|

시장보고서

상품코드

1939607

화장품 포장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cosmetic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

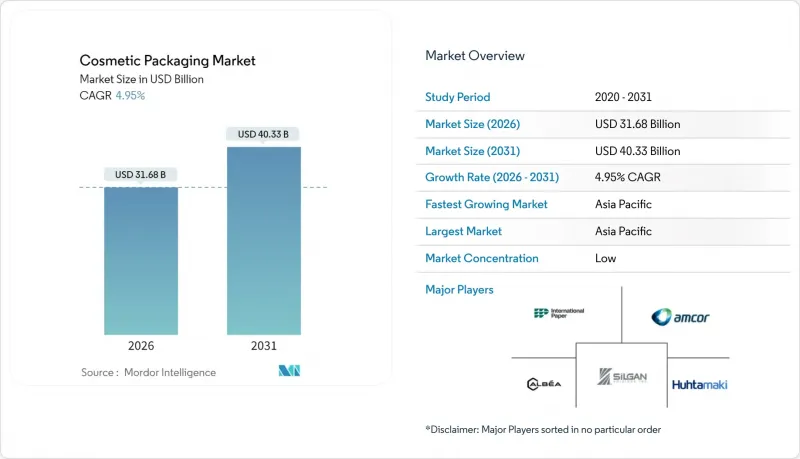

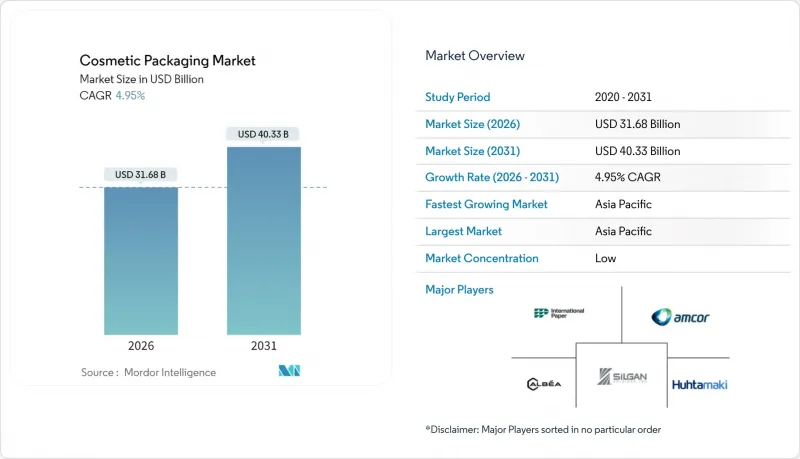

화장품 포장 시장은 2025년에 301억 9,000만 달러로 평가되며, 2026년 316억 8,000만 달러에서 2031년까지 403억 3,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 4.95%로 예상됩니다.

이는 2025년 2월부터 시행되는 유럽연합의 포장 및 포장 폐기물 규제에 대한 브랜드 대응을 반영한 것입니다. 이 규정은 재활용 가능성과 확장된 생산자 책임의 준수를 의무화하고 있습니다. 각 브랜드들은 지정학적 긴장과 중국 및 유럽의 생산 감축으로 인해 치솟는 폴리에틸렌 테레프탈레이트(PET) 비용에 대응하기 위해 재활용 소재 사용 촉진과 경량화 설계를 가속화하고 있습니다. 아시아태평양은 정교한 소비 습관과 강력한 E-Commerce 물류에 힘입어 성장의 견인차 역할을 하고 있습니다. 중국에서의 페이셜 시트 마스크의 성공과 한국, 일본에서의 프리미엄화는 이 지역의 영향력을 상징합니다. 소재 선택은 양극화 현상이 지속되고 있으며, 플라스틱은 비용 우위를 유지하는 반면, 유리는 고급품, 리필 가능 제품, 순환 경제에 대한 호소력으로 진전을 보이고 있습니다. 한편, 암콜이 베리월드와 84억 3,000만 달러 규모의 합병으로 대표되는 기업 통합은 규모와 연구개발을 통합하고 지속가능한 포장의 발전을 가속화할 것입니다.

세계 화장품 패키지 시장 동향 및 인사이트

프리미엄 매스티지 뷰티 제품 소비 확대

고급스러움의 요소가 주류 채널로 이동하고, 촉감이 좋은 마감, 두꺼운 유리, 장식적인 캡이 브랜드 스토리를 형성하고 있습니다. 로레알의 '2025 세계 리필의 날' 프로모션을 통해 프리미엄 포지셔닝을 유지하면서 리필 가능한 옵션이 5년 동안 17배 증가했습니다. 에스티로더는 이미 전체 포트폴리오의 71%를 지속가능한 형태로 공급하고 있으며, 환경 보호와 고급스러운 이미지가 공존할 수 있음을 입증하고 있습니다. 이에 따라 공급업체들은 고급 포뮬러에 대응하는 고투명 유리와 단일 소재 펌프를 우선적으로 채택하고 있습니다. 이 기회는 관련 제품의 판매 촉진과 고매출을 가능하게 하는 리필 키트에도 확대되고 있습니다. 럭셔리 브랜드가 환경적 성능을 중시하는 태도는 화장품 패키지 시장의 모든 계층에서 기준을 높이고 있습니다.

E-Commerce에 적합한 경량 포맷으로 전환

온라인 판매에서 내충격성과 부피 중량 감소는 결정적인 요소입니다. 플렉서블 파우치는 평평한 상태로 배송할 수 있으며, 완충재 절감과 운송비 절감을 실현할 수 있으며, CAGR 7.67%로 성장하고 있습니다. KISS 코스메틱스는 48만 평방피트 규모의 시설을 자동화하고 지능형 카트 피킹과 A프레임 디스펜싱을 도입했습니다. 균일하고 가벼운 패키지가 물류 비용 절감에 유리하다는 것을 입증했습니다. 포장 로봇에 대한 투자 규모는 2032년까지 75억 달러에 달할 것으로 예상되며, 다품종 SKU의 유통을 원활하게 하는 자동화의 역할이 강조되고 있습니다. 소매점 진열대가 아닌 배송 네트워크에 최적화된 브랜드는 사이클 타임을 단축하고 배출량을 줄여 물류 변동에 대한 세계 화장품 포장 시장의 내성을 강화하고 있습니다.

세계 재생수지 가격 변동성 확대

유럽의 PET 가격은 2024년 반덤핑 규제로 인한 공급 부족으로 톤당 1,130-1,170유로에서 형성되었으며, 가공업체들은 현물시장에서 입찰 경쟁을 벌여야 했습니다. 2025년 초에는 원료비 상승에 따라 폴리에틸렌과 폴리프로필렌도 각각 파운드당 5센트, 4센트의 가격 상승을 기록했습니다. 50% 재활용 소재 사용을 약속하는 브랜드는 마진에 대한 충격을 흡수하거나 자체 세척 공장 등 수직계열화를 통해 헤지책을 마련하고 있습니다. 고품질 식품용 PCR은 프리미엄 가격이 책정되므로 공급 리스크가 디자인의 자유도를 제한하고, 화장품 패키지 시장에서 버진 수지로부터의 대체를 지연시킬 수 있습니다.

부문 분석

플라스틱은 비용 효율성, 투명성, 라인 속도와의 호환성으로 인해 2025년 화장품 포장 시장에서 64.02%의 점유율을 차지할 것으로 예측됩니다. 폴리에틸렌 테레프탈레이트(PET)는 퍼스널케어 병에서 주도적인 위치를 차지하고, 폴리프로필렌(PP)은 펌프 스템과 캡을, 저밀도 폴리에틸렌(LDPE)은 플렉서블 튜브를 형성하고 있습니다. 그러나 고급 브랜드가 무게감, 스크래치 방지, 무한한 재생성을 추구함에 따라 유리는 2031년까지 연평균 복합 성장률(CAGR) 8.32%로 급성장하고 있습니다. 이러한 프리미엄 지향의 변화로 인해 유리 화장품 패키지 시장 규모는 총 패키지 수가 플라스틱보다 적지만, 두 자릿수의 매출 점유율을 차지할 것으로 예측됩니다. 에스티로더와 전략적 매트리얼즈의 협업 등 유리 재활용을 위한 노력은 컬릿 품질과 용해로의 생산성을 향상시켜 환경적 비판을 완화하고 있습니다. 금속화 알루미늄과 스틸은 장벽 성능과 차가운 질감이 매장에서 임팩트를 주는 향수 및 선물용 제품에서 여전히 틈새 시장으로 자리 잡고 있습니다. 섬유 기반 보드는 플라스틱 세금의 위험을 증가시키지 않고 E-Commerce의 완충재 수요를 충족시키기 위해 운송 용기 및 선물 세트에 점점 더 많이 사용되고 있습니다.

2세대 소재는 카테고리 간의 경계를 모호하게 만듭니다. 과거 튜브에 사용되었던 다층 PET-알루미늄 라미네이트는 재활용 공정과의 호환성을 유지하면서 단일 소재인 EVOH 배리어 PET로 전환되고 있습니다. 폴리락산 등 바이오 유래 수지는 한정판 라벨로 시험 도입이 진행되고 있지만, 내열성 및 충전 라인에서의 마찰 문제로 인해 규모 확대가 제한되고 있습니다. 이러한 과제를 해결하는 공급업체가 선점 계약을 체결하고 있으며, 이는 지속가능성 성과가 화장품 패키지 시장 전체에서 공급업체 선정의 기준이 되고 있는 현실을 반영하고 있습니다. 한편, 리필 스테이션과 연계한 리턴블 유리 프로그램은 프리미엄급 신뢰성과 환경 친화적 성향을 결합하여 유리를 주류 제품군에 더욱 깊숙이 침투시키는 좋은 예입니다.

병과 항아리는 높은 충전 속도와 소비자 친화성에 힘입어 2025년 매출의 44.12%를 차지할 것으로 예측됩니다. 입이 넓은 병은 페이스 크림의 주력 용기이며, 입이 좁은 PET병은 샴푸와 미셀워터로 주류를 이루고 있습니다. 하지만, 1회용 중량 감소와 배송시 파손 방지를 위해 파우치 및 스탠드업 파우치는 7.41%의 높은 CAGR로 성장세를 이어가고 있습니다. 적정 크기 기술을 통해 브랜드는 한 달에 한 병에서 한 봉투당 5봉지로 전환할 수 있으며, 운송시 배출 강도를 줄일 수 있습니다. 튜브와 스틱 용기는 이동 중에도 사용할 수 있는 자외선 차단제, 고체형 세럼, 컬러밤 등의 동향에 대응하고, 여행용 사이즈 규제와 완벽한 누출 방지에 대한 기대에 부응합니다. 접이식 카톤은 여전히 고급품 패키지로 선호되고 있으며, 유리 플라콘과 부스터 바이알을 담는 동시에 소프트 터치 가공과 호일 스탬핑을 통해 브랜드 스토리를 전달할 가능성이 있습니다.

운송용 박스도 진화를 거듭하고 있습니다. 골판지 제조업체는 알고리즘에 의한 박스 제조로 공극 충진을 줄이고, Packsize의 기계가 실시간 주문 치수에 맞추어 판지를 절단합니다. 소비자의 개봉 경험이 옴니채널의 차별화 요인이 되고, QR코드 삽입물이 디지털 로열티 보상을 활성화하는 구조가 확산되고 있습니다. 연포장의 배리어 코팅은 산화규소나 산화알루미늄으로 고도화되어 향기 유지성을 확보하면서 산소 투과성을 감소시켰습니다. 재활용성을 훼손하지 않으면서 유연한 소재 시장 규모를 확대하는 동시에 경질 용기에만 의존하지 않는 '매스 프리미엄' 미학을 재정의하고 있습니다.

화장품 패키지 시장은 재료 유형(플라스틱, 유리, 금속, 종이/판지), 제품 유형(병/병, 튜브/스틱, 튜브/스틱, 접이식 상자, 운송용 골판지 상자 등), 디스펜싱 메커니즘(펌프식, 스포이드/피펫, 스프레이/미스트 등), 화장품 유형(헤어케어, 색조화장품, 스킨케어 등), 지역별로 분류됩니다. 헤어케어, 색조화장품, 스킨케어 등), 지역별로 분류됩니다. 시장 규모와 예측은 금액(USD)으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 화장품 패키지 시장 매출의 42.55%를 차지할 것으로 예상되며, 가처분 소득 증가, K-뷰티의 높은 보급률, 모바일 커머스의 높은 보급률에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 7.18%를 나타낼 것으로 예측됩니다. 중국내 시트 마스크의 압도적인 보급은 일회용이지만 세련된 포장 형태에 대한 현지 수요를 보여주며, 이 지역은 미니멀하면서도 기능적인 파우치의 온상이 되고 있습니다. 일본과 한국은 에어리스 쿠션 컴팩트, 슬림 트위스트 밤 등 디자인 요소를 전 세계에 수출하고 있으며, 지역 컨버터 기업에게 선점효과를 가져다주고 있습니다.

북미 시장은 프리미엄 스킨케어 제품의 보급과 급속한 E-Commerce의 확대로 견고한 가치를 유지하고 있습니다. 뷰티 전문점에서는 리필 스테이션의 시범 도입이 진행되어 유리 카트리지 공급업체에 새로운 서비스 계약을 가져오고 있습니다. 자동화 대응의 진전으로 로봇 대응 골판지 포장과 라이너리스 라벨의 보급이 가속화. 주정부 차원의 플라스틱 감축 법안은 경량 단일 소재로의 전환을 촉구하고, 재생 PET 및 섬유 대체 소재에 대한 투자를 촉진하고 있습니다. 이러한 움직임은 성숙한 카테고리 침투율에도 불구하고 화장품 포장 시장은 여전히 활기를 띠고 있습니다.

유럽은 전 세계에 영향을 미치는 규제 프레임워크를 형성하고 있습니다. PPWR(플라스틱 포장 규제)의 시행과 프랑스의 친환경 기여금 인상은 명확한 포장재 재활용 기준을 부과하고, 분해 설계에 대한 투자를 가속화하고 있습니다. 프랑스와 이탈리아의 고급 향수 산업 클러스터는 스크래치 방지를 위한 첨단 핫엔드 코팅을 포함한 유리 소재의 혁신을 주도하고 있습니다. 한편, 중동부 유럽에서는 현지 브랜드와 수출 생산을 모두 지원하기 위해 병 성형 능력의 확장이 진행되고 있습니다. 전 세계 각 지역이 하나로 통합되어 재료 전략과 기술 이전 속도에 영향을 미치고 화장품 패키지 시장 수요 동인을 서로 연결하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The cosmetic packaging market was valued at USD 30.19 billion in 2025 and estimated to grow from USD 31.68 billion in 2026 to reach USD 40.33 billion by 2031, at a CAGR of 4.95% during the forecast period (2026-2031).

The advance mirrors brand responses to the European Union's Packaging and Packaging Waste Regulation, effective February 2025, which obliges recyclability and extended producer responsibility compliance. Brands counter rising polyethylene terephthalate costs driven by geopolitical tension and production cuts in China and Europe by accelerating recycled-content usage and lightweight designs. Asia-Pacific remains the growth engine, propelled by sophisticated consumer routines and strong e-commerce logistics; Chinese facial sheet-mask success and premiumization across South Korea and Japan typify the region's influence. Material choice continues to bifurcate: plastics retain cost leadership while glass advances on luxury, refillable, and circular-economy appeal. Meanwhile, corporate consolidation highlighted by Amcor's USD 8.43 billion merger with Berry Global bundles scale and R&D to quicken sustainable-packaging rollouts.

Global Cosmetic Packaging Market Trends and Insights

Growing Consumption of Premium and Masstige Beauty Products

Luxury cues have migrated into mainstream channels as tactile finishes, heavy-wall glass, and ornate closures shape brand storytelling. L'Oreal's 2025 World Refill Day push lifted refillable options seventeen-fold in five years without diluting premium positioning. Estee Lauder already supplies 71% of its portfolio in sustainable formats, confirming that environmental progress and upscale image can co-exist. Suppliers thus prioritise high-clarity glass and mono-material pumps that tolerate prestige formulations. The opportunity extends to refill kits that guarantee adjacency sales and invite higher margins. Luxury's embrace of environmental performance raises the bar for all tiers of the cosmetic packaging market.

Shift Toward E-commerce-Friendly Lightweight Formats

Online sales make damage resistance and dimensional-weight savings decisive. Flexible pouches grow at 7.67% CAGR because they ship flat, cut void fill, and slash freight spend. KISS Cosmetics automated its 480,000 ft2 facility with intelligent cart-picking and A-Frame dispensing, demonstrating fulfilment economics that favour uniform, lighter packs. Packaging-robot investments are projected to reach USD 7.5 billion by 2032, underlining automation's role in smoothing multi-SKU flows. Brands that optimise for courier networks rather than retail shelves secure faster cycle times and lower emissions, fortifying the global cosmetic packaging market against logistics volatility.

Escalating Global Recycled-Resin Price Volatility

European PET hovered at EUR 1,130-1,170 per t in 2024 as anti-dumping rules tightened supply, forcing converters into spot-market bidding wars. Polyethylene and polypropylene followed with five-cent and four-cent per-lb upticks in early 2025 as feedstock costs rose. Brands with 50%-recycled-content pledges thus absorb margin shocks or hedge via vertical integration, such as on-site washing plants. Because high-quality food-grade PCR commands premiums, availability risk constrains design freedom and may slow substitutions away from virgin resin in the cosmetic packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Refillable/Reusable Delivery Systems in Prestige Channels

- Rapid Adoption of Robot-Ready Secondary Packs in 3-PL Fulfilment

- Regulatory Caps on Single-Use Plastic

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics held a 64.02% cosmetic packaging market share in 2025 thanks to cost efficiency, clarity, and line-speed compatibility. Polyethylene terephthalate leads for personal-care bottles, polypropylene secures pump stems and closures, while low-density polyethylene shapes flexible tubes. Yet glass races ahead at 8.32% CAGR to 2031 because prestige brands crave heft, scratch resistance, and infinite recyclability. The premium shift lifts the cosmetic packaging market size for glass to meaningful double-digit revenue slices even as total pack count stays lower than plastic. Glass-recycling initiatives such as Estee Lauder's work with Strategic Materials Inc.improve cullet quality and furnace yields, soothing environmental criticisms. Metallised aluminium and steel remain niche for fragrances and gifting editions where barrier performance and tactile coolness drive shelf impact. Fibre-based board escalates in transit shippers and gift sets, answering e-commerce cushioning needs without raising plastic tax exposure.

Second-generation materials blur lines between categories. Multi-layer PET-aluminium laminates once seen in tubes migrate toward mono-material EVOH-barrier PET that retains recycling stream compatibility. Bio-sourced resins such as polylactic acid win trial runs for limited-edition labels but still battle heat resistance and filling-line friction, limiting scale. Suppliers addressing these hurdles gain early-mover contracts, reflecting how sustainability performance now shapes vendor selection criteria across the cosmetic packaging market. Meanwhile, returnable glass programs aligned with refill stations exemplify how premium credentials fuse with low-impact ambitions to pull glass farther into mainstream assortments.

Bottles and jars delivered 44.12% revenue in 2025, supported by high filling speeds and shopper familiarity. Wide-mouth jars continue to anchor face creams, while narrow-neck PET bottles dominate shampoos and micellar waters. However, sachets and stand-up pouches compound at a brisk 7.41% CAGR, cutting grams per dose and resisting breakage during courier drops. Right-size technology lets brands switch from one bottle-per-month to five flat sachets per envelope, lowering freight-emissions intensity. Tubes and sticks address on-the-go sunscreen, solid serum, and colour-balm trends, meshing with travel-size regulation and zero-leak expectations. Folding cartons remain favoured in luxury presentations, housing glass flacons or booster vials while conveying brand narratives through soft-touch varnish and foil embossing.

Transit boxes evolve too. Corrugated suppliers deploy algorithmic box-making to trim void fill, supported by Packsize machines that cut board in line with real-time order dimensions. Consumer unboxing gains differentiate omnichannel experiences, prompting QR-printed inserts that trigger digital loyalty rewards. Flexible-pack barrier coatings upgrade to silicon oxide or aluminium oxide, securing fragrance retention and reducing oxygen transmission without disqualifying recyclability. Such advances swell the cosmetic packaging market size credited to flexible formats and re-define mass-premium aesthetics away from solely rigid containers.

Cosmetic Packaging Market is Segmented by Material Type (Plastic, Glass, Metal, Paper and Paperboard), Product Type (Bottles and Jars, Tubes and Sticks, Folding Cartons, Corrugated Transit Boxes, and More), Dispensing Mechanism (Pump-Based, Dropper / Pipette, Spray / Mist, and More), Cosmetic Type (Hair Care, Color Cosmetics, Skin Care, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific owned 42.55% of cosmetic packaging market revenue in 2025 and will grow at a 7.18% CAGR to 2031, lifted by rising disposable income, advanced K-beauty regimens, and high mobile-commerce penetration. Sheet-mask dominance in China illustrates local appetite for single-use but sophisticated pack forms, making the region a hotbed for minimalist yet functional pouches. Japan and South Korea export design cues globally, such as airless cushion compacts and slim twist balms, giving regional converters first-mover advantages.

North America holds firm value through premium skincare adoption and rapid e-commerce. Refill station pilots appear in beauty specialty retailers, rewarding glass cartridge suppliers with new service contracts. Automation readiness drives widespread acceptance of robot-friendly corrugate and linerless labels. State-level plastic-reduction bills add urgency to lightweight mono-material shifts, redirecting investment towards recycled-content PET and fibre substitution. These moves keep the cosmetic packaging market buoyant despite mature category penetration.

Europe shapes regulatory frameworks that ripple worldwide. Enforcement of the PPWR and escalating eco-contribution fees in France imposes clear packaging recyclability thresholds, accelerating investment in design for disassembly. Luxury fragrance clusters in France and Italy champion glass innovation, including advanced hot-end coating for scratch reduction. Meanwhile, Central and Eastern Europe attract bottle moulding capacity expansions to serve both local brands and export production. Collectively, global regions influence material strategies and technology transfer rates, interlocking demand drivers for the cosmetic packaging market.

- Albea SA

- AptarGroup Inc.

- Amcor Group GmbH

- Silgan Holdings Inc.

- DS Smith PLC

- Graham Packaging LP

- Quadpack Industries SA

- Libo Cosmetics Co. Ltd

- Gerresheimer AG

- Ball Corporation

- Verescence France SA

- SKS Bottle & Packaging Inc.

- Altium Packaging

- Cosmopak Ltd

- Raepak Ltd

- Rieke Corporation

- Essel Propack Ltd

- Huhtamaki Oyj

- Alpla Werke Alwin Lehner GmbH

- RPC M&H Plastics

- HCP Packaging Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing consumption of premium and masstige beauty products

- 4.2.2 Shift toward e-commerce-friendly lightweight formats

- 4.2.3 Rise of refillable / reusable delivery systems in prestige channels

- 4.2.4 Authentication-enabled smart packaging to curb counterfeits

- 4.2.5 Brand demand for carbon-label-ready packs

- 4.2.6 Rapid adoption of robot-ready secondary packs in 3-PL fulfilment

- 4.3 Market Restraints

- 4.3.1 Escalating global recycled-resin price volatility

- 4.3.2 Regulatory caps on single-use plastics

- 4.3.3 Filling-line incompatibility of novel bio-materials

- 4.3.4 Shrinking landfill capacity driving extended-producer-responsibility fees

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastics

- 5.1.1.1 Polyethylene Terephthalate (PET)

- 5.1.1.2 polypropylene (PP)

- 5.1.1.3 Polyethylene (PE)

- 5.1.1.4 Other Plastics

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Paper and Paperboard

- 5.1.1 Plastics

- 5.2 By Product Type

- 5.2.1 Bottles and Jars

- 5.2.2 Tubes and Sticks

- 5.2.3 Folding Cartons

- 5.2.4 Corrugated Transit Boxes

- 5.2.5 Flexible Sachets and Pouches

- 5.2.6 Other Product Type

- 5.3 By Dispensing Mechanism

- 5.3.1 Pump-based

- 5.3.2 Dropper / Pipette

- 5.3.3 Spray / Mist

- 5.3.4 Stick / Twist-up

- 5.3.5 Jar / Scoop

- 5.4 By Cosmetic Type

- 5.4.1 Skin Care

- 5.4.1.1 Facial Care

- 5.4.1.2 Body Care

- 5.4.2 Hair Care

- 5.4.3 Color Cosmetics

- 5.4.4 Perfumes and Fragrances

- 5.4.5 Other Cosmetics Type

- 5.4.1 Skin Care

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacifc

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Kenya

- 5.5.4.2.4 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Albea SA

- 6.4.2 AptarGroup Inc.

- 6.4.3 Amcor Group GmbH

- 6.4.4 Silgan Holdings Inc.

- 6.4.5 DS Smith PLC

- 6.4.6 Graham Packaging LP

- 6.4.7 Quadpack Industries SA

- 6.4.8 Libo Cosmetics Co. Ltd

- 6.4.9 Gerresheimer AG

- 6.4.10 Ball Corporation

- 6.4.11 Verescence France SA

- 6.4.12 SKS Bottle & Packaging Inc.

- 6.4.13 Altium Packaging

- 6.4.14 Cosmopak Ltd

- 6.4.15 Raepak Ltd

- 6.4.16 Rieke Corporation

- 6.4.17 Essel Propack Ltd

- 6.4.18 Huhtamaki Oyj

- 6.4.19 Alpla Werke Alwin Lehner GmbH

- 6.4.20 RPC M&H Plastics

- 6.4.21 HCP Packaging Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment