|

시장보고서

상품코드

1939162

콘크리트 혼화제 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Concrete Admixtures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

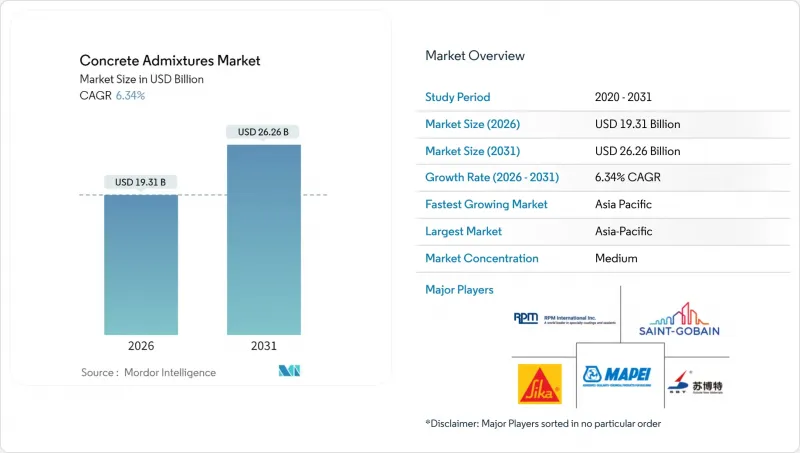

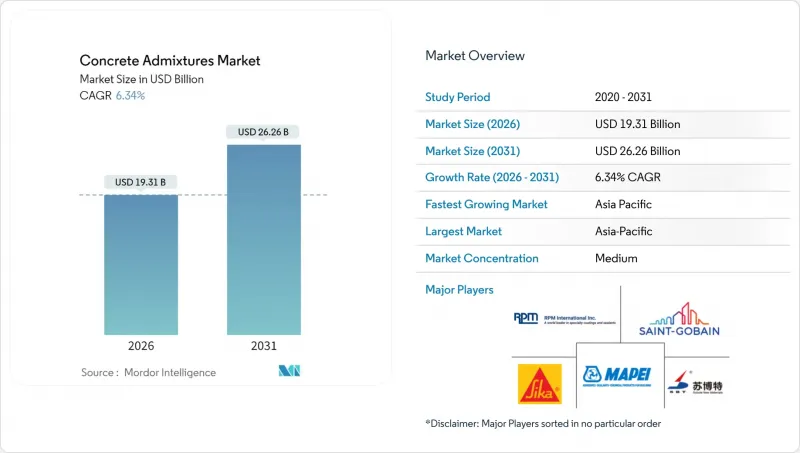

콘크리트 혼화제 시장은 2025년에 181억 6,000만 달러로 평가되며, 2026년 193억 1,000만 달러에서 2031년까지 262억 6,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2031년)의 CAGR은 6.34%로 전망됩니다.

시장 성장은 아시아태평양의 정부 주도 인프라 계획, 선진국의 엄격한 물 감소 기준, 생산성을 향상시키면서 자재 폐기물을 줄이는 자가 충전 콘크리트의 급속한 보급에 의해 주도되고 있습니다. 건설사들은 혼합의 일관성을 향상시키고 혼화제의 과다 사용을 억제하는 AI 가이드형 투약 플랫폼의 도입을 확대하고 있습니다. 주택 부문의 회복과 바이오 화학제품에 대한 선호도가 높아지면서 더 많은 성장 기회를 창출하고 있습니다. 경쟁의 강도는 여전히 중간 정도입니다. 이는 세계 공급업체들이 폴리머 기술 특허 취득과 디지털 기능 통합에 집중하는 반면, 지역 제조업체들은 물류 우위와 현지 규제에 대한 이해도를 바탕으로 틈새 시장을 점유하고 있기 때문입니다. 그러나 석유화학 원료 가격의 변동과 포름알데히드 배출 규제의 진화는 단기적으로 비용과 컴플라이언스 문제를 야기하고, 이익률 압박과 배합 개발 기간의 장기화를 초래할 수 있습니다.

세계 콘크리트 혼화제 시장 동향과 인사이트

아시아태평양 인프라 대형 프로젝트

지역 철도 회랑, 공항, 스마트 시티 계획에 대한 정부 지출은 사양 기준을 재정의하고 다양한 기후대에서 슬럼프 유지 및 내구성을 제공하는 혼화제에 대한 수요를 촉진하고 있습니다. 중국의 '일대일로' 구상은 국경을 초월한 프로젝트 파이프라인을 확대하고, 인도네시아의 신수도 계획과 인도의 국가 인프라 계획은 안정적인 수주 전망을 가져왔습니다. 프로젝트 소유자는 장시간의 운송 시간에도 유변학적 특성을 유지하는 고품질 첨가제를 선호합니다. 이를 통해 기술 문서를 보유한 공급업체는 더 높은 이익률을 확보할 수 있습니다. 공공 입찰에는 상품 등급이 아닌 성능 조항이 명시되어 있고, 가치 엔지니어링된 대체품은 엄격한 테스트 프로토콜을 통과해야하므로 콘크리트 혼화제 시장은 평균 판매 가격 상승의 혜택을 누리고 있습니다.

고성능 콘크리트 및 자기충진 콘크리트의 급속한 대중화

셀프 필링 콘크리트는 프리캐스트 전용에서 현장 타설용으로 전환되고 있습니다. 이는 시산업체가 노동력 절감과 품질 신뢰성을 요구하기 때문입니다. 타설 주기가 최대 40% 단축되고 표면 결함이 현저하게 감소하므로 SCC는 고층 빌딩의 핵심부 및 복잡한 거푸집 공사에서 선호되는 선택이 되었습니다. 8,000psi 이상의 압축강도를 목표로 하는 프로젝트에서 고성능 감수제와 시멘트계 보강재를 함께 사용하는 경우가 증가하고 있으며, 콘크리트 혼화제 시장은 보다 진보된 기술 지원 패키지로 전환하고 있습니다. 유럽의 내구성 기준은 세계 기준점 역할을 하며, 북미와 아시아에서 사업을 운영하는 다국적 기업이 보다 엄격한 배합 성능 기준을 준수하도록 유도하고 있습니다.

변동하는 석유화학 원료 가격

에틸렌 및 프로파일렌 유도체의 분기별 30% 이상의 가격 변동은 특히 헤지 능력이 없는 생산자의 경우 고성능 감수제의 비용 구조를 직접적으로 증가시킵니다. 물류 추가 요금과 관세는 지역 격차를 악화시키고, 현물 가격 차이를 발생시키며, 입찰 견적을 복잡하게 만듭니다. 중소기업은 이러한 충격을 흡수하는 데 어려움을 겪고, 경우에 따라는 장기계약을 맺는 수직계열화된 대기업에 점유율을 빼앗기기도 합니다. 따라서 콘크리트 혼화제 시장은 일시적인 이익률 압박에 직면하여 초기 가격이 높은 비석유 유래 대체품에 대한 관심이 높아지고 있습니다.

부문 분석

인프라 부문은 2025년 교통 회랑 및 유틸리티 업그레이드에 대한 정부 지출에 힘입어 콘크리트 혼화제 시장 점유율 39.62%를 유지했습니다. 주택 건설은 팬데믹 기간 중 주택 부양책에 힘입어 CAGR 6.78%로 진행 중이며, 2031년까지 격차를 좁힐 것으로 예측됩니다. 주택 분야의 콘크리트 혼화제 시장 확대는 엄격한 배합 균일성이 요구되는 조립식 패널의 채택과 맞물려 있습니다. 단독주택 기초공사에서는 블리드(혼화제 분리)를 억제하면서 내구성을 높이는 감수제 채용이 증가하고 있습니다. 한편, 30층 이상의 고층 공동주택에서는 펌프 수송성을 확보하기 위해 고성능 감수제를 채택하고 있습니다.

상업용 프로젝트(특히 사무실 개보수 및 데이터센터)가 수요의 약 1/4을 차지하며, 초기 강도와 저수축성 마무리를 모두 만족시키는 혼화제가 선택되고 있습니다. 산업 및 공공시설 건설이 나머지를 차지하며, 바닥재와 구조부재에 내화학성이 요구됩니다. 부문별 구성으로 볼 때, 유틸리티에 따른 안정적인 기반 수요를 시사하며, 주택담보대출 시장의 건전화 및 도시지역 주택 고밀도화 추세에 따른 상승 여력이 예상됩니다.

지역별 분석

아시아태평양은 2025년 콘크리트 혼화제 시장의 31.58%를 차지하며 6.79%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 중국은 여전히 핵심적인 역할을 담당하고 있지만, 품질과 환경 관리를 중시하는 규제 변화로 인해 수십 년간의 내구성 기준을 충족하는 고품질 혼화제에 대한 수요가 증가하고 있습니다. 인도와 인도네시아에서는 대규모 교통 인프라 및 도시 개발 계획이 성장의 견인차 역할을 하고 있으며, 일본과 한국에서는 디지털 배칭 기술 도입이 선행되고 있습니다. 지역 공급업체는 물류 측면에서 우위를 점하고 있지만, 성능 기준의 국제화에 따라 외국산 고성능 감수제 브랜드의 침투가 진행되고 있습니다.

북미의 성숙한 건설 생태계는 인프라 개보수 및 주택 착공에 따른 안정적인 수요가 지속되고 있습니다. 노동력 부족으로 인해 자가 충전 콘크리트의 채용이 진행되어 대규모 레미콘 차량대에서는 디지털 투약 제어가 필수적입니다. 연방 인프라 법안으로 인해 교량 및 도로 보수에 대한 지출이 확대되면서 혼화제 수요는 부식 방지 및 수축 감소 카테고리로 이동하고 있습니다.

유럽의 점유율은 EU Taxonomy 등 탄소 최적화 배합을 촉진하는 엄격한 지속가능성 규제에 기인합니다. 독일과 영국은 철도 확장 및 도시 재생 계획으로 소비를 주도하고 있으며, 프랑스와 이탈리아는 색조 균일성과 노출 마감을 필요로 하는 건축용도를 추진하고 있습니다. 동유럽에서는 결속기금 지원 고속도로 프로젝트가 성장의 여지를 제공하고 있으며, 저투수성 콘크리트의 지정이 증가하는 추세입니다.

남미, 중동 및 아프리카는 전체적으로 더 작은 점유율을 차지하지만, 브라질과 UAE의 메가 프로젝트 계획에 따라 두 자릿수 성장 지역이 존재합니다. 환율 변동과 상품 사이클은 조달을 복잡하게 만들지만, 현지 생산자는 수입 관세에 따른 국내 조달 우대 정책으로 높은 가동률을 확보할 수 있는 경우가 많습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제8장 CEO 여러분에게 향한 주요 전략적 과제

KSA 26.03.05The Concrete Admixtures Market was valued at USD 18.16 billion in 2025 and estimated to grow from USD 19.31 billion in 2026 to reach USD 26.26 billion by 2031, at a CAGR of 6.34% during the forecast period (2026-2031).

The market's growth is driven by government-backed infrastructure programs in the Asia-Pacific region, stricter water-reduction standards in developed economies, and the rapid adoption of self-consolidating concrete, which boosts productivity while reducing material waste. Contractors are broadening the adoption of AI-guided dosage platforms, which refine mix consistency and trim admixture overuse. The residential sector's rebound and mounting preference for bio-based chemistries further widen opportunity windows. Competitive intensity remains moderate because regional producers occupy niche positions based on logistics advantages and local regulatory familiarity, even as global suppliers strive to patent polymer innovations and integrate digital features. Volatile petrochemical feedstock prices and evolving formaldehyde emission limits pose short-term cost and compliance challenges that can squeeze margins and lengthen formulation timelines.

Global Concrete Admixtures Market Trends and Insights

Infrastructure Mega-Projects in Asia-Pacific

Government outlays for regional rail corridors, airports, and smart-city programs are redefining specification criteria, moving demand toward admixtures that deliver extended slump retention and durability across varied climatic zones. China's Belt and Road Initiative amplifies cross-border project pipelines, while Indonesia's new capital and India's National Infrastructure Pipeline add steady order visibility. Project owners favor premium additives that maintain rheology under long haul times, enabling suppliers with technical documentation to secure higher margins. The concrete admixtures market benefits from average selling price uplift because public tenders list performance clauses rather than commodity grades, and value-engineered alternatives must clear rigorous test protocols.

Rapid Adoption of High-Performance and SCC Concrete

Self-consolidating concrete has shifted from precast exclusivity to cast-in-place usage as contractors seek labor savings and quality reliability. Placement cycle times decrease by up to 40%, and surface defects noticeably drop, making SCC a preferred option in high-rise cores and complex formwork applications. Projects exceeding 8,000 psi compressive strength targets increasingly combine superplasticizers with supplementary cementitious materials, nudging the concrete admixtures market toward higher technical support bundles. European durability codes act as global reference points, pushing multinationals operating in North America and Asia to align with stricter mix performance thresholds.

Volatile Petrochemical Feedstock Prices

Quarterly swings of 30% or more in ethylene and propylene derivatives directly inflate superplasticizer cost structures, especially for producers without hedging capacity. Logistics surcharges and customs duties exacerbate regional disparities, resulting in spot-price spreads that complicate tender quotations. Smaller enterprises struggle to absorb shocks, sometimes ceding share to vertically integrated majors that lock in term contracts. The concrete admixtures market thus faces temporary margin compression and heightened interest in non-petroleum alternatives, albeit at higher initial price points.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Water-Reduction Regulations

- AI-Guided Dosage Optimization Platforms

- Formaldehyde-Emission Compliance Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The infrastructure segment retained 39.62% of the concrete admixtures market share in 2025, fueled by sovereign spending on transit corridors and utility upgrades. Residential construction, aided by pandemic-era housing stimulus packages, is progressing at a 6.78% CAGR and is on track to narrow the gap by 2031. The expansion of the concrete admixtures market size in housing aligns with the adoption of prefabricated panels, where stringent mix consistency is crucial. Single-family foundations increasingly specify water-reducing agents that cut bleed while boosting durability, whereas multifamily towers incorporate superplasticizers for pumpability at heights exceeding 30 stories.

Commercial projects, notably office retrofits and data centers, occupy about one-quarter of demand, selecting admixtures that balance early strength with low-shrinkage finishes. Industrial and institutional builds round out the remainder, seeking chemical resistance in floors and structural components. The segment mix implies stable base volume from public works, with upside from a healthier mortgage market and urban residential densification trends.

The Concrete Admixtures Market Report is Segmented by End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), Product Type (Accelerator, Air-Entraining, High-Range Water-Reducer, Retarder, Shrinkage-Reducing, Viscosity Modifier, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region carried 31.58% of the concrete admixtures market in 2025 and is projected to grow at a 6.79% CAGR. China remains pivotal, yet its regulatory shift toward quality and environmental stewardship intensifies demand for premium admixtures that meet multi-decade durability benchmarks. India and Indonesia provide incremental momentum through marquee transport and city-building programs, while Japan and South Korea lead the way in digital batching adoption. Regional suppliers benefit from lower logistics hurdles; however, the penetration of foreign superplasticizer brands widens as performance standards integrate international norms.

North America's mature construction ecosystem registers steady volume tied to infrastructure refurbishments and residential starts. Labor constraints have driven the adoption of self-consolidating concrete, making digital dosage control a must-have in large ready-mix fleets. Federal infrastructure bills shift spending toward bridge and roadway rehabilitation, steering admixture demand toward corrosion-inhibiting and shrinkage-reducing categories.

Europe's share stems from robust sustainability regulations, such as the EU Taxonomy, which push for carbon-optimized mixes. Germany and the United Kingdom lead the way in consumption, with rail extensions and urban renewal plans, whereas France and Italy are advancing architectural applications that require color consistency and exposed finishes. Eastern Europe offers growth headroom through cohesion fund-backed highway projects, which increasingly stipulate low-permeability concrete.

South America, the Middle East, and Africa collectively hold a smaller slice, yet they provide pockets of double-digit expansion aligned with megaproject calendars in Brazil and the UAE. Currency fluctuations and commodity cycles complicate procurement; yet, local producers often secure higher utilization rates thanks to import tariffs that favor domestic sourcing.

- CEMEX S.A.B. de C.V.

- CICO Group

- CMB

- Guangdong Redwall New Materials Co.,Ltd

- Jiangsu Subote New Materials Co., Ltd.

- Kao Corporation

- MAPEI S.p.A.

- MC-Bauchemie

- MUHU (China) Construction Materials Co., Ltd.

- Pidilite Industries Limited

- RPM International

- Saint-Gobain

- Sika AG

- SOCHEM

- Xypex Chemical Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure mega-projects in Asia-Pacific

- 4.2.2 Rapid adoption of high-performance and SCC concrete

- 4.2.3 Stricter water-reduction regulations

- 4.2.4 AI-guided dosage optimisation platforms

- 4.2.5 Bio-based admixtures from agri-waste streams

- 4.3 Market Restraints

- 4.3.1 Volatile petro-chemical feedstock prices

- 4.3.2 Low-cost conventional concrete alternatives

- 4.3.3 Formaldehyde-emission compliance risks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 By Product Type

- 5.2.1 Accelerator

- 5.2.2 Air-Entraining

- 5.2.3 High-Range Water-Reducer (Superplasticizer)

- 5.2.4 Retarder

- 5.2.5 Shrinkage-Reducing

- 5.2.6 Viscosity Modifier

- 5.2.7 Water-Reducer (Plasticizer)

- 5.2.8 Other Types

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 South Korea

- 5.3.1.8 Thailand

- 5.3.1.9 Vietnam

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CEMEX S.A.B. de C.V.

- 6.4.2 CICO Group

- 6.4.3 CMB

- 6.4.4 Guangdong Redwall New Materials Co.,Ltd

- 6.4.5 Jiangsu Subote New Materials Co., Ltd.

- 6.4.6 Kao Corporation

- 6.4.7 MAPEI S.p.A.

- 6.4.8 MC-Bauchemie

- 6.4.9 MUHU (China) Construction Materials Co., Ltd.

- 6.4.10 Pidilite Industries Limited

- 6.4.11 RPM International

- 6.4.12 Saint-Gobain

- 6.4.13 Sika AG

- 6.4.14 SOCHEM

- 6.4.15 Xypex Chemical Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment