|

시장보고서

상품코드

1939598

자동차용 타이어 공기압 모니터링 시스템(TPMS) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive TPMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

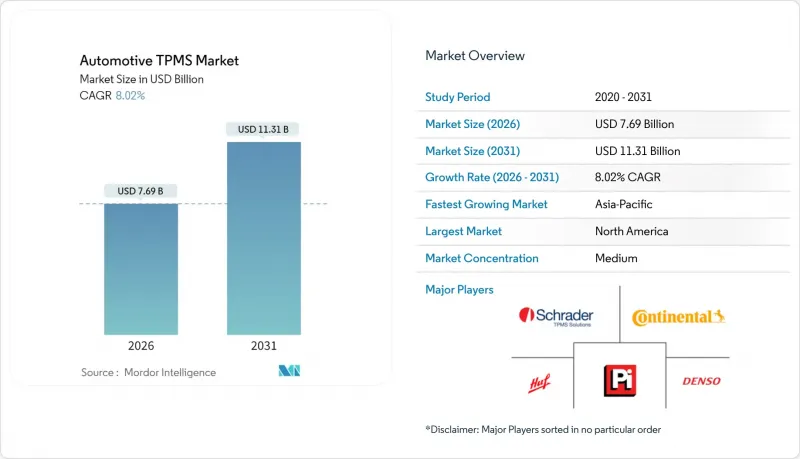

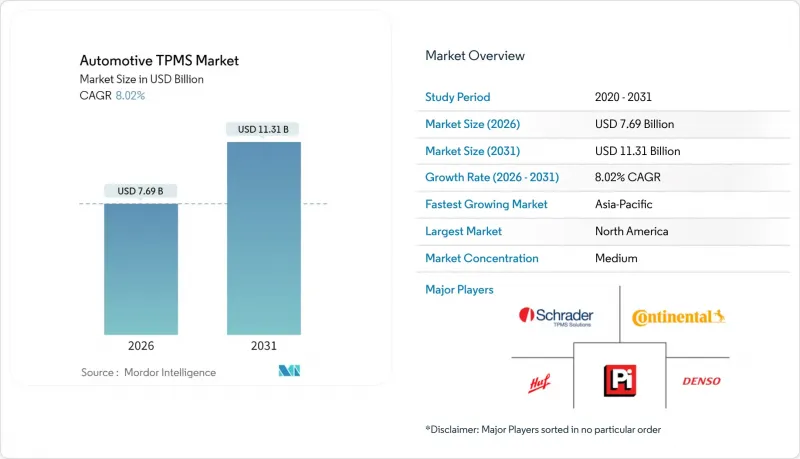

자동차용 타이어 공기압 모니터링 시스템(TPMS) 시장은 2025년 71억 2,000만 달러에서 2026년에는 76억 9,000만 달러로 성장하며, 2026-2031년에 CAGR 8.02%로 추이하며, 2031년까지 113억 1,000만 달러에 달할 것으로 예측되고 있습니다.

이러한 확대는 엄격하게 시행되는 안전 규정, 전기 파워트레인으로의 전환, 그리고 타이어 데이터를 첨단 운전 보조 시스템 및 커넥티드카 기반에 대한 깊은 통합에 기인합니다. 실시간 타이어 상태 분석은 기존의 공기압만 알려주는 경고 기능을 대체하고, 자동차 제조업체는 예측 유지보수를 무선 소프트웨어 업데이트 기능과 연계하여 무게에 민감한 전기자동차 모델에서 주행거리를 보호할 수 있게 됩니다. 센서, 게이트웨이, 클라우드 플랫폼의 통합으로 시스템 비용도 낮아져 이륜차 및 상용차 fleet에서 채택이 가속화되고 있습니다. 이와 함께 압전 에너지수확기술 기술과 2.4GHz 보안 연결의 혁신은 센서의 자가 발전 방식과 타이어-게이트웨이-클라우드 간 데이터 마이그레이션 방식을 재정의하여 자동차 타이어 공기압 모니터링 시스템(TPMS) 시장의 지속적인 성장을 위한 토대를 마련하고 있습니다. 기반을 구축하고 있습니다.

세계 자동차 타이어 공기압 모니터링 시스템(TPMS) 시장 동향 및 인사이트

신차 안전규제에서 TPMS 장착 의무화

규제 확대는 승용차를 넘어 2024년 7월부터 EU 일반안전규정에 따라 트럭, 버스, 트레일러까지 의무화가 확대되고 있습니다. 미국 FMVSS 138에 기반한 동등한 규정의 경우, 1만 파운드 미만의 모든 경량 차량이 대상에 포함되며, 차량 1대당 장착 비용은 48.44-69.89달러인 것으로 입증되었습니다. 한국의 조기 도입과 인도의 초안 프레임워크는 신흥 시장의 청사진이 될 것이며, 자동차 타이어 공기압 모니터링 시스템(TPMS) 시장이 중기적으로 규제 수요를 유지할 수 있도록 보장할 것입니다. 도입이 늦었던 상용차도 빠르게 업데이트가 진행되어 교체 수요가 확대되고, 센서 생산의 규모의 경제를 촉진하고 있습니다.

ADAS 및 커넥티드카 텔레매틱스 플랫폼과의 통합 발전

TPMS의 직접 데이터를 차량 안정성 제어, 자동 브레이크, 클라우드 분석과 통합하여 종합적인 안전 가치를 향상시킵니다. Melexis는 업계 최초로 블루투스를 지원하는 OEM용 TPMS를 출시하여 무선 소프트웨어 업데이트와 모바일 앱과의 원활한 연동을 실현했습니다. 전기자동차에서 TPMS 데이터는 최적화된 타이어 공기압이 배터리 항속거리를 향상시키고 회생제동 변동을 완화하므로 ADAS 시스템에서 필수적인 요소입니다. 2025년형 차량에 자동 긴급제동 의무화로 인해 타이어 상태는 의사결정 알고리즘의 중요한 입력 요소로 더 많이 포함될 것으로 예측됩니다.

엔트리 레벨 부문의 고비용 센서 및 캘리브레이션

가격에 민감한 A 부문 차량과 통근용 오토바이의 경우, 12-15달러의 추가 하드웨어 비용과 딜러의 보정 비용으로 인해 완전한 대응을 방해하고 있습니다. 콘티넨탈의 멀티 프로토콜 프로그래밍 가능 센서는 정비소의 SKU 수를 줄여주지만, 독립적인 수리업체는 보증 문제를 방지하기 위해 여전히 스캔 툴와 교육이 필요합니다. 배터리 수명의 제약도 밸브 제거 작업을 부담으로 여기는 저예산 소유주들의 채택 의욕을 더욱 떨어뜨리고 있습니다.

부문 분석

직접 아키텍처는 UN R141 정확도 기준을 충족하는 실시간 압력 및 온도 데이터 제공을 기반으로 2025년 자동차 타이어 공기압 모니터링 시스템(TPMS) 시장의 62.35%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 8.01%를 나타낼 것으로 예측됩니다. 간접 솔루션은 ABS 휠 속도 신호를 우회하여 차량 개조시 비용 절감 효과를 얻을 수 있지만, ADAS 센서 융합에 필요한 고화질 데이터 스트림을 제공하지 못합니다. 자동차 제조업체들이 중앙 집중식 도메인 컨트롤러로 전환하는 가운데, 직접형 TPMS 노드는 CAN-FD 및 차량용 이더넷 백본에 쉽게 통합되어 진단 작업과 무선 펌웨어 업데이트의 효율을 높입니다.

하드웨어와 병행하여 소프트웨어 분석 플랫폼은 원시 타이어 데이터를 실용적인 정비 간격, 예측 트레드 마모 경보, 동적 부하 분산 신호로 변환합니다. 차량 관리 포털은 TPMS 대시보드를 통합하여 유지보수 관리자가 도로에서 펑크가 발생하기 전에 미세한 공기 누출을 조기에 파악할 수 있도록 합니다. 이러한 예측적 가치로 인해 자동차 타이어 공기압 모니터링 시스템(TPMS) 시장은 부품 공급에서 지속적인 서비스 모델로 진화하고 있으며, 실리콘 비용의 하락에도 불구하고 프리미엄 가격 책정을 지원하고 있습니다.

2025년, MEMS 정전용량 소자는 프론트엔드 제조 기술의 성숙과 OEM의 광범위한 검증으로 자동차 타이어 공기압 모니터링 시스템(TPMS) 시장 점유율의 51.05%를 차지할 것으로 예측됩니다. 그러나 압전 에너지수확기술기는 시체 변형을 실용적인 전하로 변환하는 납-지르코늄 티탄산염 스트립을 통합하는 공급업체들의 움직임으로 인해 8.11%의 연평균 복합 성장률(CAGR) 전망으로 빠르게 보급되고 있습니다. 페루자 대학의 개념 증명 프로토타입은 2MPa의 반경 방향 하중에서 768V를 발생시켜 코인 셀 배터리 없이도 마이크로컨트롤러의 듀티 사이클을 충분히 충족시켰습니다. 배터리를 제거함으로써 수명 종료시 재활용이 용이하고, 유지보수 주기가 연장되며, 센서 접근이 어려운 허브리스 이륜차에도 TPMS 도입이 가능합니다.

한편, NXP FXTH87E와 같은 2축 가속도 센서는 자동 휠 위치 파악이 가능하여 타이어 회전 작업 시간을 5분 단축할 수 있습니다. 렌탈 차량군에서의 실지 도입을 지원하고 있습니다. 스트레인 게이지와 광학 센서는 0.1psi 미만의 해상도가 서킷 주행 가치를 높이는 틈새 고성능 차량에 대한 수요를 유지하고 있지만, 높은 부품 비용으로 인해 생산량이 제한적입니다.

지역별 분석

북미는 FMVSS(연방 자동차 안전 기준) 138을 기반으로 2025년에도 자동차 타이어 공기압 모니터링 시스템(TPMS) 시장 매출에 가장 큰 기여를 하는 지역으로 36.12%의 시장 점유율을 유지했습니다. 이는 소형차 탑재율과 탄탄한 애프터마켓 공급망에 힘입은 바 큽니다. 국가 차원의 사이버 보안에 대한 지속적인 강조로 인해 공급업체들은 향후 ISO 21434 감사에 대응할 수 있는 암호화된 BLE 및 UWB 스택으로 전환을 추진하고 있습니다. 캐나다에서는 미국 기준에 준하는 도입이 진행되고 있으며, 멕시코의 OEM 공장에서는 수출 시장을 위한 TPMS 사전 장착이 증가하고 있고, 텍사스 주와 누에보 레온 주 물류 거점에서공급망 집적화가 강화되고 있습니다. 컴플라이언스-안전-책임 평가(CSA) 점수 향상을 목표로 하는 상업용 운송 사업자들은 클래스 8 트랙터의 대량 개조 작업을 진행하고 있으며, 2025년까지 지역내 개조 보급률은 약 40%를 나타낼 것으로 예측됩니다.

유럽의 일반 안전 규정에 따라 2024년 중반부터 모든 신형 상용차에 TPMS 장착이 의무화됩니다. 다임러 트럭, MAN 등 독일 OEM 업체들은 이미 대형 플랫폼에 직접 센서를 탑재하고 있습니다. 동시에 영국의 애프터마켓 판매업체들은 밴용 개조 판매량이 전년 대비 50% 이상 성장했다고 보고하고 있습니다. 이 지역의 탈탄소화 목표에 따라 차량 사업자들은 TPMS와 저회전저항 타이어의 조합을 추진하고 있으며, TUV 노르트의 현장 테스트에서 입증된 2-3%의 연료 절감 효과를 얻고 있습니다. 유럽 전역에 걸친 UN R141의 조화로 형식 인증의 장벽이 더욱 낮아져 로테르담에서 바르샤바까지 운행하는 트레일러의 부품 번호가 국경을 넘어선 차량에서 표준화될 수 있게 되었습니다.

아시아태평양은 절대 출하량에서 1위를 유지하며 인도, 중국, 동남아시아 국가들의 이륜차 및 소형 트럭용 TPMS 규제 확대에 따라 2031년까지 연평균 복합 성장률(CAGR) 8.19%로 세계 평균을 상회하는 성장을 보일 것으로 예측됩니다. 중국의 전기자동차 급증으로 배터리 주행거리에 민감한 자동차 제조업체들은 A부문 해치백 차량에 TPMS 표준화를 요구하고 있으며, BYD는 연간 수백만 개의 센서를 현지 2등급 공급업체로부터 조달하고 있습니다. 국내에서는 2013년 초 의무화로 교체용 센서 애프터마켓이 성숙되어 있는 반면, 인도 자동차 산업표준 149 개정안에서는 2026년부터 M, N 카테고리 차량에 TPMS 의무화를 제안하고 있습니다. 베트남의 이륜차 업체들은 150cc급 1,500달러 미만의 모델에 직접식 센서를 표준으로 장착하고 있으며, 대량 생산이 가능한 아세안 생태계에서 빠른 비용절감이 가능하다는 것을 보여주고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The Automotive TPMS market is expected to grow from USD 7.12 billion in 2025 to USD 7.69 billion in 2026 and is forecast to reach USD 11.31 billion by 2031 at 8.02% CAGR over 2026-2031.

The expansion stems from tightly enforced safety rules, the shift toward electrified powertrains, and deeper integration of tire data into advanced driver-assistance and connected-car stacks. Real-time tire health analytics are replacing legacy pressure-only alerts, allowing automakers to align predictive maintenance with over-the-air software capabilities while protecting driving range in weight-sensitive electric models. Consolidation of sensor, gateway, and cloud platforms is also lowering system costs, accelerating adoption in two-wheelers and commercial fleets. In parallel, innovation in piezoelectric energy harvesting and secure 2.4 GHz connectivity is redefining how sensors power themselves and how data move between tires, gateways, and the cloud, positioning the Automotive TPMS market for resilient multi-segment growth.

Global Automotive TPMS Market Trends and Insights

Mandated TPMS Fitment In New-Vehicle Safety Regulations

Regulatory expansion is widening beyond passenger cars into trucks, buses, and trailers now mandated by the EU's General Safety Regulation from July 2024. Comparable rules in the United States under FMVSS 138 keep all light vehicles under 10,000 lb within scope and have demonstrated fitment costs of USD 48.44-69.89 per unit. Early adoption in South Korea and draft frameworks in India offer blueprints for emerging markets, ensuring the Automotive TPMS market sustains regulatory pull into the medium term. Commercial fleets that previously lagged adoption are rapidly upgrading, swelling replacement volumes and driving economies of scale in sensor production.

Rising Integration With ADAS & Connected-Car Telematics Platforms

Merging direct TPMS data with vehicle stability, automated braking, and cloud analytics amplifies overall safety value. Melexis launched the first Bluetooth-enabled OEM TPMS, unlocking over-the-air software support and frictionless pairing to mobile apps. For electric vehicles, optimized tire pressure elevates battery range and mitigates regenerative-braking variability, making TPMS data indispensable within the ADAS stack. Upcoming mandates for automatic emergency braking in 2025 vehicles further embed tire status as a critical input to decision algorithms.

High Sensor & Calibration Cost In Entry-Level Segments

In price-sensitive A-segment cars and commuter bikes, the extra USD 12-15 hardware cost plus dealer calibration fees deter full compliance. Although Continental's multi-protocol programmable sensor trims SKU counts for garages, independent repairers still require scan tools and training to avoid warranty misfires. Battery life constraints further discourage low-budget owners who view valve dismounting labor as prohibitive.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation Of Low-Cost Mems Sensors For Two-Wheelers

- Shift Toward Smart-Tire Health-Analytics Ecosystems

- Wireless TPMS Cybersecurity Vulnerabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct architectures held a 62.35% Automotive TPMS market share in 2025 and are projected to log an 8.01% CAGR through 2031, underpinned by real-time pressure and temperature delivery that meets UN R141 accuracy thresholds. Indirect solutions remain a cost hedge in fleet retrofits by piggybacking ABS wheel-speed signals but cannot furnish the high-granularity data streams required for ADAS sensor fusion. As automakers transition to centralized domain controllers, direct TPMS nodes slot neatly onto CAN-FD or Automotive Ethernet backbones, streamlining diagnostics and over-the-air firmware updates.

Parallel to hardware, software analytics platforms convert raw tire data into actionable maintenance intervals, predictive tread-wear alerts, and dynamic load balancing cues. Fleet management portals integrate TPMS dashboards, giving maintenance managers early insight into slow leaks before roadside blowouts. Such predictive value elevates the Automotive TPMS market from component supply to recurring service models, supporting premium pricing even as silicon costs decline.

MEMS capacitive elements captured 51.05% of Automotive TPMS market share in 2025 due to mature front-end fabrication and wide OEM validation. However, piezoelectric harvesters are rapidly gaining traction with an 8.11% CAGR outlook as suppliers integrate lead-zirconate-titanate strips that convert carcass deflection into usable charge. Proof-of-concept prototypes from the University of Perugia generated 768 V under 2 MPa radial load, adequate for microcontroller duty cycles without coin-cell batteries. Eliminating batteries eases end-of-life recycling, lengthens maintenance intervals, and opens TPMS deployment on hub-less two-wheelers where sensor access is tight.

Meanwhile, dual-axis accelerometers such as NXP FXTH87E enable automatic wheel localization, cutting 5 minutes from tire-rotation service times and underpinning field adoption across rental fleets. Strain-gauge and optical sensors continue filling niche performance cars where sub-0.1 psi resolution adds track-day value, but their higher BOM keeps volume modest.

The Automotive TPMS Market Report is Segmented by System Type (Direct, Indirect, and Hybrid), Sensor Technology (MEMS Capacitive, Strain-Gauge, and More), Fitting Method (Valve-Stem, Band/Rim-Mounted, and Embedded-Tire Module), Frequency Band (315 MHz and More), Vehicle Type (Passenger Cars and More), Sales Channel (OEM Factory-Fit and Aftermarket Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America, anchored by FMVSS (Federal Motor Vehicle Safety Standards) 138, remained the largest regional contributor to Automotive TPMS market revenue in 2025 with 36.12% market share, supported by light-vehicle installation rates and robust aftermarket supply chains. Ongoing emphasis on cybersecurity at the state level is steering suppliers toward encrypted BLE and UWB stacks that can satisfy upcoming ISO 21434 audits. Canadian adoption tracks U.S. standards, while Mexican OEM plants increasingly pre-install TPMS to serve export markets, reinforcing supply-chain clustering at Texas and Nuevo Leon logistics hubs. Commercial carriers pursuing Compliance, Safety, Accountability score improvements are bulk-retrofitting Class 8 tractors, lifting the regional retrofit penetration to almost two-fifths in 2025.

The General Safety Regulation in Europe mandated TPMS on all new commercial vehicles from mid-2024. German OEMs such as Daimler Truck and MAN have already embedded direct sensors on heavy-duty platforms. At the same time, British aftermarket distributors report more than half-year-on-year growth in van retrofit sales. The region's decarbonization targets encourage fleets to pair TPMS with low-rolling-resistance tires, capturing 2-3% fuel savings validated by TUV Nord field testing. Pan-European UN R141 harmonization further lowers homologation friction, allowing cross-border fleets to standardize part numbers for trailers operating from Rotterdam to Warsaw.

Asia-Pacific leads absolute shipment volume and is forecast to outpace global averages to 2031 with 8.19% CAGR as India, China, and Southeast Asian nations legislate broader two-wheeler and light-truck coverage. China's electric-vehicle surge is compelling battery-range-sensitive automakers to standardize TPMS across A-segment hatchbacks, with BYD sourcing millions of sensor annually from local tier-twos. South Korea's early 2013 mandate offers a mature aftermarket for replacement sensors, while India's Automotive Industry Standard 149 revision proposes mandatory TPMS on M and N categories from 2026. Motorcycle OEMs in Vietnam already bundle direct sensors on 150 cc models priced under USD 1,500, underscoring the rapid cost deflation achievable in high-volume ASEAN ecosystems.

- Continental AG

- Sensata Technologies / Schrader

- Pacific Industrial Co. Ltd.

- Huf Hulsbeck & Furst

- DENSO Corporation

- ZF Friedrichshafen AG (incl. TRW)

- Valeo SA

- ALLIGATOR Ventilfabrik GmbH

- Alps Alpine Co. Ltd.

- Delphi / Aptiv plc

- Continental - Vitesco JV

- PressurePro Enterprises Inc.

- Steelmate Co. Ltd.

- Orange Electronic Co. Ltd.

- Bartec USA LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandated TPMS Fitment In New-Vehicle Safety Regulations

- 4.2.2 Rising Integration With ADAS & Connected-Car Telematics Platforms

- 4.2.3 Proliferation Of Low-Cost Mems Sensors For Two-Wheelers

- 4.2.4 Shift Toward Smart-Tire Health-Analytics Ecosystems

- 4.2.5 Electrification Increasing Weight-Sensitive Range Anxiety

- 4.2.6 Insurance-Telematics Incentives For Tire-Pressure Compliance

- 4.3 Market Restraints

- 4.3.1 High Sensor & Calibration Cost In Entry-Level Segments

- 4.3.2 Aftermarket Installation Complexity & Maintenance Issues

- 4.3.3 Wireless TPMS Cybersecurity Vulnerabilities

- 4.3.4 Advent Of Airless & Run-Flat Tire Technologies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By System Type

- 5.1.1 Direct

- 5.1.2 Indirect

- 5.1.3 Hybrid

- 5.2 By Sensor Technology

- 5.2.1 MEMS Capacitive

- 5.2.2 Strain-Gauge

- 5.2.3 Piezoelectric

- 5.2.4 Others (Optical, SAW, etc.)

- 5.3 By Fitting Method

- 5.3.1 Valve-Stem (Snap-In & Clamp-In)

- 5.3.2 Band / Rim-Mounted

- 5.3.3 Embedded-Tire Module

- 5.4 By Frequency Band

- 5.4.1 315 MHz

- 5.4.2 433 MHz

- 5.4.3 More than or equal to 2.4 GHz & UWB

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Commercial Vehicle

- 5.5.3 Two-Wheelers

- 5.6 By Sales Channel

- 5.6.1 OEM Factory-Fit

- 5.6.2 Aftermarket Retrofit

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Australia

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 Egypt

- 5.7.5.5 South Africa

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Sensata Technologies / Schrader

- 6.4.3 Pacific Industrial Co. Ltd.

- 6.4.4 Huf Hulsbeck & Furst

- 6.4.5 DENSO Corporation

- 6.4.6 ZF Friedrichshafen AG (incl. TRW)

- 6.4.7 Valeo SA

- 6.4.8 ALLIGATOR Ventilfabrik GmbH

- 6.4.9 Alps Alpine Co. Ltd.

- 6.4.10 Delphi / Aptiv plc

- 6.4.11 Continental - Vitesco JV

- 6.4.12 PressurePro Enterprises Inc.

- 6.4.13 Steelmate Co. Ltd.

- 6.4.14 Orange Electronic Co. Ltd.

- 6.4.15 Bartec USA LLC

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment