|

시장보고서

상품코드

1939578

태국의 플라스틱 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Thailand Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

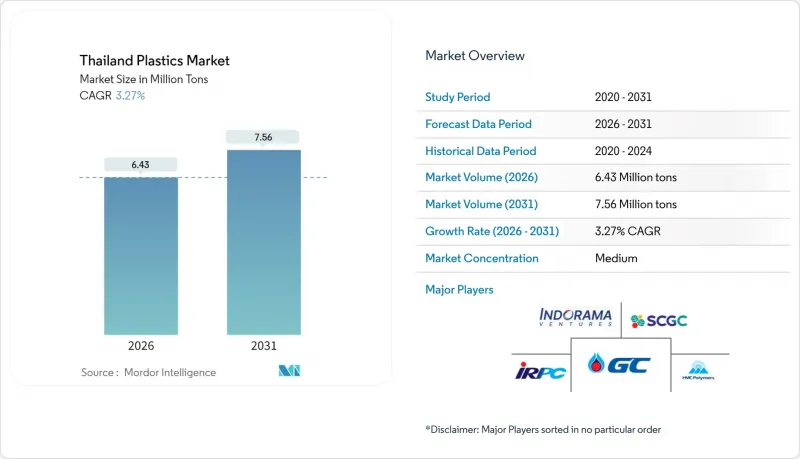

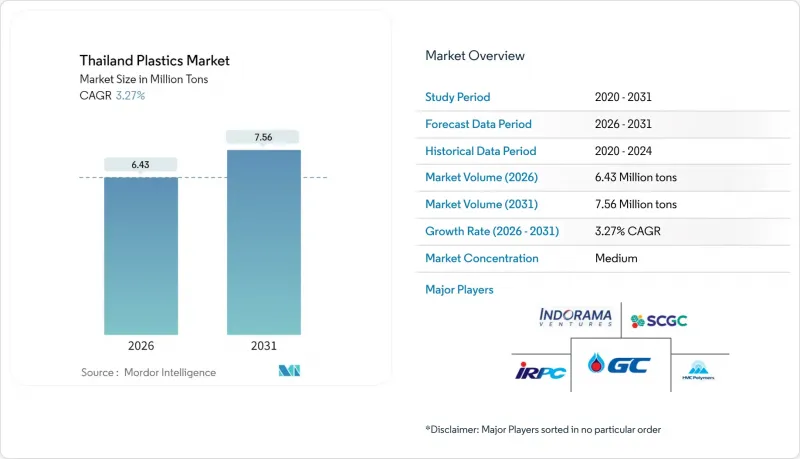

태국의 플라스틱 시장 규모는 2026년에는 643만 톤으로 추정되며, 2025년 623만 톤으로부터 성장이 전망됩니다.

2031년의 예측에서는 756만 톤에 달하며, 2026-2031년에 CAGR 3.27%로 확대할 전망입니다.

이러한 완만한 성장률의 배경에는 저탄소 원료로의 전환, 순환경제의 실천, 특수 용도로의 확장 등 결정적인 변화가 숨어있으며, 범용 제품의 스프레드가 축소되는 가운데서도 이익률을 높이고 있습니다. 기존 수지가 생산량의 주류를 차지하는 가운데, 바이오폴리머로의 전환이 빠르게 진행되고 있으며, 합작을 통한 바이오에틸렌과 PLA(폴리유산)의 대규모 생산능력 확대가 이를 지원하고 있습니다. 식품, 음료, E-Commerce 포장 분야에서 가장 강력한 수요 모멘텀을 보이고 있으며, 전기자동차 공급망의 부상과 대규모 인프라 프로젝트가 엔지니어링 수지와 고성능 컴파운드에 대한 새로운 수요를 창출하고 있습니다. 중국공급과잉 심화, 나프타 가격 변동, 폐기물 규제 강화로 이익률이 압박을 받고 있는 가운데, 원료 다변화와 재활용 인프라에 투자하는 기업이 태국의 플라스틱 시장에서 매출을 보호할 수 있는 가장 좋은 위치에 있습니다.

태국의 플라스틱 시장 동향 및 분석

식품 및 음료 포장 분야 수요 증가

국내 음료 소비는 지속적으로 확대되고 있으며, 포장 수요를 안정적으로 지원하고 있습니다. 2025년 3월부터 시행되는 새로운 식품 접촉 기준은 컨버터 기업이 재활용 가능하고 내열성이 있는 고부가가치 제품으로의 전환을 촉진하고 있습니다. 이웃 국가인 캄보디아와 베트남으로의 음료 수출이 수요를 증가시켰고, 팬데믹 이후 두 배 이상 성장한 음식 배달은 주문 당 여러 개의 플라스틱 제품을 사용하고 있습니다. 기온 상승, 급속한 도시화, 관광업의 회복과 함께 태국의 플라스틱 시장의 포장 수요 증가는 지속될 것으로 예측됩니다. 화장품 및 건강 제품 매출이 한 자릿수 성장세를 보이는 퍼스널케어 분야와 함께 경질 용기에 대한 수요도 확대되고 있으며, 전문 포장재 채택을 촉진하고 있습니다.

건축 및 건설 분야의 플라스틱 사용량 증가

150개 이상의 인프라 프로젝트에 대한 정부 지출은 PVC 파이프, 단열재, 지붕 시트에 대한 장기적인 수요를 지원하고 있습니다. 1km당 최대 5톤의 재생재료를 투입하는 '플라스틱 도로' 구상은 순환형 건설 방식으로의 정책 전환을 의미하며, 재생수지의 잠재적 시장을 확대할 수 있습니다. 현재 800개 이상의 중견 및 대형 제조업체들이 그린 빌딩 기준을 충족하기 위해 디지털 발주 툴와 저탄소 프로세스를 도입하고 있습니다. 메가 프로젝트 관련 신규 고용 100만개 창출이 예상되며, 주택 및 상업용 건축을 촉진할 것입니다. 이에 따라 에너지 가격 상승과 중국산 저가 제품 수입으로 인한 이익률 압박에도 불구하고 플라스틱 건축자재 제품 수요는 견고하게 유지될 것으로 보입니다.

일회용 플라스틱 규제 강화 및 과세

태국의 플라스틱 폐기물 대책 로드맵에 따르면 2025년 1월부터 수입 금지와 식품 접촉 제품의 품질 기준 강화가 단계적으로 시행될 예정입니다. 방콕과 같은 도시 지역에서는 하루 1,800톤의 일회용 폐기물이 발생하고 있으며, 당국은 컨버터 기업의 컴플라이언스 비용을 증가시키는 과세 및 표시 의무를 신속하게 추진하고 있습니다. 산업폐기물 관리법안에는 환경영향 복구를 위한 전용기금 조성 및 유해 스크랩의 엄격한 폐기 규정이 추가되었습니다. 태국의 플라스틱 시장의 생산자들은 인증된 재생 또는 퇴비화 가능한 대체품에 투자하고 추적 시스템을 강화해야 하며, 이를 따르지 않을 경우 처벌을 받을 수 있습니다. 이러한 규제는 처음에는 일회용 제품을 제한하는 것이지만, 궁극적으로 고부가가치의 지속가능한 수지에 대한 수요를 촉진하는 역할을 할 것입니다.

부문 분석

2025년 기준, 태국의 플라스틱 시장 점유율의 70.55%는 기존형 수지가 차지했습니다. 이는 이미 구축된 인프라, 규모의 경제, 다양한 최종 용도로의 확장에 기인합니다. 그 중 폴리에틸렌과 폴리프로필렌은 포장, 자동차, 건설 분야 수요를 지탱하고 있으며, PET는 병 용도를 넘어 산업용 원사, 타이어 원단으로 용도가 확대되고 있습니다. HMC 폴리머는 2023년 매출 250억 바트를 돌파하여 범용 등급의 상업적 중요성이 지속되고 있음을 보여줍니다. 폴리아미드, 폴리카보네이트 등 엔지니어링 수지는 전자기기 조립 및 EV 파워트레인 용도에 연동되어 한 자릿수 중반 수요 증가율을 기록했습니다.

바이오폴리머는 가장 빠르게 성장하고 있는 카테고리로, 20만 톤의 바이오에틸렌 사업과 7만5천 톤의 PLA 생산량 증가에 힘입어 연평균 5.53%의 성장세를 보이고 있습니다. 주요 제조업체들은 현재 자산 기반의 미래를 보장하고 새로운 식품 접촉 규제 하에서 경쟁력을 유지하기 위해 화학적 재활용 경로와 순환 나프타 스트림의 실증 시험을 진행하고 있습니다. 기존 공급업체들이 바이오프로세스에 대한 라이선스를 부여하는 가운데, 신규 진입 업체들은 탄소발자국 선언과 퇴비화 가능 인증으로 차별화를 꾀하고 있으며, 경쟁 격차가 축소되는 추세입니다.

태국의 플라스틱 시장 보고서는 유형별(일반 플라스틱, 엔지니어링 플라스틱, 바이오플라스틱), 용도별(포장, 전기/전자, 건축/건설, 자동차/운송기기, 가구/침구, 기타 용도)로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06Thailand Plastics Market size in 2026 is estimated at 6.43 million tons, growing from 2025 value of 6.23 million tons with 2031 projections showing 7.56 million tons, growing at 3.27% CAGR over 2026-2031.

This moderate headline growth conceals a decisive shift toward low-carbon feedstocks, circular economy practices, and specialty applications that lift margins even as commodity spreads tighten. Traditional resins dominate volumes, yet a rapid pivot to biopolymers is underway because joint ventures are unlocking bio-ethylene and PLA capacity at scale. Demand momentum remains strongest in food, beverage, and e-commerce packaging, but the emergence of an electric-vehicle supply chain and large-scale infrastructure projects creates fresh pull for engineering resins and high-performance compounds. Intensifying Chinese oversupply, volatile naphtha costs, and stricter waste regulations pressure margins; firms that diversify feedstocks and invest in recycling infrastructure are best placed to protect returns in the Thailand plastics market.

Thailand Plastics Market Trends and Insights

Rising Demand from Food and Beverage Packaging

Domestic beverage consumption continues to expand, locking in steady packaging tonnage. New food-contact standards effective March 2025 encourage converters to adopt recyclable and heat-resistant formulations that command premium pricing. Beverage exports to neighboring Cambodia and Vietnam add incremental volumes, and food-delivery growth has more than doubled since the pandemic, generating multiple plastic items per order. Rising temperatures, rapid urbanization, and a tourism rebound sustain packaging intensity in the Thailand plastics market. Demand for rigid containers grows in parallel with the personal-care segment, where mid-single-digit sales growth of cosmetics and health products boosts specialized packaging uptake.

Increasing Plastics Use in Building and Construction

Government spending across over 150 infrastructure projects underwrites long-run demand for PVC pipes, insulation, and roofing sheets. The Plastic Roads initiative, which incorporates up to five tons of recycled material per kilometer, signals a policy pivot toward circular construction practices that enlarge the addressable market for recycled resin. More than 800 mid- and large-size manufacturers now integrate digital ordering tools and low-carbon processes to satisfy green-building specifications. An expected 1 million new jobs linked to megaprojects will spur residential and commercial builds, reinforcing demand for plastic building products even as energy inflation and cheap Chinese imports squeeze margins.

Stricter Single-Use-Plastic Bans and Taxes

Thailand's plastic-waste roadmap phases out imports from January 2025 and tightens quality rules for food-contact articles. Urban centers such as Bangkok generate 1,800 metric tons of single-use waste daily, prompting authorities to fast-track levies and labeling mandates that raise compliance costs for converters. Additional legislation under the Draft Industrial Waste Management Act introduces a dedicated fund to remediate environmental impacts and imposes stricter disposal rules on hazardous scrap. Producers in the Thailand plastics market must invest in certified recyclable or compostable alternatives and enhance traceability systems or face penalties. These rules initially restrict disposable items but ultimately catalyze demand for higher-value sustainable resins.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Needs in Automotive and EV Components

- Bio-Based Polymer Joint Ventures

- Polypropylene and Polyethylene Oversupply and Low-Cost Imports from China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional resins retained 70.55% of Thailand's plastics market share in 2025 thanks to entrenched infrastructure, scale economics, and diversified end-use exposure. Among them, polyethylene and polypropylene anchor packaging, automotive, and construction demand, while PET has grown beyond bottles into technical yarns and tire fabrics. HMC Polymers surpassed THB 25 billion in sales in 2023, illustrating the continuing commercial relevance of commodity grades. Engineering resins such as polyamides and polycarbonates post mid-single-digit demand gains tied to electronics assembly and EV power-train applications.

Biopolymers are the fastest-expanding category, progressing at a 5.53% CAGR and lifted by the 200,000-ton bio-ethylene venture and the 75,000-ton PLA expansion. Mainstream producers now trial chemical-recycling routes and circular naphtha streams to future-proof their asset bases and preserve relevance under new food-contact rules. The competitive gap narrows as conventional suppliers license bio-based processes, while newcomers differentiate through carbon-footprint declarations and compostability certifications.

The Thailand Plastics Report is Segmented by Type (Traditional Plastics, Engineering Plastics, and Bioplastics), Application (Packaging, Electrical and Electronics, Building and Construction, Automotive and Transportation, Furniture and Bedding, and Other Applications). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Covestro AG

- HMC Polymers Thailand

- Indorama Ventures Public Company Limited

- INEOS Styrolution Group GmbH

- IRPC Public Company Limited

- PTT Global Chemical Public Company Limited

- SCG Chemicals Co. Ltd

- Thai Plastic Industries Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand from Food and Beverage Packaging

- 4.2.2 Increasing Plastics Use in Building and Construction

- 4.2.3 Lightweighting Needs in Automotive and EV Components

- 4.2.4 Rapid E-Commerce Growth Boosting Protective Packaging

- 4.2.5 Bio-Based Polymer Joint Ventures (E.G., SCGC, Braskem)

- 4.3 Market Restraints

- 4.3.1 Stricter Single-Use-Plastic Bans and Taxes

- 4.3.2 Crude-Oil/Naphtha Price Volatility

- 4.3.3 PP and PE Oversupply and Low-Cost Imports from China

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Traditional Plastics

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Polypropylene (PP)

- 5.1.1.3 Polyvinyl Chloride (PVC)

- 5.1.1.4 Polystyrene (PS)

- 5.1.2 Engineering Plastics

- 5.1.2.1 Polyethylene Terephthalate (PET)

- 5.1.2.2 Polyamides (PA)

- 5.1.2.3 Polycarbonates (PC)

- 5.1.2.4 Styrene Copolymers (ABS and SAN)

- 5.1.2.5 Polybutylene Terephthalate (PBT)

- 5.1.2.6 Polymethyl Methacrylate (PMMA)

- 5.1.2.7 Other Engineering Plastics

- 5.1.3 Bioplastics

- 5.1.1 Traditional Plastics

- 5.2 By Application

- 5.2.1 Packaging

- 5.2.2 Electrical and Electronics

- 5.2.3 Building and Construction

- 5.2.4 Automotive and Transportation

- 5.2.5 Furniture and Bedding

- 5.2.6 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Covestro AG

- 6.4.2 HMC Polymers Thailand

- 6.4.3 Indorama Ventures Public Company Limited

- 6.4.4 INEOS Styrolution Group GmbH

- 6.4.5 IRPC Public Company Limited

- 6.4.6 PTT Global Chemical Public Company Limited

- 6.4.7 SCG Chemicals Co. Ltd

- 6.4.8 Thai Plastic Industries Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment