|

시장보고서

상품코드

1939137

스마트 팩토리 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Smart Factory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

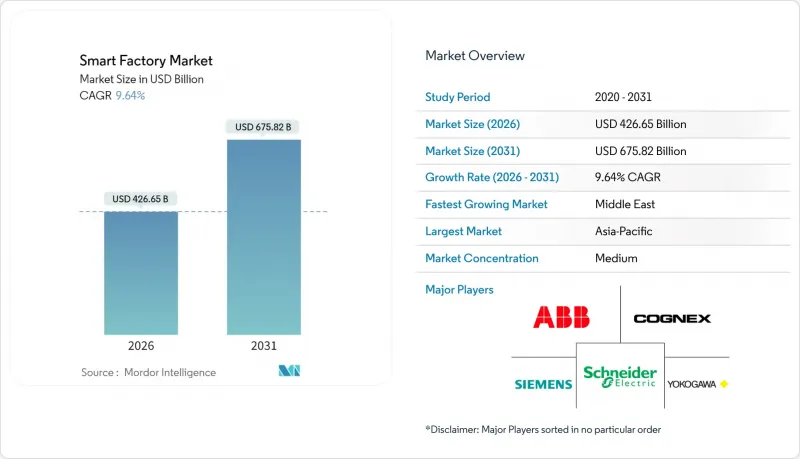

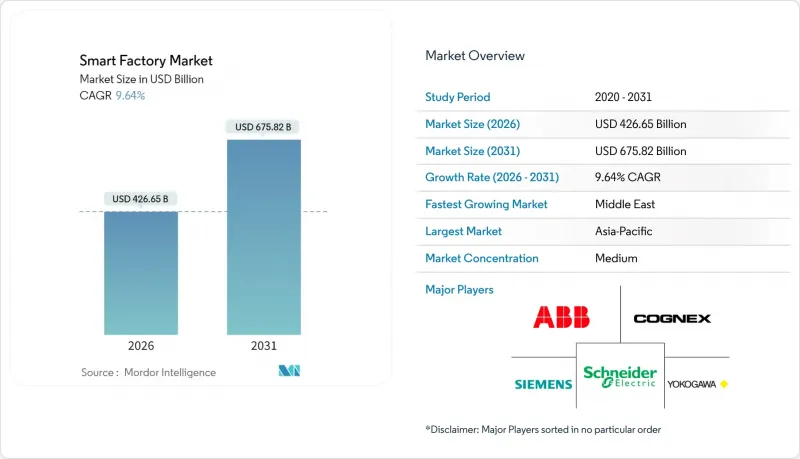

2026년 스마트 팩토리 시장 규모는 4,266억 5,000만 달러로 추정되며, 2025년 3,891억 4,000만 달러에서 성장하며, 2031년에는 6,758억 2,000만 달러에 달할 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR)은 9.64%를 나타낼 것으로 예측됩니다.

자율 및 데이터베이스 생산 시스템에 대한 견고한 수요, 센서 및 엣지 AI 비용의 하락, 정책적 인센티브가 이러한 성장 궤도를 지원하고 있습니다. 제조업체들은 산업용 IoT 플랫폼, 디지털 트윈, 머신비전 유도 로봇을 도입하여 개별 생산 및 공정 산업 전반에 걸쳐 전환 시간 단축, 에너지 사용량 감소, 폐기물 감소를 위해 노력하고 있습니다. 동남아와 중동에서는 신규 투자가 가속화되는 반면, 유럽과 북미에서는 탄소가격제 강화에 따라 기존 설비의 개보수가 활발히 진행되고 있습니다. 경쟁 환경은 하드웨어, 소프트웨어, 사이버 보안 서비스를 통합 솔루션으로 제공하여 제조업체의 투자 회수 기간을 단축할 수 있는 벤더에게 유리하게 작용합니다.

세계 스마트팩토리 시장 동향 및 인사이트

산업용 IoT 플랫폼 보급 확대

산업용 IoT 플랫폼은 센서, 액추에이터, 제어 시스템을 통합하여 예지보전과 자율 최적화를 추진하는 실시간 데이터 파이프라인을 구축합니다. 표준화된 프로토콜과 엣지 게이트웨이를 통해 도입의 복잡성을 최소화하고, 레거시 시설 전체에 비용 효율적으로 구축할 수 있습니다. 예를 들어 가이드휠(Guidewheel)은 2024년 3,100만 달러를 조달하여 배선 변경 없이 기계 데이터를 스트리밍하는 플러그 앤 플레이 방식의 FactoryOps 솔루션에 박차를 가하고 있습니다. 제조 실행 시스템(MES)에 IoT 커넥터가 내장되는 경우가 증가하고 있으며, 계획 담당자는 처리량, 품질, 에너지 지표를 한 곳에서 파악할 수 있습니다. 프라이빗 5G 네트워크의 보급은 자동차 조립 라인에서 인간과 로봇의 안전한 협업에 필요한 밀리초 미만의 지연을 실현하여 IoT의 가치 제안을 더욱 강화할 것입니다. 인도의 식품가공 생산연계형 장려제도(PLI)와 같은 국가 보조 프로그램은 초기 단계의 재정적 장벽을 낮춰 중소기업의 도입 확대에 기여하고 있습니다.

엔드투엔드 에너지 최적화에 대한 수요

전기요금 상승과 넷제로 목표에 따라 에너지 효율은 경영진의 최우선 과제가 되었습니다. 스마트 팩토리 플랫폼은 AI 기반 예측, 자동 부하 분산, 역률 보정을 적용하여 전력 소비를 20-40% 절감합니다. BMW 레겐스부르크 공장에서는 400개의 센서와 연동되는 AI 에너지 관리 시스템 도입 후 전력 사용량이 30% 감소했다고 합니다. 디지털 트윈 기술을 통해 설비 설치 전에 열과 기류의 동적 모델을 구축할 수 있으며, 공조 설비의 과잉 설계를 줄이고 자본 낭비를 방지할 수 있습니다. 수요반응 프로그램 참여를 통해 공장이 생산 스케줄을 조정하여 전력계통 안정화를 지원함으로써 부수적인 매출을 창출할 수 있습니다. 유럽연합의 친환경 세제 혜택은 투자 회수를 가속화하고, 제조업체들이 고정 속도 구동 장치를 스마트 인버터로 교체하고, 저탄소 생산의 최적 타이밍을 제안하는 에너지 대응형 MES 모듈을 도입하는 계기가 되고 있습니다.

기존 공장의 변혁을 위해서는 막대한 초기 설비투자가 필요

2010년 이전 공장을 커넥티드 플랜트로 전환하는 경우, 전기설비 업그레이드, 네트워크 배선, 다운타임을 포함하면 비용이 1,000만 달러가 넘는 경우가 많습니다. 레거시 PLC에는 이더넷 포트가 장착되어 있지 않을 수 있으며, 커스텀 펌웨어 또는 프로토콜 변환기를 도입해야 하고 엔지니어링 공수가 추가될 수 있습니다. 슈나이더 일렉트릭의 추정에 따르면 기존 공장의 투자 회수 기간은 신규 건설의 경우 2년, 기존 공장의 경우 최대 5년으로 자금 여력이 제한적인 중견기업에게는 장벽이 될 수 있습니다. 모듈형 리노베이션 키트와 구독형 가격 모델이 부담을 덜어주는 반면, 거시경제의 불확실성으로 인해 CFO들의 신중한 태도는 계속되고 있습니다.

부문 분석

산업용 로봇은 가장 큰 수입원이며, 2025년 스마트팩토리 시장 점유율의 31.35%를 차지했습니다. 반복적이고 인체공학적 부담이 큰 작업을 작업자로부터 해방시켜주는 관절형 및 협업형 유닛에 대한 수요가 증가하고 있습니다. 최종사용자가 재공구화 없이 모델 간 전환이 가능한 모듈형 하드웨어를 활용함에 따라 로봇으로 인한 스마트팩토리 시장 규모는 꾸준히 성장하고 있습니다. 머신비전 시스템은 현재 규모는 작지만, 딥러닝 카메라의 가격 하락에 따라 2031년까지 10.08%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 로봇과 비전을 통합한 셀은 검사 작업을 줄이고, 최초 합격률을 식스 시그마 수준으로 끌어올립니다. 스마트 드라이브 및 서보 모터와 같은 제어 부품은 OEM(Original Equipment Manufacturer)가 절전 펌웨어를 통합하여 건전한 업데이트 주기를 맞이하고 있습니다. 센서 어레이는 진동, 온도, 습도 데이터를 예지보전 대시보드에 공급하여 계획되지 않은 다운타임을 방지하기 위해 광범위하게 도입되고 있습니다.

프라이빗 5G 연결과 시간 민감형 네트워킹의 융합은 자율 이동 로봇을 위한 확정적인 무선 링크를 실현하고, 저스트 인 시퀀싱 방식으로 키트 배송을 가능하게 합니다. 적층제조 기술은 특히 항공우주용 공구 및 맞춤형 형상을 필요로 하는 의료용 임플란트 분야에서 점진적인 성장에 기여합니다. 한편, 경조립 환경에서는 외골격과 웨어러블 스캐너가 등장하면서 로봇 기술과 인간 증강의 경계가 모호해지고 있습니다. 전체 제품 동향은 독립적인 자동화 아일랜드에서 엣지 컴퓨팅 노드가 시각, 동작, 품질 분석을 실시간으로 조정하는 통합 에코시스템으로의 전환을 반영하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출 점유율 40.20%를 차지할 것으로 예상되며, 중국이 세계 제조업의 핵심으로 자리 잡게 될 것입니다. '중국제조 2025'와 같은 강력한 정부 정책으로 스마트 공장 개보수를 지원하는 한편, 한국과 대만은 3D 비전 기술과 반도체 제조 공장에 자원을 투입하고 있습니다. 베트남, 태국, 인도네시아는 면세 혜택과 디지털 대응형 산업단지로 외국인 직접투자를 유치하고 있습니다. 이 지역의 우위는 희토류 자석 정제량의 80%를 점유하고 있다는 점에서도 알 수 있듯이, 현지 로봇 제조업체들은 공급망에서 우위를 점하고 있습니다. 사이버 보안과 인력 재교육은 여전히 과제로 남아 있지만, 정책 당국은 인력 부족을 해결하기 위해 전국적인 기술 향상 프로그램을 시작하고 있습니다.

중동은 10.02%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. 사우디의 1,300억 달러 규모의 국가 산업 전략과 아랍에미리트의 '오퍼레이션 3,000억' 계획에 따라 석유화학 단지와 첨단 소재 공장에 자본이 집중되고 있습니다. 그린필드 건설을 통해 공장은 첫 날부터 모듈식 사이버 보안 대책을 갖춘 아키텍처를 통합할 수 있으며, 고가의 레거시 리노베이션을 피할 수 있습니다. 정부계 펀드는 유럽 및 아시아 벤더와 제휴하여 로봇 조립 및 MES 소프트웨어 커스터마이징을 현지화하는 합작회사를 설립하고 있습니다. 걸프 지역 특유의 고온 및 다분진 환경은 내환경성 인클로저와 고급 냉각 솔루션에 대한 고유한 수요를 창출하고 있습니다.

북미에서는 리쇼어링이 진행됨에 따라 그 기세가 더욱 가속화되고 있습니다. 'CHIPS and Science Act'에 따라 폐루프 노광 제어 및 AI 결함 분류 기능을 갖춘 새로운 팹에 수십억 달러가 투입될 예정입니다. 자동차 제조업체들은 높은 대역폭의 공장내 네트워크를 필요로 하는 배터리 팩 생산 라인과 소프트웨어 정의 차량 아키텍처에 투자하고 있습니다. 유럽 제조업체들은 탄소중립 목표인 'Fit for 55' 법에 대응하기 위해 공장 업그레이드를 지속하고 있으며, 녹색세액공제 및 에너지 가격 헤지를 활용하여 스마트팩토리 예산을 정당화하기 위해 노력하고 있습니다. 남미와 아프리카는 규모는 작지만, 정부가 세제혜택과 민관협력을 통해 자원 수출 의존도를 탈피하고자 하는 만큼 유망한 시장으로 남아있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The smart factory market size in 2026 is estimated at USD 426.65 billion, growing from 2025 value of USD 389.14 billion with 2031 projections showing USD 675.82 billion, growing at 9.64% CAGR over 2026-2031.

Robust demand for autonomous, data-driven production systems, falling sensor and edge AI costs, and supportive policy incentives underpin this trajectory. Manufacturers deploy industrial IoT platforms, digital twins, and machine-vision-guided robotics to shrink changeover times, cut energy use, and reduce scrap across discrete and process industries. Greenfield investments accelerate in Southeast Asia and the Middle East, while brownfield retrofits gather momentum in Europe and North America as carbon-pricing regimes tighten. Competitive dynamics favor vendors able to bundle hardware, software, and cybersecurity services into integrated offerings that shorten payback periods for manufacturers.

Global Smart Factory Market Trends and Insights

Growing Adoption of Industrial IoT Platforms

Industrial IoT platforms unify sensors, actuators, and control systems, creating real-time data pipelines that drive predictive maintenance and autonomous optimization. Standardized protocols and edge gateways minimize deployment complexity, enabling cost-effective rollout across legacy equipment. Guidewheel, for example, raised USD 31 million in 2024 to accelerate its plug-and-play FactoryOps solution that streams machine data without invasive rewiring. Manufacturing execution systems increasingly embed IoT connectors, giving planners a single pane of glass for throughput, quality, and energy metrics. The spread of private 5G networks further strengthens IoT value propositions by delivering sub-millisecond latency required for safe human-robot collaboration on automotive assembly lines. National subsidy programs such as India's Production-Linked Incentive Scheme for food processing lower early-stage financial barriers and broaden adoption among small and medium enterprises.

Demand for End-to-End Energy Optimization

Rising electricity tariffs and net-zero targets turn energy efficiency into a board-level priority. Smart factory platforms cut consumption 20-40% by applying AI-based forecasting, automated load-balancing, and power-factor correction. BMW's Regensburg plant reports 30% lower electricity use after deploying an AI energy management system connected to 400 sensors. Digital twins let engineers model thermal and airflow dynamics before equipment installation, reducing HVAC oversizing and avoiding capital waste. Participation in demand-response programs generates ancillary revenue as factories flex production schedules to support grid stability. European Union green-tax credits accelerate return on investment, prompting manufacturers to replace fixed-speed drives with smart inverters and to install energy-aware MES modules that recommend low-carbon production windows.

High Upfront CAPEX for Brownfield Transformation

Converting pre-2010 factories into connected plants often costs more than USD 10 million once electrical upgrades, network cabling, and downtime are included. Legacy PLCs may lack Ethernet ports, forcing custom firmware and protocol converters that add engineering hours. Schneider Electric estimates brownfield payback can stretch to five years versus two years for greenfield builds, discouraging mid-market firms with limited cash buffers. Modular retrofit kits and subscription pricing models partially ease the burden, yet CFOs remain cautious amid macroeconomic uncertainty.

Other drivers and restraints analyzed in the detailed report include:

- Rising Government Incentives for Smart Manufacturing

- Edge AI Chips Enabling Real-Time Quality Control

- Cybersecurity Vulnerabilities within OT Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial robotics generated the largest revenue slice, accounting for 31.35% smart factory market share in 2025. Demand stems from articulated and collaborative units that lift repetitive ergonomically taxing tasks from workers. The smart factory market size attributed to robotics grows steadily as end-users exploit modular hardware that can shift across models without re-tooling. Machine vision systems, though smaller today, register an 10.08% CAGR through 2031 as deep-learning cameras become affordable. Integrated robot-vision cells reduce inspection labor and push first-pass yield toward six sigma. Control components such as smart drives and servo motors see healthy replacement cycles as OEMs embed power-saving firmware. Sensor arrays continue broad deployment, feeding vibration, temperature, and humidity data into predictive maintenance dashboards that prevent unplanned downtime.

The convergence of private 5G connectivity and time-sensitive networking creates deterministic wireless links for autonomous mobile robots that deliver kits just-in-sequence. Additive manufacturing contributes incremental growth, especially in aerospace tooling and medical implants requiring customized geometries. Meanwhile, exoskeletons and wearable scanners emerge in light-assembly environments, blurring lines between robotics and human augmentation. The overall product landscape reflects a shift from standalone automation islands to orchestrated ecosystems where edge compute nodes coordinate vision, motion, and quality analytics in real time.

The Smart Factory Market Report is Segmented by Product Type (Machine Vision Systems, Industrial Robotics, Control Devices, Sensors, and More), Technology (PLM, HMI, ERP, MES, DCS, SCADA, PLC, and More), End-User Industry (Automotive, Semiconductors, Oil and Gas, Chemical and Petrochemical, Pharmaceutical, Aerospace and Defense, Food and Beverage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific captured 40.20% share of 2025 revenue as China cemented its position as the global manufacturing nucleus. Robust governmental agendas such as "Made in China 2025" subsidize smart factory retrofits, while South Korea and Taiwan pour resources into 3D vision and semiconductor fabs. Vietnam, Thailand, and Indonesia lure foreign direct investment with tax holidays and digital-friendly industrial parks. The region's dominance is further underpinned by its control of 80% of rare-earth magnet refining, giving local robotics producers supply-chain leverage. Cybersecurity and workforce reskilling remain pain points, but policy authorities launch nationwide upskilling programs to address talent gaps.

The Middle East is the fastest-growing region at a 10.02% CAGR. Saudi Arabia's USD 130 billion National Industrial Strategy and the UAE's Operation 300bn funnel capital into petrochemical complexes and advanced materials plants. Greenfield construction means factories can embed modular, cyber-secure architectures from day one, avoiding costly legacy remediation. Sovereign wealth funds partner with European and Asian vendors, establishing joint ventures that localize robot assembly and MES software customization. The heat and dust characteristic of Gulf environments drive unique demand for ruggedized enclosures and advanced cooling solutions.

North American momentum accelerates as reshoring gains ground. The CHIPS and Science Act channels billions into new fabs equipped with closed-loop lithography control and AI defect classification. Automotive OEMs invest in battery pack lines and software-defined vehicle architectures that demand high-bandwidth in-plant networks. European manufacturers continue upgrading factories in response to carbon "Fit for 55" legislation, leveraging green-tax credits and energy-price hedging to justify smart factory budgets. South America and Africa remain smaller but promising as governments explore tax incentives and public-private partnerships to diversify away from commodity exports.

- Siemens AG

- ABB Ltd

- Schneider Electric SE

- Rockwell Automation Inc.

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Fanuc Corporation

- Emerson Electric Co.

- Yokogawa Electric Corporation

- KUKA AG

- Cognex Corporation

- Robert Bosch GmbH

- Teledyne FLIR LLC

- General Electric Company

- Cisco Systems Inc.

- SAP SE

- PTC Inc.

- Dassault Systemes SE

- Intel Corporation

- Hewlett Packard Enterprise Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption of industrial IoT platforms

- 4.2.2 Demand for end-to-end energy optimisation

- 4.2.3 Rising government incentives for smart manufacturing

- 4.2.4 Edge AI chips enabling real-time quality control

- 4.2.5 Open-source digital twins lowering integration cost

- 4.2.6 Green-tax-driven retrofit of legacy factories

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX for brownfield transformation

- 4.3.2 Cybersecurity vulnerabilities within OT networks

- 4.3.3 Shortage of interoperable OT-IT talent

- 4.3.4 Volatile rare-earth supply for robotics actuators

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Machine Vision Systems

- 5.1.1.1 Cameras

- 5.1.1.2 Processors

- 5.1.1.3 Software

- 5.1.1.4 Enclosures

- 5.1.1.5 Frame Grabbers

- 5.1.1.6 Integration Services

- 5.1.1.7 Lighting

- 5.1.2 Industrial Robotics

- 5.1.2.1 Articulated Robots

- 5.1.2.2 Cartesian Robots

- 5.1.2.3 Cylindrical Robots

- 5.1.2.4 SCARA Robots

- 5.1.2.5 Parallel Robots

- 5.1.2.6 Collaborative Industry Robots

- 5.1.3 Control Devices

- 5.1.3.1 Relays and Switches

- 5.1.3.2 Servo Motors and Drives

- 5.1.4 Sensors

- 5.1.5 Communication Technologies

- 5.1.5.1 Wired

- 5.1.5.2 Wireless

- 5.1.6 Other Product Types

- 5.1.1 Machine Vision Systems

- 5.2 By Technology

- 5.2.1 Product Lifecycle Management (PLM)

- 5.2.2 Human Machine Interface (HMI)

- 5.2.3 Enterprise Resource Planning (ERP)

- 5.2.4 Manufacturing Execution System (MES)

- 5.2.5 Distributed Control System (DCS)

- 5.2.6 Supervisory Control and Data Acquisition (SCADA)

- 5.2.7 Programmable Logic Controller (PLC)

- 5.2.8 Other Technologies

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Semiconductors

- 5.3.3 Oil and Gas

- 5.3.4 Chemical and Petrochemical

- 5.3.5 Pharmaceutical

- 5.3.6 Aerospace and Defense

- 5.3.7 Food and Beverage

- 5.3.8 Mining

- 5.3.9 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Kenya

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 ABB Ltd

- 6.4.3 Schneider Electric SE

- 6.4.4 Rockwell Automation Inc.

- 6.4.5 Honeywell International Inc.

- 6.4.6 Mitsubishi Electric Corporation

- 6.4.7 Fanuc Corporation

- 6.4.8 Emerson Electric Co.

- 6.4.9 Yokogawa Electric Corporation

- 6.4.10 KUKA AG

- 6.4.11 Cognex Corporation

- 6.4.12 Robert Bosch GmbH

- 6.4.13 Teledyne FLIR LLC

- 6.4.14 General Electric Company

- 6.4.15 Cisco Systems Inc.

- 6.4.16 SAP SE

- 6.4.17 PTC Inc.

- 6.4.18 Dassault Systemes SE

- 6.4.19 Intel Corporation

- 6.4.20 Hewlett Packard Enterprise Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment