|

시장보고서

상품코드

1939596

아시아태평양의 연포장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

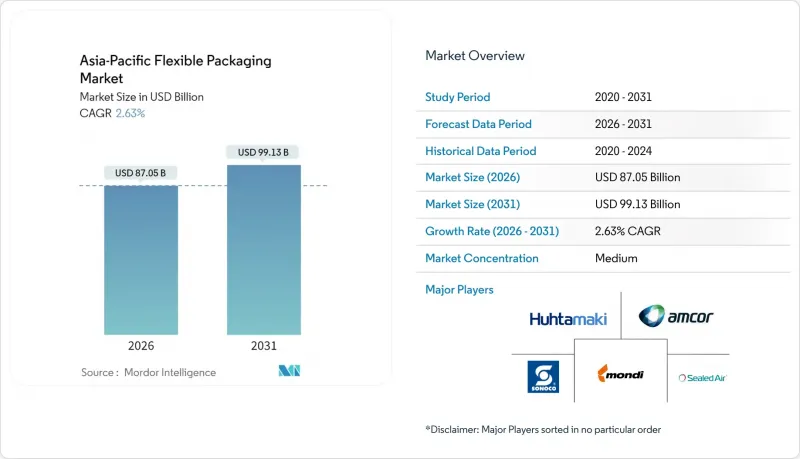

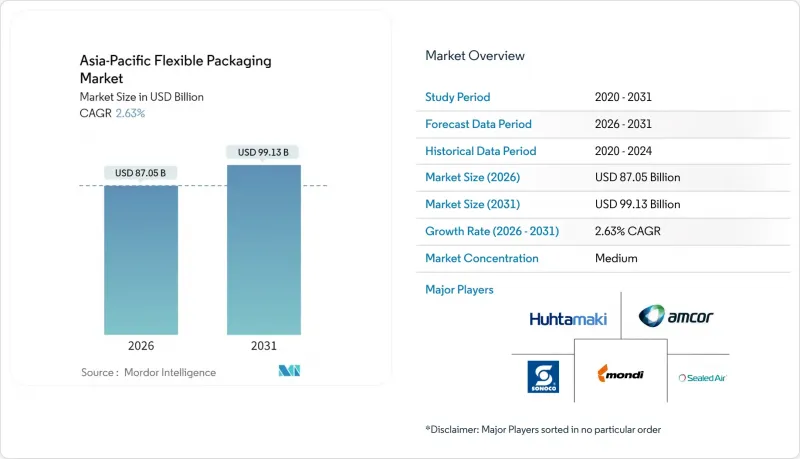

아시아태평양의 연포장 시장 규모는 2026년에 870억 5,000만 달러로 추정되고 있습니다.

이는 2025년 848억 2,000만 달러에서 성장한 수치이며, 2031년에는 991억 3,000만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년에는 CAGR 2.63%로 성장이 전망되고 있습니다.

일본, 호주, 중국 및 인도의 시범도시에서 규제 당국이 단일 재료 형식에 대한 의무를 강화함에 따라 자본은 현재 원료 톤수보다는 높은 장벽과 재활용이 가능한 설계에 집중되고 있습니다. 중국이 여전히 규모의 우위를 점하고 있지만, 인도의 4.89%의 연평균 복합 성장률(CAGR)은 가공업체들이 낮은 인건비와 스낵 및 퍼스널케어 제품에 대한 수요 증가를 추구하면서 지역적 축이 이동하고 있음을 보여줍니다. 2024년 기준 플라스틱이 68.12%의 점유율을 차지했으나, 바이오플라스틱과 퇴비화 가능한 소재가 성장세를 보이고 있으며, 브랜드 소유주들이 확대되는 생산자책임제도(EPR)에 대비하여 제품 포트폴리오의 미래성을 확보하려는 움직임으로 인해 연간 4.33%의 속도로 확대되고 있습니다. 성장하고 있습니다. 가방과 파우치는 여전히 비용 효율성이 높은 주력 제품으로 제품 유형별 매출의 47.63%를 차지했습니다. 반면, 봉지 및 스틱 팩은 3.67%의 성장 곡선을 보여 아시아 제2, 제3의 도시권에서 1회용 제품의 높은 비용 효율성을 반영하고 있습니다. 디지털 인쇄는 연간 4.76%의 성장률로 1만 미터 미만의 소량 생산도 채산성을 확보할 수 있게 되었고, 일본과 한국에서의 한정판 상품 출시를 지원함으로써 컨버터의 경제성을 재구축하고 있습니다.

아시아태평양의 연포장 시장 동향 및 인사이트

편의성 높은 포장에 대한 수요 증가

중국의 60%가 넘는 도시화율과 일본의 1인 가구 비율 증가로 인해 식사 준비 시간이 단축되고, 음식물 쓰레기를 최소화할 수 있는 용량 조절이 가능한 재밀봉 파우치에 대한 수요가 증가하고 있습니다. 동남아시아 소매업체들은 2025년까지 연포장 SKU 선반을 22% 확대하여 서보 구동 파우치 라인에 대한 컨버터 투자를 정당화할 것으로 예상하고 있습니다. 15분 이내 SKU 전환 능력은 설비 가동률을 향상시키고, 신속한 프로모션을 지원합니다. 소비자는 8-12%의 편의성 프리미엄을 지불하므로 수지 가격 변동에 따른 마진 압력을 완화하고 있습니다. 가처분 소득이 증가함에 따라 신흥 도시 지역에서는 스낵, 음료, 레토르트 식품에서 연포장이 우선적으로 선택되고 있습니다.

포장 상품의 E-Commerce 보급률 확대

인도의 온라인 식료품 점유율은 2020년 3.2%에서 2024년 7.8%로 상승하고, 베트남의 E-Commerce 물류 네트워크는 2024년 85%의 인구 커버리지를 달성할 것으로 예측됩니다. 라스트 마일의 현실에 대응하기 위해, 여러 번의 핸들링 포인트를 견딜 수 있고, 모바일 화면에서도 시인성이 높은 천공 방지 무광택 필름이 요구되고 있습니다. 컨버터 업체들은 현재 4 뉴턴 이상의 펑크 저항을 가진 다층 구조를 설계하고 있으며, 고비용의 반품을 피하기 위해 6-8%의 재료비 증가를 감수하고 있습니다. 디지털 인쇄를 통한 가변 데이터 코드는 브랜드 참여를 촉진하고, 포장과 로열티 프로그램을 연결합니다. 성능과 미적 감각을 겸비한 연포장재는 합리적인 E-Commerce 용기로서의 입지를 확고히 하고 있습니다.

플라스틱 포장의 환경 영향과 재활용에 대한 우려

베트남, 태국, 필리핀의 생산자책임재활용제도(EPR) 비용(공장출하가격의 0.8-2.1%)은 컨버터 업체들의 이익률을 40-60bp 낮추고 있습니다. 인도는 2026년까지 80%의 회수 목표를 세웠지만, 지방에서는 여전히 달성하기 어려운 상황으로 브랜드 소유자의 컴플라이언스 준수를 저해하고 있습니다. 조사에 따르면 일본과 한국 소비자의 64%는 재활용 가능한 대체품이 존재할 경우 다층 파우치를 피하고 있으며, 기존 포장 형태에 압력을 가하고 있는 것으로 나타났습니다. 퇴비화 가능한 필름은 여전히 25-30%의 프리미엄 가격이 요구되며, 습도가 높은 환경에서는 문제가 있습니다. 강력한 재활용 시스템이 구축될 때까지 브랜드 소유자는 지속가능성에 대한 약속과 비용 현실 사이의 긴장에 직면하게 될 것입니다.

부문 분석

2025년에는 플라스틱이 67.35%의 점유율로 지배적이며 폴리에틸렌은 고속 수직 충전 실링 라인의 주요 재료로 남아 있습니다. 이 중 바이오플라스틱과 퇴비화 가능한 소재는 CAGR 4.17%로 가장 빠른 성장세를 보이고 있는데, 이는 브랜드 소유주들이 일본과 호주의 향후 재활용 기준을 충족시키기 위해 PLA와 PHA 블렌드를 채택하고 있기 때문입니다. 아시아태평양의 바이오플라스틱 연포장 시장 규모는 세계 공급망 통합이 진행됨에 따라 확대될 것으로 예상되지만, 유럽으로부터의 운송 프리미엄이 착륙 비용 구조에 계속 영향을 미치고 있습니다. BOPP는 투명성과 인쇄적합성으로 스낵류 분야에서 우위를 유지하고 있으며, 알루미늄 포일은 0.5cc/m2/일 미만의 산소투과율이 필수인 의료 및 커피용도에서 틈새 시장을 유지하고 있습니다.

단일 소재화 움직임으로 폴리에틸렌 공급업체들은 PET와 나일론 층을 금속화 PE와 HDPE 코팅으로 대체하여 재활용성을 유지하면서 고배리어성 배합을 개발해야 하는 상황에 직면해 있습니다. 유플렉스의 Flex-PET(2024년 상용화)는 산소투과율 1.2cc/m2/day를 달성하여 스낵 필름 분야에서 폴리에틸렌의 우위를 강화하고 있습니다. 종이 기반 라미네이트는 18-22%의 비용 프리미엄을 수반하면서도 섬유가 풍부한 지속가능성 스토리를 제공하면서 국내 화장품 시장에서 지지를 확대하고 있습니다. 금속의 높은 차단성은 여전히 제약 분야에서 타의 추종을 불허하는 성능을 발휘하지만, 재활용시 에너지 소비에 대한 검증이 진행되고 있습니다. 전반적으로 아시아태평양의 연포장 시장에서는 복잡한 다층 구조보다 재활용 가능한 폴리올레핀을 우선시하는 수지 믹스의 재조정이 진행되고 있습니다.

가방 및 파우치는 식품, 반려동물 사료, 농업 분야에서의 범용성을 바탕으로 2025년 기준 46.95%의 점유율을 차지했습니다. 그러나 봉지 및 스틱 팩은 2031년까지 연평균 복합 성장률(CAGR) 3.55%로 확대될 것으로 예측됩니다. 다국적 기업이 샴푸, 컨디셔너, 스킨케어 크림과 같은 일회용품으로 가격에 민감한 소비자층을 공략하면서 아시아태평양내 유연포장 시장 점유율이 확대되고 있습니다. 유니레버와 프록터 앤 갬블은 2024년 인도에서월소득이 300달러 미만인 가구에 도달하기 위해 사셰 SKU를 14% 확대했습니다.

필름 및 랩 수요는 생산량과 연동되어 있으며, 스트레치 필름은 한국과 일본의 재사용 가능한 밴딩 테스트의 영향으로 역풍을 맞고 있습니다. 액체 세제 분야에서는 주둥이가 달린 스탠드업 파우치가 경질 병을 대체하고 있으며, 무게를 40% 절감하는 동시에 순환 경제에 대한 기여도를 높이고 있습니다. 아시아태평양의 연포장 시장에서는 E-Commerce 물류에 적합한 유연한 형태가 지속적으로 선호되고 있습니다. 경량화를 통해 라스트 마일 배송 비용을 절감할 수 있기 때문입니다. 뚜껑용 필름과 같은 틈새 유형은 고매출 베이커리 제품이나 농산물의 중첩 포장을 추구하고 있습니다. 제품 유형의 다양화는 수지 가격 변동에도 불구하고 컨버터 기업의 포트폴리오 회복력을 지원하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06Asia-Pacific flexible packaging market size in 2026 is estimated at USD 87.05 billion, growing from 2025 value of USD 84.82 billion with 2031 projections showing USD 99.13 billion, growing at 2.63% CAGR over 2026-2031.

Capital now flows toward high-barrier, recyclable designs rather than raw tonnage, as regulators tighten mandates on mono-material formats in Japan, Australia, and pilot cities in China and India. China still offers scale advantages, yet India's 4.89% CAGR signals a geographic pivot as converters seek lower labor costs and rising demand for snacks and personal care. Plastics held a 68.12% share in 2024, but bioplastics and compostables are gaining momentum, expanding at a rate of 4.33% annually as brand owners future-proof their portfolios against extended producer responsibility schemes. Bags and pouches remained the cost-efficient workhorse, accounting for 47.63% of product-type revenue. Meanwhile, sachets and stick packs gained ground, with a 3.67% growth curve that speaks to the affordability of single-serve products across tier-2 and tier-3 Asian cities. Digital printing, growing at a rate of 4.76% per year, is reshaping converter economics by enabling profitable runs of less than 10,000 linear meters and supporting limited-edition launches in Japan and South Korea.

Asia-Pacific Flexible Packaging Market Trends and Insights

Increased Demand for Convenient Packaging

Urbanization exceeding 60% in China and a rising share of single-person households in Japan are shrinking meal-prep time, prompting demand for portion-controlled, resealable pouches that minimize food waste. Southeast Asian retailers have raised shelf allocation for flexible SKUs by 22% in 2025, validating converters' investments in servo-driven pouch lines. The ability to switch SKUs within 15 minutes boosts asset utilization and supports rapid promotions. Consumers pay a convenience premium of 8-12%, cushioning margin pressure from resin fluctuations. As disposable incomes increase, flexible packaging becomes the preferred choice for snacks, beverages, and ready-to-eat meals in emerging urban clusters.

Growing E-Commerce Penetration for Packaged Goods

India's online grocery share rose from 3.2% in 2020 to 7.8% in 2024, and Vietnam's e-commerce logistics network reached 85% population coverage in 2024. Last-mile realities demand puncture-resistant, matte-finish films that can withstand multiple handling points and display well on mobile screens. Converters now engineer multi-layer structures with a puncture strength of> 4 newtons, accepting a 6-8% material premium to avoid costly returns. Variable-data codes printed digitally drive brand engagement, tying packaging to loyalty programs. The performance-plus-aesthetics combination cements flexible packs as the logical e-commerce container.

Concerns About Environmental Impact and Recycling of Plastic Packaging

Extended producer responsibility fees of 0.8-2.1% of the ex-factory price in Vietnam, Thailand, and the Philippines shave 40-60 basis points off converter margins. India's 80% collection target by 2026 remains elusive in rural districts, hindering brand-owner compliance. Surveys show 64% of consumers in Japan and South Korea avoid multilayer pouches when recyclable alternatives exist, pressuring legacy formats. Compostable films still command premiums of 25-30% and struggle in humid, high-moisture environments. Until robust recycling streams emerge, brand owners face a tension between their sustainability pledges and the realities of cost.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Mono-Material Flexible Packaging to Meet Recycling Mandates

- Surge in Cold Chain Expansion for Fresh Produce Exports in Southeast Asia

- Volatility in Raw Material Prices for Petrochemical Feedstocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics dominated 2025 with 67.35% share, and polyethylene remained the workhorse for high-speed vertical form-fill-seal lines. Within this base, bioplastics and compostables chart the fastest expansion at a 4.17% CAGR as brand owners adopt PLA and PHA blends to meet Japan and Australia's upcoming recyclability thresholds. The Asia-Pacific flexible packaging market size for bioplastics is on track to expand as global supply chains become more integrated, although freight premiums from Europe continue to impact landed cost structures. BOPP continues to excel in snacks and confectionery due to its clarity and printability, while aluminum foil maintains a niche in medical and coffee applications where sub-0.5 cc/m2/day oxygen levels are non-negotiable.

The drive to mono-material pushes polyethylene suppliers into higher-barrier formulations, replacing PET and nylon layers with metallized PE and HDPE coatings to maintain recyclability. Uflex's Flex-PET, commercialized in 2024, achieves 1.2 cc/m2/day oxygen transmission and reinforces polyethylene's claim on snack films. Paper-based laminates are gaining traction in South Korean cosmetics, trading at 18-22% cost premiums while offering a fiber-rich sustainability story. Metal's high barrier remains unmatched for pharmaceuticals yet faces scrutiny for recycling energy intensity. Net-net, the Asia-Pacific flexible packaging market faces a resin-mix recalibration favoring recyclable polyolefins over complex multilayers.

Bags and pouches held 46.95% share in 2025, powered by versatility across food, pet food, and agriculture. However, sachets and stick packs are projected to grow at a 3.55% CAGR through 2031. The Asia-Pacific flexible packaging market share for sachets is increasing as multinationals target price-sensitive consumers with single-use products such as shampoos, conditioners, and skincare creams. Unilever and Procter & Gamble expanded sachet SKUs by 14% in India in 2024 to reach households with monthly incomes of less than USD 300.

Films and wraps tie demand to manufacturing output, with stretch film facing headwinds from reusable bundling trials in Japan and South Korea. Stand-up pouches with spouts are replacing rigid bottles in liquid detergents, reducing weight by 40% and strengthening circular-economy credentials. The Asia-Pacific flexible packaging market continues to favor flexible formats that align with e-commerce logistics, as lighter parcels lower last-mile delivery costs. Niche types such as lidding films chase higher-margin bakery and produce overwraps. Collectively, product-type diversification supports converters' portfolio resilience amid fluctuating resin prices.

The Asia-Pacific Flexible Packaging Market Report is Segmented by Material (Plastics, Paper, Metal Foil, Bioplastics and Compostable Materials), Product Type (Bags and Pouches, Films and Wraps, and More), End-User Industry (Beverage, Healthcare and Pharmaceutical, Personal Care and Cosmetics, and More), Printing Technology (Flexography, Rotogravure, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor plc

- Mondi plc

- Sonoco Products Company

- Rengo Co., Ltd.

- Sealed Air Corporation

- Formosa Flexible Packaging Corp.

- Wapo Corporation Ltd.

- Chuan Peng Enterprise Co., Ltd.

- TCPL Packaging Ltd.

- Ester Industries Limited

- Huhtamaki Oyj

- Uflex Ltd.

- ProAmpac Holdings Inc.

- Constantia Flexibles Group GmbH

- Winpak Ltd.

- Cosmo Films Ltd.

- Glenroy Inc.

- Toppan Printing Co., Ltd.

- Fujimori Kogyo Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Demand for Convenient Packaging

- 4.2.2 Demand for Longer Shelf Life and Innovative Packaging

- 4.2.3 Growing E-Commerce Penetration for Packaged Goods

- 4.2.4 Adoption of Mono-Material Flexible Packaging to Meet Recycling Mandates

- 4.2.5 Surge in Cold Chain Expansion for Fresh Produce Exports in Southeast Asia

- 4.2.6 Brand Owner Shift Toward Digital Printing for Short-Run Personalization

- 4.3 Market Restraints

- 4.3.1 Concerns About Environmental Impact and Recycling of Plastic Packaging

- 4.3.2 Volatility in Raw Material Prices for Petrochemical Feedstocks

- 4.3.3 Regulatory Restrictions on Multilayer Structures in Japan and Australia

- 4.3.4 Limited Food-Grade Recyclate Availability for Flexible Formats

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Biaxially Oriented Polypropylene (BOPP)

- 5.1.1.3 Cast Polypropylene (CPP)

- 5.1.1.4 Other Plastics

- 5.1.2 Paper

- 5.1.3 Metal Foil

- 5.1.4 Bioplastics and Compostable Materials

- 5.1.1 Plastics

- 5.2 By Product Type

- 5.2.1 Bags and Pouches

- 5.2.2 Films and Wraps

- 5.2.3 Sachets and Stick Packs

- 5.2.4 Other Product Types

- 5.3 BY End-user Industry

- 5.3.1 Food

- 5.3.1.1 Baked Goods

- 5.3.1.2 Snacks

- 5.3.1.3 Meat, Poultry and Seafood

- 5.3.1.4 Confectionery

- 5.3.1.5 Pet Food

- 5.3.1.6 Other Food Products

- 5.3.2 Beverage

- 5.3.3 Healthcare and Pharmaceutical

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Agriculture and Horticulture

- 5.3.6 Other End-User Industries

- 5.3.1 Food

- 5.4 By Printing Technology

- 5.4.1 Flexography

- 5.4.2 Rotogravure

- 5.4.3 Digital Printing

- 5.4.4 Other Printing Technologies

- 5.5 By Country

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 Australia

- 5.5.5 South Korea

- 5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Mondi plc

- 6.4.3 Sonoco Products Company

- 6.4.4 Rengo Co., Ltd.

- 6.4.5 Sealed Air Corporation

- 6.4.6 Formosa Flexible Packaging Corp.

- 6.4.7 Wapo Corporation Ltd.

- 6.4.8 Chuan Peng Enterprise Co., Ltd.

- 6.4.9 TCPL Packaging Ltd.

- 6.4.10 Ester Industries Limited

- 6.4.11 Huhtamaki Oyj

- 6.4.12 Uflex Ltd.

- 6.4.13 ProAmpac Holdings Inc.

- 6.4.14 Constantia Flexibles Group GmbH

- 6.4.15 Winpak Ltd.

- 6.4.16 Cosmo Films Ltd.

- 6.4.17 Glenroy Inc.

- 6.4.18 Toppan Printing Co., Ltd.

- 6.4.19 Fujimori Kogyo Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment