|

시장보고서

상품코드

1939654

타이어 보강 재료 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Tire Reinforcement Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

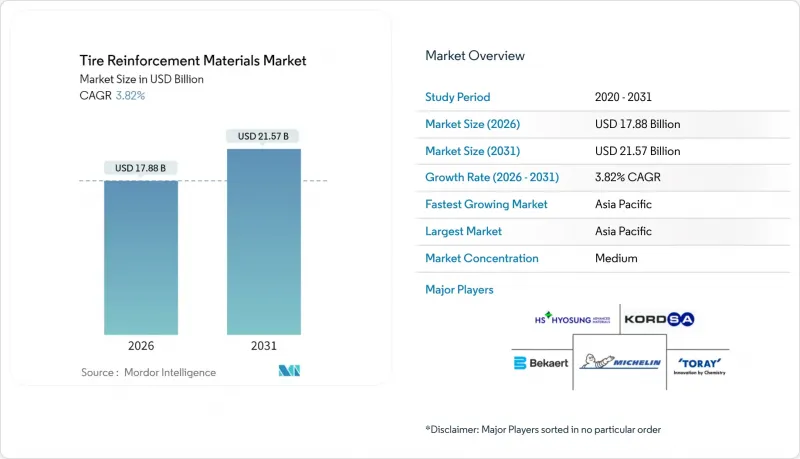

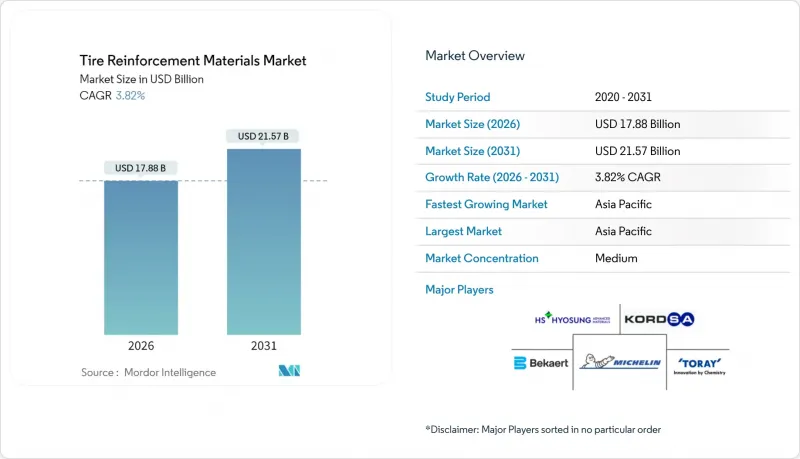

타이어 보강 재료 시장 규모는 2026년에는 178억 8,000만 달러로 추정되고 있으며, 2025년 172억 2,000만 달러에서 성장이 전망됩니다.

2031년의 예측에서는 215억 7,000만 달러에 달하며, 2026-2031년에 CAGR 3.82%로 확대할 것으로 전망되고 있습니다.

견고한 레이디얼 타이어 수요, 강화되는 연비 규제, 그리고 첨단화된 복합 코드의 꾸준한 전환이 시장 확장을 지원하고 있습니다. 강재는 높은 인장강도로 인해 비용 증가 없이 무게가 늘어나는 전기자동차를 지탱할 수 있으므로 1차 공급망의 근간이 되고 있습니다. 경량 아라미드 및 그래핀 개질 코드는 자동차 제조업체들이 구름 저항을 줄이기 위해 고급 승용차 및 상용차 부문에서 채택이 확대되고 있습니다. 한편, 폐쇄 루프 냉각 방식을 채택한 용융 방적 라인이 급속히 확대되고 있으며, 섬유 제조업체는 에너지 소비와 용제 배출량을 줄일 수 있습니다. 지역별로는 아시아태평양의 성장이 두드러지며, 현지화된 비드 와이어 공장이 타이어 제조업체의 운송비 및 관세 리스크 헤지에 기여하는 동시에 급증하는 교체용 타이어 수요에 대응하고 있습니다.

세계 타이어 보강재 시장 동향 및 전망

전 세계 자동차 보유대수 및 교체용 타이어 수요 증가 추세

신흥 국가의 자동차 보급이 가속화되면서 교체 주기가 단축되고 고급 강선 및 폴리에스테르 코드에 대한 수요가 증가하고 있습니다. 캄보디아는 2025년 3억 3,500만 달러 규모의 그린필드 타이어 공장 건설을 승인하여 캄보디아를 지역 OEM공급기지로 자리매김하고 있습니다. 베트남의 2024년 고무 수출 매출은 18% 증가한 34억 달러에 달할 것으로 예상되며, 이는 물량은 감소했지만 가격은 견고하게 유지된 것을 반영합니다. 보강재 공급업체에 유리한 공급 부족 상황이 확인되었습니다. 동남아시아 및 라틴아메리카 전역에서 중고차 수입이 증가함에 따라 차량의 평균 사용 연한이 단축되면서 내구성이 뛰어난 비드 와이어 및 벨트 플라이 패브릭에 대한 수요가 증가하고 있습니다. 따라서 브랜드 오너들은 생산 능력을 확보하고 가격 변동을 헤지하기 위해 코드 제조업체와 다년간의 오프 테이크 계약을 체결하고 있습니다. 이러한 예측 가능한 수요 추세는 스틸코드 드로잉 공장 및 폴리에스테르 용융방사 라인에 대한 단계적인 설비투자를 지원하고 있습니다.

아시아태평양 물류의 급격한 성장이 레이디얼 타이어 생산을 주도

E-Commerce의 물류 수요와 고속도로 화물 운송의 확대로 중대형 트럭용 타이어 생산이 증가하고 있습니다. ZC Rubber의 인도네시아 공장에서는 2024년 아세안 물류 사업자를 위한 디지털 통합형 가황 프레스를 도입하여 올스틸 래디얼 타이어 생산을 시작했습니다. 미국의 반덤핑 관세 정책의 변화로 태국에서 트럭-버스용 래디얼 타이어 수출이 캄보디아 등 신규 거점으로 이동하면서 비드 와이어 조달 패턴이 재편되고 있습니다. 현지 보강 시설은 다운타임을 용납할 수 없는 함대 고객의 리드타임을 단축합니다. 고탄성 폴리에스터 및 초고장력(EUT) 스틸 코드는 상업용 타이어 제조업체와의 계약에서 우선적으로 배정되어 아시아태평양에서의 성장 궤도를 확고히 하고 있습니다.

원자재 가격 변동(철강, 나일론)

코크스용 석탄, 철광석, 파라크실렌 원료 가격 급등으로 2024년에는 보강재 투입 비용이 두 자릿수 상승했습니다. 아폴로타이어는 매출 증가에도 불구하고 영업이익이 전년 대비 24% 감소해 철강재와 나일론 가격 변동에 따른 이익률 압박이 두드러졌습니다. 태국과 말레이시아의 천연고무 공급 차질은 에너지 할증료 부담에 시달리는 코드 제조업체의 운전자금을 더욱 압박했습니다. 헤지 프로그램이 없는 중소 가공업체는 유동성 위기에 직면하여 통합형 강선 대기업의 기회주의적 인수를 유발했습니다. 이러한 변동은 타이어 보강재 시장의 단기적인 EBITDA를 하락시킬 것입니다.

부문 분석

철강재는 세계 시장 가치의 39.75%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 4.12%를 유지할 것으로 예측됩니다. 인장강도 11,000N에 달하는 고탄소강선은 안전성을 유지하면서 경량화된 카카스 구조를 실현합니다. 베카르는 세계 용융 공장 통합과 폐쇄 루프 산세 공정을 활용하여 전 세계 타이어 코드 수요의 30%를 점유하고 있습니다. 이는 OEM(Original Equipment Manufacturer)공급 안정성에 대한 선호도를 강화합니다. 예측 기간 중 초고장력 등급이 양산형 EV 타이어로 전환되고, 기가팩토리 인근에서 운영되는 강선 코드 라인의 매출이 확대될 것으로 예측됩니다.

폴리에스터 원사는 가격 안정성과 가공 용이성으로 인해 비용 중심의 승용차 타이어용 플라이 소재로 계속 채택될 것입니다. 나일론은 고속 오토바이 타이어 등 고온 환경이 지속되는 틈새 시장을 유지하지만, 카프로락탐에 대한 의존도가 높아 석유화학 원료 가격 변동에 영향을 받기 쉽습니다. 아라미드는 경량화가 연비 향상과 전기자동차 주행거리 연장과 직결되는 프리미엄 분야이지만, 원료 공급이 여전히 부족한 상황입니다. 전반적으로 다양한 소재 선택은 타이어 제조업체가 브랜드 성능에 대한 약속을 훼손하지 않고 지역과 규제에 따라 SKU를 최적화할 수 있는 유연성을 제공합니다.

2025년 생산량 중 56.05%를 차지한 용융방적은 섬유업체들이 에너지 절약형 급냉 시스템을 도입하면서 2031년까지 연평균 복합 성장률(CAGR) 4.14%를 나타낼 것으로 예측됩니다. 직접 칩-투-원사 압출 성형과 고주파(HF) 고데트의 조합으로 전력 사용량을 줄이고, 보다 정밀한 데니어 제어를 실현합니다. 타이어 보강재 시장에서 용융방적 폴리에스터는 이미 해당 하위 부문에서 70% 이상의 점유율을 차지하고 있습니다. 한편, 나일론 제조업체들은 용제 다용도 용액방적에서 용액방적으로의 전환을 꾸준히 추진하고 있습니다.

특수 코드 분야에서는 다단계 연신 기술이 결정성과 내마모성을 향상시키기 때문에 연신 기술이 여전히 중요합니다. 2단계 연신 조사 결과, 단일 단계 방식에 비해 표면 평활도가 15% 향상되어 스키밍 스톡 고무와의 밀착성이 향상되었습니다. 아라미드 및 메타-아라미드 섬유는 용액방사가 계속되고 있지만, 용제 회수 의무로 인해 운영비용이 증가하는 추세입니다. 베이스 로드용 용융방적과 고성능 섬유용 용액방적의 조합이 향후 5년간의 설비 투자 결정의 특징이 될 것입니다.

타이어 보강재 보고서는 재료별(강선, 폴리에스테르, 나일론, 레이온, 아라미드, 아라미드, 기타 재료), 기술별(연신, 용융방적, 용액방적), 보강 유형별(타이어 코드 패브릭, 타이어 비드 와이어), 용도별(자동차 카카스, 벨트 플라이, 캡 플라이), 지역별(아시아태평양, 북미, 유럽, 일본, 중국, 유럽, 일본, 대만) 지역별(아시아태평양, 북미, 유럽 등)로 분류되어 있습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 매출의 50.70%를 차지할 것으로 예상되며, 중국, 인도, 동남아시아의 OEM 및 교체용 타이어 생산 확대에 따라 2031년까지 연평균 복합 성장률(CAGR) 4.54%를 나타낼 것으로 예측됩니다. 캄보디아에 중국 투자자가 투자하여 건설된 두 개의 새로운 타이어 공장은 메콩강 지역 전체에 적시 납품을 우선시하는 비드 와이어 및 코드 공급 계약을 확보했습니다.

북미는 미국 SmartWay 연비기준에 대한 차량 대응을 배경으로 프리미엄 부문에서 높은 점유율을 차지하고 있습니다. 에보닉은 찰스턴 공장에 5,000만 달러를 투자하여 저게이지, 고탄성 폴리에스테르 코드와 잘 어울리는 '친환경' 타이어 컴파운드용 실리카 생산량을 늘렸습니다. 트레레보그의 노스캐롤라이나 공장에서는 내층 보강재 역할을 하는 바이오 코팅 천을 생산하여 지역내 순환형 소재에 대한 노력을 반영하고 있습니다.

유럽에서는 지속가능성과 자동화가 중요시되고 있습니다. 미쉐린은 로안 공장에 3억 유로를 투자하여 아라미드 벨트와 저유출 비드 와이어를 통합한 초고성능 타이어 C3M 소량 생산을 시작했습니다. 탄소 국경 조정이 엄격해지면서 저탄소 인증이 없는 수입 코드 원단의 진입 장벽이 높아지고 있습니다. 따라서 슬로바키아와 루마니아의 동유럽 공장에서는 향후 규제 준수와 고객 수용성을 확보하기 위해 산세조에서 폐쇄형 루프 산 회수를 도입하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06Tire Reinforcement Materials Market size in 2026 is estimated at USD 17.88 billion, growing from 2025 value of USD 17.22 billion with 2031 projections showing USD 21.57 billion, growing at 3.82% CAGR over 2026-2031.

Robust radial-tire demand, tightening fuel-efficiency rules, and a steady shift toward advanced composite cords underpin expansion. Steel continues to anchor the tier-one supply chain because its high tensile strength supports heavier electric vehicles without raising costs. Lightweight aramid and graphene-modified cords are gaining traction in premium passenger and commercial segments as automakers chase lower rolling resistance. Meanwhile, melt-spinning lines with closed-loop cooling are scaling rapidly, allowing fiber makers to trim energy intensity and solvent emissions. Regional growth skews toward Asia-Pacific, where localized bead-wire plants help tire makers hedge against freight and tariff risks while meeting surging replacement-tire volumes.

Global Tire Reinforcement Materials Market Trends and Insights

Rising Global Vehicle Parc and Replacement-Tire Demand

Accelerating motorization in emerging economies is shortening replacement cycles and intensifying demand for premium steel and polyester cords. Cambodia approved USD 335 million in greenfield tire factories in 2025, positioning the country as a feeder hub for regional OEMs. Vietnam's 2024 rubber-export earnings rose 18% to USD 3.4 billion, reflecting strong pricing even as volumes eased, and confirming supply tightness that favors reinforcement suppliers. As used-car imports climb across Southeast Asia and Latin America, fleets age faster and require durable bead wire and belt-ply fabrics. Brand owners are therefore signing multi-year off-take accords with cord producers to lock in capacity and hedge price swings. This predictable demand profile supports incremental capex in steel-cord drawing mills and polyester melt-spinning lines.

Rapid Asia-Pacific Logistics Boom Spurring Radial-Tire Output

E-commerce fulfillment and highway-freight growth are lifting medium- and heavy-truck tire production. ZC Rubber's Indonesian plant launched all-steel radial output in 2024 with digitally integrated curing presses to serve ASEAN logistics operators. Shifting U.S. antidumping duties have also rerouted truck-bus radial exports from Thailand to newer bases like Cambodia, reshaping bead-wire sourcing patterns. Local reinforcement facilities shorten lead times for fleet customers that cannot afford downtime. High-modulus polyester and extra-ultra-tensile (EUT) steel cords thus enjoy priority allocation in contracts with commercial-tire makers, solidifying the growth trajectory in Asia-Pacific.

Raw-Material Price Volatility (Steel, Nylon)

Spikes in coking coal, iron ore, and para-xylene feedstocks lifted reinforcement input costs by double digits in 2024. Apollo Tyres' operating profit slid 24% year over year despite topline growth, underscoring the margin pinch from steel and nylon swings. Natural-rubber disruptions in Thailand and Malaysia further strained working capital for cord makers already juggling energy surcharges. Smaller processors without hedge programs faced liquidity crunches, triggering opportunistic acquisitions by integrated steel-wire majors. Such volatility shaves near-term EBITDA for the tire reinforcement materials market.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight High-Strength Cords to Meet Fuel-Efficiency Norms

- Safety Regulations Elevating Premium Reinforcement Adoption

- Emission Regulations on Carbon-Black and Steel-Cord Plants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Steel held a 39.75% of global value, and is on track for a 4.12% CAGR through 2031. High-carbon wire featuring tensile strengths up to 11,000 N enables lighter carcass profiles without sacrificing safety. Bekaert leverages global melt-shop integration and closed-loop pickling to support a 30% share of world tire-cord demand, reinforcing supply-security preferences among OEMs. Over the forecast horizon, extra-ultra-tensile grades will migrate into mass-market EV tires, expanding revenue for steel-cord lines operating in proximity to gigafactories.

Polyester yarns continue to serve cost-sensitive passenger-tire plies because of stable pricing and easy processing. Nylon retains niches that involve sustained high temperatures, such as high-speed motorcycle tires, but its reliance on caprolactam exposes producers to petrochemical swings. Aramid occupies premium slots where weight savings translate directly into fuel-economy or EV-range gains, though feedstock availability remains tight. Overall, diversified material menus give tire makers the flexibility to optimize SKUs by region and regulation without diluting brand performance commitments.

Melt-spinning accounted for 56.05% of 2025 output and is guiding a projected 4.14% CAGR by 2031 as fiber houses deploy energy-efficient quench systems. ]. Direct-chip-to-yarn extrusion paired with high-frequency (HF) godets lowers electricity use and delivers finer denier control. The tire reinforcement materials market share for melt-spun polyester already surpasses 70% within that sub-segment, while nylon players are steadily migrating away from solvent-heavy solution spinning.

Drawing technology remains critical in specialty cords, where multi-stage orientation improves crystallinity and abrasion resistance. Research testing two-step drawing achieved a 15% smoother surface than single-step methods, which elevates adhesion with skim-stock rubber. Solution spinning persists in aramid and meta-aramid fibre, though solvent-recovery mandates are escalating operating costs. A blended approach-melt spin for base loads, solution spin for performance fibers-will characterize capex decisions over the next five years.

The Tire Reinforcement Materials Report is Segmented by Material (Steel, Polyester, Nylon, Rayon, Aramid, and Other Materials), Technology (Drawing, Melt Spinning, and Solution Spinning), Reinforcement Type (Tire Cord Fabric and Tire Bead Wire), Application (Automotive Carcasses, Belt Ply, and Cap Ply), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 50.70% of 2025 revenue and is slated for a 4.54% CAGR through 2031 as China, India, and Southeast Asia expand OEM and replacement tire output. Cambodia's two new tire plants, underwritten by Chinese investors, secure bead-wire and cord supply contracts that prioritize just-in-time delivery across the Mekong subregion.

North America holds a sizable share in premium segments, propelled by fleet adherence to U.S. SmartWay fuel-efficiency benchmarks. Evonik's USD 50 million silica expansion in Charleston targets "green" tire compounds that function best when paired with low-gauge, high-modulus polyester cords. Trelleborg's North Carolina plant will fabricate bio-based coated fabrics that can double as inner-liner reinforcements, reflecting a regional push toward circular materials.

Europe emphasizes sustainability and automation. Michelin invested EUR 300 million in Roanne to run C3M small-lot production of ultra-high-performance tires, each embedding aramid belts and low-spill bead wires. Stricter carbon-border adjustments raise hurdles for imported cord fabric that lacks low-carbon verification. Eastern European plants in Slovakia and Romania are therefore adopting closed-loop acid recovery in pickling baths to secure future compliance and customer acceptance.

- Bekaert

- Century Enka Limited

- CORDENKA GmbH & Co. KG

- Dupont

- FORMOSA TAFFETA CO. LTD

- HS HYOSUNG ADVANCED MATERIALS

- Indorama Ventures Mobility

- Jiangsu Xingda Steel Cord Co., Ltd

- Kolon Industries Inc.

- Kordsa Teknik Tekstil AS

- Michelin

- SRF LIMITED

- Sumitomo Electric Industries, Ltd

- TEIJIN LIMITED

- TOKUSEN KOGYO Co.,ltd

- TORAY INDUSTRIES, INC. (Toray Hybrid Cord Inc.)

- Wuxi Taiji Industrial Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Vehicle Parc and Replacement-Tire Demand

- 4.2.2 Rapid APAC Logistics Boom Spurring Radial Tire Output

- 4.2.3 Lightweight High-Strength Cords to Meet Fuel-Efficiency Norms

- 4.2.4 Safety Regulations Elevating Premium Reinforcement Adoption

- 4.2.5 Graphene-Enhanced Cords Cutting Rolling Resistance by More than or Equal to 30%

- 4.3 Market Restraints

- 4.3.1 Raw-Material Price Volatility (Steel, Nylon)

- 4.3.2 Emission Regulations on Carbon-Black/Steel-Cord Plants

- 4.3.3 Global Aramid-Fiber Supply Crunch (Defense Demand Spikes)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Steel

- 5.1.2 Polyester

- 5.1.3 Nylon

- 5.1.4 Rayon

- 5.1.5 Aramid

- 5.1.6 Other Materials

- 5.2 By Technology

- 5.2.1 Drawing

- 5.2.2 Melt Spinning

- 5.2.3 Solution Spinning

- 5.3 By Reinforcement Type

- 5.3.1 Tire Cord Fabric

- 5.3.2 Tire Bead Wire

- 5.4 By Application

- 5.4.1 Automotive Carcasses

- 5.4.2 Belt Ply

- 5.4.3 Cap Ply

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN

- 5.5.1.6 Rest of APAC

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Bekaert

- 6.4.2 Century Enka Limited

- 6.4.3 CORDENKA GmbH & Co. KG

- 6.4.4 Dupont

- 6.4.5 FORMOSA TAFFETA CO. LTD

- 6.4.6 HS HYOSUNG ADVANCED MATERIALS

- 6.4.7 Indorama Ventures Mobility

- 6.4.8 Jiangsu Xingda Steel Cord Co., Ltd

- 6.4.9 Kolon Industries Inc.

- 6.4.10 Kordsa Teknik Tekstil AS

- 6.4.11 Michelin

- 6.4.12 SRF LIMITED

- 6.4.13 Sumitomo Electric Industries, Ltd

- 6.4.14 TEIJIN LIMITED

- 6.4.15 TOKUSEN KOGYO Co.,ltd

- 6.4.16 TORAY INDUSTRIES, INC. (Toray Hybrid Cord Inc.)

- 6.4.17 Wuxi Taiji Industrial Co., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment