|

시장보고서

상품코드

1939573

아스팔트 개질제 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asphalt Modifiers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

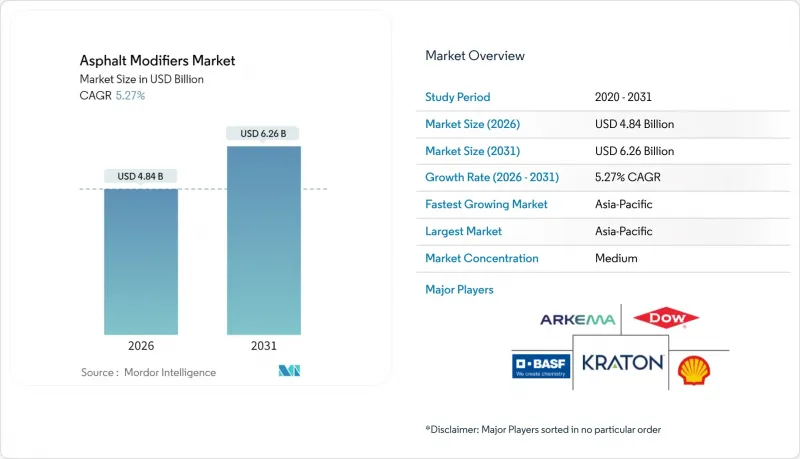

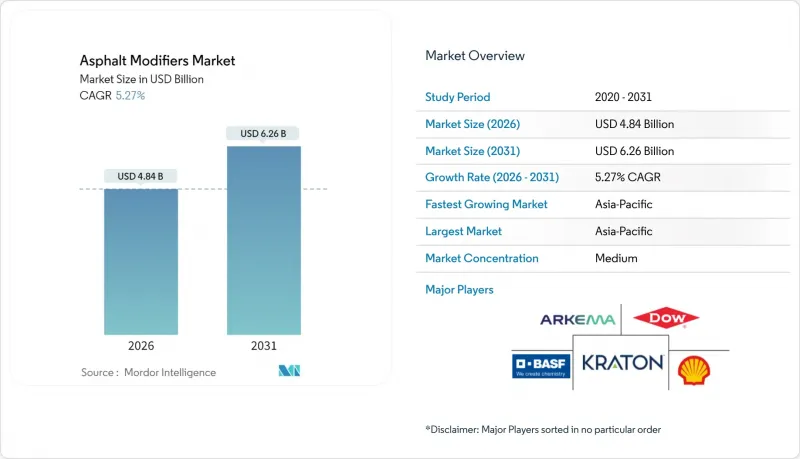

아스팔트 개질제 시장 규모는 2026년에는 48억 4,000만 달러로 추정되며, 2025년 46억 달러에서 성장이 전망됩니다.

2031년까지 62억 6,000만 달러에 달할 것으로 예상되며, 2026-2031년 연평균 5.27%의 성장률을 보일 것으로 전망됩니다.

유틸리티 예산의 확대, 엄격한 성능 기준에 기반한 도로 사양, 지속가능한 아스팔트 기술로의 점진적인 전환이 이러한 꾸준한 성장을 주도하고 있습니다. 아시아태평양은 야심찬 고속도로 확장, 교통량 증가, 급속한 도시화로 인해 고분자 개질 바인더에 대한 수요가 지속되고 있으며, 가장 규모가 큰 지역 기반을 유지하고 있습니다. 북미와 유럽에서는 보급률이 성숙 단계에 이르렀지만, 수명주기 비용 절감과 순 제로 지침으로 인해 프리미엄 개질제에 대한 수요가 지속되고 있습니다. 원유 가격에 연동된 불안정한 폴리머 가격과 아스팔트 연기에 대한 직장 안전 규제 강화로 인해 아스팔트 개질제 시장은 비용 및 규정 준수에 대한 리스크가 발생하고 있습니다. 제조업체들은 공급망 확대, 바이오 제품 포트폴리오 확대, 도로 관리 기관과의 기술 제휴 강화 등을 통해 이러한 압력에 대응하고 있습니다.

세계 아스팔트 개질제 시장 동향과 인사이트

포스트 코로나 유틸리티 프로그램에서의 인프라 지출 회복

새로운 경기 부양책으로 인해 유틸리티 기관이 최저 가격 입찰보다 장수명 포장을 우선시하는 경향이 강해지면서 프리미엄 바인더에 대한 수요가 지속되고 있습니다. 미국 인프라 투자 고용법에서만 1,100억 달러가 고속도로 및 교량에 할당되었고, 중국, 인도, 동남아시아에서도 같은 규모의 자금 투입이 잇따르고 있으며, 중교통로용 폴리머 개질 아스팔트가 중요시되고 있습니다. 이러한 자금 배분은 검증된 성능 데이터를 제공하는 공급업체에게 유리한 안정적인 프로젝트 파이프라인으로 이어집니다. 이러한 자금 환경 하에서 사양 수립 담당자들은 납세자의 투자매출을 극대화하기 위해 개질제를 중요시하는 경향이 강해지고 있습니다.

높은 교통 밀도와 중축 하중

E-Commerce와 산업 활동의 급격한 성장으로 화물 운송이 활발해지면서 차축 응력이 기존의 설계 한계를 크게 초과하고 있습니다. 현장 시험에서 SBS 개질 바인더는 비개질 아스팔트에 비해 동적 안정성 지수를 최대 10배까지 향상시키고, 트럭 통행시 굴착 깊이를 크게 감소시키는 것으로 나타났습니다. 교통부는 현재 항만 진입로 및 물류 회랑 입찰에 폴리머 요구 사항을 포함시켜 고탄성 개질제에 대한 지속적인 수요를 보장하고 있습니다.

고분자 개질 아스팔트의 초기 비용

기존 바인더 대비 15-25%의 프리미엄 가격은 여전히 최저 초기 입찰가를 우선시하는 조달 규정 하에서 채택을 가로막고 있습니다. 예산이 부족한 지자체에서는 개질제 도입을 미루고 기본적인 포장재 갱신을 선택. 수명주기 비용 절감 효과에도 불구하고 단기적인 성장 전망은 둔화되고 있습니다.

부문 분석

물리적 개질제는 2025년 아스팔트 개질제 시장의 54.10%를 차지하며 매출 측면에서 우위를 유지했습니다. SBS(스티렌-부타디엔-스티렌)와 EVA(에틸렌-초산비닐)는 여전히 고하중 및 극한의 온도 환경에서 포장에 널리 사용되고 있습니다. 이 부문에서는 SBS가 탄성 회복성과 정유사 등급 아스팔트와의 궁합이 좋아 압도적인 점유율을 차지하고 있습니다. 화학적 개질제는 수량은 적지만, 환경 규제와 내습성 요구사항을 충족하는 고온 혼합용 촉매 및 박리 방지제를 배경으로 5.36%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 하위 카테고리입니다. 타이어 재활용 촉진책에 힘입어 고무 부스러기 개질제는 폐기물의 매립처분을 피하면서 노면 내구성을 높이려는 지자체들 사이에서 보급이 확대되고 있습니다. 섬유, 광물, 나노 보강재의 각 카테고리는 물리적 특성 범위를 보완하고 틈새 내구성 요구 사항을 충족시킵니다.

향후 이해관계자들은 폴리머와 생화학 재생제를 융합한 하이브리드 시스템을 통해 강성, 내균열성, 지속가능성의 균형을 맞출 수 있을 것으로 전망하고 있습니다. 유럽의 주요 프로젝트에서 리그닌 폴리머 하이브리드가 SBS와 동등한 성능 등급을 달성하면서 저탄소화를 실현한 사례가 제시되고 있습니다. 신뢰할 수 있는 바이오 원료 공급원을 확보하고 배합 호환성 문제를 극복한 공급업체는 탈탄소화가 가속화됨에 따라 높은 수익성을 확보할 수 있을 것입니다.

아스팔트 개질제 보고서는 개질제 유형(물리적 개질제, 화학적 개질제), 아스팔트 혼합 기술(핫믹스 아스팔트, 웜믹스 아스팔트, 콜드 및 하프 웜믹스), 용도(포장, 루핑, 기타 용도), 지역(아시아태평양, 북미, 유럽, 유럽, 남미, 중동 및 아프리카)으로 분류됩니다. 남미, 중동 및 아프리카) 별로 분류되어 있습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 아스팔트 개질제 시장의 38.25%를 차지할 것으로 예상되며, 수조 달러 규모의 고속도로 및 벨트 코리더십에 힘입어 5.81%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 중국은 2025년까지 12만km 이상의 고품질 고속도로를 완성하고, 국내 정유사들은 내수 수요를 충족시키기 위해 SBS 라인의 병목현상을 지속적으로 해소하고 있습니다. 인도의 회랑 계획과 공항 활주로 확장은 몬순 주기와 무거운 화물을 견딜 수 있는 고성능 바인더에 대한 지역적 수요를 더욱 가속화시키고 있습니다. 동남아시아 국가들은 신속한 배치가 가능한 모듈식 아스팔트 플랜트에 투자하고 있으며, 세계 유수의 기업이 공급하는 즉시 사용 가능한 폴리머 펠릿을 선호하고 있습니다.

북미에서는 성능 등급 사양을 포함한 포장재 갱신 프로젝트가 장기적으로 지속되는 '인프라 투자 및 고용법'에 의해 시장이 지원되고 있습니다. 미국 주 교통국의 80% 이상이 주간 고속도로에 개질 아스팔트 사용을 의무화하고 있으며, 성숙하면서도 탄탄한 매출 기반을 유지하고 있습니다. 캘리포니아, 워싱턴 등 CO2 감축 목표가 적극적인 주에서는 온배합 아스팔트 도입이 특히 빠르며, 화학첨가제 공급업체들은 유통 거점을 지역화해야 하는 상황에 처해 있습니다.

유럽은 생산량은 적지만 'Fit for 55' 규제에 따라 탄소 최적화 바인더 솔루션에 대한 선구적인 노력을 기울이고 있습니다. 이 지역에서는 이미 많은 국가 계약에서 온혼합 아스팔트를 의무화하고 있으며, 리그닌과 폴리머의 하이브리드 기술에 대한 첨단인 연구를 지원하고 있습니다. 예를 들어 스칸디나비아 국가 기관에서는 저온기술로 인한 CO2 감축량 1톤당 계약자에게 보상금을 지급하고 있으며, 이로 인해 온배합 아스팔트용 개질제 수요가 확대되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05Asphalt Modifiers Market size in 2026 is estimated at USD 4.84 billion, growing from 2025 value of USD 4.60 billion with 2031 projections showing USD 6.26 billion, growing at 5.27% CAGR over 2026-2031.

Expanding public-works budgets, stringent performance-based road specifications, and the gradual switch to sustainable asphalt technologies drive this steady growth. Asia-Pacific retains the largest regional foothold as ambitious highway expansions, heavier traffic loads, and rapid urbanization sustain demand for polymer-modified binders. North America and Europe show mature penetration rates but continue to favor premium modifiers thanks to lifecycle cost savings and net-zero directives. Volatile crude-linked polymer prices, coupled with tighter workplace-safety rules on asphalt fumes, introduce cost and compliance risks in the asphalt modifiers market. Producers counter these pressures by scaling supply chains, widening bio-based portfolios, and deepening technical partnerships with road agencies.

Global Asphalt Modifiers Market Trends and Insights

Infrastructure Spending Rebound in Post-COVID Public Works Programs

Fresh stimulus packages sustain demand for premium binders as agencies favor longer-life pavements over least-cost bids. The U.S. Infrastructure Investment and Jobs Act alone earmarked USD 110 billion for highways and bridges, and comparable funding waves in China, India, and Southeast Asia emphasize polymer-modified asphalt for heavy-duty corridors. These allocations translate into consistent project pipelines that reward suppliers offering proven performance data. Under this funding climate, specification writers increasingly treat modifiers as critical for maximizing return on taxpayer investment.

High Traffic Density and Heavier Axle Loads

Booming e-commerce and industrial activity intensify freight movements, raising axle stresses well above legacy design limits. Field trials show SBS-modified binders boosting dynamic-stability indices by up to tenfold compared with unmodified asphalt, sharply cutting rut depth under truck traffic. Transport ministries now embed polymer requirements in tenders for port approaches and logistics corridors, ensuring recurrent volumes for high-modulus modifiers.

High Upfront Cost of Polymer-Modified Asphalt

Premiums of 15-25% over conventional binders deter adoption where procurement rules still favor lowest initial bids. Municipalities with tight budgets postpone modifier uptake in favor of basic resurfacing, muting short-run growth prospects despite clear lifecycle savings.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Performance-Based Asphalt Specifications (Superpave)

- Net-Zero Carbon Mandates for Road Construction

- Occupational and Fume-Exposure Health Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Physical modifiers dominated revenue with a 54.10% asphalt modifiers market share in 2025 as SBS and EVA remained ubiquitous for heavy-load and temperature-extreme pavements. Within this segment, SBS captured the lion's portion owing to its elastic recovery and compatibility with refinery-grade asphalt. Chemical modifiers, albeit smaller in volume, are the fastest-growing subset at a 5.36% CAGR, underpinned by warm-mix catalysts and anti-stripping agents that satisfy environmental and moisture-resistance mandates. Rubber crumb modifiers, propelled by tire-recycling incentives, are gaining ground among municipalities aiming to divert waste from landfills while adding resilience to road surfaces. Fiber, mineral, and nano-reinforcement families round out the physical spectrum and answer niche durability demands.

Looking ahead, stakeholders foresee hybrid systems that blend polymers with biochemical rejuvenators to balance stiffness, crack resistance, and sustainability credentials. Flagship projects in Europe showcase lignin-polymer hybrids achieving performance grades equivalent to SBS while claiming lower embodied carbon. Suppliers that secure dependable bio-feedstock streams and master compound-compatibility issues could carve profitable positions as decarbonization accelerates.

The Asphalt Modifiers Report is Segmented by Modifier Type (Physical Modifiers, and Chemical Modifiers), Asphalt Mix Technology (Hot-Mix Asphalt, Warm-Mix Asphalt, and Cold and Half-Warm Mix), Application (Paving, Roofing, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38.25% asphalt modifiers market share in 2025 and is advancing at a 5.81% CAGR, propelled by multi-trillion-dollar highway and belt-corridor initiatives. China completed more than 120,000 km of high-grade expressways by 2025, and domestic refiners continue debottlenecking SBS lines to meet internal demand. India's corridor programs, coupled with airport-runway expansions, further tilt regional growth toward high-performance binders that outlast monsoon cycles and heavy freight. Southeast Asian members invest in modular asphalt plants designed for quick deployment, which favor ready-to-dose polymer pellets supplied by global majors.

North America is buoyed by the Infrastructure Investment and Jobs Act's long runway of resurfacing projects that embed performance-graded specifications. Over 80% of U.S. state DOTs now require modified asphalt for interstate highways, sustaining a mature but sturdy revenue base. Warm-mix adoption is especially fast in states with aggressive CO2-reduction targets, such as California and Washington, compelling chemical-additive suppliers to localize distribution points.

Europe, while smaller in tonnage, pioneers carbon-optimized binder solutions under Fit-for-55 regulations. The region already mandates warm-mix for many national contracts and sponsors advanced research into lignin-polymer hybrids. Scandinavian agencies, for instance, reimburse contractors for every ton of CO2 saved via low-temperature techniques, thereby amplifying demand for WMA modifiers.

- Arkema

- BASF

- Cargill, Incorporated

- Dow

- Engineered Additives LLC

- Evonik Industries AG

- Exxon Mobil Corporation

- Genan Holding A/S

- Honeywell International Inc.

- Iterchimica SpA

- Kao Corporation

- Kraton Corporation

- McAsphalt Industries Limited

- Nouryon

- PQ Corporation

- Sasol

- Shell plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure Spending Rebound in Post-COVID Public Works Programs

- 4.2.2 High Traffic Density and Heavier Axle Loads

- 4.2.3 Adoption of Performance-Based Asphalt Specifications (eg., Superpave)

- 4.2.4 Net-Zero Carbon Mandates for Road Construction

- 4.2.5 Surge in Graphene-Enhanced Binder Research

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Polymer-Modified Asphalt

- 4.3.2 Occupational and Fume-Exposure Health Concerns

- 4.3.3 Volatile Prices of SBS/SEBS and Other Polymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Modifier Type

- 5.1.1 Physical Modifiers

- 5.1.1.1 Plastics (HDPE, SBS, EVA)

- 5.1.1.2 Rubber (crumb-rubber, devulcanized)

- 5.1.1.3 Fibers (cellulose, aramid, glass)

- 5.1.1.4 Mineral fillers and extenders

- 5.1.2 Chemical Modifiers

- 5.1.2.1 Anti-stripping Agents

- 5.1.2.2 Warm-mix Additives

- 5.1.2.3 Rejuvenators and Antioxidants

- 5.1.2.4 Others (nano-clay, graphene)

- 5.1.1 Physical Modifiers

- 5.2 By Asphalt Mix Technology

- 5.2.1 Hot-Mix Asphalt (HMA)

- 5.2.2 Warm-Mix Asphalt (WMA)

- 5.2.3 Cold and Half-Warm Mix

- 5.3 By Application

- 5.3.1 Paving

- 5.3.2 Roofing

- 5.3.3 Other Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Australia

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Arkema

- 6.4.2 BASF

- 6.4.3 Cargill, Incorporated

- 6.4.4 Dow

- 6.4.5 Engineered Additives LLC

- 6.4.6 Evonik Industries AG

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 Genan Holding A/S

- 6.4.9 Honeywell International Inc.

- 6.4.10 Iterchimica SpA

- 6.4.11 Kao Corporation

- 6.4.12 Kraton Corporation

- 6.4.13 McAsphalt Industries Limited

- 6.4.14 Nouryon

- 6.4.15 PQ Corporation

- 6.4.16 Sasol

- 6.4.17 Shell plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Emerging Preference for Warm-Mix Asphalt