|

시장보고서

상품코드

1939670

헬스케어용 반도체 애플리케이션 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Semiconductor Applications In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

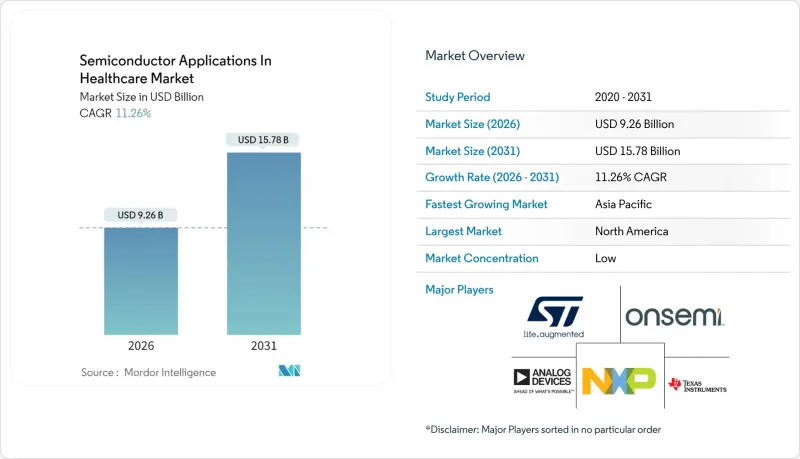

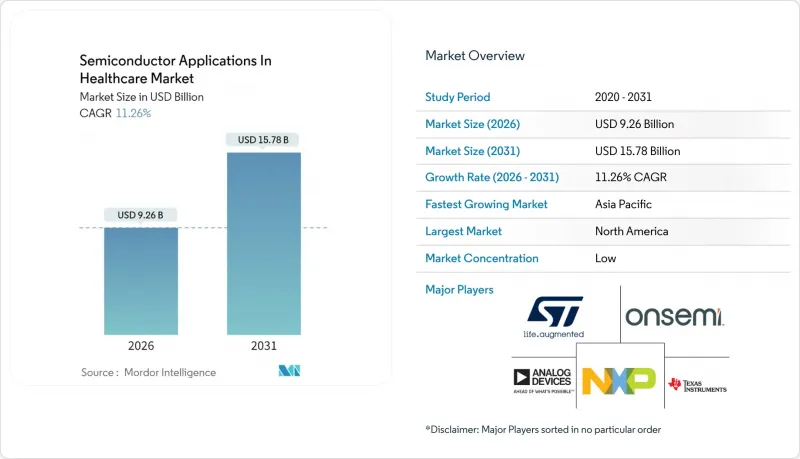

2026년 헬스케어용 반도체 애플리케이션 시장 규모는 92억 6,000만 달러로 추정되며, 2025년 83억 2,000만 달러에서 성장이 전망됩니다.

2031년의 예측에서는 157억 8,000만 달러에 달하며, 2026-2031년에 CAGR 11.26%로 확대할 전망입니다.

이러한 급속한 성장은 병원의 인공지능(AI) 영상 진단, 임베디드 바이오 MEMS, 중앙 집중식 검사실에서 검사를 분산시키는 랩온칩 진단 기술에 대한 투자에 기인합니다. 또한 초저전력 시스템온칩(SoC)과 보안 요소 디바이스가 네트워크 엣지에서 환자 데이터를 수집, 처리, 보호하는 '커넥티드 케어'로의 결정적인 전환도 성장 요인입니다. 임상의들이 오랜 기간 중정적으로 작동하는 인증된 하드웨어를 찾는 가운데, 첨단 패키징 기술, 생체적합성 소재, 장기적인 제품 지원을 결합할 수 있는 칩 제조업체가 범용 벤더를 능가하는 성장세를 보일 것으로 예측됩니다. 마지막으로 각국의 반도체 장려 프로그램은 공급 기반을 재구축하고, 의료용 인증 실리콘의 리드타임 단축과 단일 지역 생산 거점에 대한 의존도 감소를 촉진하고 있습니다.

세계 헬스케어 분야 반도체 용도 시장 동향 및 인사이트

커넥티드 의료기기와 IoT의 확산

세계 병원 및 재택치료 생태계에서는 스마트 모니터, 주입 펌프, 환경 지원형 생활 툴이 도입되어 활력 징후를 지속적으로 기록하고 있습니다. 이러한 시스템은 블루투스 LE, Wi-Fi 6 또는 5G 무선 및 센서 인터페이스, 암호화 스토리지를 통합하고 슬립 사이클 동안 마이크로와트 단위의 전력 소비로 작동하는 무선 SoC에 의존합니다. 긴 수명의 코인 셀 배터리 구동은 에너지수확기술 지원 PMIC에 대한 수요를 촉진하고, 공급업체들이 무선 스택과 전력 도메인을 함께 최적화하도록 유도하고 있습니다. 이 장치군에는 임상의가 펌웨어 업데이트를 인증할 수 있는 하드웨어 루트 오브 트러스트(Root of Trust) 모듈도 내장되어 있습니다. 성과 기반 보상 체계가 성과 기반 모델로 전환됨에 따라 프로바이더들은 지연과 네트워크 혼잡을 줄이는 엣지 프로세싱 데이터 채택을 늘리고 있으며, 이로 인해 기기당 실리콘 함량이 확대되고 있습니다.

AI 탑재 이미징 시스템 보급 확대

영상의학과에서는 사후적인 영상 판독에서 콘솔에서 제공되는 실시간 의사결정 지원으로 전환하고 있습니다. 광자 계수형 CT 스캐너는 더 높은 스펙트럼 해상도를 제공하므로 원시 데이터의 양이 증가하고, 이미지 재구성 및 딥러닝 알고리즘을 몇 밀리초 만에 실행할 수 있는 온보드 가속기 어레이가 필요합니다. 반도체 설계자들은 2.5D 인터포저 내에서 고 대역폭 HBM 스택과 저 형상 로직 다이를 결합하여 소형 실적를 유지하면서 처리량을 향상시키고 있습니다. 이와 함께 갈륨비소나 페로브스카이트 소재를 사용한 화합물 반도체 검출기는 더 낮은 방사선량으로 더 선명한 콘트라스트를 구현하여 전용 아날로그 프론트엔드와 고전압 드라이버에 대한 백엔드 수요를 창출하고 있습니다.

레거시 의료기기의 높은 업그레이드 비용

많은 병원들은 10년 전에 구입한 MRI 스캐너, 침대 옆 모니터, 주입 펌프 등을 여전히 가동하고 있으며, 반도체 집약적인 업그레이드에 투자할 수 있는 자본은 한정되어 있습니다. 따라서 OEM 업체들은 신규 시스템 전체가 아닌 기존 장비에 교체 가능한 보드를 출시할 수밖에 없어 차세대 AI 프로세서의 보급이 늦어지고 있습니다. 자금 부족은 상환이 지연되고 조달 주기가 유럽과 미국의 평균을 크게 초과하는 소규모 민간 클리닉과 신흥 경제국에서 가장 심각합니다. 이러한 장벽을 극복하기 위해 공급업체들은 실리콘 비용을 다년간의 유지보수 계약으로 상각하는 금융 패키지와 사용량 기반 서비스 모델을 결합하여 제공합니다.

부문 분석

의료 영상 진단은 2025년 매출의 35.22%를 차지할 것으로 예상되며, 헬스케어 분야 반도체 용도 시장의 핵심 가치 창출원으로서의 역할을 강조했습니다. 이 분야에서는 컴퓨터단층촬영(CT), 자기공명영상 진단(MRI), 초음파 콘솔에 고해상도 디지타이저, 필드프로그래머블게이트어레이(FPGA), AI 가속기를 통합한 멀티다이 모듈이 채택되고 있습니다. 스펙트럼 CT 및 광자 계수 CT로의 전환으로 인해 처리 수요가 증가하고 있으며, OEM 업체들은 4GB/s 이상의 데이터 속도를 관리할 수 있는 HBM 지원 SoC의 채택을 추진하고 있습니다. 한편, 휴대용 초음파 시스템은 단일 칩 통합을 활용하여 응급 현장에서의 현장 진단을 실현합니다. 예측 모델에 따르면 의료 영상 분야는 2031년까지 헬스케어 반도체 용도 시장에서 12.06%의 연평균 복합 성장률(CAGR)을 유지할 것으로 예측됩니다.

보완적인 성장은 소비자용 의료용 전자기기 분야에서도 나타나고 있습니다. 연결형 혈압계 커프, 혈당 모니터, 심전도 패치에는 보안 무선 기능과 저전력 마이크로컨트롤러가 통합되어 있습니다. 진단용 환자 모니터링 및 치료 장비도 꾸준히 확대되고 있으며, 병원은 네트워크화된 바이탈 사인 허브를 표준화하고 데이터를 전자 건강 기록으로 스트리밍하고 있습니다. 의료기기는 안정적이고 역동성이 부족한 카테고리로, 정확성과 수명을 중시하는 검증된 65nm 이상의 아날로그 노드를 채택한 실험실 자동화에 주력하고 있습니다.

지역별 분석

북미는 2025년 32.74%의 매출 점유율을 유지하며, 고정밀진단 장비에 대한 보험사 환급이 가능한 성숙한 의료 보험자 생태계에 힘입어 선도적인 위치를 유지할 것으로 예측됩니다. 연방정부의 인센티브로 국내 아날로그 혼합 신호 웨이퍼 생산이 가속화되고 있으며, FDA 승인 부품의 리드타임이 단축되고 있습니다. 캘리포니아, 매사추세츠, 텍사스를 중심으로 한 학계와 의료기관의 협력으로 신경조절 및 이식형 센서의 시제품이 지속적으로 공급되고 있으며, 빠르게 임상시험으로 전환되고 있습니다. 그러나 특정 고대역폭 AI 가속기에 대한 수출 규제 고려사항은 전 세계에 이미징 콘솔을 배송하려는 다국적 OEM(Original Equipment Manufacturer)의 계획을 복잡하게 만들고 있습니다.

아시아태평양은 13.08%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장세를 보이고 있으며, 중국, 인도, 동남아시아의 병원 인프라에 대한 대규모 공공 투자가 이를 주도하고 있습니다. 심천에 위치한 팹은 의료용 ASIC 생산을 전문으로 하며, 턴키 방식의 ISO 13485 준수 조립 서비스를 제공함으로써 지역내 의료기기 스타트업 기업의 설계 주기 단축을 실현하고 있습니다. 인도에서는 정부 주도의 디지털 헬스 캠페인으로 인해 블루투스 LE와 저전력 RISC-V 코어를 통합한 비용 최적화 SoC에 대한 수요가 증가하고 있으며, 이를 통해 지역 진료소에서 생체신호 수집이 가능해졌습니다. 일본 제조업체는 정밀도와 재료 혁신을 중시하고, 최근 8인치 SiC 웨이퍼로의 전환은 MRI 그라데이션 증폭기내 고전압 전원 공급을 지원하고 있습니다.

유럽은 의료기기 규정(MDR)을 통해 부품의 추적성 및 시판 후 조사 요건을 규정하는 등 강력한 규제 발신력을 유지하고 있습니다. EU 칩법에서는 임박한 PFAS 규제에 대응하기 위해 무용제 다이애치 화학물질을 채택하는 포장 공장에 대한 보조금을 지정하고 있습니다. 범유럽 구매 컨소시엄은 공급업체의 재생에너지 사용 실적을 중시하는 경향이 강해지고 있으며, 칩 제조업체에 탄소 감축 로드맵을 문서화할 것을 촉구하고 있습니다. 전체 성장률은 아시아태평양에 비해 뒤쳐져 있지만, 유럽이 지속가능성과 데이터 보호 컴플라이언스를 중시하는 만큼 보안 처리 및 암호화 실리콘에 대한 고부가가치 주문이 꾸준히 발생하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The semiconductor applications in the healthcare market size in 2026 is estimated at USD 9.26 billion, growing from 2025 value of USD 8.32 billion with 2031 projections showing USD 15.78 billion, growing at 11.26% CAGR over 2026-2031.

Rapid gains stem from hospital investments in artificial-intelligence imaging, implantable bio-MEMS, and lab-on-chip diagnostics that shift testing away from centralized laboratories. Growth also reflects a decisive push toward connected care, where ultra-low-power system-on-chips (SoCs) and secure element devices capture, process, and protect patient data at the network edge. Chipmakers able to combine advanced packaging, biocompatible materials, and long-lifecycle product support are positioned to outpace general-purpose vendors as clinicians demand certified hardware that runs reliably for years. Finally, national semiconductor incentive programs are reshaping the supply base, shortening lead times for medically validated silicon and reducing dependence on single-region production hubs.

Global Semiconductor Applications In Healthcare Market Trends and Insights

Proliferation of Connected Medical Devices and IoT

Global hospital and home-care ecosystems now deploy smart monitors, infusion pumps, and ambient-assisted living tools that continuously log vital signs. These systems rely on wireless SoCs that merge Bluetooth LE, Wi-Fi 6, or 5G radios with sensor interfaces and encrypted storage while consuming microwatts during sleep cycles. Long-life coin-cell operation reinforces demand for energy-harvesting PMICs, prompting suppliers to co-optimize radio stacks and power domains. Device fleets also incorporate hardware root-of-trust modules, allowing clinicians to authenticate firmware updates. As reimbursement frameworks shift toward outcome-based models, providers are increasingly favoring edge-processed data that reduces latency and network congestion, thereby expanding the addressable silicon content per device.

Growing Adoption of AI-Enabled Imaging Systems

Radiology suites are transitioning from retrospective image reads to real-time decision support delivered on-console. Photon-counting CT scanners offer higher spectral resolution, thereby increasing the raw data volume and necessitating on-board accelerator arrays capable of executing image reconstruction and deep-learning algorithms in milliseconds. Semiconductor designers address this by pairing high-bandwidth HBM stacks with low-geometry logic dies within 2.5-D interposers, thereby boosting throughput while maintaining compact footprints. In parallel, compound-semiconductor detectors using gallium arsenide or perovskite materials deliver sharper contrast at lower radiation doses, creating back-end demand for specialized analog front-ends and high-voltage drivers.

High Upgrade Costs for Legacy Medical Equipment

Many hospitals continue operating MRI scanners, bedside monitors, and infusion pumps purchased a decade ago, leaving limited capital for semiconductor-intensive upgrades. Original equipment manufacturers (OEMs), therefore, face pressure to release drop-in boards rather than entirely new systems, which slows the penetration of next-generation AI processors. Funding gaps are most acute in small private clinics and emerging economies, where reimbursements lag and procurement cycles extend well beyond Western averages. To counter the barrier, suppliers bundle financing packages and usage-based service models that amortize silicon costs over multi-year maintenance contracts.

Other drivers and restraints analyzed in the detailed report include:

- Rising Chronic-Disease Burden Driving Remote Monitoring

- Government Incentives for Healthcare-Specific Fabs

- Stringent Regulatory Approval Cycles for Chip Changes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medical imaging contributed 35.22% of 2025 revenue, underscoring its role as the core value generator for the semiconductor applications in the healthcare market. Within this arena, computed tomography, magnetic resonance imaging, and ultrasound consoles incorporate multi-die modules that combine high-resolution digitizers, field-programmable gate arrays, and AI accelerators. The migration toward spectral and photon-counting CT elevates processing demand, prompting OEMs to specify HBM-enabled SoCs that manage data rates exceeding 4 GB/s. Meanwhile, handheld ultrasound systems leverage single-chip integration to deliver point-of-care diagnostics in emergency settings. Forecast models indicate medical imaging will sustain a 12.06% CAGR in the semiconductor applications in the healthcare market by 2031.

Complementary growth stems from consumer medical electronics, where connected blood-pressure cuffs, glucose monitors, and ECG patches integrate secure radios and power-efficient microcontrollers. Diagnostic patient monitoring and therapy equipment also expand steadily as hospitals standardize on networked vital-sign hubs that stream data into electronic health records. Medical instruments remain a stable but less dynamic category, concentrating on laboratory automation that favors tried-and-tested 65 nm and above analog nodes for precision and longevity.

The Semiconductor Applications in Healthcare Market Report is Segmented by Application (Medical Imaging, Consumer Medical Electronics, Medical Instruments, and More), Component (Integrated Circuits, Optoelectronics, Sensors, and More), Technology Node (Less Than 28 Nm, 28-65 Nm, Above 65 Nm), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains its leadership position, with 32.74% revenue in 2025, driven by a mature healthcare payer ecosystem that can reimburse premium diagnostics. Federal incentives have accelerated domestic analog and mixed-signal wafer starts, reducing lead times for FDA-cleared components. Academic-medical partnerships centered in California, Massachusetts, and Texas sustain a continuous pipeline of neuromodulation and implantable sensor prototypes that transition swiftly into clinical trials. However, export-control considerations on certain high-bandwidth AI accelerators introduce planning complexity for multinational OEMs shipping imaging consoles worldwide.

The Asia-Pacific region posts the fastest trajectory at a 13.08% CAGR, fueled by large-scale public investments in hospital infrastructure across China, India, and Southeast Asia. Shenzhen-based fabs specializing in medical-grade ASIC production now offer turnkey ISO 13485 assembly services, shortening design cycles for regional device startups. In India, government digital-health campaigns are spurring demand for cost-optimized SoCs that integrate Bluetooth LE and power-efficient RISC-V cores, enabling vital-sign collection in rural clinics. Japanese manufacturers emphasize precision and materials innovation; recent transitions to 8-inch SiC wafers support high-voltage supplies inside MRI gradient amplifiers.

Europe maintains a strong regulatory voice through its Medical Device Regulation, which shapes the requirements for component traceability and post-market surveillance. The EU Chips Act earmarks grants for packaging plants that adopt solvent-free die-attach chemistries to comply with impending PFAS restrictions. Pan-European purchasing consortiums increasingly weigh suppliers' renewable-energy footprints, encouraging chipmakers to document carbon-reduction roadmaps. While overall growth trails that of the Asia-Pacific region, Europe's emphasis on sustainability and data-protection compliance ensures consistent high-value orders for secure processing and encryption silicon.

- Analog Devices Inc.

- ams Osram AG

- Broadcom Inc.

- Dialog Semiconductor Ltd.

- Infineon Technologies AG

- Mediatek Inc.

- Microchip Technology Inc.

- Micron Technology Inc.

- Nordic Semiconductor ASA

- NXP Semiconductors N.V.

- ON Semiconductor Corp.

- Qualcomm Inc.

- Renesas Electronics Corp.

- Rohm Semiconductor

- Samsung Electronics Co. Ltd.

- Sensirion AG

- Skyworks Solutions Inc.

- STMicroelectronics N.V.

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Texas Instruments Inc.

- Toshiba Electronic Devices & Storage Corp.

- Vishay Intertechnology Inc.

- Zilog Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of connected medical devices and IoT

- 4.2.2 Growing adoption of AI-enabled imaging systems

- 4.2.3 Rising chronic-disease burden driving remote monitoring

- 4.2.4 Government incentives for healthcare-specific fabs

- 4.2.5 Implantable bio-MEMS with on-chip power

- 4.2.6 Lab-on-chip diagnostics reducing central-lab dependence

- 4.3 Market Restraints

- 4.3.1 High upgrade costs for legacy medical equipment

- 4.3.2 Stringent regulatory approval cycles for chip changes

- 4.3.3 Thermal issues in miniaturised wearable/implantables

- 4.3.4 Supply-chain concentration in specialist substrates

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Impact of Key Macro Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Medical Imaging

- 5.1.2 Consumer Medical Electronics

- 5.1.3 Diagnostic Patient Monitoring and Therapy

- 5.1.4 Medical Instruments

- 5.2 By Component

- 5.2.1 Integrated Circuits

- 5.2.1.1 Analog

- 5.2.1.2 Logic

- 5.2.1.3 Memory

- 5.2.1.4 Micro-components

- 5.2.2 Optoelectronics

- 5.2.3 Sensors

- 5.2.4 Discrete Components

- 5.2.5 Research Institutes

- 5.2.1 Integrated Circuits

- 5.3 By Technology Node

- 5.3.1 Less than 28 nm

- 5.3.2 28-65 nm

- 5.3.3 Above 65 nm

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 South-East Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.6 Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Analog Devices Inc.

- 6.4.2 ams Osram AG

- 6.4.3 Broadcom Inc.

- 6.4.4 Dialog Semiconductor Ltd.

- 6.4.5 Infineon Technologies AG

- 6.4.6 Mediatek Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Micron Technology Inc.

- 6.4.9 Nordic Semiconductor ASA

- 6.4.10 NXP Semiconductors N.V.

- 6.4.11 ON Semiconductor Corp.

- 6.4.12 Qualcomm Inc.

- 6.4.13 Renesas Electronics Corp.

- 6.4.14 Rohm Semiconductor

- 6.4.15 Samsung Electronics Co. Ltd.

- 6.4.16 Sensirion AG

- 6.4.17 Skyworks Solutions Inc.

- 6.4.18 STMicroelectronics N.V.

- 6.4.19 Taiwan Semiconductor Manufacturing Co. Ltd.

- 6.4.20 Texas Instruments Inc.

- 6.4.21 Toshiba Electronic Devices & Storage Corp.

- 6.4.22 Vishay Intertechnology Inc.

- 6.4.23 Zilog Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment