|

시장보고서

상품코드

1939652

ASEAN의 건설 기계 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)ASEAN Construction Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

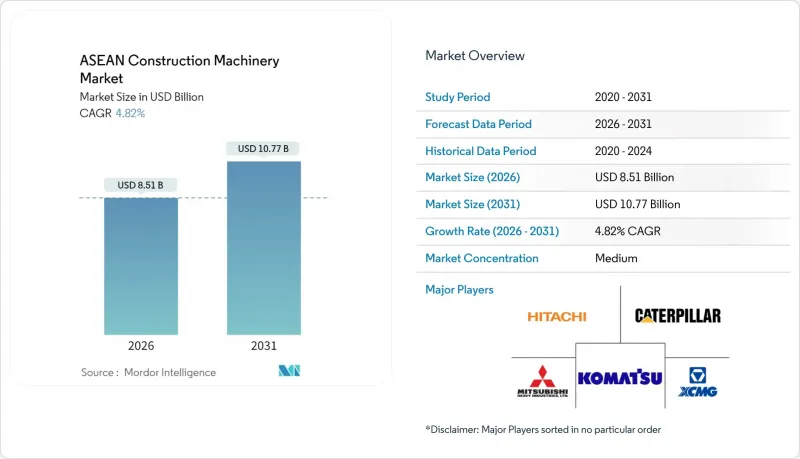

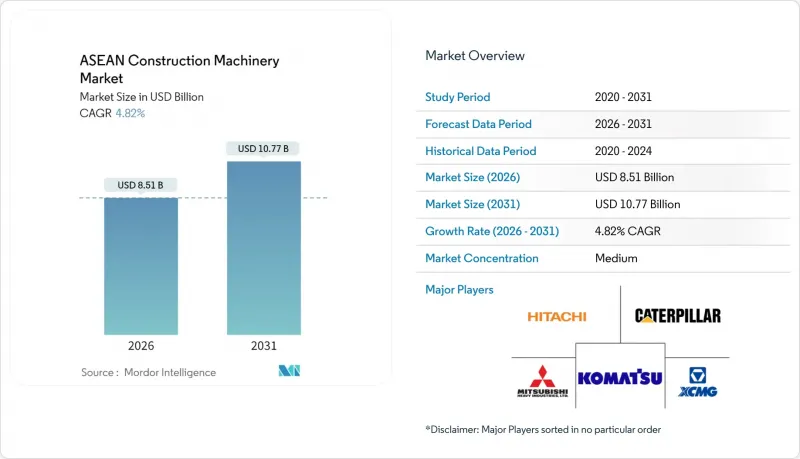

ASEAN의 건설 기계 시장은 2025년 81억 2,000만 달러에서 2026년에는 85억 1,000만 달러로 성장하며, 2026-2031년에 CAGR 4.82%로 추이하며, 2031년까지 107억 7,000만 달러에 달할 것으로 예측되고 있습니다.

이 시장의 모멘텀은 인도네시아 동부 깔리만딴주의 신수도에서 태국-베트남 고속철도 회랑에 이르는 인프라 슈퍼사이클을 반영하고 있습니다. 산업단지에 대한 지속적인 외국인 직접투자, 니켈 채굴 설비 투자 회복, 현장의 디지털화 가속화, 전체 주요 장비 카테고리의 차량 업데이트가 지속적으로 촉진되고 있습니다. 동시에 중국 제조업체들은 계약자의 현지화 요청에 따라 빠르게 확장하며 경쟁 구도와 가격대를 재편하고 있습니다. 정부의 배기가스 규제 강화와 건설사의 지속가능성에 대한 노력을 배경으로 설비 전동화와 수소 프로토타입의 등장은 새로운 기회요인이 되고 있습니다. 미중 무역 마찰에 따른 공급망 혼란과 지속적인 운영자 부족은 여전히 성장을 저해하는 주요 요인으로 작용하고 있지만, 적극적인 기술 훈련 프로그램과 공급처 다변화 전략으로 이러한 리스크는 점차 상쇄되고 있습니다.

아세안 건설기계 시장 동향 및 인사이트

인도네시아의 IKN 수도 건설이 주도하는 인프라 슈퍼 사이클

누산타라 계획의 기반시설은 단계별 패키지로 진행되고 있으며, 조달 주기는 2040년대 중반까지 연장되어 있습니다. 5개 민간 투자자들은 이미 2025년까지 생활거점, 복합용도지구, 핵심 인프라 개발에 2조 4,000억 루피아 이상을 투자하기로 약속한 바 있습니다. 공공 부문의 예산 배분은 100조 루피아를 넘어섰으며, 디지털 트윈 기술을 활용한 도로 구간 설계도 포함되어 있습니다. 이러한 프로젝트 규모는 굴착기, 로더, 콘크리트 펌프, 특수 리프팅 장비의 수주 파이프라인을 유지하는 동시에 OEM 업체의 부품 공급의 현지화를 촉진하고 있습니다. 그러나 시멘트 출하 지연과 간헐적인 예산 재검토는 실행 리스크를 나타내며, 단기적으로 설비 발주를 억제할 가능성이 있습니다. 계획 중인 민관협력(PPP) 구조는 향후 10년간 대출기관의 기반을 확대함으로써 자금 조달 압력을 완화할 것으로 기대됩니다.

초대형 굴착기 수요를 견인하는 니켈광산 붐 조성

인도네시아가 세계 최대 니켈 생산국으로 부상한 것이 초대형 설비 수주 확대를 지원하고 있습니다. 120톤급 굴착기 'EX1200'의 양산은 2024년 11월부터 시작되며, 현재 신규 광산 개발 및 기존 광산 확장에 투입될 예정입니다. 배터리 재료 수요 증가에 따라 2029년까지 광산 설비 보유량은 크게 증가할 것으로 예측됩니다. OEM 업체들은 라테라이트 광석 조건에 특화된 100톤급 및 150톤급 시제품을 전시하고 있으며, 현지 업체들은 두 자릿수 시장 점유율 확대를 목표로 하고 있습니다. 니켈 가격이 회복세를 보이고 있으며, 광산은 선투자를 진행하고 있지만, 환경감사의 강화로 인해 추가적인 기술 투자가 필요할 수 있습니다.

초기 설비투자 급증과 프로젝트 파이낸싱 금리 긴축으로 인한 초기 설비투자 증가

세계 금리 사이클에 따라 금리 부담이 증가하면서 신규 설비 구매의 문턱이 높아지고 있습니다. 정부 예산 조정(특히 인도네시아의 경우, 2025년 인프라 예산이 축소됨에 따라 공공 부문 입찰이 제한되고 있습니다. 부채가 많은 국영 건설업체들은 단기채무 재융자를 계속하고 있지만, 이익 감소로 인해 기계설비 자체 자금조달 능력에 제약이 있습니다. 대출 서류의 표준화를 위한 지역적 노력은 보험 및 연금 자본을 장기 인프라 투자 수단으로 동원하여 중기적으로 자금 조달의 제약을 완화하는 것을 목표로 하고 있습니다. 건설 관련 대출을 많이 취급하는 은행들은 저공해 기계 도입을 장려하는 지속가능성 연동형 대출 한도를 도입하고 있습니다.

부문 분석

2025년 아세안 건설기계 시장 규모에서 굴착기가 차지하는 비중은 35.10%로, 이 카테고리의 우위를 확고히 하고 있습니다. 인도네시아의 광산 사양은 고톤수 모델이 주류를 이루고 있으며, 중형 기계는 도로 및 철도 프로젝트에서 여전히 널리 채택되고 있습니다. 혼잡한 도시 환경에서 굴착과 적재를 동시에 할 수 있는 백호 로더는 지자체의 배수로 및 통신선로 정비에 따라 9.86%의 가장 높은 CAGR을 기록했습니다. 크롤러 굴착기(20-30톤급)는 인도네시아 수주량의 4분의 3 이상을 차지하며, 복합지형 현장에서의 높은 활용성을 보여주고 있습니다. 로더 수요는 항만 확장으로 견고한 수요를 유지하는 한편, 모터 그레이더와 포장기계는 고속도로 복선화 사업으로 수요가 확대. 텔레핸들러와 덤프트럭은 수량은 적지만 산업단지 창고와 광물 운반 경로에서 틈새 수요를 유지하고 있습니다.

도입 동향을 보면 통합 제어 시스템으로의 꾸준한 전환이 뚜렷하며, 이러한 추세로 인해 중고 시장에서는 비교적 새로운 모델에 대한 평가가 높아지고 있습니다. 렌탈 업체들이 텔레매틱스 계약을월요금에 포함시키는 경우가 증가하고 있으며, 이는 계약자가 커넥티드 기기를 선택할 수 있는 인센티브를 제공하여 서비스 매출의 잠재적 시장이 확대되고 있습니다. 현지 조립업체는 관세 우대를 활용하고, 신용공여 한도를 확대하여 중소기업의 구매 장벽을 낮추고, 주요 토목기계의 교체 주기를 유지하고 있습니다.

토목 건설기계는 아세안 건설기계 시장 점유율의 53.72%를 차지하며, CAGR 4.83%로 가장 빠르게 성장하고 있는 분야입니다. 누산타라 도시 건설, 국경 횡단 철도 회랑과 같은 메가 프로젝트에서는 광활한 지역에 걸쳐 지속적인 굴착, 정돈, 운반 작업이 요구됩니다. 콘크리트 도로 건설은 베트남의 대규모 고속도로 프로젝트 수주에 힘입어 슬립 폼 포장기는 하루 500 미터의 생산성을 달성하고 있습니다. 산업단지 입주자들이 라인 기계와 조립식 모듈을 수입함에 따라 자재관리량도 증가하고 있습니다.

광업 지원 분야는 니켈 채굴에 대한 지속적인 투자로 지역 평균을 상회하는 성장세를 유지하고 있습니다. 한편, 도심 재개발에 따라 철거 및 재활용 활동은 그 규모가 확대되고 있습니다. 특히 광섬유 기간선이나 송전망 업그레이드 등 유틸리티 설비 공사에서는 서비스 중단을 최소화하기 위해 첨단 감지 기능을 갖춘 콤팩트한 장비가 활용되고 있습니다. 디지털 트윈의 통합, 특히 스마트 시티 및 철도 노선 계획의 도입으로 인해 손 반환 주기가 단축되고 정밀 유도 기계에 대한 수요가 증가하고 있습니다. 건설사들은 텔레매틱스 데이터 활용으로 유휴시간이 10-15% 감소했다고 보고하고 있으며, 고성능 기술 패키지의 도입 의의가 더욱 커지고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The ASEAN construction machinery market is expected to grow from USD 8.12 billion in 2025 to USD 8.51 billion in 2026 and is forecast to reach USD 10.77 billion by 2031 at 4.82% CAGR over 2026-2031.

The market's momentum reflects an infrastructure super-cycle stretching from Indonesia's new capital city in East Kalimantan to a Thailand-Vietnam high-speed rail corridor. Sustained foreign direct investment into industrial parks, a resurgence in nickel-mining capital expenditure, and accelerating job-site digitalization continue to refresh fleets across every major equipment category. At the same time, Chinese original-equipment manufacturers (OEMs) are expanding rapidly under contractor-localization mandates, reshaping competitive dynamics and price points. Equipment electrification and emerging hydrogen prototypes signal another layer of opportunity as governments tighten emissions regulations and construction firms pursue sustainability credentials. Supply-chain shocks tied to U.S.-China trade frictions and persistent operator shortages remain the principal brakes on growth, but proactive skills-training programs and diversified sourcing strategies are gradually offsetting these risks

ASEAN Construction Machinery Market Trends and Insights

Infrastructure Super-Cycle Driven by Indonesia's IKN Capital-City Build

Groundwork at the Nusantara project is proceeding in phased packages that extend procurement cycles into the mid-2040s. Five private investors have already committed more than Rp 2.4 trillion for 2025 milestones covering lifestyle centers, mixed-use precincts, and essential utilities. Public-sector allocations have surpassed Rp 100 trillion and include road sections designed within a digital-twin framework. Such project breadth sustains order pipelines for excavators, loaders, concrete pumps, and specialist lifting gear while encouraging OEMs to localize component supply. Nonetheless, delayed cement shipments and episodic budget revisions illustrate execution risks that could temper near-term equipment call-offs. Planned public-private-partnership structures are expected to relieve funding pressure by broadening the lender base over the next decade.

Nickel-Mine Boom Fuelling Demand for Ultra-Large Excavators

Indonesia's ascent as the world's leading nickel producer underpins a wave of ultra-large equipment orders. Mass production of 120-ton class EX1200 hydraulic excavators began in November 2024 and is now geared toward both green-field and brown-field mine expansions. The mining equipment fleet is positioned to climb significantly by 2029 as battery-materials demand widens. OEMs are showcasing 100-ton and 150-ton prototypes tailored for laterite ore conditions, while local contractors target double-digit market share gains. With nickel prices rebounding, mines are front-loading capital outlays although tighter environmental audits could require additional technology investments.

High Upfront Capex and Tightening Project-Finance Rates

Interest costs have climbed alongside global rate cycles, lifting hurdle rates for new equipment purchases. Government budget adjustments, most visible in Indonesia where the 2025 infrastructure allocation has narrowed, restrict public-sector tender releases. Highly leveraged state-owned contractors continue to refinance short-dated debt, but profit erosion limits their ability to self-fund machinery. A regional effort to standardize loan documentation seeks to mobilize insurance and pension capital into long-dated infrastructure vehicles, thereby easing financing constraints over the medium term. Banks with large construction portfolios are introducing sustainability-linked loan tranches that reward the uptake of low-emission machinery.

Other drivers and restraints analyzed in the detailed report include:

- Thailand-Vietnam High-Speed Rail Corridor Boosting Cross-Border Equipment Demand

- Strong FDI Inflows into ASEAN Industrial Parks and Sezs

- Shortage of Certified Operators Inflating OPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The ASEAN construction equipment market size for excavators amounted to 35.10% of total value in 2025, solidifying the category's lead. High-tonnage models now dominate Indonesian mine specifications, while medium-class units remain omnipresent on road and railway projects. Backhoe loaders, which deliver combined digging and loading capability in congested urban environments, post the fastest 9.86% CAGR as municipalities upgrade drainage and telecom lines. Crawler excavators in the 20-30 tonne band captured more than three-quarters of Indonesian orders, underscoring their versatility within mixed-terrain sites. Loader demand stays resilient on account of port expansions, whereas motor graders and pavers benefit from motorway duplication programs. Telehandlers and dump trucks, although smaller in volume, enjoy niche resilience for industrial-park warehousing and mineral-haul circuits.

Adoption patterns reveal a steady pivot toward integrated control systems, a trend that moves secondary-market valuations in favor of more recent models. Rental companies increasingly bundle telematics subscriptions with monthly rates, incentivizing contractors to opt for connected equipment and thereby enlarging the addressable service revenue pool. Local assemblers, leveraging tariff preferences, extend credit lines that lower acquisition barriers for small contractors and sustain the replacement cycle for primary earth-moving machines.

Earth-moving held 53.72% of ASEAN construction equipment market share and remains the fastest-expanding application at a 4.83% CAGR. Mega-projects such as the Nusantara city build and the cross-border rail corridor require continuous excavation, grading, and hauling across vast footprints. Concrete-road construction benefits from large expressway packages in Vietnam where slip-form pavers reach productivity outputs of 500 meters per day. Material-handling volumes climb as industrial-park tenants import line machinery and prefabricated modules.

Mining support continues to outpace regional averages thanks to sustained investment in nickel extraction, while demolition and recycling activities scale up alongside inner-city redevelopment. Utility-installation works, especially fiber-optic backbones and grid upgrades, leverage compact equipment fitted with advanced detection to minimize service interruptions. Integration of digital twins, especially on smart-city and rail alignments, compresses rework cycles and elevates demand for precision-guided machines. Contractors report 10% to 15% reductions in idle time by exploiting telematics data, reinforcing the case for premium technology packages.

The ASEAN Construction Machinery Market Report is Segmented by Machinery Type (Excavators, Loaders, and More), Application (Earth-Moving, Concrete and Road Construction, and More), End-Use Industry (Residential Construction, Commercial Construction, and More), Propulsion (Diesel, Hybrid, and More), and Country (Indonesia, Thailand, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co.

- XCMG Group

- Sany Heavy Industry

- Liebherr Group

- JCB

- CNH Industrial (CASE and New Holland)

- Volvo Construction Equipment

- Zoomlion Heavy Industry

- Doosan Infracore

- Hyundai Construction Equipment

- Kobelco Construction Machinery

- Yanmar Co., Ltd.

- Wirtgen Group

- Kubota Corporation

- Sandvik Mining and Rock Tech.

- Terex Corporation

- Sumitomo Construction Machinery

- Manitou Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure Super-Cycle Driven by Indonesia's IKN Capital-City Build

- 4.2.2 Nickel-Mine Boom Fuelling Demand for Ultra-Large Excavators

- 4.2.3 Thailand-Vietnam High-Speed Rail Corridor Boosting Cross-Border Equipment Demand

- 4.2.4 Strong FDI Inflows into ASEAN Industrial Parks and Sezs

- 4.2.5 Belt and Road Contractor-Localization Mandates Increasing Chinese OEM Sales

- 4.2.6 Job-Site Digitalization (BIM + 5G Telematics) Accelerating Fleet Renewal

- 4.3 Market Restraints

- 4.3.1 High Upfront Capex and Tightening Project-Finance Rates

- 4.3.2 Shortage of Certified Operators Inflating OPEX

- 4.3.3 Sparse Charging / Hydrogen Refuelling Network Slowing Green-Equipment Uptake

- 4.3.4 China-US Trade Volatility Causing Engine and Parts Supply Shocks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Machinery Type

- 5.1.1 Excavators

- 5.1.2 Loaders

- 5.1.3 Cranes

- 5.1.4 Backhoe Loaders

- 5.1.5 Motor Graders

- 5.1.6 Pavers and Compactors

- 5.1.7 Others (Telehandlers, Dump Trucks, etc.)

- 5.2 By Application

- 5.2.1 Earth-Moving

- 5.2.2 Concrete and Road Construction

- 5.2.3 Material Handling and Logistics

- 5.2.4 Mining Support

- 5.2.5 Demolition and Recycling

- 5.2.6 Utilities Installation

- 5.2.7 Others

- 5.3 By End-Use Industry

- 5.3.1 Residential Construction

- 5.3.2 Commercial Construction

- 5.3.3 Infrastructure / Public Works

- 5.3.4 Mining

- 5.3.5 Oil and Gas

- 5.3.6 Industrial Manufacturing

- 5.3.7 Others

- 5.4 By Propulsion

- 5.4.1 Diesel

- 5.4.2 Hybrid

- 5.4.3 Battery-Electric

- 5.4.4 Hydrogen Fuel-Cell

- 5.4.5 Others

- 5.5 By Country

- 5.5.1 Indonesia

- 5.5.2 Thailand

- 5.5.3 Vietnam

- 5.5.4 Philippines

- 5.5.5 Malaysia

- 5.5.6 Singapore

- 5.5.7 Rest of ASEAN (Myanmar, Laos, Cambodia, Brunei)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Hitachi Construction Machinery Co.

- 6.4.4 XCMG Group

- 6.4.5 Sany Heavy Industry

- 6.4.6 Liebherr Group

- 6.4.7 JCB

- 6.4.8 CNH Industrial (CASE and New Holland)

- 6.4.9 Volvo Construction Equipment

- 6.4.10 Zoomlion Heavy Industry

- 6.4.11 Doosan Infracore

- 6.4.12 Hyundai Construction Equipment

- 6.4.13 Kobelco Construction Machinery

- 6.4.14 Yanmar Co., Ltd.

- 6.4.15 Wirtgen Group

- 6.4.16 Kubota Corporation

- 6.4.17 Sandvik Mining and Rock Tech.

- 6.4.18 Terex Corporation

- 6.4.19 Sumitomo Construction Machinery

- 6.4.20 Manitou Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment