|

시장보고서

상품코드

1939111

자동차 유리 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

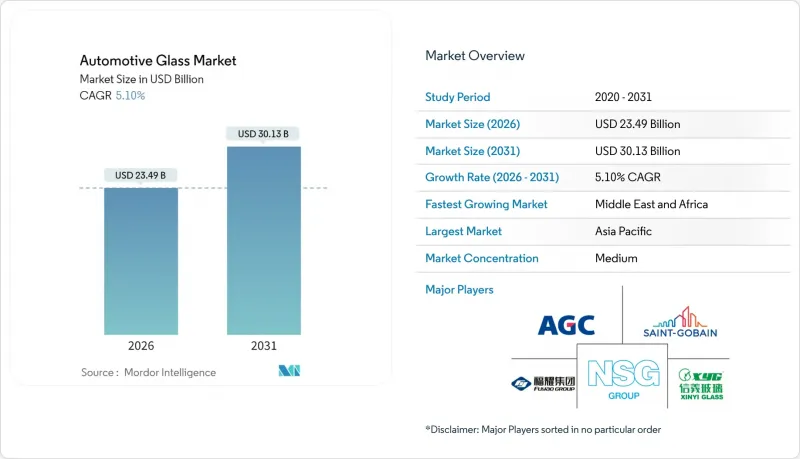

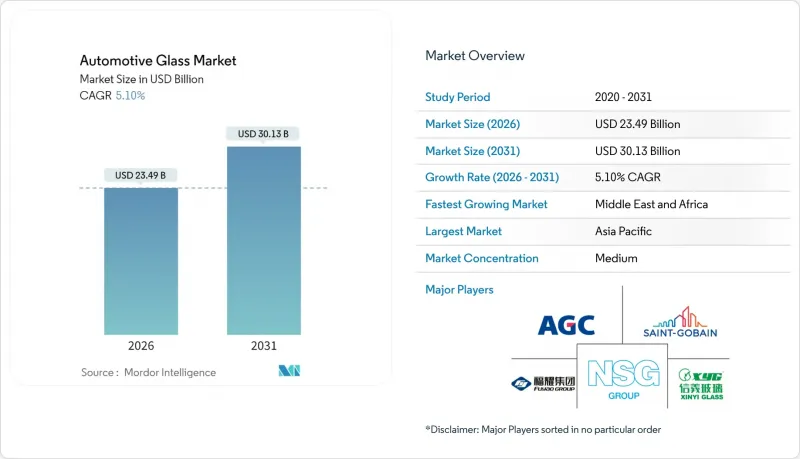

자동차 유리 시장은 2025년 223억 5,000만 달러에서 2026년에는 234억 9,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 5.1%를 기록하며 2031년까지 301억 3,000만 달러에 달할 것으로 예측됩니다.

원자재 가격 및 물류 비용의 변동에도 불구하고, 자동차 생산량 증가, 안전 기준 강화, 전기 모빌리티로의 전환이 성장 모멘텀을 뒷받침하고 있습니다. 파노라마 루프, 경량 접합유리, 일렉트로크로믹 유리에 대한 수요 확대에 따라 제조사들은 전문 라인의 확대와 OEM과의 제휴 강화를 추진하고 있습니다. SUV의 대형 유리 표면의 중요성과 CO2 배출량 감소에 대한 규제 압력으로 인해 코팅 가공품 및 다기능 제품의 채택이 가속화되고 있습니다. 이러한 요인들이 결합되어 향후 10년간 자동차 유리 시장은 기술 주도의 견조한 성장을 보일 것으로 예상됩니다.

세계 자동차 유리 시장 동향 및 전망

EV 플랫폼에서 파노라마 유리로 전환하는 과정

전기자동차 제조사들은 차량 내부의 분위기와 브랜드 아이덴티티를 높이기 위해 더 큰 루프 패널을 채택하고 있습니다. 테슬라의 사이버트럭과 메르세데스-벤츠의 비전 V 콘셉트는 색조 레벨을 조절하는 전기변색 지붕을 통합하여 차량 내부 온도를 최대 18°F(약 10°C)까지 낮춰 HVAC 부하를 줄입니다. 차량 당 유리 면적이 급증할 것으로 예상되며, 공급업체들은 와이드 포맷 벤딩 가공, 저방사선(Low-E) 코팅, 적외선 흡수 중간막에 대한 투자를 진행하고 있습니다. 이 프리미엄 사양은 생산비용이 낮아짐에 따라 중저가 전기자동차에도 보급이 확대되어 자동차 유리 시장의 지속적인 성장을 뒷받침할 것으로 예상됩니다.

CO2 배출량 목표 달성을 위한 경량 접합유리의 OEM 수요

유럽 규정은 2030년까지 자동차 그룹 평균 CO2 배출량을 100g/km로 설정하고 있으며, 자동차 제조업체들은 모든 방법을 동원해 무게를 줄이기 위해 노력하고 있습니다. EPA의 2017년형 포드 GT에 대한 조사에 따르면, 접합유리가 무게 30% 감소에 크게 기여한 것으로 나타났습니다. 현재 이온 플라스틱 중간막을 사용한 박막 접합유리는 내충격 성능의 저하 없이 최대 30%의 경량화를 실현하고 있습니다. AGC와 산고반은 경량화와 차음성을 겸비한 1.6mm 전면유리 구조를 상용화하여 자동차 유리 시장의 장기적인 전망을 강화하고 있습니다.

특수 중간막(PVB, 이오노플라스틱) 공급망 부족

클라레의 PVB 생산능력 확대가 방음·HUD용 필름의 수요 증가를 따라잡지 못해 납기 연장 및 할당제 도입이 불가피한 상황입니다. 유럽 라미네이터 업체들은 스팟 부족으로 애프터마켓 주문보다 OEM 생산을 우선시할 수밖에 없는 상황입니다. 실험 단계의 바이오 기반 중간막은 53.1%의 유망한 기계적 특성 향상을 실현했지만, 대량 생산에는 몇 년이 걸릴 것으로 예상됩니다. 신공장이 가동되기 전까지는 단기적인 공급 부족이 자동차 유리 시장의 성장을 억제할 수 있습니다.

부문 분석

2025년 기준, 일반 유리는 비용 효율성과 생산 설비의 확립으로 인해 자동차 유리 시장의 82.05%를 차지했습니다. 접합유리는 충격 시 파편을 잡아주는 특성으로 세계 안전기준을 충족하며 강화유리 형식에 비해 점유율을 확대하고 있습니다. 이러한 전환으로 인해 특수 중간막의 공급이 타이트해졌지만, OEM 업체들이 더 얇고 가벼운 구조를 요구함에 따라 라미네이터 업체들은 고부가가치 창출의 기회를 얻게 되었습니다. 스마트 글래스는 현재 소수이지만, 12.1%의 CAGR로 성장하며 고급차 및 하이엔드 EV에서 틈새시장을 개척할 것으로 예상됩니다.

전기 염료 지붕이 초기 도입을 주도하고 있습니다. 메르세데스-벤츠의 Vision V 프로토타입에 채택된 부유 입자 장치(SPD)는 보다 빠른 스위칭과 내구성을 실현했습니다. 폴리머 분산형 액정(PDLC) 창은 프라이버시 파티션을 목표로 하고 있으며, 열염료 필름은 아직 상용화 전 단계에 있습니다. 규모의 경제가 향상됨에 따라 스마트 글래스는 플래그십 모델을 넘어 보급되어 자동차 유리 시장을 강화할 것입니다.

2025년 기준 앞유리는 자동차 유리 시장 규모의 44.15%를 차지할 것으로 예상되며, 의무 장착화와 ADAS 센서 탑재량 증가가 그 기반이 되고 있습니다. 복잡성은 단가 상승을 촉진하고, 공급업체와 OEM의 공동 개발 주기를 강화하고 있습니다. 한편, 선루프는 SUV의 파노라마 시야를 위한 대형 개구부의 표준화로 인해 CAGR 9.6%로 가장 빠르게 성장하는 애플리케이션이 되었습니다.

백라이트는 방음 라미네이트에 의한 점진적인 수요 확대가 예상되나, 보증 문제가 보급 속도를 억제하고 있습니다. 사이드 라이트는 특히 유럽과 일본의 배출 방지법 대응을 위해 라미네이트 구조로 전환 중입니다. 백미러와 쿼터 윈도우에는 넓은 면적을 요구하지 않는 기능 추가로서 일렉트로크로믹 눈부심 방지 코팅이 통합되어 있습니다. 이러한 용도 구성이 결합되어 자동차 유리 시장의 꾸준한 확장을 뒷받침하고 있습니다.

지역별 분석

아시아태평양은 자동차 유리 시장을 주도하고 있으며, 2025년 매출의 48.75%를 차지할 것으로 예상됩니다. 중국의 방대한 생산량과 급속한 국내 수요 확대가 그 기반이 되고 있습니다. 정부의 우대 정책으로 공장 가동률은 높은 수준을 유지하고 있으며, 인도의 생산 증가는 새로운 수요 축을 형성하고 있습니다. 상하이에서 열리는 회의에서는 지능형 유리, LiDAR 투과성, AR-HUD 통합 기술이 주목받고 있으며, 지속적인 기술 혁신을 보여주고 있습니다. 일본과 한국은 고급 OEM을 위한 고급 접합유리 및 코팅 제품을 공급하여 전체 자동차 유리 시장 내에서 고수익의 틈새시장을 유지하고 있습니다.

각 제조사들은 중국산 수입품으로 인한 수익률 압박에 대응하기 위해 스마트 글래스 및 지속가능성 프로그램으로 전환하고 있습니다. AGC와 산고반이 공동 개발한 볼타로는 CO2 배출 강도 감소를 위한 전략적 움직임의 증거입니다. 한편, 북미는 SUV 수요로 인해 여전히 영향력을 유지하고 있습니다. 미국에서는 애프터마켓이 활성화되어 있으며, Auto Glass Now와 같은 브랜드가 전국적으로 확대하여 교체 수요의 수익 창출을 목표로 하고 있습니다.

중동 및 아프리카는 2031년까지 CAGR 6.8%로 가장 빠르게 성장할 것으로 예상됩니다. 사우디아라비아의 풍부한 실리카 광상은 공급의 현지화를 목적으로 한 플로트 글라스 투자를 유치하고 있습니다. 산업다각화 정책에 따른 보조금 제도는 자동차 부품 생산을 촉진하고, 이 지역의 자동차 유리 시장 점유율 확대에 기여하고 있습니다. 남미의 전망은 주로 브라질의 조립량에 의존하고, 아프리카의 성장은 남아프리카공화국의 비교적 성숙한 부문이 중심입니다. 세계 공급업체들은 인근 생산 전략을 통해 다양한 지역에서의 운송 비용과 적시성 기대치 사이의 균형을 맞추고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The automotive glass market is expected to grow from USD 22.35 billion in 2025 to USD 23.49 billion in 2026 and is forecast to reach USD 30.13 billion by 2031 at 5.1% CAGR over 2026-2031.

Rising vehicle production, stricter safety mandates, and the shift toward electric mobility are sustaining momentum even as raw-material prices and logistics costs fluctuate. Growing demand for panoramic roofs, lightweight laminated windshields, and electrochromic glazing is encouraging manufacturers to scale specialized lines and deepen partnerships with OEMs. The emphasis on larger glass surfaces in SUVs, coupled with regulatory pressure to cut CO2 emissions, is accelerating the adoption of coated and multi-functional products. Together, these forces position the automotive glass market for resilient, technology-led growth through the decade.

Global Automotive Glass Market Trends and Insights

Shift Toward Panoramic Glazing In EV Platforms

Electric-vehicle makers are installing larger roof panes to enhance cabin ambience and brand identity. Tesla's Cybertruck and Mercedes-Benz's Vision V concept integrate electrochromic roofs that modulate tint levels, cutting cabin temperatures by up to 18°F and lowering HVAC loads. Glass area per vehicle is forecast to surge, prompting suppliers to invest in wide-format bending, low-E coatings, and infrared-absorbing interlayers. This premium specification is expected to permeate mid-priced EVs as production costs fall, supporting sustained growth in the automotive glass market.

OEM Demand For Lightweight Laminated Glass To Meet CO2 Targets

European regulations set a 100 g/km fleet-average CO2 goal for 2030, pushing automakers to shave every kilogram. EPA studies of the 2017 Ford GT show laminated glazing contributed materially to a 30% mass drop. Thin-gauge laminates using ionoplast interlayers now trim weight by up to 30% without compromising impact performance. AGC and Saint-Gobain are commercializing 1.6-mm windshield constructions that pair weight savings with acoustic damping, reinforcing long-term prospects for the automotive glass market.

Supply-Chain Crunch Of Specialty Interlayers (PVB, Ionoplast)

Kuraray's PVB capacity expansions have not kept pace with rising demand for acoustic and HUD-grade films, extending lead times and forcing allocation programs. European laminators report spot shortages, compelling them to prioritize OEM production over aftermarket orders. Experimental bio-based interlayers deliver promising mechanical gains of 53.1% but remain years from scale. Short-term supply stress may temper automotive glass market growth until new plants start up.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Sunroof Penetration In SUVs

- Regulation-Led Mandatory Safety Glazing For Side Windows

- Margin Erosion From Chinese Float-Glass Overcapacity Flooding EU Market

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Regular glass commanded 82.05% of the automotive glass market share in 2025, thanks to cost efficiency and entrenched production assets. Laminated variants are gaining against tempered formats because they keep shards intact on impact, satisfying global safety norms. The shift tightens the supply of specialty interlayers, yet it positions laminators for higher value capture as OEMs demand thinner, lighter constructions. Smart glass, though only a minority today, is projected to post a 12.1% CAGR, carving out niches in luxury vehicles and high-end EVs.

Electrochromic roofs dominate early adoption; suspended particle devices (SPD) deliver faster switching and durability, as shown in Mercedes-Benz's Vision V prototype. Polymer-dispersed liquid crystal (PDLC) windows target privacy partitions, while thermochromic films remain pre-commercial. As economies of scale improve, smart glass will expand beyond flagships, bolstering the automotive glass market.

Windshields held 44.15% of the automotive glass market size in 2025, underpinned by mandatory fitment and rising ADAS sensor content. Complexity drives up unit value, reinforcing supplier-OEM co-development cycles. Sunroofs, however, are the fastest-growing application at 9.6% CAGR as SUVs standardize large openings for panoramic vistas.

Backlites see modest traction from acoustic laminates, though warranty issues temper speed. Sidelites transition to laminated construction to meet ejection-prevention laws, especially in Europe and Japan. Rear-view mirrors and quarter windows integrate electrochromic anti-glare coatings, adding feature content without large area demand. Collectively, the application mix underpins steady expansion in the automotive glass market.

The Automotive Glass Market Report is Segmented by Glass Type (Regular Glass and Smart Glass), Application (Windshield, Sunroof and More), Vehicle Type (Passenger Cars, and More), Propulsion (Internal Combustion Engine, Battery Electric Vehicle (BEV), and More), Sales Channel (OEM, and Aftermarket), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the automotive glass market, with 48.75% of the revenue in 2025, anchored by China's vast output and rapid domestic uptake. Government incentives have kept plants near capacity, while India's production climb adds a fresh demand axis. Conferences in Shanghai spotlight intelligent glazing, LiDAR transparency, and AR-HUD integration, showcasing continual innovation. Japan and South Korea supply advanced laminated and coated products for premium OEMs, preserving high-margin niches as part of the broader automotive glass market.

Producers combat margin squeeze from Chinese imports by pivoting into smart glass and sustainability programs. AGC and Saint-Gobain's joint Volta furnace evidences a strategic move to slash CO2 intensity. Meanwhile, North America remains influential due to the demand for SUVs. The United States features vibrant aftermarket activity; brands such as Auto Glass Now scale national footprints to capture replacement revenue.

The Middle East and Africa are expected to be the fastest climbers at 6.8% CAGR through 2031. Saudi Arabia's silica-rich deposits attract float-glass investments intended to localize supply. Subsidies aligned with broader industrial-diversification agendas incentivize auto-component production, broadening the region's stake in the automotive glass market. South America's outlook is tied chiefly to Brazilian assembly volumes, while Africa's growth centers on South Africa's relatively mature sector. Proximity production strategies help global suppliers balance freight costs and just-in-time expectations across these varied geographies.

- AGC Inc. (Asahi Glass)

- Saint-Gobain S.A.

- Nippon Sheet Glass Co. Ltd.

- Fuyao Glass Industry Group Co. Ltd.

- Xinyi Glass Holdings Ltd.

- Guardian Automotive (Koch Industries)

- Webasto SE

- Carlex Glass America LLC

- Magna International Inc.

- Vitro Automotive

- Corning Incorporated

- Sisecam Automotive

- Shanghai Yaohua Pilkington Glass

- Gentex Corporation

- AGP Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward Panoramic Glazing In EV Platforms

- 4.2.2 OEM Demand For Lightweight Laminated Glass To Meet CO2 Targets

- 4.2.3 Rapid Sunroof Penetration In SUVs

- 4.2.4 Regulation-Led Mandatory Safety Glazing For Side Windows

- 4.2.5 Growing Retrofit Of HUD-Compatible Windshields By Premium OEMs

- 4.2.6 Integration Of Embedded Sensors For ADAS Functionality

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Crunch Of Specialty Interlayers (PVB, Ionoplast)

- 4.3.2 Margin Erosion From Chinese Float-Glass Overcapacity Flooding EU Market

- 4.3.3 High Warranty Costs Linked To Acoustic Laminated Backlights In SUVs

- 4.3.4 Slow Replacement Cycles In Mature Aftermarket Channels

- 4.4 Value-Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 OEM vs. Aftermarket Trend Analysis

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Glass Type

- 5.1.1 Regular Glass

- 5.1.1.1 Laminated Glass

- 5.1.1.2 Tempered Glass

- 5.1.2 Smart Glass

- 5.1.2.1 Electrochromic

- 5.1.2.2 Suspended Particle Device (SPD)

- 5.1.2.3 Polymer Dispersed Liquid Crystal (PDLC)

- 5.1.2.4 Thermochromic

- 5.1.1 Regular Glass

- 5.2 By Application

- 5.2.1 Windshield

- 5.2.2 Backlite (Rear Window)

- 5.2.3 Sidelite (Side Windows)

- 5.2.4 Sunroof

- 5.2.5 Rear-view & Side-view Mirrors

- 5.2.6 Other Glazing (Quarter & Vent)

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.1.1 Hatchback

- 5.3.1.2 Sedan

- 5.3.1.3 SUV & Crossover

- 5.3.1.4 Luxury & Sports

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.3.1 Passenger Cars

- 5.4 By Propulsion

- 5.4.1 Internal Combustion Engine (ICE)

- 5.4.2 Battery Electric Vehicle (BEV)

- 5.4.3 Hybrid Electric Vehicle (HEV/PHEV)

- 5.4.4 Fuel Cell Electric Vehicles (FCEV)

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 AGC Inc. (Asahi Glass)

- 6.4.2 Saint-Gobain S.A.

- 6.4.3 Nippon Sheet Glass Co. Ltd.

- 6.4.4 Fuyao Glass Industry Group Co. Ltd.

- 6.4.5 Xinyi Glass Holdings Ltd.

- 6.4.6 Guardian Automotive (Koch Industries)

- 6.4.7 Webasto SE

- 6.4.8 Carlex Glass America LLC

- 6.4.9 Magna International Inc.

- 6.4.10 Vitro Automotive

- 6.4.11 Corning Incorporated

- 6.4.12 Sisecam Automotive

- 6.4.13 Shanghai Yaohua Pilkington Glass

- 6.4.14 Gentex Corporation

- 6.4.15 AGP Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment