|

시장보고서

상품코드

1939710

데이터센터 인프라 관리(DCIM) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Data Center Infrastructure Management (DCIM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

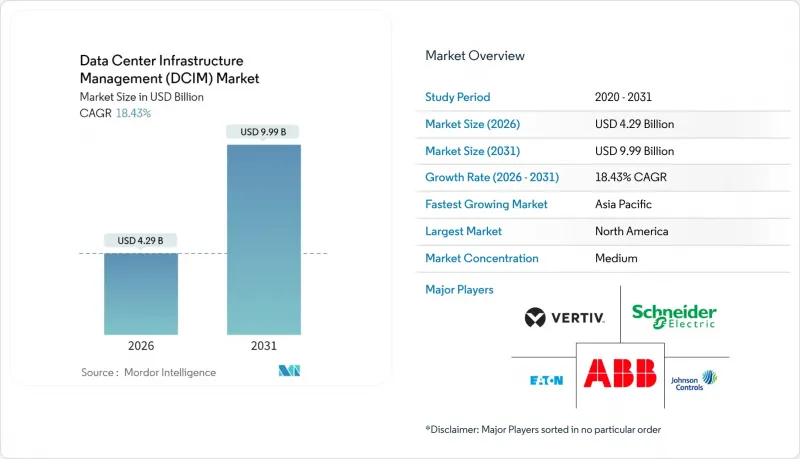

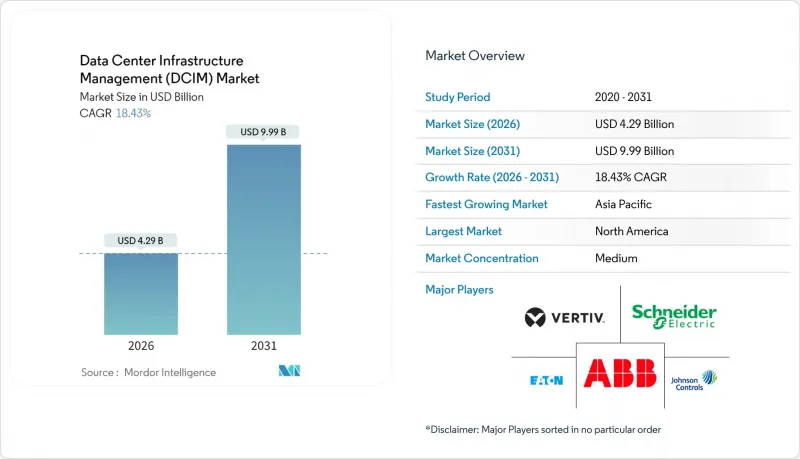

데이터센터 인프라 관리(DCIM) 시장은 2025년에 36억 2,000만 달러로 평가되며, 2026년 42억 9,000만 달러에서 2031년까지 99억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 18.43%로 예상됩니다.

성장을 주도하는 것은 AI 기반 열 부하, 유럽연합의 에너지 사용량 공개 의무화, 그리고 캠퍼스당 500MW 이상의 하이퍼스케일 프로젝트가 전 세계에서 확산되고 있는 추세입니다. 사이버 보험의 텔레메트리 요건을 충족하고 규제 준수를 측정 가능한 에너지 절감 효과로 전환하기 위해 예측 분석의 통합을 강화하고 있습니다. 관리형 DCIM 운영 관련 서비스가 가장 빠르게 성장하고 있는 배경에는 데이터센터 운영자들이 만성적인 시설 엔지니어 부족에 직면해 있기 때문입니다. 경쟁의 초점은 랙 레벨에서 냉각, 전력 및 자산 활용도를 최적화하는 통합 하드웨어 및 소프트웨어 포트폴리오에 집중되어 있습니다. 투자자들은 자금조달 비용을 검증 가능한 ESG 지표와 연동하고, DCIM 인증 효율을 신규 건설 및 리노베이션의 차별화 요소로 인식하고 있습니다.

세계 데이터센터 인프라 관리(DCIM) 시장 동향 및 인사이트

넷제로 달성 가속화 및 에너지 사용량 공개 의무화

EU 에너지 효율 지침에 따라 500kW 이상의 모든 데이터센터는 2024년 9월까지 전력사용효율(PUE), 탄소사용효율(CUE), 물사용효율(WUE) 공개가 의무화됨에 따라 DCIM은 임의 최적화 소프트웨어에서 필수적인 컴플라이언스 기반으로 포지셔닝이 변화하고 있습니다. 필수적인 컴플라이언스 기반이 되고 있습니다. 실시간 DCIM을 도입한 사업자는 동적 용량 예측을 통해 18%의 에너지 절감 효과를 보고하고 있으며, 규제 대응 투자에 대한 구체적인 매출이 입증되고 있습니다. 다국적 기업은 현재 지속가능성 보고의 효율성과 지역별 감사를 피하기 위해 모든 시설에서 동일한 DCIM 스택을 표준화하고 있습니다. 투자자들이 조화로운 ESG 공시를 요구함에 따라 그 수요는 유럽 외 지역으로 확대되고 있습니다. 이 지침은 EU 전력 소비의 약 3%를 차지하는 시설도 대상이며, 점진적인 효율성 향상은 지역 전체의 전력망 부하 감소로 이어질 수 있습니다.

500MW 이상의 클러스터 규모에 이르는 하이퍼스케일 확장

Compass Data Centers의 미시시피주 100억 달러 규모의 미시시피 프로젝트와 같은 캠퍼스 규모의 투자에는 모듈식 전원 및 냉각 장치군에 걸쳐 수천 개의 랙을 조정하는 DCIM 플랫폼이 필수적입니다. 기존 빌딩 관리 시스템은 기가 와트 규모의 랙 레벨 텔레메트리와 고장 예측 경고를 제공할 수 없습니다. 지멘스의 다년 공급 계약으로 대표되는 조립식 전력 모듈과의 통합은 DCIM 소프트웨어와 전기 인프라의 연계를 강화합니다. 자본 집약도가 높아지면서 사업자들은 운영 비용 절감을 위해 기류와 용량의 실시간 가시성을 우선시하고 있습니다. 500MW 이상의 규모로의 전환은 프로젝트 타당성 조사의 핵심에 DCIM이 자리 잡게 됨을 의미합니다.

지속적인 OT-IT 통합의 복잡성과 레거시 BMS의 중복성

레거시 빌딩 관리 시스템은 현대의 DCIM API와 상호 운용되지 않는 독자적인 프로토콜에 의존하는 경우가 많습니다. 그 결과, 운용사들은 센서와 대시보드를 중복으로 도입할 수밖에 없어 자본 지출과 운영 비용을 모두 증가시키면서도 통합된 자산 원장을 구축하지 못하고 있습니다. 커스텀 미들웨어 프로젝트는 업그레이드를 위해 재코딩이 필요하므로 도입 일정이 수개월 지연되고 수명주기 비용이 증가합니다. 멀티 벤더 환경에서는 각 기계 장비 공급업체가 기능을 폐쇄적인 툴 체인에 가두어 종합적인 에너지 최적화를 저해할 수 있습니다.

부문 분석

서비스 매출은 연평균 22.99%의 연평균 복합 성장률(CAGR)로 증가할 것으로 예측됩니다. 이는 운영자의 58%가 자격을 갖춘 시설 엔지니어를 채용하는 데 어려움을 겪고 있다고 답했기 때문입니다. 자산 관리의 도입은 프로젝트 기반 구현에서 지속적인 최적화가 번들로 제공되는 구독형 프레임워크로 전환되고 있습니다. 매니지드 서비스는 AI 클러스터에 따른 액체 냉각 루프의 조정이라는 복잡성도 흡수합니다. 2025년 기준 솔루션이 데이터센터 인프라 관리 시장의 65.55%를 차지했으나, 성과 기반 계약의 부상은 서비스 중심의 미래를 암시하고 있습니다. 기업은 센서 교정, 펌웨어 관리, 컴플라이언스 보고를 아웃소싱하여 인건비 상한선을 설정하는 것을 선호합니다.

엣지 노드의 확대에 따라 네트워크 및 연결성 관리 기능에 대한 수요도 증가하고 있습니다. 한편, 하이퍼스케일 사이트에서는 전력 및 냉각 관리가 여전히 중요하며, 벤더들은 레거시 BMS를 통합하는 액셀러레이터를 제공하여 고객이 단일 관리 화면에서 파악할 수 있도록 하고 있습니다. 이러한 진화는 단발성 소프트웨어 라이선스에서 전문적 지원을 기반으로 한 지속적인 매출 모델로의 전략적 전환을 강조하고 있습니다.

메가 시설(150MW 이상 캠퍼스)은 21.74%의 연평균 복합 성장률(CAGR)로 성장하며, 기존 클라우드 파도를 주도한 매시브 시설을 대체할 것으로 예측됩니다. 운영자는 GPU 상호 연결의 이점이 지연 페널티를 능가하므로 AI 트레이닝 클러스터를 중앙 집중화합니다. 메가캠퍼스는 규모의 경제를 실현하고 여러 홀에서 수랭식 루프를 공유할 수 있게 함으로써 냉각 플랜트 효율을 PUE 1.1 이하로 낮출 수 있습니다. 센서 수가 수백만 개에 달하면서 오케스트레이션의 복잡성이 증가함에 따라 이 부문의 데이터센터 인프라 관리(DCIM) 시장 규모는 빠르게 확대될 것으로 예측됩니다.

메가 스케일 캠퍼스로의 전환은 모듈형 전원 공급 장치 스키드 및 조립식 홀 부문에서의 혁신을 촉진할 것입니다. 이들은 공장 테스트를 거친 DCIM 통합 기능을 갖추고 도입됩니다. 소규모 기업 시설은 지연에 민감한 워크로드를 위한 역할을 유지하지만, 예산 제약으로 인해 고급 디지털 트윈 모듈의 도입은 제한적입니다.

데이터센터 인프라 관리(DCIM) 시장 보고서는 업계를 데이터센터 규모(중소규모, 기타), 도입 형태(On-Premise, 코로케이션), 구성요소(솔루션, 서비스), 최종사용자 산업(IT, 통신, BFSI(은행, 금융, 보험), 기타), 지역(북미, 유럽, 아시아), 기타) 지역(북미, 유럽, 기타)으로 분류하고 있습니다. 시장 예측은 금액(USD) 기준으로 제공됩니다.

지역별 분석

북미는 하이퍼스케일 시설의 건설과 AI 트레이닝 센터의 조기 도입으로 2025년 매출의 41.92%를 차지했습니다. 현지 사업자들은 액체 냉각과 디지털 트윈을 도입하고, 랙 밀도를 50kW 이상으로 높여 DCIM 지출을 확대하고 있습니다. 연방 및 주정부의 에너지 효율화 인센티브는 실시간 모니터링의 비즈니스 사례를 더욱 강화하고 있습니다.

아시아태평양은 중국이 2027년까지 1,250억 달러 규모의 데이터센터 경제를 목표로 하고 있고, 인도가 '디지털 인디아(Digital India)' 구상에 박차를 가하고 있으며, 2031년까지 연평균 복합 성장률(CAGR) 34.12%를 나타낼 것으로 예측됩니다. 일본은 세계 최고 수준의 건설 비용에 직면하고 있으며, 평방미터당 최대 용량을 끌어내는 자동화 DCIM에 대한 관심이 높아지고 있습니다. 싱가포르와 호주는 지역 허브 역할을 하며, 다양한 컴플라이언스 요건을 충족해야 하는 국경을 초월한 클라우드 서비스를 제공합니다.

유럽에서는 에너지 효율화 지침을 배경으로 안정적인 성장세를 유지하고 있습니다. 사업자들은 2024년 9월 보고 기한을 맞추기 위해 기존 시설의 개보수 및 신규 건설 모두에 DCIM을 통합하기 위해 경쟁적으로 노력하고 있습니다. 중동 및 남미 시장에서는 지역 클라우드 프로바이더들이 지연을 줄이기 위해 인프라를 현지화하려는 움직임에 따라 수요가 증가하고 있습니다. 아프리카는 아직 개발도상국이지만, 모바일 인터넷 이용이 증가함에 따라 경량형 DCIM의 도입이 진행될 것으로 예측됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The Data Center Infrastructure Management market was valued at USD 3.62 billion in 2025 and estimated to grow from USD 4.29 billion in 2026 to reach USD 9.99 billion by 2031, at a CAGR of 18.43% during the forecast period (2026-2031).

Growth is propelled by AI-driven thermal loads, mandatory energy-use disclosure rules in the European Union, and a global wave of hyperscale projects that now top 500 MW per campus. Providers increasingly embed predictive analytics to meet cyber-insurance telemetry requirements and to convert regulatory compliance into measurable energy savings. Services linked to managed DCIM operations are accelerating fastest because data-center operators face persistent shortages of facility engineers. Competitive activity centres on integrated hardware-software portfolios that optimise cooling, power, and asset utilisation at rack level. Investors are tying financing costs to verifiable ESG metrics, turning DCIM-verified efficiency into a differentiator for new builds and retrofits.

Global Data Center Infrastructure Management (DCIM) Market Trends and Insights

Accelerated Pursuit of Net-Zero and Mandatory Energy-Use Disclosure

The EU Energy Efficiency Directive requires all data centers above 500 kW to disclose Power Usage Effectiveness, Carbon Usage Effectiveness, and Water Usage Effectiveness by September 2024, repositioning DCIM from optional optimisation software to mandatory compliance infrastructure. Operators that deployed real-time DCIM report 18% energy savings through dynamic capacity forecasting, demonstrating tangible returns on regulatory spending. Multinationals now standardise identical DCIM stacks in every facility to streamline sustainability reporting and to avoid region-specific audits. Demand is spreading beyond Europe because investors demand harmonised ESG disclosures. The directive also covers centres consuming nearly 3% of EU electricity, so incremental efficiency gains translate into region-wide grid relief.

Hyperscale Build-Outs Exceeding 500 MW Clusters

Campus-scale investments such as Compass Datacenters' USD 10 billion Mississippi project require DCIM platforms that coordinate thousands of racks across modular power and cooling skids. Traditional building-management systems cannot deliver rack-level telemetry or predictive failure alerts at gigawatt scale. Integration with prefabricated power modules, exemplified by Siemens' multi-year supply agreement, tightens the link between DCIM software and electrical infrastructure. Operators prioritise real-time visualisation of airflow and capacity to shave operating expenses as capital intensity rises. The shift to 500 MW-plus footprints thus anchors DCIM at the heart of project feasibility studies.

Persistent OT-IT Integration Complexity and Legacy BMS Overlap

Legacy building-management systems often rely on proprietary protocols that do not interoperate with modern DCIM APIs. Operators then duplicate sensors and dashboards, inflating both capex and opex while still lacking a unified asset inventory. Custom middleware projects add months to deployment schedules and raise lifecycle costs because upgrades must be recoded. In multi-vendor estates, each mechanical contractor may lock functionality inside closed toolchains, hampering holistic energy optimisation.

Other drivers and restraints analyzed in the detailed report include:

- Edge and Micro-Data-Center Proliferation for 5G/IoT

- AI/ML-Driven Thermal Loads Demanding Real-Time CFD-Coupled DCIM

- Data-Sovereignty Worries About Cloud-Hosted DCIM Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is projected to climb at 22.99% CAGR because 58% of operators report difficulty hiring qualified facility engineers. Asset-management rollouts now shift from project-based implementations to subscription frameworks that bundle continuous optimisation. Managed services also absorb the complexity of tuning liquid-cooling loops that accompany AI clusters. Though Solutions held 65.55% of Data Center Infrastructure Management market share in 2025, the rise of outcome-based contracts points to a service-centric future. Enterprises prefer to cap labour overheads by outsourcing sensor calibration, firmware management, and compliance reporting.

Demand for Network and Connectivity Management functions also increases as edge nodes expand, while Power and Cooling Management stays critical for hyperscale sites. Vendors package integration accelerators that bridge legacy BMS so clients see a single pane of glass. The evolution underscores a strategic pivot from one-off software licences toward recurring revenue backed by expert support.

Mega facilities, defined as campuses above 150 MW, are expected to post a 21.74% CAGR, displacing Massive facilities that dominated earlier cloud waves. Operators centralise AI training clusters because GPU interconnect benefits outweigh latency penalties. Mega campuses unlock economies of scale, allowing liquid cooling loops to be shared across several halls and driving cooling plant efficiency below 1.1 PUE. The Data Center Infrastructure Management market size for this segment will expand rapidly as orchestration complexity multiplies with sensor counts running into millions.

The migration toward mega-scale campuses also seeds innovation in modular power skids and prefabricated hall segments that arrive with factory-tested DCIM integrations. Smaller enterprise facilities retain a role for latency-sensitive workloads, but budget constraints limit adoption of advanced digital-twin modules.

Data Center Infrastructure Management (DCIM) Market Report Segments the Industry Into Data Center Size(Small and Medium, and More), Deployment Type (On -Premise, Colocation), Component(solutions, Services), End-User Industry(IT and Telecom, BFSI and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 41.92% of 2025 revenue thanks to hyperscale builds and early adoption of AI training centres. Operators there deploy liquid cooling and digital twins to push rack densities past 50 kW, amplifying DCIM spending. Federal and state energy-efficiency incentives further reinforce the business case for real-time monitoring.

Asia-Pacific is forecast to grow at 34.12% CAGR through 2031 as China targets a USD 125 billion data-center economy by 2027 and India accelerates under the Digital India initiative. Japan faces the world's highest construction costs, driving interest in automated DCIM to extract maximum capacity from every square metre. Singapore and Australia act as regional hubs, supplying cross-border cloud services that must meet diverse compliance mandates.

Europe maintains steady expansion on the back of the Energy Efficiency Directive. Operators race to meet September 2024 reporting deadlines, integrating DCIM into both brownfield retrofits and new builds. Middle Eastern and South American markets show rising demand as regional cloud providers localise infrastructure to cut latency. Africa remains nascent but is expected to adopt lightweight DCIM as mobile-internet use increases.

- Schneider Electric SE

- Vertiv Group Corp.

- ABB Ltd

- Eaton Corporation plc

- Johnson Controls International plc

- IBM Corporation

- Siemens AG

- CommScope (Nlyte and iTRACS)

- Sunbird Software

- FNT GmbH

- Device42

- Panduit Corp.

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd

- Raritan Inc. (Legrand)

- Siemens Smart Infrastructure

- EkkoSense Ltd

- RFcode Inc.

- Modius Inc.

- OpenDCIM (open-source)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated pursuit of net-zero and mandatory energy-use disclosure

- 4.2.2 Hyperscale build-outs exceeding 500 MW clusters

- 4.2.3 Edge and micro-data-center proliferation for 5G/IoT

- 4.2.4 AI/ML-driven thermal loads demanding real-time CFD-coupled DCIM

- 4.2.5 Cyber-insurance policies now requiring DCIM-based risk telemetry

- 4.2.6 ESG-linked financing that scores DCIM-verified efficiency metrics

- 4.3 Market Restraints

- 4.3.1 Persistent OT-IT integration complexity and legacy BMS overlap

- 4.3.2 Data-sovereignty worries about cloud-hosted DCIM platforms

- 4.3.3 Shortage of DCIM-literate facility engineers

- 4.3.4 Rising AI rack densities outpacing sensor network retrofits

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macro Economic Trends on the Market

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Asset and Capacity Management

- 5.1.1.2 Power and Cooling Management

- 5.1.1.3 Network and Connectivity Management

- 5.1.2 Services

- 5.1.2.1 Consulting and Integration

- 5.1.2.2 Managed and Support Services

- 5.1.1 Solutions

- 5.2 By Data-Center Size

- 5.2.1 Small

- 5.2.2 Medium

- 5.2.3 Large

- 5.2.4 Massive

- 5.2.5 Mega

- 5.3 By Deployment Mode

- 5.3.1 On-premise

- 5.3.2 Colocation

- 5.3.2.1 Retail Colo

- 5.3.2.2 Wholesale / Hyperscale Colo

- 5.3.3 Cloud / DCIM-as-a-Service

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life-Sciences

- 5.4.4 Government and Defence

- 5.4.5 Manufacturing and Industrial

- 5.4.6 Retail and E-commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Singapore

- 5.5.3.5 Australia

- 5.5.3.6 Malaysia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Chile

- 5.5.4.3 Argentina

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirate

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Vertiv Group Corp.

- 6.4.3 ABB Ltd

- 6.4.4 Eaton Corporation plc

- 6.4.5 Johnson Controls International plc

- 6.4.6 IBM Corporation

- 6.4.7 Siemens AG

- 6.4.8 CommScope (Nlyte and iTRACS)

- 6.4.9 Sunbird Software

- 6.4.10 FNT GmbH

- 6.4.11 Device42

- 6.4.12 Panduit Corp.

- 6.4.13 Cisco Systems Inc.

- 6.4.14 Huawei Technologies Co. Ltd

- 6.4.15 Raritan Inc. (Legrand)

- 6.4.16 Siemens Smart Infrastructure

- 6.4.17 EkkoSense Ltd

- 6.4.18 RFcode Inc.

- 6.4.19 Modius Inc.

- 6.4.20 OpenDCIM (open-source)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment