|

시장보고서

상품코드

1939668

클라우드 AI : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cloud AI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

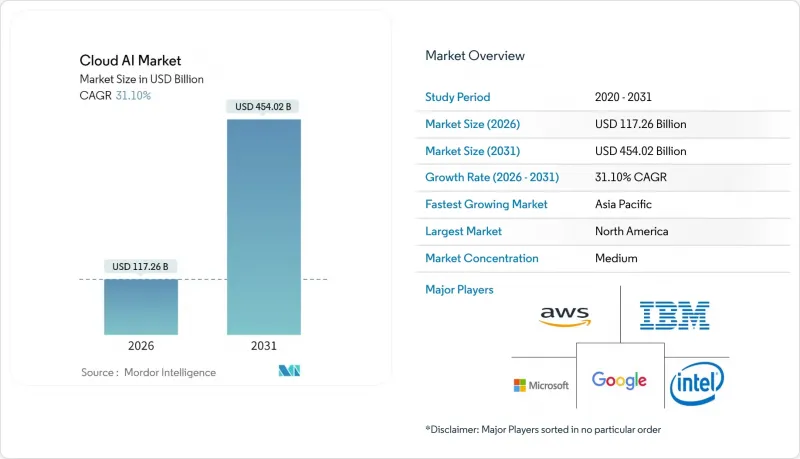

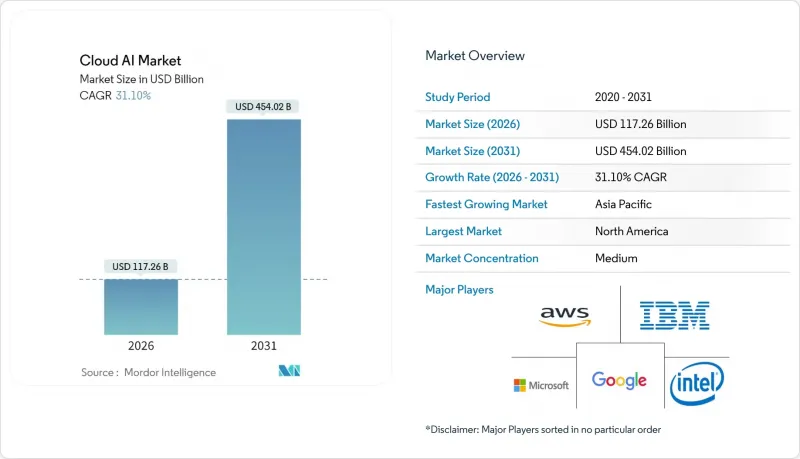

클라우드 AI 시장은 2025년에 894억 3,000만 달러로 평가되며, 2026년 1,172억 6,000만 달러에서 2031년까지 4,540억 2,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 31.10%로 예상됩니다.

마이크로소프트의 OpenAI에 대한 130억 달러 투자, 아마존의 Anthropic에 대한 80억 달러 투자 등 생성형 AI 분야의 제휴는 기업의 처리 능력 확대, 진입장벽 감소, 가치 실현 시간 단축을 촉진하고 있습니다. GPU의 분할 이용 기술을 통한 인프라 비용 절감으로 중견기업을 중심으로 도입이 확대되고 있습니다. 반면, 의료 및 금융 서비스 분야의 산업별 규제는 탄탄한 거버넌스를 입증할 수 있는 프로바이더를 우대하는 경향이 있습니다. 하이퍼스케일러들 사이에서는 특히 고대역폭 메모리공급망 동향이 칩 다양화 전략을 촉진하고 있으며, 탄소 인식이 높은 워크로드 오케스트레이션이 데이터센터 입지 결정에 영향을 미치기 시작했습니다.

세계 클라우드 AI 시장 동향 및 인사이트

AIaaS(AI-as-a-Service) 채택 확대

기업은 자본 집약적인 On-Premise 도입에서 종량제 AI 서비스로 전환하고 있습니다. 마이크로소프트의 AI 사업은 2025 회계연도 2분기 연간 130억 달러의 매출을 달성하며 Azure 성장률에 16% 기여했습니다. AWS Trainium2와 같은 커스텀 실리콘은 30-40%의 가격 대비 성능 향상을 실현하고, 지역 데이터 주권 규제를 충족해야 하는 중견기업의 AI 접근성을 확장하고 있습니다. 유럽과 아시아에서 채택이 두드러지고 있으며, 중견기업의 60%가 2025년까지 지역 특화형 언어 모델을 활용할 것으로 예상하고 있습니다.

늘어나는 빅데이터 양

비정형 데이터는 기업 정보 자산의 80% 이상을 차지하며 실시간 AI 분석 수요를 견인하고 있습니다. 의료 분야에서는 메이요 클리닉이 10만 명의 환자 유전체 기록을 처리하여 질병 조기 발견을 향상시키고 있습니다. 금융 서비스에서는 클라우드 AI를 적용하여 자금세탁방지 스크리닝에서 오감지율을 95% 감소시켰습니다. 엣지와 클라우드의 융합을 통해 제조업체는 IoT 데이터 스트림을 이용한 예측 유지보수를 밀리초 단위의 응답 시간으로 수행할 수 있습니다.

GPU/HBM 공급망 부족 현상 지속

SK하이닉스는 HBM 시장의 70%를 점유하고 있으며, 2025년까지 공급이 타이트한 것으로 보고되어 클라우드 프로바이더에 비용 압박을 가하고 있습니다. AWS는 트레이니엄 커스텀 칩에 대응하고, Oracle은 트레이닝 능력을 유지하기 위해 수천 대의 엔비디아 블랙웰 GPU를 조달하고 있습니다. 메모리 공급 부족으로 DDR5와 VRAM 가격이 급등하고 있는 가운데, 삼성은 AMD와 30억 달러 규모의 HBM3E 공급 계약을 체결했습니다.

부문 분석

2025년, 솔루션은 클라우드 AI 시장의 62.40%를 차지했습니다. 기업은 기존 데브옵스 파이프라인과 통합 가능한 패키지 플랫폼에 집중하여 빠른 도입과 일관된 성능을 보장합니다. 도입이 심화됨에 따라 전환 로드맵과 거버넌스에 대한 전문가의 지도가 필수적이며, 서비스 부문은 CAGR 33.42%를 나타낼 것으로 예측됩니다.

서비스 분야의 성장은 전략 수립, 모델 조정, 운영 관리를 포함한 다년간의 혁신 프로그램을 반영하고 있습니다. 액센츄어 등은 Anthropic-on-AWS 도입을 위해 1,400명의 엔지니어를 재교육하여 기업의 스킬 갭을 직접적으로 해소했습니다. 솔루션과 서비스를 결합한 제공 형태가 확산되면서 조직은 내부 역량을 구축하면서 AI를 빠르게 도입할 수 있게 되었습니다.

BFSI(은행, 금융, 보험) 분야는 부정행위 분석, 로보 어드바이저리 등의 이용 사례로 인해 2025년 클라우드 AI 시장의 28.55%를 차지할 것으로 예측됩니다. 그러나 의료 분야는 AI를 활용한 진단 및 환경 임상 문서화에 힘입어 34.98%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

병원에서는 방사선과 선별진료 및 개별 치료 권고에 거대 언어 모델을 도입하고 있습니다. 2025년 1월 FDA의 지침은 명확한 규제 경로를 제시하여 설비 투자를 촉진하고 있습니다. 제조업 및 소매업도 이에 이어 각각 결함 검출과 재고 최적화에 AI를 활용하고 있습니다.

클라우드 AI 시장 보고서는 유형별(솔루션 및 서비스), 최종사용자 산업별(은행, 금융서비스 및 보험(BFSI), 의료, 자동차 및 모빌리티 등), 도입 모델별(퍼블릭 클라우드, 프라이빗 클라우드 등), 용도별(부정 및 위험 분석, 마케팅 및 개인화 등), 기술별(머신러닝, 생성형 AI 등), 지역별로 분류되어 있습니다. 마케팅-개인화 등), 기술별(머신러닝, 생성형 AI 등), 지역별로 분류되어 있습니다.

지역별 분석

북미는 2025년 클라우드 AI 시장 점유율 40.60%를 유지하며, 하이퍼스케일러 거점 구축과 벤처 자금이 기반이 되고 있습니다. FDA의 AI 디바이스 가이드라인으로 대표되는 규제 명확화가 생명과학 및 금융 분야에서의 도입을 촉진하고 있습니다. 자본 지출에는 아마존의 80억 달러 규모의 Anthropic 투자 및 Microsoft의 지속적인 OpenAI 통합이 포함되며, 지역적 우위를 강화하는 데 기여하고 있습니다.

아시아태평양은 31.88%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. 중국의 2025년 클라우드 지출 전망치 460억 달러와 알리바바의 다년간의 설비 투자 약속이 인프라 확장을 주도하고 있습니다. 일본은 Oracle의 80억 달러 투자 발표와 OpenAI의 첫 인도 태평양 지사를 도쿄에 설립하면서 가속도가 붙었습니다. 인도와 동남아시아는 디지털 공공 인프라 계획과 확장된 개발자 커뮤니티의 혜택을 누리고 있습니다.

유럽은 복잡한 규제 환경 속에서도 꾸준한 성장세를 보이고 있습니다. EU의 AI 법은 조화로운 프레임워크를 제공하고, 인증된 거버넌스를 갖춘 프로바이더에게 우위를 제공합니다. 소버린 클라우드 구상 및 탄소 감축 의무는 하이브리드 아키텍처를 촉진합니다. 중동 및 아프리카 신흥 시장에서는 데이터센터에 대한 국부(國富)의 투자를 배경으로 조기 도입이 진행되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The Cloud AI market was valued at USD 89.43 billion in 2025 and estimated to grow from USD 117.26 billion in 2026 to reach USD 454.02 billion by 2031, at a CAGR of 31.10% during the forecast period (2026-2031).

Generative AI partnerships, such as Microsoft's USD 13 billion commitment to OpenAI and Amazon's USD 8 billion investment in Anthropic, are expanding capacity, lowering entry barriers, and accelerating time-to-value for enterprises. Mid-market adoption is rising as GPU-fractionalization technologies reduce infrastructure costs, while sector-specific regulations in healthcare and financial services favor providers that can demonstrate robust governance. Supply-chain dynamics, notably in high-bandwidth memory, spur chip diversification strategies among hyperscalers, and carbon-aware workload orchestration begins to influence data-center siting decisions.

Global Cloud AI Market Trends and Insights

Growing Adoption of AI-as-a-Service (AIaaS)

Enterprises are shifting from capital-heavy on-premises deployments to pay-as-you-go AI services. Microsoft's AI business reached a USD 13 billion annual run rate in Q2 FY 2025, contributing 16 percentage points to Azure growth. Custom silicon such as AWS Trainium2 delivers 30-40% price-performance gains, broadening AI accessibility for mid-market firms that must meet regional data-sovereignty rules. Uptake is evident across Europe and Asia, where 60% of mid-size enterprises expect regionally trained language models by 2025.

Rising Big-Data Volume

Unstructured data exceeds 80% of enterprise information assets, driving demand for real-time AI analytics. Healthcare use cases include Mayo Clinic processing genomic records from 100,000 patients to improve early disease detection. Financial services apply cloud AI to reduce false positives in anti-money-laundering screening by 95%. Edge-cloud convergence allows manufacturers to perform predictive maintenance on IoT data streams with millisecond response times.

Persistent GPU/HBM Supply-Chain Shortages

SK Hynix controls 70% of the HBM market and reports full allocation through 2025, creating cost pressures for cloud providers. AWS counters with Trainium custom chips, while Oracle procures thousands of NVIDIA Blackwell GPUs to sustain training capacity. Tight memory supply has triggered price spikes in DDR5 and VRAM, with Samsung inking a USD 3 billion HBM3E supply deal with AMD.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Virtual Assistants and GenAI Chatbots

- GenAI GPU-Fractionalization Expanding SME Access

- Lack of Skilled Workforce and Data-Security Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions represented 62.40% of the Cloud AI market in 2025. Enterprises gravitated to packaged platforms that integrate with existing DevOps pipelines, ensuring quick deployment and consistent performance. As adoption deepens, professional guidance becomes essential for migration roadmaps and governance, pushing the Services segment to a forecast 33.42% CAGR.

Services growth reflects multi-year transformation programs that include strategy, model tuning, and managed operations. Firms such as Accenture have retrained 1,400 engineers for Anthropic-on-AWS implementations, directly addressing enterprise skills gaps. Combined solution-service offerings are growing in popularity, enabling organizations to onboard AI quickly while building internal competencies.

BFSI held 28.55% Cloud AI market share in 2025 due to fraud analytics and robo-advisory use cases. However, Healthcare is set to grow at 34.98% CAGR, buoyed by AI-enabled diagnostics and ambient clinical documentation.

Hospitals deploy large language models for radiology triage and personalized treatment recommendations. The FDA's January 2025 guidance provides a clear regulatory path, encouraging capital investment. Manufacturing and retail follow, leveraging AI for defect detection and inventory optimization, respectively.

The Cloud AI Market Report is Segmented by Type (Solution and Service), End-User Vertical (BFSI, Healthcare, Automotive and Mobility, and More), Deployment Model (Public Cloud, Private Cloud, and More), Application (Fraud and Risk Analytics, Marketing and Personalisation, and More), Technology (Machine Learning, Generative AI, and More), and Geography.

Geography Analysis

North America retained 40.60% Cloud AI market share in 2025, anchored by hyperscaler footprints and venture funding. Regulatory clarity, exemplified by the FDA's AI device guidelines, encourages adoption across life-sciences and finance. Capital outlays include Amazon's USD 8 billion Anthropic investment and Microsoft's continued OpenAI integration, reinforcing regional dominance.

Asia Pacific is the fastest-growing territory with 31.88% CAGR. China's projected USD 46 billion cloud spend for 2025, along with Alibaba's multi-year capex commitment, fuels infrastructure expansion. Japan accelerates with Oracle's USD 8 billion pledge and Tokyo's selection for OpenAI's first Indo-Pacific branch. India and Southeast Asia benefit from digital public-infrastructure programs and rising developer communities.

Europe shows steady growth amid complex regulation. The EU AI Act provides a harmonized framework that advantages providers with certified governance. Sovereign cloud initiatives and carbon-reduction mandates encourage hybrid architectures. Emerging markets in the Middle East and Africa witness early uptake, backed by sovereign-wealth investments in data centers.

- Amazon Web Services

- Microsoft Corp.

- Google LLC

- IBM Corp.

- Salesforce Inc.

- NVIDIA Corp.

- Oracle Corp.

- Alibaba Cloud

- SAP SE

- ServiceNow

- Databricks

- Snowflake Inc.

- Hugging Face

- OpenAI LP

- Anthropic PBC

- CoreWeave

- AMD Inc.

- Intel Corp.

- Wipro Ltd.

- Infosys Ltd.

- SoundHound AI Inc.

- Twilio Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising big-data volume

- 4.2.2 Growing adoption of AI-as-a-Service (AIaaS)

- 4.2.3 Increasing demand for virtual assistants and GenAI chatbots

- 4.2.4 GenAI GPU-fractionalization expanding SME access

- 4.2.5 Edge-cloud AI interoperability standards (e.g., ONNX, MEDAL)

- 4.2.6 Carbon-aware workload orchestration incentives

- 4.3 Market Restraints

- 4.3.1 Lack of skilled workforce and data-security concerns

- 4.3.2 Persistent GPU/HBM supply-chain shortages

- 4.3.3 AI datacentre energy constraints and carbon regulations

- 4.3.4 Geopolitical GPU export-control frameworks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Solution

- 5.1.2 Service

- 5.2 By End-user Vertical

- 5.2.1 BFSI

- 5.2.2 Healthcare

- 5.2.3 Automotive and Mobility

- 5.2.4 Retail and E-commerce

- 5.2.5 Government and Public Sector

- 5.2.6 Education

- 5.2.7 Manufacturing

- 5.3 By Deployment Model

- 5.3.1 Public Cloud

- 5.3.2 Private Cloud

- 5.3.3 Hybrid / Multi-cloud

- 5.4 By Application

- 5.4.1 Customer Service and Contact-Centre AI

- 5.4.2 Predictive Maintenance and Asset Ops

- 5.4.3 Fraud and Risk Analytics

- 5.4.4 Marketing and Personalisation

- 5.4.5 Computer-Vision-as-a-Service

- 5.5 By Technology

- 5.5.1 Machine Learning

- 5.5.2 Natural Language Processing

- 5.5.3 Computer Vision

- 5.5.4 Generative AI

- 5.5.5 Reinforcement and Edge AI

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Netherlands

- 5.6.3.7 Russia

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC (Saudi Arabia, UAE, Qatar, etc.)

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Kenya

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services

- 6.4.2 Microsoft Corp.

- 6.4.3 Google LLC

- 6.4.4 IBM Corp.

- 6.4.5 Salesforce Inc.

- 6.4.6 NVIDIA Corp.

- 6.4.7 Oracle Corp.

- 6.4.8 Alibaba Cloud

- 6.4.9 SAP SE

- 6.4.10 ServiceNow

- 6.4.11 Databricks

- 6.4.12 Snowflake Inc.

- 6.4.13 Hugging Face

- 6.4.14 OpenAI LP

- 6.4.15 Anthropic PBC

- 6.4.16 CoreWeave

- 6.4.17 AMD Inc.

- 6.4.18 Intel Corp.

- 6.4.19 Wipro Ltd.

- 6.4.20 Infosys Ltd.

- 6.4.21 SoundHound AI Inc.

- 6.4.22 Twilio Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment