|

시장보고서

상품코드

1939677

샌드위치 패널 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Sandwich Panels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

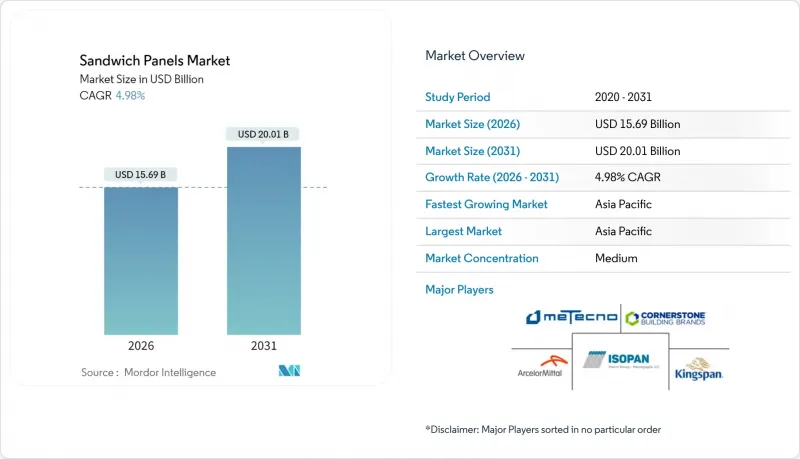

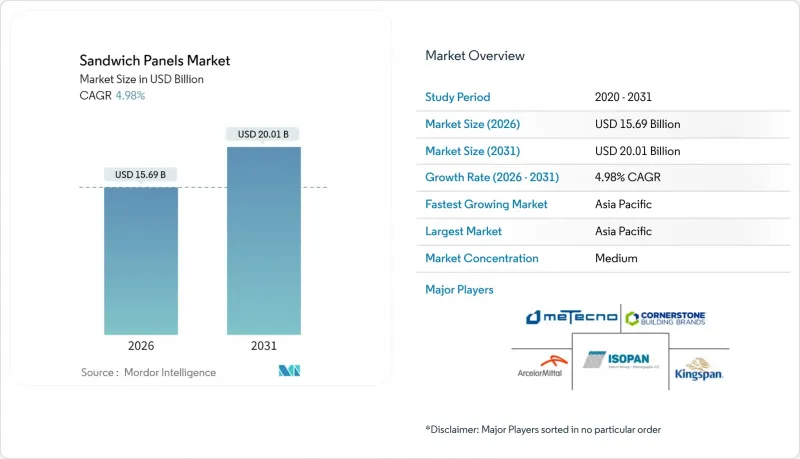

샌드위치 패널 시장은 2025년 149억 5,000만 달러에서 2026년에는 156억 9,000만 달러로 성장하며, 2026-2031년에 CAGR 4.98%로 추이하며, 2031년까지 200억 1,000만 달러에 달할 것으로 예측되고 있습니다.

데이터센터, 냉장 보관 시설, 모듈식 조립식 생산 라인에서 고성능 건축 외피에 대한 지속적인 수요가 이러한 확장을 지원하고 있습니다. 산업 개발업체들은 구조적 무결성, 단열 효율, 신속한 설치가 가능한 공장 생산 패널을 선호하며, 공공 정책은 건축 기준을 높은 단열 성능(R값)과 낮은 제조 과정의 탄소 배출량(내장 탄소)으로 유도하고 있습니다. 따라서 제조업체는 연속 생산 확대, 재활용 가능한 핵심 재료의 화학적 특성에 대한 실험, 프로젝트 주기를 단축하는 디지털 설계 툴의 통합을 추진하고 있습니다. 업계 구조조정은 완만한 속도로 진행 중: 주요 다국적 기업은 수직적 통합을 심화시키는 한편, 지역 특화 전문 업체들이 다수 존재하며, 지역 특화 구성을 지속적으로 공급함으로써 가격 규율이 유지되고 있습니다. 샌드위치 패널 시장은 또한 전력 소비가 많은 디지털 인프라의 수혜를 받고 있습니다. 하이퍼스케일 사업자들은 견고하고 기밀성이 높은 외관을 선호하며, 이를 통해 시운전을 가속화하고 기계적 부하를 줄일 수 있습니다.

세계 샌드위치 패널 시장 동향과 인사이트

구조용 단열패널의 냉장창고 용도 확대

R값 7-8, 작동 온도 범위 -45℃-+80℃의 폴리우레탄 패널은 EPS나 유리섬유를 능가하여 새로운 냉장실 사양의 주류가 되고 있습니다. 개발업체들은 리노베이션보다 37년된 노후화된 창고의 재건축을 늘리고 있으며, HACCP 세척 프로토콜을 준수하는 공장 마감의 위생적인 패널을 선호하고 있습니다. 2024년에는 투기적 냉장창고 착공 면적이 250만 평방피트에 달하고, 기관투자자들의 장기적인 신뢰를 보여주고 있습니다. 에너지 집약형 냉동고 역시 고단열 외장재에 대한 공공요금 환급을 유도하여 고단열 샌드위치 패널의 수주를 더욱 끌어올리고 있습니다.

PVDF 기반 알루미늄 복합 패널 수요 증가

건축가와 파사드 기술자들은 PVDF 코팅 알루미늄 외장재의 15년 이상의 수명을 높이 평가했습니다. 나노 PVDF 배합 기술은 자체 세척 특성을 추가하여 눈에 띄는 커튼월의 운영 비용 절감에 기여합니다. AAMA 2605-05 시험 준수는 내스크래치성, 끓는 물 부착성, 내변색성(ΔE<1.3)과 같은 성능 지표를 지원합니다. 가볍고 디자인성이 뛰어난 프로파일과 난연성 코어의 조합으로 파사드 고정이 단순화되어 시공을 신속하게 할 수 있습니다. 또한 디지털 인쇄 그래픽을 지원하므로 브랜드를 전면에 내세운 외장 프로젝트에 적합합니다.

특정 패널 유형의 내화 성능에 대한 제한 사항

폴리우레탄(PUR), 폴리이소시아네이트(PIR), 발포폴리스티렌(EPS), 발포폴리스티렌(XPS) 등의 유기계 발포 코어 소재는 250℃ 이상에서 빠르게 열화됩니다. 이로 인해 질량이 손실되고 독성 배출물이 방출되어 플래시 오버 상태가 가속화됩니다. 유럽의 보험사들은 특히 식품 가공 공장에서 가연성 코어 재료로 마감된 시설에 대한 보험 가입을 거부하거나 할증된 보험료를 부과하는 경우가 많습니다. 미네랄울로 만든 대체품은 더 높은 온도를 견딜 수 있지만 무게와 비용이 증가합니다. 팽창성 중간층, 접합부 방화막, 광물섬유 방화벽 등의 혁신 기술이 주류가 되고 있지만, 규제 승인을 받기 위해서는 여전히 실물 크기 연소 시험이 표준입니다. 독일과 같은 국가에서는 가장 엄격한 외벽 가연성 규제가 적용되어 프로젝트 팀의 재료 선택을 제한하고 있습니다.

부문 분석

2025년 기준 PUR 패널은 샌드위치 패널 시장 점유율 41.32%를 차지하며 냉동고 건설에서 폴리이소시아놀레이트, EPS, 유리섬유를 능가하는 R-7-R-8의 단열 성능에 힘입어 5.34%의 연평균 복합 성장률(CAGR)로 선두를 유지할 것으로 예측됩니다. PUR 코어를 기반으로 한 샌드위치 패널 시장 규모는 냉장창고 개발업체들이 기존 설비를 개조하고 은폐식 체결 조인트와 식품 안전 가공제를 갖춘 연속 제조 모듈을 채택함에 따라 확대될 것으로 예측됩니다.

MDI 원료공급 병목현상이 나타나면서 각 제조업체들은 촉매 패키지의 최적화를 통해 폐쇄공극률을 유지하면서 사이클 타임을 단축하기 위해 노력하고 있습니다. 한편, 환경 규제 강화로 인해 지구 온난화 계수가 낮은 바이오 유래 폴리올과 발포제의 채택이 제조업체에 촉구되고 있습니다.

2025년 기준 알루미늄은 샌드위치 패널 시장 점유율의 45.29%를 차지할 것으로 예상되며, 그 배경에는 압출 성형 능력의 보급, 내식성, 아노다이징 처리의 다용도성이 있습니다. PVDF 코팅 코일은 15년 색상 보증을 자랑하며, 나노 PVDF로의 업그레이드를 통해 파사드의 청결을 유지하고, 유지보수로 인한 가동 중단 시간을 최소화합니다. 연속섬유강화 열가소성 플라스틱은 5.38%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, 경량 패널이 지진 하중을 완화하는 데이터센터 외장재로 채택이 증가하고 있습니다. 탄소섬유 테이프는 보강 백플레이트 없이도 두 자릿수 스팬 단축을 가능하게 합니다.

CFRT 외판은 복잡한 곡률로 열성형이 가능하여 절삭 가공이나 후가공 접착의 수고를 덜어줍니다. 또한 매트릭스와 보강재가 모두 열가소성이기 때문에 폐쇄형 재활용이 가능합니다. 반면, 중량보다 점하중 저항이 우선시되는 경우, 특히 중하중 랙 고정이 요구되는 냉장 물류시설에서는 강판 외판이 주류를 이루고 있습니다. 염수분무로 인한 금속의 열화가 심한 양식업과 같은 부식성 환경에서는 유리섬유 강화 패널이 우위를 발휘합니다.

샌드위치 패널 시장 보고서는 핵심 소재(폴리우레탄(PUR), 폴리이소시아네이트(PIR) 등), 외장재(알루미늄, 강판, 유리섬유강화패널(FRP) 등), 제조기술(연속식, 간헐식), 용도(벽면, 지붕 등), 최종 용도(주택, 상업시설 등), 지역(아시아, 북미 등)별로 분석되었습니다. 등), 지역별(아시아태평양, 북미 등)로 분석되고 있습니다.

지역별 분석

아시아태평양은 2025년 49.85%의 점유율로 1위를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 5.78%로 가장 빠른 성장세를 보일 것으로 예측됩니다. 인도의 데이터센터 계획, 싱가포르의 그린에너지 물류, 말레이시아의 반도체 공장 등은 모두 단열성이 우수하고 신속한 설치가 가능한 외장을 필요로 하고 있습니다. 중국의 성장은 둔화되고 있지만 구조적으로 큰 규모를 유지하고 있습니다. 베이징시의 개조 프로그램으로의 전환은 경량 샌드위치 외피에 적합한 박형 오버클래드 단열 개조를 촉진하고 있습니다.

북미는 인프라 투자 고용법(IIJA)의 혜택을 받고 있습니다. 썬벨트 지역과 중부 대서양 연안 지역의 콜드체인 확장에는 캘리포니아 주 건축법(Title 24) 및 IGCC 코드 요건을 충족하는 200mm 두께의 PUR 패널이 채택되었습니다. 캐나다의 탄소가격제도는 EPD(환경 제품 선언) 문서를 보유한 광물성 울 코어 소재를 유틸리티에 유도하고 있습니다. 멕시코의 마킬라도라 회랑에서는 USMCA(미국-멕시코-캐나다 협정)의 에너지 규정 준수를 위해 단열 지붕재를 추가로 도입하고 있으며, 이러한 변화는 현지의 패널 적층 능력을 촉진하고 있습니다.

유럽은 낮은 수준에서 회복세를 보이고 있으며, EU 전역에서 건설 활동이 활발해지고 있습니다. 그러나 에너지 성능 지침의 제로 에미션 목표가 개보수 보조금을 추진하면서 예산은 박형, 고단열 성능의 외벽재에 집중되고 있습니다.

중동의 메가 프로젝트, 사우디의 데이터센터 캠퍼스, UAE의 프리존 창고에서는 주변 온도 50℃에 대응하는 저연소성 클래딩 시스템이 요구되고 있습니다. 라틴아메리카는 여전히 지역적 차이가 있습니다. 브라질의 물류 클러스터는 PIR 패널을 채택하고 있지만, 정치 상황의 변동으로 인해 대규모 공공 조달에 영향을 미치고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The Sandwich Panels market is expected to grow from USD 14.95 billion in 2025 to USD 15.69 billion in 2026 and is forecast to reach USD 20.01 billion by 2031 at 4.98% CAGR over 2026-2031.

Sustained demand for high-performance building envelopes in data centers, cold-storage hubs, and modular prefabrication lines anchors this expansion. Industrial developers favor factory-produced panels that combine structural integrity, thermal efficiency, and rapid installation, while public policy is moving building codes toward higher R-values and lower embodied carbon. Manufacturers are therefore scaling continuous production, experimenting with recyclable core chemistries, and integrating digital design tools that shorten project cycles. Consolidation remains moderate: leading multinationals deepen vertical integration, yet a long tail of regional specialists continues to supply localized configurations, keeping pricing discipline tight. The sandwich panels market benefits additionally from power-hungry digital infrastructure; hyperscale operators prefer robust, airtight envelopes that expedite commissioning and reduce mechanical loads.

Global Sandwich Panels Market Trends and Insights

Growing Cold-Storage Applications of Structural Insulated Panels

Polyurethane panels, rated R-7 to R-8 and operational from -45 °C to +80 °C, outperform EPS and fiberglass and thus dominate new cold-room specifications. Developers increasingly replace aging 37-year-old warehouses rather than retrofit, preferring factory-finished, hygienic panels that answer HACCP cleaning protocols. Speculative cold-store starts reached 2.5 million ft2 in 2024, signaling long-range confidence among institutional investors. Energy-intensive freezers also trigger utility rebates for better-insulated envelopes, further lifting orders for high-R sandwich assemblies.

Increasing Demand for PVDF-Based Aluminum Composite Panels

Architects and facade engineers value the 15-year-plus service life of PVDF-coated aluminum skins, while nano-PVDF formulations add self-cleaning properties that reduce OPEX in high-profile curtain walls. AAMA 2605-05 test compliance underlines scratch hardness, boiling-water adhesion, and color-fastness (ΔE < 1.3) performance metrics. The lightweight, design-flexible profile-paired with fire-retardant cores-simplifies facade anchoring, accelerates installation, and supports digitally printed graphics for brand-centric cladding projects.

Fire-Performance Limitations of Certain Panel Types

Organic foam cores such as PUR, PIR, EPS, and XPS can degrade rapidly above 250 °C, shedding mass and releasing toxic effluent that accelerates flashover conditions. European insurers often decline or surcharge facilities finished with combustible cores, especially in food-processing plants. Mineral-wool alternatives withstand higher temperatures but add weight and cost. Innovations such as intumescent inter-layers, fire stops at joints, and mineral-fiber fire barriers are being mainstreamed, yet full-scale burn tests remain the gold standard for regulatory acceptance. Countries such as Germany apply some of the strictest facade combustibility rules, constraining project-team material choices.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Prefabricated and Modular Construction

- Energy-Efficiency Regulations for Building Envelopes

- Oriented-Strand-Board VOC Emissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PUR panels contributed 41.32% to the sandwich panels market share in 2025 and are forecast to lead with a 5.34% CAGR, buoyed by R-7 to R-8 performance that outclasses polyisocyanurate, EPS, and fiberglass in freezer construction. The sandwich panels market size tied to PUR cores should widen as cold-storage developers retro-commission older stock and adopt continuous-manufactured modules that arrive with concealed-fastener joints and food-safe finishes.

Emerging supply bottlenecks in MDI feedstock have prompted producers to finetune catalyst packages, trimming cycle times without sacrificing closed-cell content. Environmental scrutiny, however, is nudging manufacturers to explore bio-sourced polyols and blowing agents with lower global-warming potential.

Aluminum captured 45.29% of the sandwich panels market share in 2025, underpinned by widespread extrusion capacity, corrosion resistance, and anodizing versatility. PVDF-coated coils boast 15-year color warranties, and nano-PVDF upgrades prolong facade cleanliness, minimizing service downtime. Continuous fiber reinforced thermoplastics, projected at 5.38% CAGR, are finding traction in data-center cladding where lightweight panels mitigate seismic loads, and carbon-fiber tapes allow double-digit span reductions without stiffener back-plates.

CFRT skins can be thermo-formed into complex radii, eliminating kerf-cutting and post-bonding labor. They also enable closed-loop recycling because both matrix and reinforcement remain thermoplastic. By contrast, steel skins dominate when point-load resistance trumps weight, especially in refrigerated logistics parks that specify heavy-duty racking ties. Fiberglass reinforced panels win in corrosive atmospheres such as aquaculture, where salt spray degrades metal fast.

The Sandwich Panels Report is Segmented by Core Material (Polyurethane (PUR), Polyisocyanurate (PIR), and More), Skin Material (Aluminum, Steel, Fiberglass Reinforced Panel (FRP), and More), Technology (Continuous and Discontinuous), Application (Wall Panels, Roof Panels, and More), End-Use Sector (Residential, Commercial, and More), and Geography (Asia-Pacific, North America, and More).

Geography Analysis

Asia-Pacific dominated with a 49.85% share in 2025 and posts the fastest 5.78% CAGR through 2031. India's data-center pipeline, Singapore's green-energy logistics, and Malaysia's semiconductor fabs all mandate thermally efficient, rapidly deployable envelopes. China's growth moderates yet remains structurally sizable; Beijing's shift to renovation programs favors thin, over-clad insulation retrofits that suit lightweight sandwich skins.

North America benefits from the Infrastructure Investment and Jobs Act. Cold-chain expansion in the Sunbelt and Mid-Atlantic integrates 200 mm PUR panels that satisfy Title 24 and IGCC code pathways. Canada's carbon-pricing framework steers public projects toward mineral-wool cores with EPD documentation. Mexico's maquiladora corridor is adding insulated roofing to comply with USMCA energy stipulations, a shift that spurs local panel lamination capacity.

Europe is rebounding from a low base; EU-wide construction. Still, the Energy Performance Directive's zero-emission targets drive retrofit vouchers, funneling budget toward thin-profile, high-lambda facades.

Middle East megaprojects, Datacenter campuses in KSA, free-zone warehouses in UAE, demand low-combustible cladding systems rated for 50 °C ambient. Latin America remains patchy: Brazilian logistics clusters adopt PIR panels, but political flux dampens larger public procurements.

- Alubel

- ArcelorMittal

- Areco

- Assan Panel A.S.

- Building Component Solutions LLC

- Cornerstone Building Brands, Inc.

- DANA Group of Companies

- EPACK Prefab

- Isopan

- Jiangsu Jingxue Energy Saving Technology Co., Ltd.

- Kingspan Group

- Lattonedil

- Marcegaglia Steel S.p.A.

- Metecno Group

- NAV SYSTEM

- Rautaruukki Corporation

- Romakowski GmbH and Co. KG

- Sintex

- Structural Panels

- Tata Steel

- Teknopanel

- Tonmat Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing cold-storage applications of structural insulated panels

- 4.2.2 Increasing demand for PVDF-based aluminium composite panels

- 4.2.3 Rapid growth of prefabricated and modular construction

- 4.2.4 Energy-efficiency regulations for building envelopes

- 4.2.5 Data-centre boom requiring high-performance envelopes

- 4.3 Market Restraints

- 4.3.1 Fire-performance limitations of certain panel types

- 4.3.2 Oriented-strand-board VOC emissions

- 4.3.3 Moisture ingress and long-term degradation in PUR/PIR cores

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Core Material

- 5.1.1 Polyurethane (PUR)

- 5.1.2 Polyisocyanurate (PIR)

- 5.1.3 Mineral Wool

- 5.1.4 Expanded Polystyrene (EPS)

- 5.1.5 Other Core Materials

- 5.2 By Skin Material

- 5.2.1 Continuous Fiber Reinforced Thermoplastics (CFRT)

- 5.2.2 Fiberglass Reinforced Panel (FRP)

- 5.2.3 Aluminum

- 5.2.4 Steel

- 5.2.5 Other Skin Materials

- 5.3 By Technology

- 5.3.1 Continuous

- 5.3.2 Discontinuous

- 5.4 By Application

- 5.4.1 Wall Panels

- 5.4.2 Roof Panels

- 5.4.3 Insulated Panels

- 5.4.4 Other Applications

- 5.5 By End-use Sector

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.5.4 Institutional and Infrastructure

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 Italy

- 5.6.3.4 France

- 5.6.3.5 Spain

- 5.6.3.6 Poland

- 5.6.3.7 NORDIC Countries

- 5.6.3.8 Hungary

- 5.6.3.9 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alubel

- 6.4.2 ArcelorMittal

- 6.4.3 Areco

- 6.4.4 Assan Panel A.S.

- 6.4.5 Building Component Solutions LLC

- 6.4.6 Cornerstone Building Brands, Inc.

- 6.4.7 DANA Group of Companies

- 6.4.8 EPACK Prefab

- 6.4.9 Isopan

- 6.4.10 Jiangsu Jingxue Energy Saving Technology Co., Ltd.

- 6.4.11 Kingspan Group

- 6.4.12 Lattonedil

- 6.4.13 Marcegaglia Steel S.p.A.

- 6.4.14 Metecno Group

- 6.4.15 NAV SYSTEM

- 6.4.16 Rautaruukki Corporation

- 6.4.17 Romakowski GmbH and Co. KG

- 6.4.18 Sintex

- 6.4.19 Structural Panels

- 6.4.20 Tata Steel

- 6.4.21 Teknopanel

- 6.4.22 Tonmat Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment