|

시장보고서

상품코드

1939117

테라헤르츠 기술 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Terahertz Technologies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

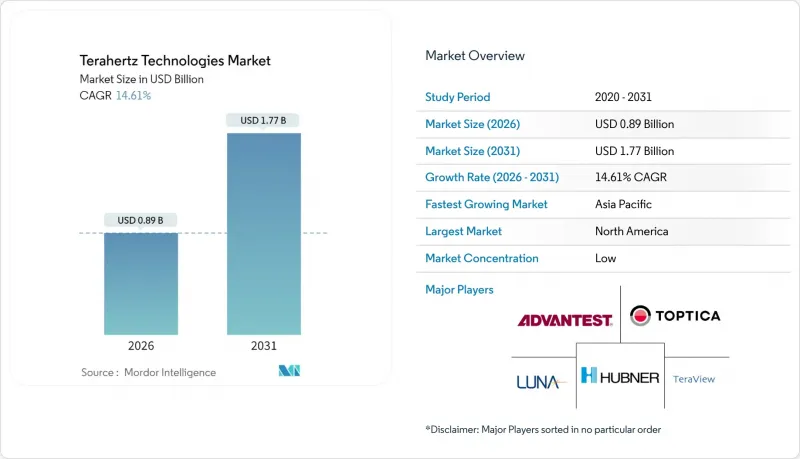

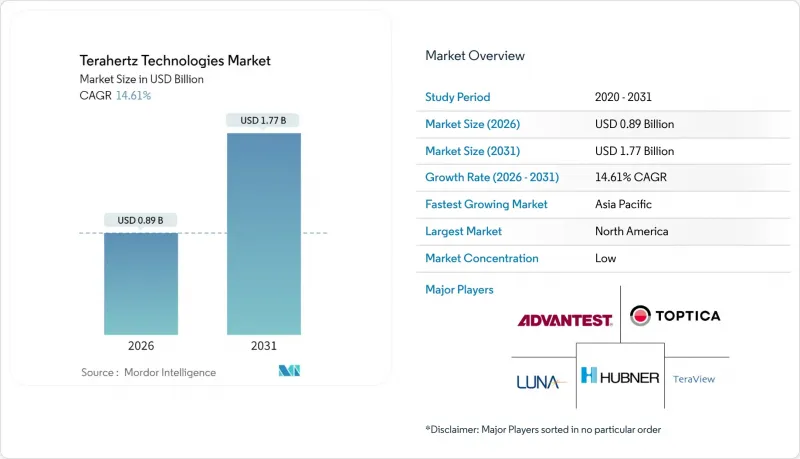

테라헤르츠 기술 시장은 2025년 7억 8,000만 달러에서 2026년에는 8억 9,000만 달러로 성장하며, 2026-2031년에 CAGR 14.61%로 추이하며, 2031년까지 17억 7,000만 달러에 달할 것으로 예측되고 있습니다.

소형 광 집적 광원의 혁신, 6G 실증 백홀 링크의 확대, 제약 기업의 실시간 인라인 품질관리로의 전환이 상용화를 가속화하고 있습니다. 중주파수 시스템(1-5 THz)은 대기 투과율과 이미지 해상도의 균형으로 수요가 유지되고 있으며, 5 THz 이상의 고주파 시스템은 정밀 측정 및 고데이터 레이트 조사 분야에서 주목받고 있습니다. 의료 분야가 가장 큰 최종사용자이지만, 6G 주파수 전략이 구체화됨에 따라 통신 분야가 가장 급격한 성장을 기록하고 있습니다. 벤더들의 산업별 전문화로 인해 분절화는 계속되고 있지만, 가치는 개별 부품에서 AI 기반 분석 기능을 갖춘 턴키 플랫폼으로 이동하고 있습니다.

세계 테라헤르츠 기술 시장 동향과 인사이트

소형 광 집적형 테라헤르츠 광원의 발전 추세

실리콘 포토닉스 기술로 테라헤르츠 엔진이 소형화되어 부피가 큰 극저온 냉각장치가 불필요해져 개별 구조 대비 설치 면적이 75% 감소했습니다. TOPTICA는 상온에서 3THz까지 10mW/cm2 이상의 출력을 구현하는 모놀리식 양자 캐스케이드 레이저의 통합에 성공하여, 예상 기간 내에 단가를 몇 배로 절감할 수 있는 양산화의 길을 열었습니다.

6G 백홀 실증 시험 급증

NTT도코모와 후지쯔는 2024년 도시 지역 시험에서 300GHz 대역에서 1km 거리를 100Gbps로 전송하는 데 성공하여 고밀도 스몰셀 구성에서 테라헤르츠 기술의 실현 가능성을 입증했습니다. 삼성도 비슷한 데이터 속도를 달성함과 동시에 밀리파 방식 대비 소비전력을 40% 절감했습니다.

대기 투과성 창문의 제한으로 인해 야외 링크가 제한됨

수증기 흡수로 인해 220GHz, 340GHz, 650GHz 부근의 좁은 대역 외에는 100 dB/km의 손실이 발생합니다. 따라서 정밀한 주파수 제어가 필수적이며, 야외 링크는 단거리 또는 통제된 환경에서의 작동으로 제한됩니다.

부문 분석

테라헤르츠 이미징은 제약, 보안, 비파괴 검사 분야에서의 도입이 성숙해지면서 2025년 기준 테라헤르츠 기술 시장의 41.32%를 차지할 것으로 예측됩니다. 통신 플랫폼은 현재 매출 기여도가 낮지만, 6G 아키텍처가 공식화됨에 따라 15.46%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장할 것으로 예측됩니다. 로슈의 코팅 검사에서 99.8%에 달하는 강력한 결함 검출 정확도는 이미징의 고부가가치 제안을 지원하는 기반이 되고 있습니다. 한편, 통신 분야는 표준화 이정표에 의존하고 있습니다.

수요 동향은 초기 도입자가 이미징 분야에서 확립된 투자수익률(ROI)을 활용하는 한편, 네트워크 사업자는 밀집된 도심지 네트워크의 광섬유 부하 경감을 위해 멀티 기가비트 링크의 시험 운용을 추진하고 있습니다. 하드웨어 벤더들은 AI 지원 분석 기능을 번들로 제공하고, 제약 MES(제조 실행 시스템) 및 통신 오케스트레이션 스택에 쉽게 통합할 수 있도록 함으로써 성능 데이터를 활용하는 소프트웨어 구독 매출으로의 전환을 촉진하고 있습니다.

1-5 THz 대역에서 작동하는 플랫폼은 우수한 전송 대 해상도 비율로 인해 2025년 테라헤르츠 기술 시장 점유율의 38.20%를 차지할 것으로 예측됩니다. 고주파 대역(5 THz 이상) 시스템은 초기 단계이지만, 주파수 증폭기 체인이 6 THz 이상에서 성숙해짐에 따라 15.81%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 버지니아 다이오드의 고체 증폭기는 안정적인 출력을 실현하고, 나노미터 단위의 정밀 계측을 가능하게 함으로써 대응 가능한 이용 사례를 확대하고 있습니다.

중간 대역은 공급망 성숙과 부품 가격 하락으로 기존 우위를 유지합니다. 반도체 선폭 측정, 적층형 격자 검사, 양자 재료 연구 등 극한 해상도가 새로운 가치를 창출하는 분야에서 고 대역폭의 채택이 증가하여 광학 조정의 복잡성 증가를 상쇄할 것으로 예측됩니다.

지역별 분석

북미는 2025년 34.45% 시장 점유율을 확보했습니다. 이는 1억 5,000만 달러의 연방 연구 보조금, 스탠드오프 스캐너의 국방 조달, PAT 준수를 요구하는 제약업계의 기존 기업에 의한 추진에 따른 것입니다. 산학 컨소시엄은 공유 클린룸 시설과 지적재산권 풀을 통해 사업화를 가속화하고, 스타트업의 컨셉에서 파일럿까지 사이클을 단축하고 있습니다. 캐나다의 광업 및 펄프 및 제지 부문은 원격 광석 및 섬유 등급 분류를 위해 견고한 테라헤르츠 이미저를 통합하고 있습니다.

아시아태평양은 17.55%의 연평균 복합 성장률(CAGR)로 성장을 이끌었습니다. 중국 사업자가 테라헤르츠 6G 연구개발에 20억 달러 이상을 투자하고, 일본 정밀 공구업체가 중파장대 프로브를 측정 벤치에 통합했습니다. 한국에서는 EUV 반도체 공장에 THz 분석 기술을 도입하여 다이본딩 균일성 검사 실시. 인도 제네릭 의약품 제조업체는 수출 약전 기준 대응을 위해 인라인 분광계를 도입했습니다. 정부의 강력한 보조금과 국내 공급망 확대가 비용 절감을 촉진합니다.

유럽에서는 자동차 경량화, 제약 연속 제조, Horizon Europe 연구개발(2억 유로=2억 1,400만 달러 상당)을 기반으로 꾸준한 보급이 이루어지고 있습니다. 독일 기계 제조업체는 테라헤르츠 트랜시버를 인더스트리 4.0 로봇에 통합하고, 북유럽 항공우주 기업은 고 대역폭 이미저를 복합재 박리 검사에 활용하고 있습니다. 중동의 에너지 기업은 하이드레이트 매핑을 위한 유정 감지 툴을 시험 운영하고 있으며, 브라질의 농업 관련 기업은 옥수수 수출을 위한 아플라톡신 검출용 핸드헬드 스캐너를 시험 도입했습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The terahertz technologies market is expected to grow from USD 0.78 billion in 2025 to USD 0.89 billion in 2026 and is forecast to reach USD 1.77 billion by 2031 at 14.61% CAGR over 2026-2031.

Breakthroughs in compact photonic-integrated sources, the expansion of 6G proof-of-concept backhaul links, and pharmaceutical companies' shift toward real-time inline quality control are accelerating commercialization. Mid-frequency systems (1-5 THz) sustain demand by balancing atmospheric transmission with imaging resolution, while high-frequency systems above 5 THz attract precision metrology and high-data-rate research. Healthcare remains the largest end user, yet telecommunications records the steepest growth as 6G spectrum strategies crystallize. Fragmentation persists because vendors specialize by vertical; value is migrating from discrete components to turnkey platforms with AI-driven analytics.

Global Terahertz Technologies Market Trends and Insights

Advances in compact photonic-integrated THz sources

Silicon photonics has shrunk terahertz engines, eliminating bulky cryocoolers and cutting the footprint by 75% relative to discrete architectures. TOPTICA demonstrated monolithic quantum-cascade-laser integration delivering >10 mW/cm2 at room temperature up to 3 THz, opening mass-manufacturing pathways that can slash per-unit costs by an order of magnitude within the outlook period.

Surge in 6G backhaul proof-of-concept installations

NTT DOCOMO and Fujitsu achieved 100 Gbps over 1 km at 300 GHz in urban trials in 2024, validating the feasibility of terahertz technology for dense small-cell topologies. Samsung logged similar data rates while lowering power consumption by 40% compared to millimeter-wave alternatives.

Limited atmospheric transmission windows constrain outdoor links

Water-vapor absorption imposes 100 dB/km losses outside narrow bands near 220 GHz, 340 GHz, and 650 GHz, forcing precise frequency control and restricting outdoor spans to short ranges or controlled climates.

Other drivers and restraints analyzed in the detailed report include:

- Rising adoption in inline pharmaceutical QA/QC

- Defense demand for millimeter-resolution passive standoff scanners

- Cryogenic cooling requirements for high-power QCL sources

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Terahertz imaging retained 41.32% of the terahertz technology market in 2025 as pharmaceutical, security, and non-destructive testing installations matured. Communication platforms contribute modest revenue today, yet are set to expand fastest at 15.46% CAGR as 6G architectures formalize. Robust defect-detection accuracy-99.8% in Roche's coating inspections-underpins imaging's premium value proposition, whereas communications hinge on standard-setting milestones.

Demand patterns show early adopters capitalizing on established ROI for imaging, while network operators trial multi-gigabit links to offload fiber in dense urban grids. Hardware vendors bundle AI-enabled analytics, easing integration into pharmaceutical MES or telecom orchestration stacks, thereby shifting revenue toward software subscriptions that monetize performance data.

Platforms operating 1-5 THz commanded 38.20% of the terahertz technologies market share in 2025 thanks to favorable transmission-to-resolution ratios. High-band (>5 THz) systems, though nascent, should log 15.81% CAGR as frequency-multiplier chains mature beyond 6 THz. Solid-state multipliers from Virginia Diodes now deliver stable output enabling nanometer-precision metrology, broadening addressable use cases.

Mid-band incumbency benefits from supply-chain maturity and lower component prices. High-band adoption will rise where extreme resolution unlocks new value, such as in semiconductor linewidth metrology, additive-manufactured lattice inspection, and quantum materials research, offsetting the higher optical-alignment complexity.

The Terahertz Technologies Market Report is Segmented by Application Category (Terahertz Imaging Systems, and More), Frequency Range (Low-Frequency Terahertz, and More), End User (Healthcare, Defense and Security, and More), Component Type (Terahertz Sources, Terahertz Detectors, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America secured 34.45% market share in 2025, propelled by USD 150 million federal research grants, defense procurement of standoff scanners, and pharmaceutical incumbents seeking PAT compliance. Academic-industry consortia accelerate commercialization through shared clean-room facilities and IP pools, shortening concept-to-pilot cycles for start-ups. Canadian mining and pulp-and-paper sectors integrate ruggedized THz imagers for remote ore and fiber-grade classification.

Asia-Pacific leads growth at 17.55% CAGR as Chinese operators earmark over USD 2 billion for terahertz 6G R&D and Japanese precision-tool vendors integrate mid-band probes into metrology benches. South Korea embeds THz analytics in EUV semiconductor fabs for die-bond uniformity checks, and Indian generics producers deploy inline spectrometers to meet export pharmacopeia standards. Robust government subsidies and domestic supply-chain scaling compress cost curves.

Europe charts steady uptake anchored in automotive lightweighting, pharmaceutical continuous manufacturing, and Horizon Europe R&D funding worth EUR 200 million (USD 214 million). German machine builders bundle terahertz transceivers into Industry 4.0 robotics, while Nordic aerospace firms use high-band imagers for composite delamination audits. Middle East energy companies pilot well-logging tools for hydrate mapping, and Brazilian agribusinesses trial handheld scanners for aflatoxin detection in corn exports.

- ADVANTEST Corporation

- Luna Innovations Incorporated

- TeraView Limited

- TOPTICA Photonics AG

- HUBNER GmbH and Co. KG

- BATOP GmbH

- Microtech Instruments Inc.

- Menlo Systems GmbH

- Gentec-EO Inc.

- Bakman Technologies LLC

- QMC Instruments Ltd

- Bruker Corporation

- Lytid SAS

- Attocube Systems AG

- Helmut Fischer GmbH

- Baugh and Weedon Ltd

- Das-nano S.L.

- Teravil Ltd

- Terasense Group Inc.

- Virginia Diodes Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advances in compact photonic-integrated THz sources

- 4.2.2 Surge in 6G-backhaul proof-of-concept installations

- 4.2.3 Rising adoption in inline pharmaceutical QA/QC

- 4.2.4 Defense demand for mm-resolution passive standoff scanners

- 4.2.5 Accelerating deployment of MHz-repetition ultrafast laser-pumped THz systems

- 4.2.6 Government-funded astronomy payloads requiring cryogenic THz detectors

- 4.3 Market Restraints

- 4.3.1 Limited atmospheric transmission windows constrain outdoor links

- 4.3.2 Cryogenic cooling requirements for high-power QCL sources

- 4.3.3 Scarcity of volume-manufacturable low-loss THz packaging

- 4.3.4 Absence of harmonised global EMC/health exposure limits above 275 GHz

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

- 4.9 Pricing Analysis

- 4.10 Analysis of Non-destructive Testing Applications of Terahertz Technology

- 4.11 Legal and Regulatory Space for Terahertz Technologies

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application Category

- 5.1.1 Terahertz Imaging Systems

- 5.1.1.1 Active Systems

- 5.1.1.2 Passive Systems

- 5.1.2 Terahertz Spectroscopy Systems

- 5.1.2.1 Time-Domain

- 5.1.2.2 Frequency-Domain

- 5.1.3 Communication Systems

- 5.1.1 Terahertz Imaging Systems

- 5.2 By Frequency Range

- 5.2.1 Low-Frequency Terahertz (0.1 - 1 THz)

- 5.2.2 Mid-Frequency Terahertz (1 - 5 THz)

- 5.2.3 High-Frequency Terahertz (Above 5 THz)

- 5.3 By End User

- 5.3.1 Healthcare

- 5.3.2 Defense and Security

- 5.3.3 Telecommunications

- 5.3.4 Industrial

- 5.3.5 Food and Agriculture

- 5.3.6 Laboratories

- 5.3.7 Other End Users

- 5.4 By Component Type

- 5.4.1 Terahertz Sources

- 5.4.2 Terahertz Detectors

- 5.4.3 Optics and Passive Components

- 5.4.4 Systems and Software

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ADVANTEST Corporation

- 6.4.2 Luna Innovations Incorporated

- 6.4.3 TeraView Limited

- 6.4.4 TOPTICA Photonics AG

- 6.4.5 HUBNER GmbH and Co. KG

- 6.4.6 BATOP GmbH

- 6.4.7 Microtech Instruments Inc.

- 6.4.8 Menlo Systems GmbH

- 6.4.9 Gentec-EO Inc.

- 6.4.10 Bakman Technologies LLC

- 6.4.11 QMC Instruments Ltd

- 6.4.12 Bruker Corporation

- 6.4.13 Lytid SAS

- 6.4.14 Attocube Systems AG

- 6.4.15 Helmut Fischer GmbH

- 6.4.16 Baugh and Weedon Ltd

- 6.4.17 Das-nano S.L.

- 6.4.18 Teravil Ltd

- 6.4.19 Terasense Group Inc.

- 6.4.20 Virginia Diodes Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment