|

시장보고서

상품코드

1939113

접착제 및 실란트 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

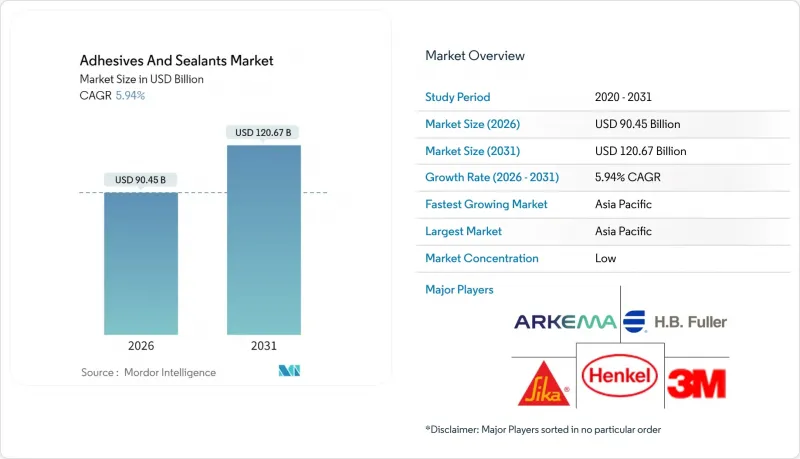

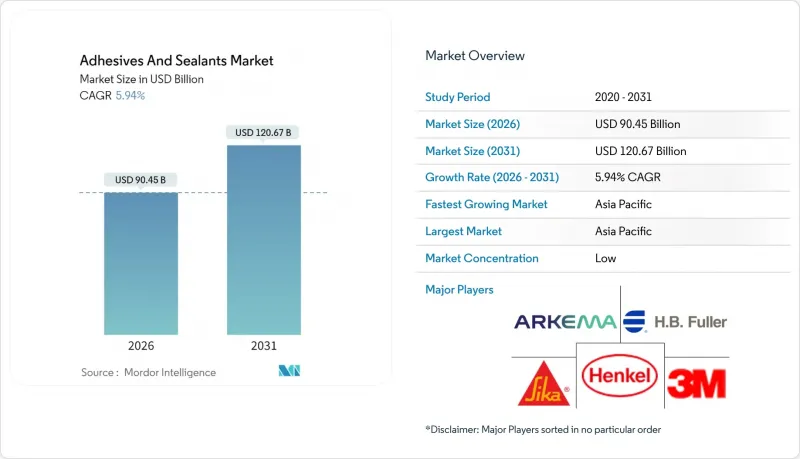

접착제 및 실란트 시장 규모는 2026년에는 904억 5,000만 달러로 추정되며, 2025년 853억 8,000만 달러에서 성장이 전망됩니다.

2031년에는 1,206억 7,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 5.94%로 성장할 것으로 전망됩니다.

자동차 경량화, 자동화된 EC 포장, 모듈식 건축을 지원하는 고성능 접착 솔루션에 대한 수요 증가로 인해 견고한 성장세를 보이고 있습니다. 특히 EU 그린딜에 따른 저배출 화학제품에 대한 규제 압력으로 인해 바이오 기반 및 저 VOC 배합으로의 전환이 가속화되고 있습니다. 아시아태평양은 산업 확대와 인프라 투자에 힘입어 성장을 견인할 것입니다. 한편, 북미와 유럽에서는 엄격한 지속가능성 기준을 충족하는 기술 업그레이드에 집중하고 있습니다. 이소시아네이트와 아크릴 모노머의 공급망 취약성은 가격에 지속적으로 영향을 미치고 있으며, 제조업체들은 원료의 다양화 및 바이오 기반 제법에 대한 투자를 촉진하고 있습니다. 경쟁 환경은 우수한 내구성, 고온 저항성, 가공 속도 향상을 약속하는 실리콘 및 반응성 기술로 점점 더 많은 변화를 겪고 있습니다.

세계 접착제 및 실란트 시장 동향과 인사이트

경량 복합재 차량 조립의 급증으로 구조용 접착제 수요 증가 견인

전기자동차 제조업체들은 경량화, 충돌 성능 향상, 알루미늄, 복합재, 고강도 강철의 접합을 위해 용접과 리벳을 구조용 접착제로 대체하고 있습니다. 접착제는 배터리 하우징을 고정하는 데도 사용되며 열 관리 및 전기 절연을 제공합니다. 팩 내부의 열 계면 재료는 폭주를 방지하고 배터리 수명을 연장하기 때문에 접착제 및 실란트 시장 내에서 특별한 틈새 시장을 형성하고 있습니다. 자동차 제조업체는 접착 기술이 광범위한 온도 변화에도 치수 안정성을 유지하고 차량 수명 내내 유체에 노출되는 것을 견딜 수 있기를 기대합니다. 이러한 까다로운 요구로 인해 배합 기술자들은 강도와 유연성을 겸비한 반응성 폴리우레탄 핫멜트 및 변성 에폭시 수지의 개발을 추진하고 있습니다. 따라서 EV 보급률의 확대는 접착제 및 실란트 시장의 구조적 수요의 촉매제 역할을 하고 있습니다.

빠르게 성장하는 세계 EC 시장이 요구하는 고성능 포장용 접착 솔루션

소비자 직송 배송에서 골판지 상자는 진동, 습도 및 극한의 온도에 노출되기 때문에 브랜드 소유자는 복잡한 물류 체인 전체에서 포장을 밀봉 상태로 유지하기 위해 고점착성 핫멜트 또는 수성 시스템을 채택합니다. 포장 분야는 접착제 및 실란트 시장의 43%를 차지하고 있으며, E-Commerce 물량 증가에 따라 지속적으로 확대되고 있습니다. 지속가능성 기준은 재활용이 가능한 접착제를 요구하고 있으며, 헨켈과 팍스 사이즈는 바이오 기반 핫멜트 '에코팍스'를 도입했습니다. 이는 연간 3억 4,000만 상자 생산 시 온실가스 배출량을 32% 감축할 수 있는 수치입니다. 자동 케이스 조립 라인에서는 에너지 절약을 위해 저온에서 유동하는 저점도 등급도 필요합니다. 이러한 촉진요인에 대한 혁신이 접착제 및 실란트 시장의 꾸준한 물량 성장을 뒷받침하고 있습니다.

불안정한 이소시아네이트 아크릴 단량체 공급망으로 인한 비용 압박

새로운 EU 규정에 따라 유리 이소시아네이트 함량이 0.1%를 초과하는 폴리우레탄계 제품을 취급하는 사람은 특별 교육을 의무적으로 받아야 하며, 관리 비용이 증가하고 중소 컨버터들의 진입이 제한되고 있습니다. 동시에 아크릴산 공급 부족으로 인해 가격 변동성이 높아져 최종사용자는 분기별로 계약을 재협상해야 하는 상황에 처해 있습니다. 생산자들은 원료 조달을 지역화하고, 식물성 기름에서 유래한 바이오 루트를 채택하여 헤지를 시도하고 있지만, 이러한 조치에는 자본 지출이 수반되어 수익률을 압박하고 있습니다. 원자재 가격 지수의 급등은 다운스트림 가격으로 파급되어 건설 및 자동차 분야의 프로젝트 승인이 지연되고 있습니다. 접착제 및 실란트 시장은 성능 유지와 비용 상승 사이의 균형을 찾아야 하며, 이러한 미묘한 조정이 성장 전망을 억제하는 요인으로 작용하고 있습니다.

부문 분석

2025년 아크릴 수지는 접착제 및 실란트 시장 매출의 23.45%를 차지했습니다. 다양한 기판과의 궁합과 합리적인 비용을 인정받았기 때문입니다. 그러나 실리콘이 2026년부터 2031년까지 8.23%의 CAGR을 보이는 것은 고온 및 내후성 응용 분야, 특히 자동차 전장 및 건축 외장 분야로의 전환을 시사합니다. 이러한 변화는 성능 차별화가 주도하고 있습니다. 실리콘계 접착제는 -50℃에서 200℃ 범위에서 탄성을 유지하고, 전기 절연성을 유지하며, 자외선 열화를 견딜 수 있어 LED 어셈블리 및 5G 안테나 모듈에 적합합니다. 이에 비해 아크릴계는 기능성 모노머의 개질을 통해 경화 속도를 향상시키고, 저표면 에너지 플라스틱에 대한 접착력을 높인 차세대 배합으로 대응하고 있습니다. 폴리우레탄은 동적 하중에 노출되는 구조적 접합부에 대한 선택이 계속되고 있으며, 시아노아크릴레이트는 정밀 의료기기 및 소비자 전자기기 응용 분야에 활용되고 있습니다. 글리세롤과 리그닌으로 생산되는 바이오 기반 에폭시는 초기 단계의 잠재력을 보여주며 접착제 및 실란트 산업에서 탈탄소화가 점진적으로 진행될 것임을 시사합니다.

수성 시스템은 지역별 VOC 규제에 대한 적합성과 다공성 기판에 대한 견고한 접착력을 바탕으로 2025년 매출의 41.70%를 차지할 것으로 예상됩니다. 골판지 상자 밀봉, 라벨 라미네이션, 가구 조립과 같은 접착제 및 실란트 시장의 중요한 하위 부문에서 지배적인 위치를 차지하고 있습니다. 고분자 분산 기술의 발전으로 건조 시간이 단축되어 자동화 라인의 기존 속도 제약이 해소되었습니다.

반응성 기술은 열경화성 네트워크에 가교 결합하여 에폭시 수지로만 가능했던 구조적 강도를 구현함으로써 접착제 및 실란트 업계에서 가장 빠른 7.98%의 CAGR을 달성하고 있습니다. 반응성 폴리우레탄 핫멜트는 습기 노출 후 최종 화학적 결합 외에도 즉각적인 초기 강도를 제공하여 가전 및 운송 장비 제조업체의 조립 시간을 단축합니다. UV 경화형 아크릴레이트계는 용제 배제 및 신속한 처리가 필수적인 전자기기 및 의료기기 분야에 대응합니다. 솔벤트 기반 및 고무 기반 시스템은 자동차 내장재 및 신발과 같은 틈새 응용 분야에서 여전히 사용되고 있으며, 독특한 점착성과 박리 강도의 균형이 규제 장벽을 상쇄하고 있습니다.

지역별 분석

아시아태평양은 2025년 세계 매출의 36.70%를 차지할 것으로 예상되며, 인프라 메가 프로젝트와 아세안 국가로의 전자부품 공급망 이전을 배경으로 CAGR 6.44%로 성장하고 있습니다. 중국에서는 고속철도와 재생에너지에 대한 대규모 투자가 지속되고 있으며, 구조용 실란트 및 풍력 블레이드 접착 시스템에 대한 수요를 자극하고 있습니다. 인도의 1조 4,000억 달러 규모의 국가 인프라 계획은 도로, 공항, 저가 주택용 접착제 수요를 창출할 것입니다. 베트남과 한국의 전자기기 제조는 반도체 및 디스플레이 패널용 저공극, 고열전도성 접착제에 대한 지역적 수요를 심화시키고 있습니다. 이러한 분야에서 온도 안정성을 지속적으로 추구하기 때문에 실리콘 제품이 가장 큰 혜택을 받고 있으며, 아시아태평양이 접착제 및 실란트 시장에서 선도적인 위치를 유지하는 요인으로 작용하고 있습니다.

북미는 성숙한 시장으로 기술적 차별화와 빠른 규제 대응이 중요시되는 시장입니다. 미국의 전기자동차 생산량은 2024년 100만 대를 돌파할 것으로 예상되며, 배터리 팩과 바디인화이트 조립용 구조용 및 내충격성 접착제의 소비가 증가하고 있습니다. 교량 및 광대역에 대한 연방정부의 자금 투입으로 인해 가혹한 기후에서도 유연성을 유지하는 토목용 실란트에 대한 수요가 더욱 증가하고 있습니다. 캐나다 목조건축에서는 기밀성 향상으로 인한 에너지 절약 효과를 가져오는 폴리우레탄 접착제의 채택이 가속화되고 있습니다. 접착제 및 실란트 시장은 CARB(캘리포니아 대기자원국) 및 EPA(미국 환경보호청)의 VOC 규제에 부합하는 수계 대체품의 도입으로 5% 내외의 안정적인 성장세를 유지하고 있습니다.

유럽에서는 2050년까지 탄소 중립 제품을 요구하는 EU 그린딜의 요구가 시장을 주도하고 있습니다. 제조업체들은 시장 접근성을 유지하기 위해 리그닌계 페놀계 대체품 및 바이오 재생 에폭시 수지로의 전환을 가속화하고 있습니다. 독일과 북유럽의 조립식 공장에서는 크로스 라미네이트 목재 모듈에 인증된 저VOC 접착제를 사용하여 창문과 파사드 씰링용 실리콘 수요를 촉진하고 있습니다. 유럽의 접착제 및 실란트 시장은 엄격한 품질 요구 사항의 혜택을 누리고 있지만, 규정 준수 비용이 EBIT 마진을 압박하고 있습니다. 동유럽의 자동차 공장은 생산기지를 확장하고 있으며, 이 지역의 접착제 수요를 증폭시키고 있습니다.

남미는 작지만 활기찬 시장입니다. 브라질의 주택 부족은 정부 주도의 사회 프로그램을 촉진하고, 저비용 주택을 위해 실리콘 및 아크릴계 실란트가 채택되고 있습니다. 아르헨티나의 농업 포장 분야에서는 장기 보관 및 수출 경로에 대응하기 위해 핫멜트 제품의 업데이트가 진행되고 있습니다. 칠레의 광산에서는 내산성이 우수한 하이브리드 실란트가 사용되어 접착제 및 실란트 시장 내에서 틈새 성장 영역을 형성하고 있습니다.

중동 및 아프리카에서는 사우디아라비아의 네오엠 도시계획, 나이지리아의 라고스 이바단 철도 등 인프라 구축에 대한 의지가 높아지고 있습니다. 가혹한 기후 조건으로 인해 자외선 및 먼지 저항성이 우수한 실리콘계 및 폴리설파이드계 실란트에 대한 수요가 증가하고 있습니다. 걸프 국가의 수입 대체 정책은 현지 접착제 공장 설립을 촉진하여 운송 비용과 납기를 단축하고 있습니다. 전반적으로, 다양한 기후 조건과 규제 상황이 접착제 및 실란트 시장에서 지역 플레이어의 제품 라인업을 차별화하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09Adhesives And Sealants Market size in 2026 is estimated at USD 90.45 billion, growing from 2025 value of USD 85.38 billion with 2031 projections showing USD 120.67 billion, growing at 5.94% CAGR over 2026-2031.

Strong gains stem from rising demand for high-performance bonding solutions that support light-weighting in vehicles, automated e-commerce packaging, and modular construction. Regulatory pressure for lower-emission chemistries, especially under the EU Green Deal, is accelerating the shift toward bio-based and low-VOC formulations. Asia-Pacific remains the growth engine, supported by industrial expansion and infrastructure spending, while North America and Europe focus on technology upgrades that meet strict sustainability rules. Supply chain fragility for isocyanates and acrylic monomers continues to influence pricing, prompting producers to diversify feedstocks and invest in bio-based routes. Competitive dynamics are increasingly shaped by silicone and reactive technologies, which promise superior durability, higher temperature resistance, and improved processing speeds.

Global Adhesives And Sealants Market Trends and Insights

Surge in Lightweight Multi-material Vehicle Assemblies Boosting Structural Adhesive Uptake

Electric-vehicle makers are replacing welds and rivets with structural adhesives to save weight, improve crash performance, and enable joining of aluminum, composites, and high-strength steel. Adhesives also secure battery housings, where they manage heat and provide electrical insulation. Thermal interface materials inside packs prevent runaway and extend battery life, creating a specialized niche within the adhesives and sealants market. Automakers expect bonding technologies to remain dimensionally stable across wide temperature swings and resist fluid exposure for the entire vehicle lifespan. Such stringent requirements are pushing formulators toward reactive polyurethane hot-melts and modified epoxies that combine strength with flexibility. Growing EV penetration therefore acts as a structural demand catalyst for the adhesives and sealants market.

Explosive Growth of E-commerce Requiring High-Performance Packaging Adhesive Solutions Globally

Direct-to-consumer shipping exposes cartons to vibration, humidity, and temperature extremes, prompting brand owners to adopt high-tack hot-melt and water-based systems that keep packages sealed throughout complex logistics chains. Packaging represents 43% of the adhesives and sealants market and continues to expand as e-commerce volumes rise. Sustainability standards now require adhesives compatible with recycling streams; Henkel and Packsize introduced Eco-Pax, a bio-based hot-melt that can cut greenhouse gas emissions by 32% per 340 million boxes produced annually. Automated case-erection lines also demand low-viscosity grades that flow at reduced temperatures to save energy. Innovation in this driver underpins steady volume growth in the adhesives and sealants market.

Volatile Isocyanate & Acrylic Monomer Supply Chains Creating Cost Pressures

New EU rules require special training for anyone handling polyurethane systems with greater than 0.1% free isocyanate, adding administrative cost and limiting smaller converters' access. Parallel tightness in acrylic acid supply elevates price volatility, prompting end users to renegotiate contracts quarterly. Producers hedge by localizing feedstock procurement and adopting bio-routes from vegetable oils, yet these measures involve capital outlays that weigh on margins. Sudden spikes in raw-material indices ripple through downstream prices, delaying project approvals in construction and automotive. The adhesives and sealants market must therefore navigate cost inflation while maintaining performance, a balancing act that tempers the growth outlook.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Modular & Prefabricated Construction Methods in Asia-Pacific

- EU Green Deal & Global Regulatory Push Accelerating Bio-based, Low-VOC Adhesives

- Stringent Environmental Regulations Regarding VOC Emissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic resins generated 23.45% of the adhesives and sealants market revenue in 2025, favored for broad substrate compatibility and moderate cost. Nevertheless, silicone's 8.23% CAGR over 2026-2031 signals a pivot toward high-temperature, weather-resistant applications, notably in automotive electronics and building facades. Performance differentiation drives this shift. Silicone adhesives retain elasticity from -50 °C to 200 °C, remain electrically insulating, and resist UV degradation, making them fit for LED assemblies and 5G antenna modules. Acrylics respond with next-generation formulations that cure faster and bond low-surface-energy plastics through functional monomer modifications. Polyurethane remains the choice for structural joints exposed to dynamic loads, while cyanoacrylates serve precision medical and consumer electronics uses. Bio-based epoxies produced from glycerol and lignin showcase early-stage potential, signaling a gradual decarbonization of the adhesives and sealants industry.

Water-based systems held 41.70% revenue in 2025, aided by compliance with regional VOC caps and robust adhesion on porous substrates. They dominate corrugated box sealing, label lamination, and furniture assembly, all critical subsegments of the adhesives and sealants market. Product advances in polymer dispersion lower drying times, addressing historical speed constraints on automated lines.

Reactive technologies deliver the fastest 7.98% CAGR in the adhesives and sealants industry because they crosslink into thermoset networks, achieving structural strength once considered exclusive to epoxies. Reactive polyurethane hot-melts supply instant green strength plus final chemical bonding after moisture exposure, reducing assembly time for appliance and transportation manufacturers. UV-cured acrylates address electronics and medical devices where solvent elimination and rapid throughput are essential. Solvent-borne and rubber-based systems persist in niche uses, such as automotive interior trim and footwear, where their unique balance of tack and peel strength offsets regulatory hurdles.

The Adhesives and Sealants Market Report is Segmented by Adhesive Resin (Polyurethane, Epoxy, and More), Adhesives Technology (Solvent-Borne, Reactive, and More), Sealant Resin (Silicone, Polyurethane, and More), End-User Industry (Aerospace, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 36.70% of global revenue in 2025 and is growing at 6.44% CAGR, driven by infrastructure megaprojects and the relocation of electronics supply chains into ASEAN nations. China continues large-scale high-speed rail and renewable-energy investments, stimulating demand for structural sealants and wind blade bonding systems. India's USD 1.4 trillion National Infrastructure Pipeline channels adhesive consumption into roads, airports, and affordable housing. Electronics manufacturing in Vietnam and South Korea deepens regional requirements for low-void, high-thermal-conductivity adhesives used in semiconductors and display panels. Silicone products benefit most, given relentless pursuit of temperature stability in these sectors, ensuring Asia-Pacific retains primacy within the adhesives and sealants market.

North America represents a mature arena emphasizing technology differentiation and rapid regulatory alignment. U.S. electric-vehicle output surpassed 1 million units in 2024, raising consumption of structural, crash-durable adhesives for battery packs and body-in-white assemblies. Federal funding for bridges and broadband further elevates demand for civil-engineering sealants that remain flexible under extreme climates. Canadian wood-frame construction accelerates adoption of polyurethane adhesives that improve energy efficiency through airtight assemblies. The adhesives and sealants market shows steady mid-single-digit growth as producers offer drop-in water-borne alternatives conforming to CARB and EPA VOC limits.

Europe is shaped by the EU Green Deal's call for carbon-neutral products by 2050. Manufacturers accelerate the transition to lignin-based phenolic alternatives and bio-renewable epoxies to retain market access. German and Nordic prefabrication plants rely on certified low-VOC adhesives in cross-laminated timber modules, reinforcing silicone demand for window and facade sealing. The adhesives and sealants market in Europe benefits from stringent quality expectations, though compliance costs lower EBIT margins. Eastern European vehicle plants broaden production footprints, amplifying regional adhesive requirements.

South America remains a small but vibrant arena. Brazil's housing deficit spurs government-funded social programs that channel silicone and acrylic sealants into low-cost housing. Argentina's agricultural packaging sector benefits from hot-melt upgrades to address prolonged storage and export routes. Chilean miners apply hybrid sealants that withstand acid exposure, adding niche growth pockets inside the adhesives and sealants market.

The Middle East & Africa lean on infrastructure ambitions such as Saudi Arabia's NEOM city and Nigeria's Lagos-Ibadan railway. Harsh climates reward silicone and polysulfide sealants with elevated UV and sand-abrasion resistance. Import substitution policies in the Gulf encourage local adhesive plants, reducing freight costs and delivery times. Overall, diverse climatic and regulatory landscapes shape differentiated product lineups for regional players in the adhesives and sealants market.

- 3M

- Aica Kogyo Co. Ltd.

- Akzo Nobel N.V.

- Arkema S.A. (Bostik)

- Avery Dennison Corporation

- DELO Industrial Adhesives

- DIC Corporation

- Dow

- DuPont

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- MAPEI S.p.A.

- Nanpao Resins Chemical Group

- Parker Hannifin

- Permabond LLC

- Pidilite Industries Ltd.

- RPM International Inc.

- Sika AG

- Soudal Group

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Lightweight Multi-material Vehicle Assemblies Boosting Structural Adhesive Uptake

- 4.2.2 Explosive Growth of E-commerce Requiring High-Performance Packaging Adhesive Solutions Globally

- 4.2.3 Rapid Expansion of Modular and Prefabricated Construction Methods in Asia-Pacific

- 4.2.4 EU Green Deal and Global Regulatory Push Accelerating Bio-based, Low-VOC Adhesives

- 4.2.5 Healthcare Wearables Adoption Driving Medical-grade Reactive Hot-Melt Adhesives

- 4.3 Market Restraints

- 4.3.1 Volatile Isocyanate and Acrylic Monomer Supply Chains Creating Cost Pressures

- 4.3.2 Stringent Environmental Regulations Regarding VOC Emissions

- 4.3.3 Low Substitution Cost of Mechanical Fasteners in Emerging Markets Limiting Penetration

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Adhesive Resin

- 5.1.1 Polyurethane

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Silicone

- 5.1.5 Cyanoacrylate

- 5.1.6 VAE / EVA

- 5.1.7 Other Resins (Polyester, Rubber, etc.)

- 5.2 By Adhesive Technology

- 5.2.1 Solvent-borne

- 5.2.2 Reactive

- 5.2.3 Hot Melt

- 5.2.4 UV-cured

- 5.2.5 Water-borne

- 5.3 By Sealant Resin

- 5.3.1 Silicone

- 5.3.2 Polyurethane

- 5.3.3 Acrylic

- 5.3.4 Epoxy

- 5.3.5 Other Resins (Bituminous, Polysulfide UV-curable, etc.)

- 5.4 By End-user Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging (Paper and Flexible)

- 5.4.7 Woodwork and Joinery

- 5.4.8 Other End-user Industries (Electronics, Consumer/DIY, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Indonesia

- 5.5.1.6 Malaysia

- 5.5.1.7 Thailand

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Turkey

- 5.5.3.8 Nordic Countries

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Algeria

- 5.5.5.7 Rest of Middle and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments}

- 6.4.1 3M

- 6.4.2 Aica Kogyo Co. Ltd.

- 6.4.3 Akzo Nobel N.V.

- 6.4.4 Arkema S.A. (Bostik)

- 6.4.5 Avery Dennison Corporation

- 6.4.6 DELO Industrial Adhesives

- 6.4.7 DIC Corporation

- 6.4.8 Dow

- 6.4.9 DuPont

- 6.4.10 Dymax

- 6.4.11 H.B. Fuller Company

- 6.4.12 Henkel AG & Co. KGaA

- 6.4.13 Illinois Tool Works Inc.

- 6.4.14 MAPEI S.p.A.

- 6.4.15 Nanpao Resins Chemical Group

- 6.4.16 Parker Hannifin

- 6.4.17 Permabond LLC

- 6.4.18 Pidilite Industries Ltd.

- 6.4.19 RPM International Inc.

- 6.4.20 Sika AG

- 6.4.21 Soudal Group

- 6.4.22 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 Increasing Awareness of Renewable and Eco-friendly Products

- 7.2 White-space and Unmet-need Assessment