|

시장보고서

상품코드

1939121

다이캐스트 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

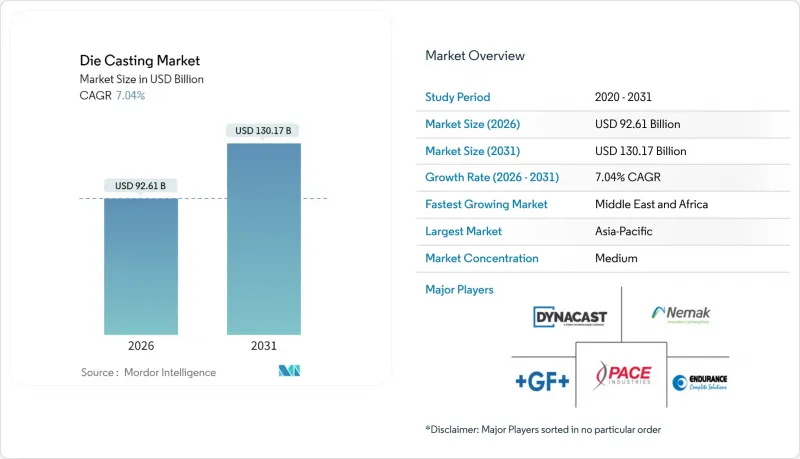

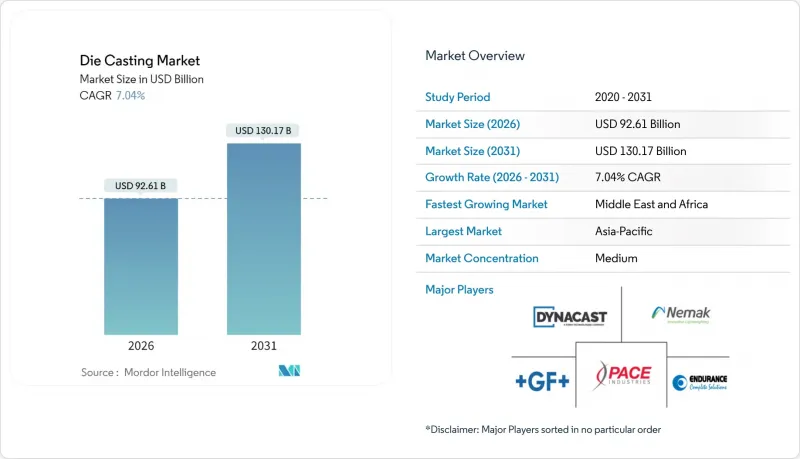

다이캐스트 시장은 2025년에 865억 2,000만 달러로 평가되며, 2026년 926억 1,000만 달러에서 2031년까지 1,301억 7,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2031년)의 CAGR은 7.04%로 전망됩니다.

전동화가 파워트레인의 요구를 재구성하는 가운데, OEM(Original Equipment Manufacturer)들은 여러 개의 스탬핑 및 용접 부품으로 구성된 어셈블리를 구조적 강성을 유지하면서 무게와 부품 수를 줄이는 고도로 통합된 단일 주조품으로 대체하고 있습니다. 이러한 전환으로 내연기관차 생산량이 감소하는 가운데서도 다이캐스팅 시장은 견고한 성장세를 유지하고 있습니다. 전기자동차에서 배터리 트레이, 모터 하우징, 차체 하부용 대형 주조 부품에 대한 수요 증가로 차량당 다이캐스팅 부품 사용량이 증가하고 있기 때문입니다. 모빌리티 분야 외에는 재생에너지 인프라, 5G 구축, 자동화 프로그램이 복잡한 니어 네트형 부품에 대한 수요를 지원하고 있습니다. Tier 1 공급업체, 전문 주조업체, 수직계열화를 추진하는 자동차 업체들이 기가 프레스 기술 습득, 비용 관리를 위한 현지 재생에너지 도입, 금형 윤활유 PFAS 금지 대응을 위해 경쟁하면서 경쟁이 심화되고 있습니다.

세계 다이캐스팅 시장 동향과 인사이트

내연기관차에서 전기자동차로 구조부품 경량화 추진

배터리 전기자동차는 부품 수를 줄인 설계를 채택하고 있지만, 배터리 하우징, 모터 프레임, 통합 섀시 섹션과 같은 주요 구조 부품에는 더 큰 크기의 일체형 주조 부품이 요구됩니다. 대표적인 예가 테슬라의 후방 언더바디용 메가캐스팅으로, 여러 개의 스탬핑 부품을 통합하고 있습니다. 이는 총 생산량 변동에 관계없이 각 차량에서 다이캐스팅의 전략적 중요성과 가치가 증가하고 있음을 보여줍니다. 연구에 따르면 구조용 메가 캐스팅은 차량 중량을 10-15% 줄일 수 있으며, 중요한 항속거리 향상과 동시에 조립의 복잡성을 줄일 수 있습니다.

기가프레스 백색 차체용 니어넷 형상 압력 다이캐스팅(기가프레스 화이트 차체)

초대형 기가프레스는 과거에는 여러 개의 용접 부품이 필요했던 구조물을 단일 부품으로 제작할 수 있게 했습니다. 전통적 자동차 제조업체는 이러한 프레스를 새로운 전기자동차 플랫폼에 통합하는 반면, 중소형 주조 제조업체는 높은 초기 불량률과 값비싼 금형 조정과 같은 문제에 직면하고 있습니다. 한편, 첨단 설비 라인에서는 사이클 타임의 단축이 진행되어 막대한 설비 투자 비용이 절감되는 동시에 다이캐스팅 산업은 적은 수이지만 크게 대형화된 생산 셀로 집적화가 진행되고 있습니다.

2026년 이후 중국 수출 규제에 따른 마그네슘 공급 리스크

중국은 마그네슘의 주요 공급원으로서의 지위를 유지하고 있습니다. 그러나 최근 중국의 수출 허가 조치로 인해 공급 관리가 강화되고 있음을 시사하고 있습니다. 이러한 움직임은 다운스트림 주조 계약에 혼란을 가져올 수 있습니다. 증산에 수년이 소요되는 유럽과 미국의 제련소는 가격 변동으로 어려움을 겪고 있으며, 장기적인 차량 플랫폼 계획을 복잡하게 만들고 있습니다. 알루미늄보다 가벼운 마그네슘의 장점을 활용하여 온 자동차 및 항공우주 분야의 프로그램들은 부품을 재설계하거나 재료를 비축해야 하는 어려운 결정에 직면해 있습니다.

부문 분석

자동차 용도는 2025년 매출의 61.73%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 8.02%로 확대될 것으로 예측됩니다. 이는 전기자동차(EV)의 구조부품 수요가 내연기관차(ICE)의 감소를 상쇄하고 있음을 보여줍니다. 배터리 인클로저, 모터 하우징, 차체 하부 주조 부품용 다이캐스팅 시장 규모는 예측 기간이 끝날 때까지 크게 성장할 것으로 예측됩니다. 자동차 제조업체들은 수십 개의 스탬핑 부품을 소수의 대형 주조품으로 통합하는 경향이 있으며, 조달 전략의 전환이 진행되고 있습니다. 특히 기가프레스 가동에 정통한 공급업체, 특히 완벽한 가동 주기를 가진 업체를 선호하는 경향이 강해지고 있습니다. 자동차 분야 외에도 재생에너지, 통신 분야 등에서도 수요가 꾸준히 증가하고 있습니다.

한편, 항공우주산업에서는 차세대 기체 구조재로 티타늄 및 고강도 알루미늄에 대한 관심이 높아지고 있습니다. 이러한 산업 전반의 전환에 따라 연성합금과 진공보조충진기술에 대한 연구개발이 활발히 이루어지고 있으며, 모두 엄격한 충돌안전기준에 대응하기 위한 것입니다. 기존 엔진 부품 중심이었던 1차 협력사들은 현재 사업 전환을 추진하고 있습니다. 용광로 개조 및 대규모 주조 셀 설치로 구조 부품 및 배터리 트레이에 대한 집중력 강화. 이러한 추세는 중소 주조업체들의 진입장벽을 높이고, OEM의 차체 공장과 가까운 곳에서 가공과 조립을 원활하게 통합하는 허브형 산업 구조로의 전환을 촉진하고 있습니다.

2025년 매출에서 압력 주조가 여전히 55.02%를 차지할 것으로 예상되지만, 안전성이 매우 중요한 EV 구조 부품에는 열처리 및 용접이 가능한 부품이 필요하므로 진공 주조는 CAGR 8.93%로 확대될 것으로 예측됩니다. 기공 함량이 60-80% 감소하면 자동차 제조업체는 알루미늄 부품을 파열 위험 없이 T6 열처리를 할 수 있으며, 레이저 용접을 통해 복합재 프레임에 통합할 수 있습니다. 이 기술은 Kg당 최대 30%의 가격 상승을 실현하고, 합금 비용 상승에도 높은 이익률을 유지할 수 있습니다. 그 결과, 다이캐스팅 시장에서는 진공 챔버를 추가하거나 콜드 챔버 셀의 하이브리드 구성으로 전환이 진행되고 있습니다.

장기적으로는 스퀴즈 주조나 반고체 공정이 단조와 같은 미세구조를 필요로 하는 항공우주 분야나 대형 트럭용 스티어링 너클과 같은 틈새 시장에 대응할 수 있습니다. 그러나 이러한 공정은 사이클 시간이 여전히 느리기 때문에 대량 생산 산업에서는 금형내 냉각 및 강화된 공정 모니터링을 보완하는 수단으로 압력 주조 및 진공 주조가 여전히 선호되고 있습니다.

지역별 분석

2025년 아시아태평양은 세계 매출의 56.21%를 차지할 것이며, 중국의 거대한 자동차, 가전, 전자제품 클러스터가 그 핵심을 형성했습니다. 수십년간 축적된 노하우, 풍부한 스크랩 알루미늄 공급, 수직적으로 통합된 공구강 생태계가 원가 경쟁력을 유지하고 있습니다. 한국과 일본은 제어 시스템 혁신에 기여하고, 인도는 생산 연동형 인센티브를 활용하여 새로운 경량 부품 라인에 자금을 조달하고 있습니다. OEM 업체들이 조달처를 다변화하는 가운데, 동남아시아는 복잡도가 낮은 부품 및 백업 능력 분야에서 점유율을 확대하며 아세안 전체 다이캐스팅 시장의 발자취를 넓혀가고 있습니다.

중동 및 아프리카은 8.42%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. 걸프협력회의 회원국들은 비전 2030 기금을 활용하여 태양광발전용 인버터, 풍력발전용 하우징, 전기자동차 충전기를 국내에서 생산하고 있습니다. NEOM과 같은 메가 프로젝트는 알루미늄 파사드 노드 및 구조용 커넥터를 주조할 수 있는 고톤수 프레스 기계에 대한 수요를 유발하고 있습니다. 튀르키예의 자동차 수출과 이집트의 산업단지 정책은 제련소 규모 확대까지 업스트림 잉곳 공급을 수입에 의존하고 있는 이 지역의 수주를 더욱 활성화시키고 있습니다.

북미와 유럽에서는 공장 수 증가보다는 기술의 변화에 의해 주로 성장하고 있습니다. 미국에서는 국내 배터리 및 구동계 부품 조달에 대한 세액공제가 적용되므로 OEM들은 오하이오, 앨라배마, 온타리오 주에 있는 조립공장 근처에 메가캐스팅을 현지화하고 있습니다. 유럽의 탄소국경조정 메커니즘은 재생에너지로 재활용 알루미늄 용광로를 가동하는 지역 공장의 경쟁력을 강화합니다. 두 지역 모두 PFAS의 단계적 폐지와 수명주기 탄소감사를 실시하여 다이캐스팅 시장을 촉진하고, 설비 업데이트와 디지털 추적성 모듈 도입을 가속화하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The die casting market was valued at USD 86.52 billion in 2025 and estimated to grow from USD 92.61 billion in 2026 to reach USD 130.17 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031).

As electrification reshapes power-train needs, OEMs are replacing multi-piece stamp-and-weld assemblies with single, high-integrity castings that cut weight and part counts while preserving structural rigidity. This pivot keeps the die casting market resilient even as internal-combustion volumes plateau, because the content-per-vehicle in electric cars rises on the back of battery trays, motor housings, and under-body megacastings. Outside mobility, renewable-energy infrastructure, 5G rollouts, and automation programs sustain demand for complex, near-net-shape components. Competitive intensity tightens as tier-1 suppliers, pure-play foundries, and vertically integrating automakers race to master giga-press technology, deploy on-site renewables for cost control, and navigate looming PFAS bans in mold lubricants.

Global Die Casting Market Trends and Insights

ICE-to-EV Structural-Parts Lightweighting Push

Battery-electric vehicles streamline their design with fewer components, yet they demand larger, integrated castings for essential structures such as battery housings, motor frames, and unified chassis sections. A prime example is Tesla's rear underbody megacasting, which consolidates several stamped parts. This underscores the rising strategic significance and value of die casting in each vehicle, regardless of fluctuations in overall production volumes. Studies indicate structural megacasting can reduce curb weight by 10-15%, bringing critical range benefits while lowering assembly complexity .

Near-Net-Shape Pressure-Die-Casting for Giga-Press Body-in-White

Ultra-large giga-presses now create single-piece structures, a feat that once demanded multiple welded components. While traditional automakers are integrating these presses into their new electric vehicle platforms, smaller foundries grapple with challenges like high initial scrap rates and expensive die adjustments. Meanwhile, advanced equipment lines are achieving quicker cycle times, a move that mitigates hefty capital costs and pushes the die-casting industry towards consolidating into fewer, yet significantly larger, production cells.

Post-2026 Magnesium Supply Risk from China Export Controls

China continues to lead as the primary source of magnesium. However, recent export licensing measures from the country hint at tighter supply controls. Such moves could potentially disrupt downstream casting contracts. Western smelters, taking years to ramp up, are grappling with price volatility, complicating long-term vehicle platform planning. Programs in the automotive and aerospace sectors, which have relied on magnesium's lightweight benefits over aluminum, now confront difficult decisions: redesigning components or stockpiling the material.

Other drivers and restraints analyzed in the detailed report include:

- In-Mold Sensors Enabling Zero-Defect "First-Shot" Quality

- Circular-Economy Aluminum-Recycling Mandates Spur Secondary HPDC Demand

- Tightening PFAS Emissions Norms on Lubricants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive applications contributed 61.73% of 2025 revenues and will deliver an 8.02% CAGR to 2031, illustrating how EV structural content offsets ICE decline. The die casting market size for battery enclosures, motor housings, and under-body castings will grow significantly by the end of the forecast period. Automakers are consolidating dozens of stamped components into just a few large castings, leading to a shift in sourcing strategies. They're now favoring suppliers adept at giga-press operations, especially those with flawless startup cycles. Beyond the automotive realm, sectors like renewable energy and telecom are witnessing a steady uptick in demand.

Meanwhile, the aerospace industry is showing heightened interest in titanium and high-strength aluminum, eyeing them for next-generation airframes. This industry-wide transition is spurring intensified R&D efforts into ductile alloys and vacuum-assisted filling, all in a bid to meet stringent crash safety standards. Tier-1 suppliers, previously centered on engine parts, are now pivoting. They're retrofitting furnaces and setting up massive casting cells, focusing on structural components and battery trays. Such trends are elevating entry barriers for smaller foundries and nudging the industry towards integrated hubs, seamlessly blending machining and assembly close to OEM body shops.

While pressure casting still owns 55.02% of 2025 billings, vacuum casting will clock a 8.93% CAGR as safety-critical EV structures require heat-treatable, weldable parts. When pore content falls 60-80%, automakers can T6-treat aluminum parts without blow-out risk and laser-weld them into multi-material frames. That capability lifts price realizations by up to 30% per kilogram, keeping margin potential high even where alloy cost rises. Consequently, the die casting market sees plants adding vacuum chambers or converting cold-chamber cells to hybrid configurations.

Longer term, squeeze casting and semi-solid processes address niche aerospace and heavy-truck steering knuckles that need forged-like microstructures. Yet their cycle times remain slower, so high-volume industries still favor pressure or vacuum options supplemented by in-die cooling and intensified process monitoring.

The Die Casting Market Report is Segmented by Application (Automotive, Electrical and Electronics, and More), Process (Pressure Die Casting, Vacuum Die Casting, and More), Raw Material (Aluminum, Magnesium, and More), Casting-Machine Clamping Force (<=4, 000 KN, 4, 001-10, 000 KN, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 56.21% of global sales in 2025, anchored by China's vast auto, appliance and electronics clusters. Decades of cumulative know-how, high scrap-aluminum availability, and vertically integrated tool-steel ecosystems keep cost positions sharp. Korea and Japan contribute control-system innovation, while India rides production-linked incentives that fund new lightweight-component lines. As OEMs diversify sourcing, Southeast Asia gains share for low-complexity parts and back-up capacity, broadening the die casting market footprint across ASEAN.

The Middle East & Africa region is the fastest riser at 8.42% CAGR. Gulf Cooperation Council states use Vision 2030 funds to manufacture solar inverters, wind housings, and EV chargers domestically. Megaprojects like NEOM draw demand for high-tonnage presses able to cast aluminum facade nodes and structural connectors. Turkey's auto exports and Egypt's industrial-park policies further energize regional orders, though upstream ingot supply relies on imports until smelters scale.

North America and Europe grow chiefly through technology shifts rather than plant count. United States tax credits favor domestic battery and drivetrain sourcing, causing OEMs to localize megacasting next to assembly plants in Ohio, Alabama, and Ontario. Europe's Carbon Border Adjustment Mechanism boosts competitive standing for regional shops running recycled aluminum furnaces on renewable power. Both regions further the die casting market by enforcing PFAS phase-outs and lifecycle carbon audits, spurring capital upgrades and digital traceability modules.

- Form Technologies Inc. (Dynacast)

- Nemak S.A.B. de C.V.

- Endurance Technologies Limited

- Sundaram Clayton Ltd

- Shiloh Industries, inc.

- Georg Fischer Ltd

- Gibbs Die Casting Corporation

- Bocar Group

- Engtek Group

- Rheinmetall AG

- Rockman Industries Limited

- Ryobi Die Casting

- Linamar Corporation

- Meridian Lightweight Technologies Inc.

- Sandhar Group

- Alcoa Corporation

- Pace Industries Inc.

- CIE Automotive

- China Hongqiao Group Limited

- Consolidated Metco, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ICE-to-EV Structural-Parts Lightweighting Push

- 4.2.2 Near-Net-Shape Pressure-Die-Casting for Giga-Press Body-in-White

- 4.2.3 In-Mold Sensors Enabling Zero-Defect "First-Shot" Quality

- 4.2.4 Circular-Economy Aluminum-Recycling Mandates Spur Secondary HPDC Demand

- 4.2.5 Energy-Price Hedging via On-Site Renewables at Foundries

- 4.2.6 3D-Sand-Printed Cores Unlocking Complex EV Geometries

- 4.3 Market Restraints

- 4.3.1 Post-2026 Magnesium Supply Risk from China Export Controls

- 4.3.2 Tightening PFAS Emissions Norms on Lubricants

- 4.3.3 OEM Insourcing with Giga-Pressing Reducing Tier-1 Volumes

- 4.3.4 EU Carbon-Border Taxes Raising Cost Base for Energy-Intensive Foundries

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Application

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Industrial Machinery

- 5.1.4 Aerospace and Defense

- 5.1.5 Consumer Appliances

- 5.1.6 Others

- 5.2 By Process

- 5.2.1 Pressure Die Casting

- 5.2.2 Vacuum Die Casting

- 5.2.3 Squeeze Die Casting

- 5.2.4 Gravity Die Casting

- 5.3 By Raw Material

- 5.3.1 Aluminum

- 5.3.2 Magnesium

- 5.3.3 Zinc

- 5.3.4 Copper

- 5.3.5 Others (Lead, Tin Alloys)

- 5.4 By Casting-Machine Clamping Force

- 5.4.1 <=4,000 kN

- 5.4.2 4,001-10,000 kN

- 5.4.3 Above 10,000 kN

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Thailand

- 5.5.4.6 Indonesia

- 5.5.4.7 Malaysia

- 5.5.4.8 Australia

- 5.5.4.9 Rest of Asia-Pacific

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Form Technologies Inc. (Dynacast)

- 6.4.2 Nemak S.A.B. de C.V.

- 6.4.3 Endurance Technologies Limited

- 6.4.4 Sundaram Clayton Ltd

- 6.4.5 Shiloh Industries, inc.

- 6.4.6 Georg Fischer Ltd

- 6.4.7 Gibbs Die Casting Corporation

- 6.4.8 Bocar Group

- 6.4.9 Engtek Group

- 6.4.10 Rheinmetall AG

- 6.4.11 Rockman Industries Limited

- 6.4.12 Ryobi Die Casting

- 6.4.13 Linamar Corporation

- 6.4.14 Meridian Lightweight Technologies Inc.

- 6.4.15 Sandhar Group

- 6.4.16 Alcoa Corporation

- 6.4.17 Pace Industries Inc.

- 6.4.18 CIE Automotive

- 6.4.19 China Hongqiao Group Limited

- 6.4.20 Consolidated Metco, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment