것으로 예상됩니다. 인플레이션 억제법에 따른 연방 자금과 주정부 세금 공제가 계측, 전기자동차 충전, 건물 개조 프로젝트를 촉진하고 있습니다. 에버소스, 내셔널 그리드 등 유틸리티 회사들은 2024년까지 수백만 개의 스마트 엔드포인트를 추가하여 고도화된 분석을 지원하는 데이터 기반을 구축했습니다. 슈나이더 일렉트릭은 이에 대응하여 미국 공장에 7억 달러를 투자하는 확장 계획을 시행했습니다. 개폐기, 마이크로그리드 제어장치, 소프트웨어 연구개발의 현지 생산화를 추진하여 정책의 안정성과 고객 수요에 대한 확신을 보여주고 있습니다.

유럽도 유럽 그린딜과 'Fit for 55' 패키지를 통해 2030년까지 1990년 대비 55%의 배출량 감축을 규정하는 등 긴밀하게 따라가고 있습니다. 회원국은 디지털 빌딩 요건을 지역 규제에 포함시켜 통합 빌딩 분석에 대한 견고한 수요를 촉진하고 있습니다. 독일의 P2P 거래 샌드박스 도입과 네덜란드의 적극적인 히트 펌프 보조금 제도는 규제가 확대되고 있음을 보여줍니다. TPG가 서브미터링 및 효율화 서비스를 통한 지속적인 수익에 매료되어 67억 유로에 테켐을 인수한 사례는 TPG의 투자 의욕이 얼마나 높은지 잘 보여줍니다. 전력회사들은 변동하는 재생에너지 흐름에 대응하기 위해 그리드 엣지의 디지털화를 가속화하고 있으며, 에너지 관리 시스템(EMS) 시장을 더욱 확대시키고 있습니다.

아시아태평양은 연평균 CAGR 15.88%의 성장 동력이 될 것으로 예상됩니다. 중국은 2030년까지 계획된 1,200GW의 풍력 및 태양광발전 용량을 조정하기 위해 초고전압 송전망과 AI 강화형 지령센터에 대한 투자를 진행하고 있습니다. 일본의 가정용 EMS 및 빌딩용 EMS에 대한 보조금(2025년도에 40억 엔이 책정됨)은 벤더의 수주 파이프라인을 강화할 것입니다. 인도의 스마트 시티 계획은 공공건물 및 가로등 네트워크 입찰에 EMS 요구사항을 포함시키고 있습니다. 한편, 동남아시아 국가에서는 빠르게 확산되고 있는 지붕 설치형 태양광발전에 대응하기 위해 송전망 안정화 솔루션이 요구되고 있습니다. 지역 제조 거점을 설립하는 다국적 기업들은 초기 단계부터 EMS를 지정하여 신규 수요를 가속화하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

- 시장 개요

- 시장 성장 촉진요인

- 첨단 계량 인프라(AMI)의 신속한 구축

- 2026년부터 주요 경제국에서 의무적으로 시행되는 탄소중립 건물 기준

- AI 기반 예측 유지보수를 통한 유틸리티 기업의 운영 비용 절감

- 세분화된 에너지 데이터에 대한 기업 PPA(전력 구매 계약)의 증가

- 블록체인 기반 P2P(개인 간) 에너지 거래 시범 사업

- 시장 성장 억제요인

- 높은 초기 시스템 통합 비용

- 기존 OT/IT 상호 운용성 격차 (브라운필드 사이트)

- 진화하는 중요 인프라 관련 법률에 따른 사이버 보안 책임

- OECD 국가 외 지역의 EMS 숙련 기술자 부족

- 산업가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- EMS 유형별

- 건물 에너지 관리 시스템(BEMS)

- 산업용 EMS(IEMS)

- 가정 응급 의료 서비스(HEMS)

- 최종 사용자별

- 제조

- 전력 및 에너지

- 정보 기술 및 통신

- 의료 서비스

- 주거 및 상업용

- 적용 분야별

- 에너지 생성

- 에너지 전송

- 에너지 모니터링 및 최적화

- 구성 요소별

- 하드웨어

- 소프트웨어

- 서비스

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 아세안

- 기타 아시아태평양

- 중동

- GCC(사우디아라비아, 아랍에미리트, 카타르 등)

- 터키

- 기타 중동

- 아프리카

- 남아프리카공화국

- 나이지리아

- 케나

- 기타 아프리카

- 북미

제6장 경쟁 구도

- Schneider Electric

- Siemens AG

- Honeywell International Inc.

- ABB Ltd.

- General Electric

- Eaton Corporation

- Rockwell Automation Inc.

- Johnson Controls

- IBM Corporation

- Oracle Corporation

- SAP SE

- Cisco Systems

- Enel X

- Autogrid Systems

- Itron Inc.

- Honeywell Smart Energy

- Mitsubishi Electric

- Yokogawa Electric

- Tendril (Uplight)

- WAGO Kontakttechnik

제7장 시장 기회 및 향후 전망

KSM 26.03.09The Energy Management Systems market was valued at USD 63.64 billion in 2025 and estimated to grow from USD 73.49 billion in 2026 to reach USD 150.83 billion by 2031, at a CAGR of 15.48% during the forecast period (2026-2031).

The surge reflects stricter decarbonization rules, rapid smart-grid deployment, and mounting corporate net-zero targets that elevate real-time energy optimization from optional to indispensable. Utilities are rolling out advanced metering infrastructure (AMI) at scale, giving operators the granular data they need to pair with AI-driven analytics for self-healing grid functions and lower operating costs. Commercial real-estate owners face mandatory net-zero building codes starting in 2026, driving a jump in demand for connected HVAC, lighting, and controls platforms. Meanwhile, firms signing large renewable power-purchase agreements require integrated systems capable of hourly tracking, certificate management, and carbon accounting. Beyond climate policy, volatile commodity prices and growing carbon costs sharpen the economic case for the Energy Management Systems market, as enterprises chase double-digit savings and resilience against supply-side shocks.

Global Energy Management Systems Market Trends and Insights

Rapid Roll-out of Advanced Metering Infrastructure Transforms Grid Intelligence

Utilities across mature economies accelerated AMI programs in 2024, installing millions of smart meters that stream interval data to cloud analytics engines. Eversource finished a 1.3 million-meter project spanning Massachusetts and Connecticut, while National Grid connected 3.4 million endpoints in the Northeast. The data feed underpins automated demand response, outage self-healing, and predictive load forecasting, all core modules in modern Energy Management Systems market platforms. AI algorithms re-route power within seconds, cutting restoration times and trimming distribution losses. As distribution operators monetize grid services and accommodate renewables, AMI forms the essential layer linking field assets with cloud-based optimization.

Mandatory Net-Zero Building Codes Accelerate Commercial EMS Adoption

Jurisdictions such as New York City, Washington State, and California enacted rules that push large buildings toward net-zero operations, starting as early as 2026. Local Law 97 requires facilities over 25,000 ft2 to cut emissions 40% by 2030, with steep fines for non-compliance. California's Title 24 updates stipulate advanced controls and measurement, turning Energy Management Systems market deployments from voluntary upgrades into compliance necessities. Similar mandates ripple across Canada and the EU, expanding addressable demand for integrated HVAC, lighting, and renewable-ready platforms.

High Up-Front System Integration Costs Constrain SME Market Penetration

Comprehensive deployments still command USD 50,000-500,000, a hurdle for cash-constrained facilities. Hardware, integration, and training extend payback to 18-36 months, delaying adoption in small enterprises. Energy-as-a-Service subscriptions now re-cast capex as opex, lowering entry barriers; Iris Ohyama's 2025 launch of the ENEverse cloud suite typifies that pivot, bundling sensors, analytics, and remote operations into a no-hardware model.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered Predictive Maintenance Revolutionizes Utility Operations

- Corporate Power Purchase Agreements Drive Granular Energy Data Requirements

- Legacy OT/IT Interoperability Gaps Complicate Brownfield Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Building Energy Management Systems capture the largest slice of the Energy Management Systems market at 45.62% in 2025. Tighter codes, tenant sustainability reporting, and the premium on healthy indoor environments keep commercial campuses investing in advanced controls that trim 25-40% of utility spend. Home solutions post the fastest trajectory, rising at a 16.85% CAGR as rising electricity tariffs, smart-appliance penetration, and utility demand-response incentives nudge households toward voice-controlled thermostats and automated EV-charger scheduling. Integrated platforms now fuse occupancy sensors, PV inverters, and battery dispatch to create self-balancing nanogrids. Suppliers differ on architecture-edge hubs versus cloud-first-but all route data into AI engines for real-time optimization, broadening the Energy Management Systems market addressable base.

Recent advancements illustrate the shift from rule-based automation to predictive orchestration. C3.ai models combine physics-based equipment libraries with machine learning to anticipate load peaks and pre-condition HVAC for minimal energy intensity. Carrier's BluEdge Command Center streams chiller-level data to remote engineers who tweak set points in minutes, achieving double-digit savings without on-site staff. The result is a feedback loop: verified savings fund further retrofits, cementing long-term service contracts that anchor vendor revenue.

Manufacturing facilities accounted for 31.05% of Energy Management Systems market share in 2025 owing to energy bills that routinely reach 20% of operating costs. Sectors such as cement, steel, and chemicals leverage high-speed sensors and digital twins to orchestrate furnaces, compressors, and process lines, seeking every kilowatt of productivity. Nevertheless, the healthcare vertical is expanding at a 16.02% CAGR. Hospitals run 24/7, with stringent humidity and temperature thresholds, making them ideal candidates for AI-guided HVAC and boiler sequencing. Apollo Hospitals reports 30% utility savings after deploying a cloud EMS that integrates medical equipment scheduling and cogeneration controls.

Power utilities, the second-largest end-user, rely on EMS modules for demand forecasting and renewables integration. IT and telecom operators apply similar logic inside data centers where cooling loads approach 40% of total consumption. As server densities jump with AI workloads, advanced airflow modeling and liquid-cooling optimization enter mainstream facility roadmaps. Residential and commercial mixed-use complexes round out demand, driven by net-metering policies and the urge to monetize rooftop solar.

The Energy Management System Market Report is Segmented by Type of EMS (BEMS, IEMS, and HEMS), End-User (Manufacturing, Power and Energy, IT and Telecommunication, Healthcare, and Residential and Commercial), Application (Energy Generation, Energy Transmission, and Energy Monitoring), Component (Hardware, Software, and Services), and Geography.

Geography Analysis

North America retains its pole position with 35.18% of Energy Management Systems market revenue in 2025. Federal funding through the Inflation Reduction Act and state tax credits catalyze metering, EV-charging, and building-retrofit projects. Utilities such as Eversource and National Grid added millions of smart endpoints in 2024, laying the data fabric that underpins advanced analytics. Schneider Electric responded with a USD 700 million expansion across U.S. plants to localize production of switchgear, microgrid controllers, and software R&D, signalling confidence in policy stability and customer demand.

Europe follows closely, propelled by the European Green Deal and Fit-for-55 package that stipulate 55% emission cuts versus 1990 by 2030. Member states embed digital-building requirements in local codes, fostering robust demand for integrated building analytics. Germany's roll-out of P2P trading sandboxes and the Netherlands' aggressive heat-pump incentives showcase regulatory breadth. Investment appetite surfaced when TPG paid EUR 6.7 billion for Techem, attracted by recurring revenues from sub-metering and efficiency services. Utilities accelerate grid-edge digitization to handle variable renewable flows, further enlarging the Energy Management Systems market.

Asia-Pacific is the growth engine with a projected 15.88% CAGR. China invests in ultra-high-voltage transmission and AI-enhanced dispatch centers to balance its 1,200 GW of wind-solar capacity planned by 2030. Japan's subsidies for Home EMS and Building EMS, backed by JPY 4 billion earmarked in 2025, bolster vendor pipelines. India's Smart Cities Mission embeds EMS requirements in tenders for public buildings and street-lighting networks, while Southeast Asian economies seek grid-stability solutions to cope with rapid rooftop-solar adoption. Multinationals setting up regional manufacturing hubs specify EMS from day one, accelerating greenfield demand.

- Schneider Electric

- Siemens AG

- Honeywell International Inc.

- ABB Ltd.

- General Electric

- Eaton Corporation

- Rockwell Automation Inc.

- Johnson Controls

- IBM Corporation

- Oracle Corporation

- SAP SE

- Cisco Systems

- Enel X

- Autogrid Systems

- Itron Inc.

- Honeywell Smart Energy

- Mitsubishi Electric

- Yokogawa Electric

- Tendril (Uplight)

- WAGO Kontakttechnik

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid roll-out of advanced metering infrastructure (AMI)

- 4.2.2 Mandatory net-zero building codes in major economies from 2026

- 4.2.3 AI-powered predictive maintenance lowering OPEX for utilities

- 4.2.4 Growing corporate PPAs demanding granular energy data

- 4.2.5 Blockchain-enabled peer-to-peer (P2P) energy trading pilots

- 4.3 Market Restraints

- 4.3.1 High up-front system integration costs

- 4.3.2 Legacy OT/IT interoperability gaps in brownfield sites

- 4.3.3 Cyber-security liability under evolving critical-infrastructure laws

- 4.3.4 Shortage of EMS-skilled technicians outside OECD

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type of EMS

- 5.1.1 Building EMS (BEMS)

- 5.1.2 Industrial EMS (IEMS)

- 5.1.3 Home EMS (HEMS)

- 5.2 By End-User

- 5.2.1 Manufacturing

- 5.2.2 Power and Energy

- 5.2.3 IT and Telecommunication

- 5.2.4 Healthcare

- 5.2.5 Residential and Commercial

- 5.3 By Application

- 5.3.1 Energy Generation

- 5.3.2 Energy Transmission

- 5.3.3 Energy Monitoring and Optimization

- 5.4 By Component

- 5.4.1 Hardware

- 5.4.2 Software

- 5.4.3 Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC (Saudi Arabia, UAE, Qatar, etc.)

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric

- 6.4.2 Siemens AG

- 6.4.3 Honeywell International Inc.

- 6.4.4 ABB Ltd.

- 6.4.5 General Electric

- 6.4.6 Eaton Corporation

- 6.4.7 Rockwell Automation Inc.

- 6.4.8 Johnson Controls

- 6.4.9 IBM Corporation

- 6.4.10 Oracle Corporation

- 6.4.11 SAP SE

- 6.4.12 Cisco Systems

- 6.4.13 Enel X

- 6.4.14 Autogrid Systems

- 6.4.15 Itron Inc.

- 6.4.16 Honeywell Smart Energy

- 6.4.17 Mitsubishi Electric

- 6.4.18 Yokogawa Electric

- 6.4.19 Tendril (Uplight)

- 6.4.20 WAGO Kontakttechnik

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment