|

시장보고서

상품코드

1939698

시험, 검사, 인증(TIC) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Testing, Inspection, And Certification - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

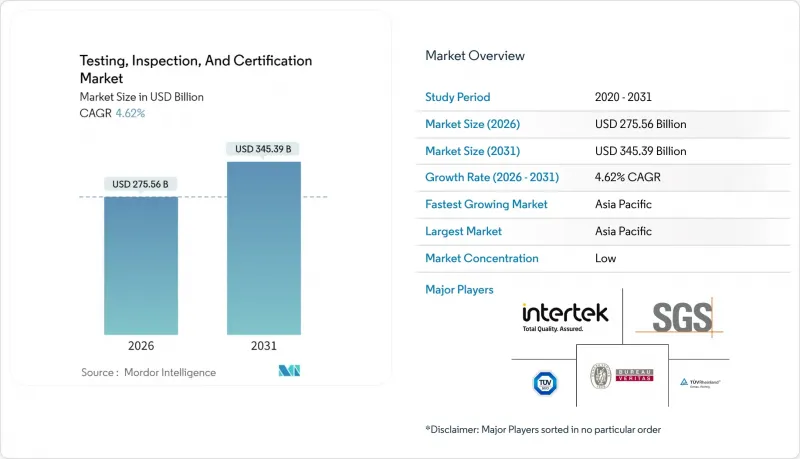

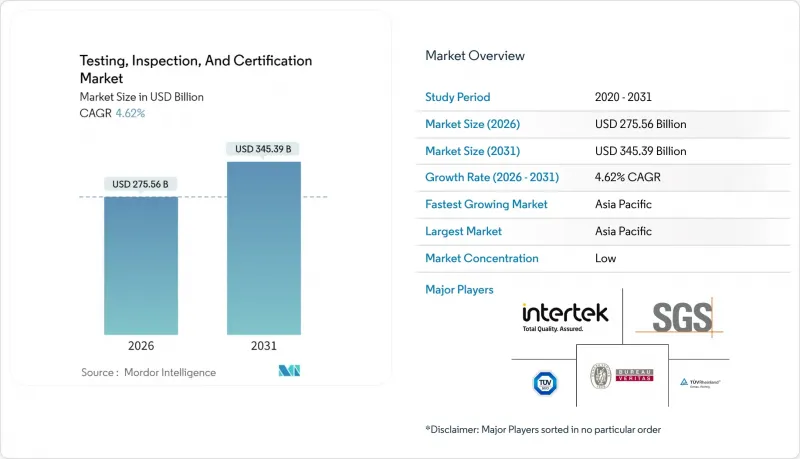

시험·검사·인증(TIC) 시장은 2025년 2,634억 달러에서 2026년에는 2,755억 6,000만 달러로 성장하며, 2026-2031년에 CAGR 4.62%로 추이하며, 2031년까지 3,453억 9,000만 달러에 달할 것으로 예측되고 있습니다.

규제 감시 강화, 제품 안전에 대한 기대치 상승, 디지털 전환의 진전으로 인해 소비재, 전자제품, 에너지 저장, 자동차 등 각 밸류체인에서 독립적인 보증 서비스에 대한 수요가 증가하고 있습니다. ESG 및 탄소발자국 검증 의무화, 커넥티드 제품에 대한 사이버 보안 규제 강화, 세계화된 공급망의 복잡성으로 인해 기업은 공인된 제3자 기관에 의존할 수밖에 없는 상황에 처해 있습니다. 전략적 통합과 AI를 활용한 검사 기술의 결합을 통해 시장 리더는 서비스 범위를 확장하고 효율성을 향상시키고 있습니다. 한편, 배터리 및 5G 테스트와 같은 틈새 분야의 비용 압박과 인력 부족으로 인해 공급업체들은 이익률을 보호하기 위해 자동화 및 인력 개발에 투자해야 하는 상황에 직면해 있습니다.

세계 시험, 검사 및 인증(TIC) 시장 동향 및 인사이트

의무화된 ESG/탄소발자국 검증으로 수출 규정 준수 가속화

세계 탈탄소화 정책에 따라 탄소발자국 인증은 자발적 노력에서 국경 간 무역의 전제조건으로 자리매김하고 있습니다. EU의 탄소국경조정기구(CBAM)는 ISO 14067에 따라 제품 탄소발자국 검증을 요구하고 있으며, 전 세계 수출업체들이 인증 보증을 받도록 장려하고 있습니다. SGS는 30년간 쌓아온 지속가능성 전문성을 바탕으로 검증 프로그램을 확대하기 시작했습니다. 한편, 뷰로베리타스는 조직 차원의 ESG 인증 스위트를 제공합니다. SGS가 Worldly와 제휴한 데이터 검증 플랫폼과 같은 통합 디지털 플랫폼은 지속적인 공급망 배출량 추적과 독립적인 검증을 결합하여 감사 가능한 실시간 증거를 요구하는 규제 당국의 요구에 부응합니다.

AI를 활용한 원격 모니터링으로 서비스 제공 모델을 혁신

인공지능 툴은 반복적인 육안 검사의 자동화, 설비 고장 예측, 현장 입회 없이 지속적인 품질 모니터링을 실현하고 있습니다. 디지털 트윈 기술은 물리적 자산을 가상공간에 재현하여 검사자가 이상 징후를 감지하고 성능 파라미터를 거의 실시간으로 검증할 수 있도록 합니다. 주요 TIC 프로바이더들은 AI 지원 이미지 분석 및 센서 퓨전 도입 후 현장 방문 횟수를 최대 50%까지 줄였다고 보고하고 있습니다. 이동 시간 단축과 빠른 피드백 루프를 통해 숙련된 기술자를 고부가가치 업무에 재배치할 수 있으며, 고객의 다운타임을 줄일 수 있습니다. 북미와 유럽 규제 당국의 원격 발급 인증서 수용이 확대되면서 이러한 플랫폼의 대규모 도입이 가속화되고 있습니다.

경쟁으로 인한 마진 압박으로 기존 모델에 대한 부담 가중

수천 개의 소규모 연구소가 상품화된 테스트 분야에서 경쟁하면서 일상적인 화학, 재료 및 소비재 분석의 가격 결정력을 떨어뜨리고 있습니다. 이에 반해, 주요 공급업체들은 구독 기반의 지속적인 모니터링 서비스 및 데이터가 풍부한 ESG 검증으로 전환하여 고객과의 대화를 단가에서 가치 창출로 전환하고자 노력하고 있습니다. 그러나 디지털 플랫폼 구축, IoT 센서 통합, 데이터 분석에 대한 직원 교육에 많은 자본 지출이 필요하고, 중견기업에게는 과도한 부담이 되고 있습니다. 이로 인해 발생하는 서비스 제공 비용의 격차는 세계 리더와 지역 전문 기업 간의 격차를 확대시킬 위험이 있습니다.

부문 분석

시험은 2025년 시험, 검사 및 인증(TIC) 시장 점유율의 61.25%를 차지할 것으로 예상되며, 제품 개발 및 컴플라이언스 주기에서 시험의 기본적 역할을 강조하고 있습니다. 엄격한 자동차 사이버 보안 규제와 복잡한 5G 무선 주파수 특성으로 인해 시험소는 밀리미터파 챔버와 무선 시스템에 대한 투자를 추진하고 있습니다. 또한 UL 솔루션즈가 주요 EV 생산 기지 인근에 시험소를 확장하고 열 폭주 및 진동 프로토콜을 지원함에 따라 배터리 평가 시험, 검사 및 인증(TIC) 시장 규모도 확대되고 있습니다.

인증 서비스는 규모는 작지만 4.88%의 가장 빠른 CAGR로 성장할 것으로 예측됩니다. 사이버 트러스트 마크와 같은 새로운 프로그램은 ISO/IEC 17065 인증 기관의 사이버 보안 라벨 인증을 의무화하고 있으며, 이는 적절한 인증을 획득한 기업에게 새로운 수입원이 되고 있습니다. 탄소발자국 검증과 관련된 ESG 기준은 수요를 더욱 확대할 것이며, 수익성 높은 성장을 추구하는 기업에게 인증은 전략적 우선순위가 되고 있습니다. 검사는 두 부문의 중간에 위치하며, 공급망 검증 의무화의 혜택을 받으면서도 AI 기반 원격 시각 툴로 인한 대체 압력에 직면해 있습니다.

2025년 시험-검사-인증(TIC) 시장에서는 아웃소싱 서비스가 74.65%의 점유율을 차지할 것으로 예상되며, 이는 제조업체가 증가하는 표준에 대응하기 위해 제3자의 전문 지식에 의존하고 있기 때문으로 분석됩니다. 독립형 시험소는 전자기 호환성 시험, 고에너지 배터리 가혹 시험 등 자본 집약적인 분야에서 규모의 우위를 발휘하고 있으며, 전 세계 거점 네트워크를 통해 다국적 기업의 컴플라이언스 프로세스 조정을 지원하고 있습니다. 이러한 추세는 특히 가전 분야에서 두드러지게 나타나고 있으며, 빠른 모델 업데이트 주기로 인해 최첨단 설비를 유지하는 외부 시험소가 유리하게 작용하고 있습니다.

데이터 기밀성 및 운영 관리를 중시하는 생명과학, 유틸리티, 국방 관련 기업에서는 사내 프로그램이 여전히 필수적이지만, 그 시장 점유율은 점차 줄어들고 있습니다. 자동차 OEM 업체들은 설계 검증 벤치를 자체적으로 유지하면서 세계 시장 진입을 위한 형식승인 시험을 인증기관에 위탁하는 하이브리드형 접근방식이 부상하고 있습니다. 이는 내부 모니터링과 외부 인증이 공존하며 리소스를 최적화하는 방법을 보여줍니다.

지역별 분석

아시아태평양은 2025년 기준 47.05%의 점유율을 차지하며 수요의 핵심으로 자리 잡고 있으며, 예측 기간 중 5.28%의 높은 성장률을 보일 것으로 예측됩니다. 이 지역의 성장은 주로 중국, 인도, 베트남, 인도네시아의 제조 거점 확대와 전자, 자동차, 재생에너지 분야의 국내 기준의 단계적 강화에 의해 주도되고 있습니다. 국제적인 TIC 그룹은 증가하는 현지 인증 요건에 대응하기 위해 이 지역의 EV 배터리 기가팩토리 인근에 연구소에 대한 투자를 확대하고 있습니다. 중산층의 소비 확대에 따라 제품 안전 라벨에 대한 관심이 높아지면서 제3자 보증 프로바이더 시장 침투가 가속화되고 있습니다.

북미는 테스트, 검사 및 인증(TIC) 시장에서 두 번째 점유율을 차지하고 있으며, 항공우주, 의료기기, 첨단 전자기기 부문의 견고한 성장에 힘입은 바 있습니다. 사이버 트러스트 마크는 자율적인 사이버 보안 인증을 선도적으로 도입하려는 규제 당국의 의지를 보여주며, 무선, 암호화 기술, 무선 시험(OTA) 분야의 시험소 인증을 촉진하고 있습니다. 수입업체들이 FDA의 신속한 통관을 가능하게 하는 '공인 수입업체 인증'을 요구하고 있는 가운데, 식품 안전은 안정적인 검사량의 기반이 되고 있습니다.

유럽에서는 ESG, 사이버 보안, 자동차 기능 안전 지침을 통합한 촘촘한 규제 프레임워크가 작동하고 있습니다. EU 삼림파괴 방지 규정, CBAM(탄소국경조정 메커니즘) 등 유럽 대륙의 순환경제 대책에 대한 선도적인 입장은 전 세계 수출업체들이 검증된 지속가능성 인증을 획득하도록 장려하고 있습니다. UNECE(유엔 유럽경제위원회)의 자동차 사이버 보안 및 소프트웨어 업데이트 관리에 관한 규정 R155 및 R156은 새로운 형식 인증 프로그램을 만들어 TIC(시험, 검사 및 인증) 프로바이더에 위협 분석, 침투 테스트, 안전한 업데이트 검증을 위한 전문 트랙을 구축하도록 촉구하고 있습니다. 전문 트랙을 구축하도록 장려하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The testing inspection certification market is expected to grow from USD 263.40 billion in 2025 to USD 275.56 billion in 2026 and is forecast to reach USD 345.39 billion by 2031 at 4.62% CAGR over 2026-2031.

Escalating regulatory scrutiny, rising product-safety expectations, and digital transformation are strengthening demand for independent assurance services across consumer goods, electronics, energy storage, and automotive value chains. Mandatory ESG and carbon-footprint verification requirements, tighter cybersecurity rules for connected products, and the complexity of globalized supply networks are compelling firms to rely on accredited third parties. Strategic consolidation combined with AI-enabled inspection technologies is allowing market leaders to widen service scope and improve efficiency. At the same time, cost pressures and talent shortages in niche domains such as battery and 5G testing are forcing providers to invest in automation and workforce development to protect margins.

Global Testing, Inspection, And Certification Market Trends and Insights

Mandatory ESG / Carbon-Footprint Verification Accelerates Export Compliance

Global decarbonization policies are repositioning carbon-footprint certification from a voluntary gesture to a prerequisite for cross-border trade. The EU Carbon Border Adjustment Mechanism requires ISO 14067 product carbon-footprint verification and is encouraging exporters worldwide to secure accredited assurance. SGS has leveraged three decades of sustainability expertise to launch expanded verification programs, while Bureau Veritas has rolled out organization-level ESG certification suites. Integrated digital platforms, such as SGS's data-validation partnership with Worldly, couple continuous supply-chain emissions tracking with independent verification, aligning with regulators' preference for auditable, real-time evidence.

AI-Enabled Remote Monitoring Transforms Service Delivery Models

Artificial intelligence tools are automating repetitive visual checks, predicting equipment failures, and enabling continuous quality monitoring without on-site presence. Digital twins recreate physical assets virtually, permitting inspectors to identify anomalies and validate performance parameters in near real time. Major TIC providers report up to 50% cuts in field visits after adopting AI-supported image analytics and sensor fusion. Savings in travel time and faster feedback loops allow reallocation of skilled technicians to higher-value tasks while reducing customer downtime. Growing acceptance of remotely issued certificates by regulatory bodies in North America and Europe is accelerating the large-scale deployment of these platforms.

Margin Squeeze from Price Competition Pressures Traditional Models

Thousands of small laboratories compete in commoditized testing niches, eroding pricing power for routine chemical, materials, and consumer-product assays. Larger providers are responding by migrating toward subscription-based continuous-monitoring offers and data-rich ESG verification, aiming to shift customer conversations away from unit pricing toward value creation. However, building digital platforms, integrating IoT sensors, and training staff in data analytics entail substantial capital outlays that disproportionately burden mid-tier firms. The resulting cost-to-serve gap risks widening the divide between global leaders and regional specialists.

Other drivers and restraints analyzed in the detailed report include:

- Cyber-Physical Security Certification Drives IoT Testing Demand

- Global Supply-Chain Complexity Intensifies Third-Party Assurance

- Talent Shortages in Specialized Domains Constrain Growth

- Increase in Lead Times Due to Complex Global Supply Chains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testing accounted for 61.25% of the 2025 testing inspection certification market share, underlining its foundational role in product development and compliance cycles. Stringent automotive cybersecurity rules and complex 5G radio frequency characteristics are driving laboratories to invest in millimeter-wave chambers and over-the-air systems. The testing, inspection certification market size for battery evaluations is also expanding as UL Solutions extends laboratories near major EV production clusters to support thermal-runaway and vibration protocols.

Certification services, although smaller, are forecast to record the fastest 4.88% CAGR. New programs such as the Cyber Trust Mark require ISO/IEC 17065-accredited bodies to authorize cybersecurity labels, creating additional revenue streams for firms with the right accreditations. ESG standards linked to carbon-footprint verification further amplify demand, making certification a strategic priority for providers seeking margin-resilient growth. Inspection sits between the two segments, benefiting from supply-chain verification mandates yet facing substitution pressure from AI-enabled remote visual tools.

Outsourced services dominated the 2025 testing, inspection certification market, capturing a 74.65% share as manufacturers relied on third-party expertise to navigate proliferating standards. Independent labs offer scale advantages in capital-intensive domains such as electromagnetic compatibility and high-energy battery abuse testing, while their global footprint helps multinational clients harmonize compliance processes. The trend is strongest in consumer electronics, where rapid model refresh cycles favor external labs that maintain state-of-the-art facilities.

In-house programs remain essential for life-science, utility, and defense entities that insist on data confidentiality and operational control, but their market share is gradually eroding. Hybrid approaches are emerging: automotive OEMs retain design-validation benches yet outsource type-approval testing to accredited bodies for global market entry, illustrating how internal oversight and external certification can coexist to optimize resources.

The Testing, Inspection, and Certification Market Report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House, and Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, and More), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific remains the fulcrum of demand with a 47.05% share in 2025 and is expected to grow at a rapid rate of 5.28% during the forecast period. The region is mainly driven by expanding manufacturing footprints in China, India, Vietnam, and Indonesia, and by progressively stringent domestic standards across electronics, automotive, and renewables. International TIC groups have ramped up laboratory investments near EV battery gigafactories in the region to meet escalating local certification requirements. Rising middle-income consumption is also raising awareness of product-safety labels, accelerating market penetration for third-party assurance providers.

North America holds the second-largest slice of the testing, inspection certification market, supported by robust aerospace, medical-device, and advanced electronics sectors. The Cyber Trust Mark shows regulatory willingness to pioneer voluntary cybersecurity labeling, stimulating lab accreditation in wireless, cryptography, and over-the-air testing. Food safety continues to underpin steady inspection volumes as importers seek Qualified Importer Certification to unlock expedited FDA clearance.

Europe benefits from a dense regulatory framework that integrates ESG, cybersecurity, and automotive functional-safety directives. The continent's leadership in circular-economy measures, such as the EU Deforestation Regulation and CBAM, pushes exporters worldwide to obtain verified sustainability certificates. UNECE's R155 and R156 rules for automotive cybersecurity and software update management have spawned new homologation programs, prompting TIC providers to establish specialized tracks for threat analysis, penetration testing, and secure update validation.

- SGS SA

- Bureau Veritas SA

- Intertek Group plc

- TUV SUD AG

- TUV Rheinland AG

- TUV NORD GROUP

- DEKRA SE

- UL Solutions Inc.

- DNV AS

- Applus Servicios Tecnologicos S.A.

- Eurofins Scientific SE

- ALS Limited

- Kiwa N.V.

- Lloyd's Register Group Limited

- RINA S.p.A.

- Element Materials Technology Group

- Centre Testing International Group Co. Ltd.

- SAI Global Pty Ltd

- MISTRAS Group Inc.

- NSF International

- BSI Group (The British Standards Institution)

- Cotecna Inspection SA

- SOCOTEC Group SA

- FLOCERT GmbH

- Perry Johnson Registrars Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing regulatory compliance and product-safety mandates

- 4.2.2 Expansion of global supply chains demanding third-party assurance

- 4.2.3 Surge in consumer electronics and IoT product launches

- 4.2.4 AI-enabled remote and continuous monitoring platforms

- 4.2.5 Mandatory ESG / carbon-footprint verification in export markets

- 4.2.6 Cyber-physical security certification for connected products

- 4.3 Market Restraints

- 4.3.1 Margin squeeze from price competition

- 4.3.2 Trade frictions and divergent national standards

- 4.3.3 OEM self-certification via digital twins

- 4.3.4 Talent shortages in niche test domains (battery, 5G, biotech)

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Industry Vertical

- 5.3.1 Consumer Goods and Retail

- 5.3.2 ICT and Telecom

- 5.3.3 Automotive and Transportation

- 5.3.4 Aerospace and Defense

- 5.3.5 Oil, Gas and Petrochemicals

- 5.3.6 Energy and Utilities

- 5.3.7 Industrial Manufacturing and Machinery

- 5.3.8 Chemicals and Materials

- 5.3.9 Construction and Infrastructure

- 5.3.10 Life Sciences and Healthcare

- 5.3.11 Food, Agriculture and Beverage

- 5.3.12 Others (Environment, Sustainability, etc.)

- 5.4 By Mode of Service Delivery

- 5.4.1 On-site

- 5.4.2 Off-site/Laboratory

- 5.4.3 Remote / Digital

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 South-East Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SGS SA

- 6.4.2 Bureau Veritas SA

- 6.4.3 Intertek Group plc

- 6.4.4 TUV SUD AG

- 6.4.5 TUV Rheinland AG

- 6.4.6 TUV NORD GROUP

- 6.4.7 DEKRA SE

- 6.4.8 UL Solutions Inc.

- 6.4.9 DNV AS

- 6.4.10 Applus Servicios Tecnologicos S.A.

- 6.4.11 Eurofins Scientific SE

- 6.4.12 ALS Limited

- 6.4.13 Kiwa N.V.

- 6.4.14 Lloyd's Register Group Limited

- 6.4.15 RINA S.p.A.

- 6.4.16 Element Materials Technology Group

- 6.4.17 Centre Testing International Group Co. Ltd.

- 6.4.18 SAI Global Pty Ltd

- 6.4.19 MISTRAS Group Inc.

- 6.4.20 NSF International

- 6.4.21 BSI Group (The British Standards Institution)

- 6.4.22 Cotecna Inspection SA

- 6.4.23 SOCOTEC Group SA

- 6.4.24 FLOCERT GmbH

- 6.4.25 Perry Johnson Registrars Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment