|

시장보고서

상품코드

1939656

연마재 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Abrasives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

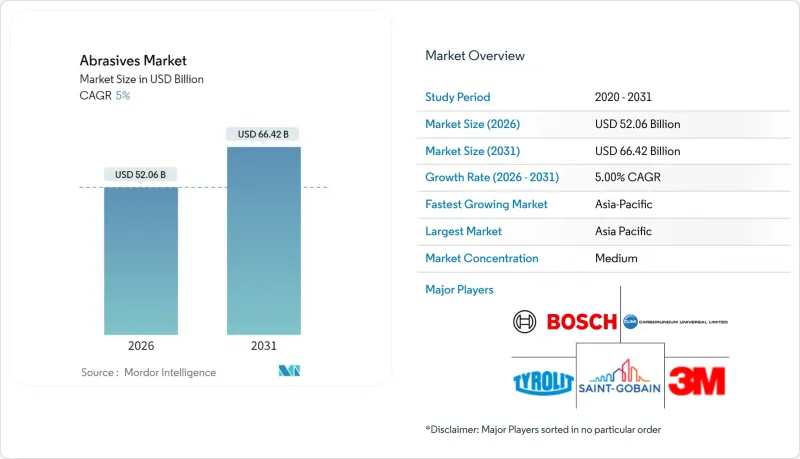

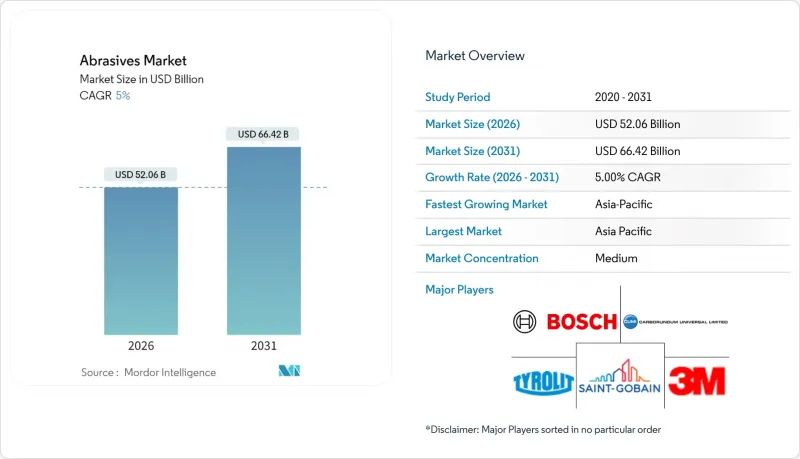

연마재 시장은 2025년 495억 8,000만 달러에서 2026년에는 520억 6,000만 달러로 성장하며, 2026-2031년에 CAGR 5.0%로 추이하며, 2031년까지 664억 2,000만 달러에 달할 것으로 예측되고 있습니다.

판매 모멘텀은 특히 전기자동차(EV) 및 항공우주 부품 가공에서 첨단 CNC 장비에서 엄격한 공차를 유지할 수 있는 고성능 소재에 대한 수요 증가를 반영하고 있습니다. 합성 재종은 신뢰할 수 있는 경도와 열 안정성을 제공하므로 지속적으로 수주를 받고 있으며, 결합형은 고온 연삭의 주력 제품으로 자리매김하고 있습니다. 아시아의 급속한 산업화, 정밀 전자제품으로의 전환, 적층가공(3D 프린팅)의 후처리 수요 증가는 연마재 시장의 성장 기반을 강화하고 있습니다. 규제 당국의 미립자 물질 및 휘발성유기화합물(VOC) 기준 강화에 따라 경쟁사 간 적대적 관계가 심화되고 있으며, 기존 대기업은 친환경 화학 성분을 중심으로 제품 포트폴리오를 고도화하고 있습니다. 한편, 틈새 업체들은 다이아몬드계 초연마재 등 특수 분야에서 점유율을 확대하고 있습니다.

세계 연마재 시장 동향과 인사이트

항공우주 및 자동차 산업 수요 증가

첨단 항공기용 합금과 경량 EV 구동계에 대한 수요가 증가함에 따라 제조업체들은 고속 가공에서도 형상을 유지하는 입방정 질화붕소(CBN)와 다이아몬드 휠을 지정하는 경향이 있습니다. Tier 1 공급업체는 유리질 CBN과 세라믹 연마재를 사용한 가공 라인을 최적화하여 E-Axle(전기식 액슬), 로터 샤프트, 배터리 하우징 가공에서 사이클 타임 단축과 드레서 간격 연장을 실현하고 있습니다. 노턴브러시브에 따르면 다이아몬드 공구와 자동 부하 감지 시스템을 결합하면 스크랩율이 현저하게 감소하는 것으로 보고되고 있으며, 이는 OEM(Original Equipment Manufacturer)가 반복성을 중시하여 고품질 등급을 표준화하는 이유를 보여줍니다. 조립 라인에 로봇이 보급됨에 따라 수작업 연삭으로는 달성할 수 없는 균일한 표면 마감가 요구되면서 연마재 시장은 계속 성장하고 있습니다.

계속 성장하는 금속 제조 및 가공 산업

강재 서비스 센터, 압력 용기 공장, 계약 가공 업체는 연삭 스테이션을 세라믹 연마 벨트로 업데이트했습니다. 이를 통해 최대 40%의 절삭량 증가를 실현하는 동시에 전력 소비를 절감하고 있습니다. 벨트 교체로 인한 다운타임 감소는 종합 설비 효율(OEE)의 향상으로 이어집니다. 이 지표는 린 생산 방식 하에서 점점 더 중요하게 여겨지고 있습니다. VSM TOP SIZE와 같은 특수 탑코트는 스테인리스 가공품의 열변색을 감소시키고, 열변형 없이 높은 이송 압력을 가능하게 합니다. 이러한 생산성 향상은 주문의 신속한 처리를 지원하며, 비용 중심의 대량 생산 환경에서 고급 세라믹 등급은 필수 불가결한 요소입니다.

높은 생산 비용과 설비 비용

합성 다이아몬드 및 CBN 결정은 지질학적 조건을 초과하는 압력과 온도에서 성장하므로 반응 용기의 자본 집약도는 기존의 용융 알루미나 라인을 크게 능가합니다. 다이아몬드 그라인딩 휠용으로 구성된 단일 헤드 CNC 연삭기는 정밀 스핀들과 폐쇄 루프 냉각 시스템이 필요하며, 도입 비용이 높아집니다. 이러한 공구는 수명이 길고 부품당 비용이 저렴하지만, 가격에 민감한 경제권의 중소형 가공 공장은 여전히 업데이트를 미루는 경향이 있습니다. 업체들은 리스 모델과 소모품 크레딧 프로그램을 시범적으로 도입하고 있지만, 자금 조달의 제약으로 인해 보급이 제한적입니다.

부문 분석

2025년 기준 합성 연마재는 연마재 시장의 66.35%를 차지할 것으로 예상되며, 이는 생산 공정에서 예측 가능한 마모 패턴으로 이어지는 균일한 결정 형태에 대한 사용자 선호도를 지원합니다. 알루미나가 여전히 주요 연마재이지만, 비철금속 가공에는 실리콘 카바이드가, 경화강 가공에는 CBN이 적합합니다. 스미토모전기가 개발중인 신규 나노 다결정 다이아몬드는 우수한 파괴 인성을 약속하며, 연마재 시장이 낮은 휠 마모율로 니켈계 초합금에 대응할 수 있는 기반을 마련하고 있습니다. 천연 가넷은 재활용 가능한 벌크 매체와 낮은 유리 실리카 함량으로 인한 현장 안전성 향상으로 인해 워터젯 및 발파 작업에서 기반을 유지하고 있으며, 인프라 개보수 프로젝트에서 매력적인 선택이 되고 있습니다.

합성 제품으로의 전환은 입도 분포를 엄격하게 관리해야 하는 자동 공급 시스템과의 일관성을 보여 주며, 이 매개 변수는 설계된 제조 공정을 통해 쉽게 달성할 수 있습니다. 아시아 지역의 용융알루미나 생산능력 확대에 따라 공급 안정성은 향상되고 있지만, 전력 요금의 변동이 생산 비용에 영향을 미칠 수 있습니다. 환경마크 획득을 목표로 하는 제조업체들은 규제 지역에서의 점유율 유지를 위해 재생에너지 구동 아크 로와 폐쇄 루프 수냉 시스템에 대한 투자를 진행하고 있습니다. 그 결과, 연마재 시장은 대량 생산 부문에서도 품질 기준이 지속적으로 향상되고 있습니다.

2025년 매출의 47.55%를 차지한 결합 연삭 휠은 자동차, 항공우주, 일반 기계 공장의 절삭, 연삭, 표면 처리 작업에서 그 역할을 반영하고 있습니다. 수지 및 유리질 매트릭스는 깊은 절삭 가공시 열적 안정성을 제공하고, 금속 조직의 무결성이 중요한 크랭크샤프트와 터빈 블레이드에서 일관된 공차를 제공합니다. 졸겔 공법의 알루미나 및 설계된 기공 구조의 발전으로 칩 배출성이 향상되어 화상 위험 없이 더 높은 금속 제거율을 실현하고 있습니다.

코팅 연마재는 톤수는 적지만 마무리 가공이나 디버링에 널리 활용되고 있습니다. 유연한 필름부터 섬유 디스크까지 다양한 기판으로 곡면이나 손이 닿기 어려운 영역에서의 성능에 최적화되어 있습니다. 초연마재는 현재 틈새 시장이지만, 두 자릿수 성장이 연마재 시장 전망 방향성을 지원하고 있습니다. 적층제조 공장에서는 기존의 연삭 휠이 금방 막히는 얇은 두께의 티타늄 부품에 다이아몬드 패드와 CBN 맨드릴을 지정하고 있습니다. 이멜리스와 같은 공급업체는 드레서 간격을 연장하는 맞춤형 용융 알루미나 및 졸겔 입자를 제공하여 결합 연삭 휠의 우위를 강화하는 동시에 초연마재와의 성능 차이를 메우고 있습니다.

연마재 시장 보고서는 재료별(천연 연마재와 합성 연마재), 유형별(결합 연마재, 코팅 연마재, 초연마재), 연마재 입자/원료별(알루미나, 탄화규소 등), 최종사용자 산업별(금속 제조 및 가공, 자동차 및 항공우주 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다.

지역별 분석

2025년 아시아태평양은 전 세계 구매량의 55.40%를 차지했습니다. 이는 중국의 거대한 가공 기반과 인도의 가속화된 인프라 구축을 반영합니다. 국내 전기자동차 배터리 제조 및 전자기기 조립에 대한 정부의 우대정책이 현지 수요를 더욱 자극하고 있습니다. 일본과 한국은 첨단 다이아몬드 반도체 조사를 활용하여 대면적 다이아몬드 웨이퍼 절단 등 초연마 입자의 새로운 다운스트림 용도를 창출하고 있습니다. 이러한 요인들이 복합적으로 작용하여 아시아의 선도적 지위를 유지하고, 다국적 기업의 혼합 및 프레스 공정의 현지화를 촉진하고 있습니다.

북미에서는 항공우주, 의료, 적층제조 분야에서 견고한 성장세를 유지하고 있습니다. 휘발성 유기화합물(VOC) 및 미립자 물질 배출에 대한 규제 강화로 가넷 블라스팅 매체 및 수성 쿨런트로의 전환이 진행되어 제품 구성의 고도화가 촉진되고 있습니다.

유럽에서는 지속가능성과 순환경제의 원칙이 강조되고 있으며, 산고밴과 같은 공급업체들은 탄소 강도 감소를 위해 재생 본드 시스템을 도입하고 있습니다. 독일 정밀기계 클러스터에서는 초연마재의 채택이 가속화되고 있으며, 남유럽에서는 건설 관련 발파 처리 및 절단 디스크의 소비에 초점을 맞추었습니다. 남미, 중동 및 아프리카는 여전히 규모는 작지만 산업화 진전에 따라 견고한 성장세를 보이고 있습니다. 브라질의 조선소와 걸프 지역의 석유화학 프로젝트는 최종사용자의 다양화가 진행되고 있음을 보여줍니다. 현지 가공 파트너십을 통해 세계 브랜드가 해당 지역에 진출하여 연마재 시장의 세계 커버리지를 강화할 수 있도록 돕고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The Abrasives Market is expected to grow from USD 49.58 billion in 2025 to USD 52.06 billion in 2026 and is forecast to reach USD 66.42 billion by 2031 at 5.0% CAGR over 2026-2031.

Sales momentum reflects rising demand for high-performance materials that can hold tight tolerances on advanced CNC equipment, especially in electric vehicle (EV) and aerospace component machining. Synthetic grades continue to capture orders because they deliver reliable hardness and thermal stability, while bonded formats remain the workhorse for high-temperature grinding. Rapid industrialization in Asia, the pivot toward precision electronics, and the emergence of post-processing needs for additive manufacturing all reinforce the growth runway for the abrasives market. Competitive rivalry is intensifying: large incumbents are refining product portfolios around eco-friendly chemistries as regulators tighten particulate and volatile-organic-compound (VOC) standards, and niche producers are carving share in specialty niches such as diamond-based super-abrasives.

Global Abrasives Market Trends and Insights

Increasing use in aerospace and automotive industries

Demand for advanced aircraft alloys and lightweight EV drivetrains is pushing producers to specify cubic boron nitride (CBN) and diamond wheels that maintain form at high speeds. Tier-one suppliers are optimizing E-Axle, rotor shaft, and battery-housing machining lines with vitrified CBN and ceramic media that cut cycle time and extend dresser intervals. Norton Abrasives reports measurable reductions in scrap rates when diamond tools are paired with automated load-sensing systems, illustrating why OEMs are standardizing on premium grades for repeatability. As robotics proliferate on assembly lines, the abrasives market gains from consistent surface-finish requirements that manual grinding cannot meet.

Growing metal manufacturing and fabrication industries

Steel service centers, pressure-vessel shops, and contract fabricators have upgraded grinding stations with ceramic-grain belts that increase stock removal by up to 40% while lowering power draw. Lower downtime for belt changes translates into higher overall equipment effectiveness (OEE), a metric increasingly monitored under lean programs. Specialized top-coats such as VSM TOP SIZE mitigate heat discoloration on stainless workpieces, enabling higher feed pressures without thermal distortion. These productivity gains support rapid order throughput, making high-end ceramic grades essential in cost-sensitive mass-production settings.

High production and equipment cost

Synthetic diamond and CBN crystals are grown under pressures and temperatures that exceed geological conditions, pushing capital intensity for reactor vessels well above conventional fused-alumina lines. Single-head CNC grinders configured for diamond wheels require precision spindles and closed-loop coolant systems, raising acquisition costs. While these tools deliver longer life and lower per-part expense, small and midsize job shops in price-sensitive economies still defer upgrades. Vendors are experimenting with leasing models and consumable-credit programs, but adoption remains gated by financing constraints.

Other drivers and restraints analyzed in the detailed report include:

- Growing manufacturing activities in emerging economies

- Additive-manufacturing post-processing requiring super-abrasives

- Stringent regulations on usage of abrasives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic grades commanded 66.35% share of the abrasives market in 2025, underlining user preference for consistent crystal morphology that translates into predictable wear patterns during production runs. Aluminum oxide remains the volume leader; however, silicon carbide addresses non-ferrous machining, while CBN is preferred for hardened steels. Novel nano-polycrystalline diamonds under development by Sumitomo Electric promise superior fracture toughness, positioning the abrasives market to tackle nickel-based super-alloys at lower wheel wear rates. Natural garnet retains a foothold in waterjet and blasting tasks where recyclable bulk media and low free-silica content improve site safety, making it attractive for infrastructure refurbishment projects.

The shift toward synthetic offerings aligns with automated feed systems that demand tight grit distributions, a parameter easier to achieve through engineered production routes. With Asia ramping fused-alumina capacity, supply security is improving, although power-tariff volatility can swing output costs. Manufacturers pursuing eco-labels are investing in renewable-powered arc furnaces and closed-loop water quench circuits to retain share in regulated regions. As a result, the abrasives market continues to upgrade quality benchmarks even in high-volume segments.

Bonded wheels generated 47.55% of 2025 revenue, reflecting their role in cutting, sharpening, and surface-conditioning jobs across automotive, aerospace, and general engineering workshops. Resinoid and vitrified matrices provide thermal stability during deep-cut operations, enabling consistent tolerances on crankshafts and turbine blades where metallurgical integrity is critical. Advances in sol-gel alumina and engineered pore structures improve chip evacuation, permitting higher metal removal rates without risk of burn.

Coated abrasives, while lighter in tonnage, enjoy widespread use in finishing and deburring. Backings ranging from flexible film to fiber discs optimize performance across curved surfaces and hard-to-reach areas. Super-abrasives hold a niche position today, but their double-digit growth underpins the future direction of the abrasives market. Additive manufacturing shops specify diamond pads and CBN mandrels for thin-wall titanium parts where conventional wheels load quickly. Suppliers such as Imerys offer tailor-made fused alumina and sol-gel grains that extend dresser intervals, reinforcing bonded wheels' dominance while bridging performance gaps with super-abrasives.

The Abrasives Market Report is Segmented by Material (Natural Abrasives and Synthetic Abrasives), Type (Bonded Abrasives, Coated Abrasives, and Super Abrasives), Abrasives Grain/Raw Material (Aluminum Oxide, Silicon Carbide, and More), End-User Industry (Metal Manufacturing and Fabrication, Automotive and Aerospace, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific accounted for 55.40% of global purchases in 2025, reflecting China's large machining base and India's accelerated infrastructure build-out. Government incentives for domestic EV battery manufacturing and electronics assembly further stimulate local demand. Japan and South Korea leverage advanced diamond semiconductor research to create new downstream uses for super-abrasives, such as slicing large-area diamond wafers. These factors collectively sustain Asia's leadership position and encourage multinationals to localize mixing and pressing operations.

North America retains strong momentum in aerospace, medical, and additive-manufacturing segments. Regulatory scrutiny on VOCs and particulate emissions propels shifts toward garnet blasting media and water-based coolants, generating product-mix upgrades.

Europe emphasizes sustainability and circular-economy principles, with suppliers like Saint-Gobain implementing recycled-bond systems to curtail carbon intensity. Adoption of super-abrasives is accelerating in Germany's precision engineering clusters, while southern Europe focuses on construction-related blasting and cutting disc consumption. South America, the Middle East, and Africa remain smaller in volume yet register healthy growth as industrialization deepens; Brazil's shipbuilding yards and Gulf petrochemical projects illustrate expanding end-user diversity. Local converting partnerships help global brands penetrate these regions, strengthening global coverage of the abrasives market.

- 3M

- Abrasive Technology

- ARC Abrasives Inc.

- Asahi Diamond Industrial Co. Ltd.

- CUMI

- Deerfos

- Fujimi Incorporated

- Imerys

- Mirka Ltd.

- NORITAKE CO., LIMITED

- Robert Bosch GmbH

- Saint-Gobain

- SAK ABRASIVES LIMITED

- Sia Abrasives Industries AG

- Tyrolit - Schleifmittelwerke Swarovski AG & Co KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Use in the Aerospace and Automotive Industries

- 4.2.2 Growing Metal Manufacturing and Fabrication Industries

- 4.2.3 Growing Manufacturing Activities in Emerging Economies

- 4.2.4 Additive-Manufacturing Post-processing Requiring Super-abrasives

- 4.2.5 Increased Adoption of Precision and CNC Machinery

- 4.3 Market Restraints

- 4.3.1 High production and Equipment Cost

- 4.3.2 Stringent Regulations on Usage of Abrasives

- 4.3.3 Substitution by Alternative Materials or Methods

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Natural Abrasives

- 5.1.2 Synthetic Abrasives

- 5.2 By Type

- 5.2.1 Bonded Abrasives

- 5.2.2 Coated Abrasives

- 5.2.3 Super Abrasives

- 5.3 By Abrasive Grain/Raw Material

- 5.3.1 Aluminum Oxide

- 5.3.2 Silicon Carbide

- 5.3.3 Ceramic and Zirconia Alumina

- 5.3.4 Others (Including Garnet)

- 5.4 By End-user Industry

- 5.4.1 Metal Manufacturing and Fabrication

- 5.4.2 Automotive and Aerospace

- 5.4.3 Electronics and Semiconductors

- 5.4.4 Construction and Infrastructure

- 5.4.5 Medical Devices

- 5.4.6 Oil and Gas

- 5.4.7 Others (Industrial Machinery and Agriculture Equipment)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Malaysia

- 5.5.1.6 Thailand

- 5.5.1.7 Indonesia

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordic Countries

- 5.5.3.7 Turkey

- 5.5.3.8 Russia

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Qatar

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 South Africa

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Abrasive Technology

- 6.4.3 ARC Abrasives Inc.

- 6.4.4 Asahi Diamond Industrial Co. Ltd.

- 6.4.5 CUMI

- 6.4.6 Deerfos

- 6.4.7 Fujimi Incorporated

- 6.4.8 Imerys

- 6.4.9 Mirka Ltd.

- 6.4.10 NORITAKE CO., LIMITED

- 6.4.11 Robert Bosch GmbH

- 6.4.12 Saint-Gobain

- 6.4.13 SAK ABRASIVES LIMITED

- 6.4.14 Sia Abrasives Industries AG

- 6.4.15 Tyrolit - Schleifmittelwerke Swarovski AG & Co KG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growing Use of Automation and Robotics