|

시장보고서

상품코드

1939669

음성 인식 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Voice Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

세계의 음성 인식 시장은 2025년에 183억 9,000만 달러로 평가되며, 2026년 224억 9,000만 달러에서 2031년까지 617억 1,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 22.38%로 예상됩니다.

시장 확대는 엣지 인공지능(AI) 칩셋의 급속한 보급, 긴급 통신망 현대화를 위한 규제 압력, 고객 인증을 위한 음성 생체인식 기술로의 기업 전환 등 세 가지 요인이 동시에 작용하고 있음을 반영하고 있습니다. 소프트웨어 중심 아키텍처가 현재 주류가 되고 있으며, 시장 가치의 70.7%가 소프트웨어 개발 키트(SDK)와 애플리케이션 프로그래밍 인터페이스(API) 플랫폼에 집중되어 있습니다. 한편, 2024년 도입 사례의 62.1%는 클라우드 구축으로 인한 것입니다. 지역별로는 다국어 인터페이스 수요와 강력한 칩 제조 생태계를 바탕으로 아시아가 2024년 32.5%의 시장 점유율로 1위를 차지했습니다. 음성 인식 기술은 81.2%의 점유율로 주요 기술 기반을 유지했으나, 디바이스 내장형 프로세싱이 25%의 가장 빠른 CAGR을 달성하며 클라우드 전용 설계에서 하이브리드 또는 완전 로컬 추론 엔진으로의 결정적인 전환을 보여주었습니다.

세계 음성 인식 시장 동향 및 인사이트

아시아 전역에 걸쳐 엣지 디바이스용 음성 AI 칩이 급증

Chipintelli의 14가지 오프라인 AI 음성 칩 출시와 MediaTek의 MR Breeze ASR 25 모델은 지역 언어에 최적화된 전용 실리콘에 대한 투자가 가속화되고 있음을 보여줍니다. 로컬라이제이션은 저 지연을 실현하고, 클라우드 스트리밍에 따른 프라이버시 우려를 해소하며, 기존 북미 하이퍼스케일러에 의존하던 국내 공급망을 정착시킬 수 있습니다. 아시아 반도체 기업은 이러한 이점을 활용하여 인도네시아, 베트남, 인도 등 시장에서 코드 스위칭을 처리하는 턴키 음성 스택을 장치 OEM에 제공함으로써 엣지 추론 혁신 분야에서 이 지역의 리더십을 강화하고 있습니다.

북미의 음성 대응 911 및 긴급 신고 시스템 규제 강화

미국 연방통신위원회(FCC)의 새로운 규정에 따라 미국 통신사업자들은 911 신고를 IP 기반 세션 개시 프로토콜(SIP)을 통해 라우팅해야 하며, 반경 165미터 이내에서 90%의 신뢰도로 오경로를 줄이고, 실시간 텍스트 및 비디오를 지원해야 합니다. 의무화되었습니다. 긴급 서비스 분야에 집중하는 음성 인식 업체는 전국 및 지역 사업자의 컴플라이언스 기한이 6-12개월 이내로 설정되어 있으며, 예측 가능한 매출 성장이 예상됩니다. 이 의무화는 유럽의 공공안전 네트워크에도 영향을 미칠 가능성이 높은 템플릿이 될 것이며, 음성 분석의 잠재적 수요를 확대할 것입니다. 음성분석은 전사된 음성과 메타데이터로 인시던트 데이터를 보강하는 기술입니다.

아프리카의 악센트와 방언 인식의 문제가 보급을 가로막고 있습니다.

아프리카 93개 악센트를 대상으로 한 시험에서 의료 관련 기관 오인식률이 여전히 25-34% 개선이 필요한 것으로 나타났습니다. NaijaVoices의 1,800시간 분량의 데이터세트는 Whisper 모델의 단어 오인식률을 75.86% 감소시켰지만, 문화적으로 풍부한 말뭉치 구축 비용과 복잡성으로 인해 상용화가 지연되고 있습니다. Intron Health의 160만 달러의 시드 라운드는 투자자들이 이 문제를 인식하고 있다는 것을 보여주는 동시에, 현지화된 모델 훈련에 대한 자본 수요가 높다는 것을 보여줍니다.

부문 분석

2025년에는 클라우드 제공이 전 세계 매출의 61.60%를 차지할 것으로 예상되며, 기업이 신속한 배포, 지속적인 모델 업데이트, 광범위한 언어 지원을 우선시함에 따라 이 비중은 더욱 확대될 것으로 전망됩니다. 금융기관과 의료 서비스 프로바이더들은 원시 데이터는 On-Premise에 보관하고 모델 훈련 결과를 클라우드에서 공유하는 하이브리드 아키텍처를 선택하는 경향이 증가하고 있습니다. 이 접근 방식은 컴플라이언스 준수와 집약적 학습을 통한 성능 향상 사이의 균형을 유지합니다. 따라서 On-Premise 도입은 주권 데이터 요구 사항에서 여전히 중요하며, 2031년까지 이 부문이 두 자릿수 성장을 유지할 것으로 예측됩니다.

고가용성 음성 엔드포인트에 대한 수요가 증가함에 따라 하이퍼스케일러는 턴키 API 제공을 추진하고 있습니다. 그 결과, 중견기업의 총소유비용(TCO)이 낮아지고, 독립 개발자의 진입장벽이 완화되었습니다. 이에 따라 음성 인식 시장의 채택 대상이 소비자 기기에서 프로세스 자동화, 물류, 현장 서비스 업무 흐름으로 확대되고 있습니다. 클라우드 구현의 음성 인식 시장 규모는 신규 워크로드 및 기존 도입 확대를 반영하여 2031년까지 385억 달러에 육박할 것으로 예측됩니다.

소프트웨어 플랫폼은 2025년 전 세계 지출의 70.05%를 차지할 것으로 예상되며, 이 결정적인 차이는 업계가 독점 하드웨어에서 모듈식 및 개발자 친화적인 툴로 전환하는 데 결정적인 역할을 하고 있습니다. RESTful API와 사전 구축된 언어 모델을 사용할 수 있으므로 많은 이용 사례에서 맞춤형 실리콘이 필요하지 않습니다. 서비스 분야는 규모는 작지만 기업의 도메인 튜닝, 악센트 적응, 보안 컴플라이언스 위탁이 증가하면서 23.20%의 연평균 복합 성장률(CAGR)로 확대되고 있습니다.

하드웨어는 엣지 레이턴시, 오프라인 가용성, 음향 빔포밍이 중요한 분야(자동차 인포테인먼트, 산업용 헤드마운트 디스플레이 등)에서 여전히 존재감을 발휘합니다. 그러나 많은 신규 시장 진출기업이 PaaS(Platform as a Service) 솔루션을 이용하여 하드웨어를 회피하고 있으며, 수평적 소프트웨어 프로바이더와 수직적 통합형 하드웨어 전문 기업 간의 격차가 확대되고 있는 것으로 나타났습니다.

음성 인식 시장은 도입 형태(클라우드/On-Premise), 구성요소(소프트웨어/SDK, 하드웨어, 서비스), 기술(음성 인식, 음성 생체인식, 엣지 음성 AI), 디바이스 유형(스마트폰, 스마트 스피커, 자동차, 웨어러블, POS), 용도(인증, 음성 검색 등), 최종사용자 산업별(자동차, BFSI(은행, 금융, 보험), 기타), 지역별로 분류됩니다. 등), 최종사용자 산업별(자동차, 은행, 금융서비스 및 보험(BFS), 기타), 지역별로 분류됩니다. 시장 예측은 금액 기준(USD)으로 제시됩니다.

지역별 분석

아시아 지역은 2025년 매출의 32.10%를 차지할 것으로 예상되며, 이는 아시아 지역의 반도체 생산 능력과 언어의 다양성을 반영합니다. 국내 정책이 AI 보급을 촉진하고 있으며, 일본의 동남아시아 언어 모델에 대한 자금 지원 구상이 그 한 예입니다. 북미는 여전히 기술 초기 도입의 거점이지만, 적극적인 현지화와 저비용 장치로 인해 아시아에 점유율을 내주었습니다. 유럽은 자동차 및 BFSI 분야의 도입 확대로 꾸준히 성장하고 있습니다.

중동은 22.60%의 가장 빠른 CAGR을 보이고 있는데, 이는 걸프 지역 국가들의 스마트 시티 계획에 대화형 키오스크가 시민 서비스 인프라에 통합되어 있기 때문입니다. 남미는 E-Commerce에서 음성 검색과 은행 인증의 보급으로 10%대 중반의 성장률을 기록하고 있습니다. 아프리카는 악센트의 다양성으로 인해 범용 모델 구축이 복잡해져 뒤쳐져 있지만, 기부금에 의한 언어 프로젝트와 통신 인프라 업그레이드로 인해 2027년 이후 잠재적 수요가 풀릴 가능성이 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

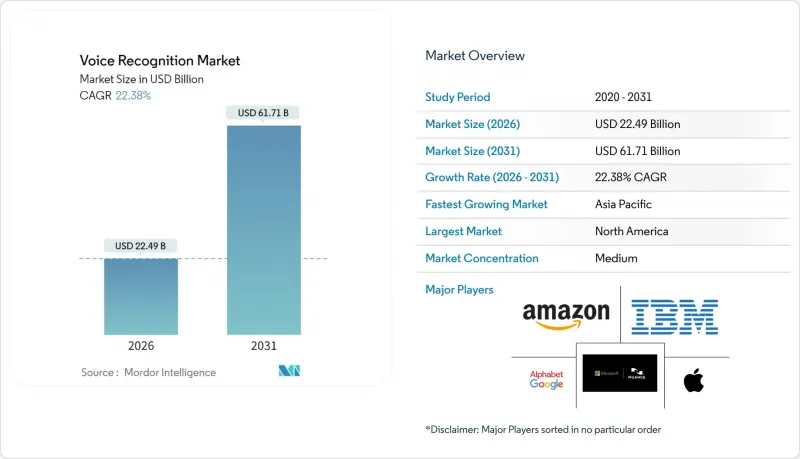

KSA 26.03.05The global voice recognition market was valued at USD 18.39 billion in 2025 and estimated to grow from USD 22.49 billion in 2026 to reach USD 61.71 billion by 2031, at a CAGR of 22.38% during the forecast period (2026-2031).

Market expansion reflects three concurrent forces: the rapid roll-out of edge artificial intelligence (AI) chipsets, regulatory pressure for modernising emergency communications networks, and enterprise migration to voice biometrics for customer authentication. Software-centric architectures now dominate because 70.7% of market value sits in software development kits and application-programming-interface platforms, while cloud deployment accounts for 62.1% of implementations in 2024. Regionally, Asia led with 32.5% market share in 2024 on the back of multilingual interface demand and strong chip manufacturing ecosystems; speech recognition technology remained the principal technology pillar with 81.2% share, yet embedded on-device processing delivered the fastest 25% CAGR, showing a decisive shift from cloud-only designs to hybrid or fully local inference engines.

Global Voice Recognition Market Trends and Insights

Explosion of Voice-AI Chips in Edge Devices across Asia

The release of 14 offline AI speech chips by Chipintelli and MediaTek's MR Breeze ASR 25 model signal escalating investment in specialised silicon optimised for regional languages. Localisation delivers lower latency, resolves privacy concerns tied to cloud streaming, and entrenches domestic supply chains that historically depended on North American hyperscalers. Asian semiconductor firms leverage this advantage to offer device OEMs turnkey voice stacks that handle code-switching in markets such as Indonesia, Vietnam, and India, reinforcing the region's leadership in edge inference innovation.

Regulatory Push for Voice-Enabled 911 and Emergency Dispatch Upgrades in North America

New FCC rules obligate US carriers to route 911 calls via IP-based Session Initiation Protocol, cut misrouting below a 165-meter radius at 90% confidence, and support real-time text and video. Voice recognition vendors positioned around emergency services gain a predictable revenue ramp because compliance deadlines fall within a 6-12-month horizon for nationwide and regional operators. The mandate creates a template likely to influence European public safety networks, expanding total addressable demand for voice analytics that enrich incident data with transcribed speech and metadata.

Accent and Dialect Recognition Gaps Limiting Adoption in Africa

Tests across 93 African accents showed medical entity error rates that still required 25-34% refinement via accent-specific fine-tuning. NaijaVoices' 1,800-hour dataset cut word-error rates for Whisper models by 75.86%, but the cost and complexity of curating culturally rich corpora slow commercial roll-outs. Intron Health's USD 1.6 million seed round underlines investor recognition of the problem, yet it also highlights the capital demands of localised model training.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Shift to Embedded Voice OS for Cockpit Personalisation

- BFSI Adoption of Voice Biometrics to Replace Knowledge-Based Authentication in Europe

- Privacy Regulations (GDPR, India DPDP) Restricting Cloud Voice-Data Retention

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud delivery generated 61.60% of global revenue in 2025, and that share is projected to widen as enterprises prioritise rapid rollout, continuous model updates, and broad language coverage. Financial institutions and healthcare providers increasingly select hybrid architectures that keep raw recordings on premises but pool model-training insights in the cloud. The approach balances compliance with the performance gains of aggregated learning. On-premise deployments therefore remain relevant for sovereign-data mandates, explaining why the segment still posts double-digit growth through 2031.

Demand for high-availability voice endpoints has pushed hyperscalers to expose turnkey APIs. Consequently, total cost of ownership falls for mid-sized enterprises, and barriers to entry lower for independent developers. The result is a wider application funnel for voice recognition market adoption, extending beyond consumer devices into process automation, logistics, and field-service workflows. The voice recognition market size for cloud implementations is set to approach USD 38.5 billion by 2031, reflecting both new workloads and expansion of existing deployments.

Software platforms captured 70.05% of global spend in 2025, a decisive margin that underpins the industry's pivot from proprietary hardware to modular, developer-friendly tooling. The availability of RESTful APIs and pre-built language models removes the need for bespoke silicon in many use cases. Services, although representing a smaller base, rise at 23.20% CAGR as enterprises engage specialist vendors for domain tuning, accent adaptation, and security compliance.

Hardware maintains relevance where edge latency, offline availability, or acoustic beam-forming matter, such as in automotive infotainment or industrial head-mounted displays. Yet most new entrants bypass hardware by consuming platform-as-a-service offerings, illustrating an expanding gap between horizontally oriented software providers and vertically integrated hardware specialists.

Voice Recognition Market is Segmented by Deployment (Cloud, On-Premise), Component (Software/SDK, Hardware, Services), Technology (Speech Recognition, Voice Biometrics, Edge Voice AI), Device Type (Smartphones, Smart Speakers, Automotive, Wearables, POS), Application (Authentication, Voice Search, and More), End-User Vertical (Automotive, BFSI, and Morel), and by Geography. Market Forecasts in Value (USD).

Geography Analysis

Asia generated 32.10% of 2025 turnover, reflecting the region's semiconductor capacity and linguistic diversity. Domestic policy supports AI acceleration; Japan's initiative to fund Southeast Asian language models is one example. North America remains technology's early-adopter hub but ceded share to Asia because of aggressive localisation and lower device costs. Europe grew steadily, influenced by automotive and BFSI thematic adoption.

The Middle East exhibits the quickest 22.60% CAGR as Gulf smart-city programmes embed conversational kiosks in citizen-services infrastructure. South America records mid-teens growth from e-commerce voice search and banking authentication. Africa faces a lag because accent diversity complicates universal models; however, donor-funded language projects and telecom upgrades may unlock latent demand from 2027 onward.

- Apple Inc.

- Alphabet Inc. (Google LLC)

- Amazon.com Inc.

- Nuance Communications Inc. (Microsoft)

- IBM Corporation

- Baidu Inc.

- Samsung Electronics Co. Ltd.

- SoundHound AI Inc.

- iFLYTEK Co. Ltd.

- Sensory Inc.

- Cerence Inc.

- Verint Systems Inc.

- NICE Ltd.

- ElevenLabs

- Auraya Systems Pty Ltd.

- Intron Health

- PlayAI

- Mobvoi Information Technology Co. Ltd.

- Deepgram Inc.

- AssemblyAI Inc.

- Speechmatics Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion of Voice-AI Chips in Edge Devices across Asia

- 4.2.2 Regulatory Push for Voice-Enabled 911 and Emergency Dispatch Upgrades in North America

- 4.2.3 Automotive OEM Shift to Embedded Voice OS for Cockpit Personalisation

- 4.2.4 BFSI Adoption of Voice Biometrics to Replace Knowledge-Based Authentication in Europe

- 4.2.5 Rapid Proliferation of Voice Commerce in Smart-Speaker Centric Households

- 4.2.6 Growth of Multilingual Voice UX Demand in Emerging APAC Markets

- 4.3 Market Restraints

- 4.3.1 Accent and Dialect Recognition Gaps Limiting Adoption in Africa

- 4.3.2 Privacy Regulations (GDPR, India DPDP) Restricting Cloud Voice Data Retention

- 4.3.3 High Cost of Annotated Domain-Specific Speech Corpora

- 4.3.4 Persistent Accuracy Lags in Noisy Industrial Environments

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Component

- 5.2.1 Software/SDK

- 5.2.2 Hardware (ASIC, DSP, Microphone Arrays)

- 5.2.3 Services (Managed and Professional)

- 5.3 By Technology

- 5.3.1 Speech Recognition

- 5.3.2 Speaker/Voice Biometrics

- 5.3.3 Embedded/Edge Voice AI

- 5.4 By Device Type

- 5.4.1 Smartphones and Tablets

- 5.4.2 Smart Speakers and Displays

- 5.4.3 Automotive Infotainment and Telematics

- 5.4.4 Wearables (TWS, Smart-watch, AR/VR)

- 5.4.5 Commercial Kiosks and POS

- 5.5 By Application

- 5.5.1 Authentication and Security

- 5.5.2 Voice Search and Command

- 5.5.3 Transcription and Captioning

- 5.5.4 Virtual Assistants and Chatbots

- 5.5.5 Medical Documentation

- 5.6 By End-user Vertical

- 5.6.1 Automotive

- 5.6.2 Banking and Financial Services

- 5.6.3 Telecommunications

- 5.6.4 Healthcare Providers

- 5.6.5 Government and Defence

- 5.6.6 Consumer Electronics

- 5.6.7 Retail and E-commerce

- 5.6.8 Industrial and Manufacturing

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 ASEAN

- 5.7.4.6 Australia

- 5.7.4.7 New Zealand

- 5.7.4.8 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 GCC

- 5.7.5.1.2 Turkey

- 5.7.5.1.3 Israel

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Egypt

- 5.7.5.2.4 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 Apple Inc.

- 6.4.2 Alphabet Inc. (Google LLC)

- 6.4.3 Amazon.com Inc.

- 6.4.4 Nuance Communications Inc. (Microsoft)

- 6.4.5 IBM Corporation

- 6.4.6 Baidu Inc.

- 6.4.7 Samsung Electronics Co. Ltd.

- 6.4.8 SoundHound AI Inc.

- 6.4.9 iFLYTEK Co. Ltd.

- 6.4.10 Sensory Inc.

- 6.4.11 Cerence Inc.

- 6.4.12 Verint Systems Inc.

- 6.4.13 NICE Ltd.

- 6.4.14 ElevenLabs

- 6.4.15 Auraya Systems Pty Ltd.

- 6.4.16 Intron Health

- 6.4.17 PlayAI

- 6.4.18 Mobvoi Information Technology Co. Ltd.

- 6.4.19 Deepgram Inc.

- 6.4.20 AssemblyAI Inc.

- 6.4.21 Speechmatics Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment