|

시장보고서

상품코드

1939730

유틸리티 빌링 소프트웨어 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Utility Billing Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

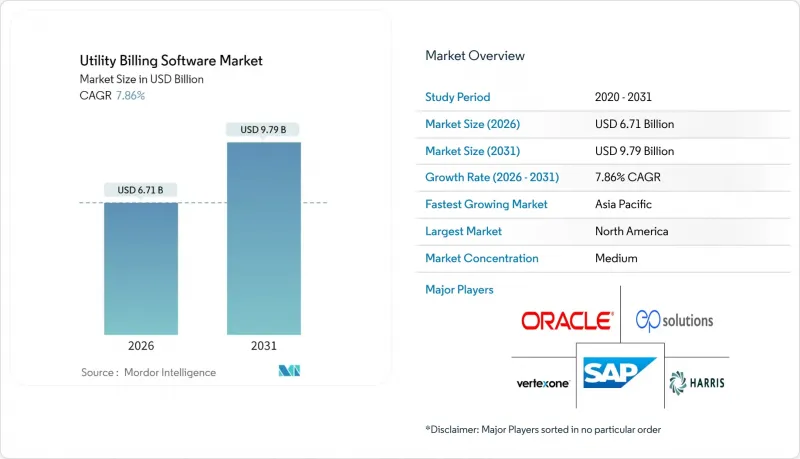

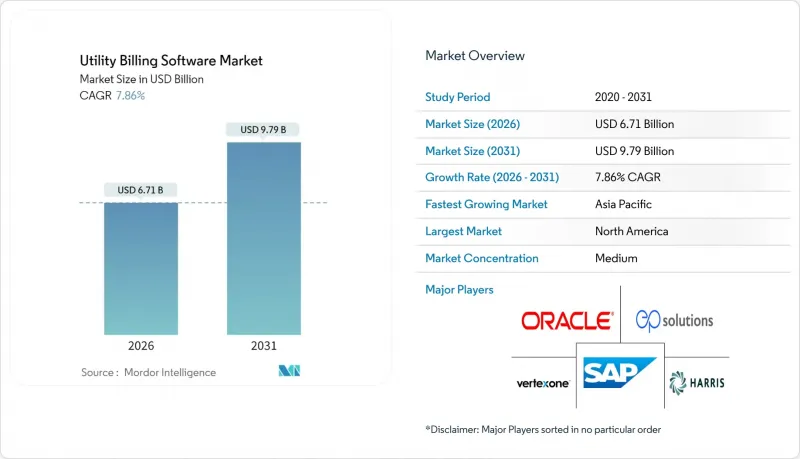

유틸리티 빌링 소프트웨어 시장은 2025년에 62억 2,000만 달러로 평가되며, 2026년 67억 1,000만 달러에서 2031년까지 97억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 7.86%로 예상됩니다.

엄격한 규제 일정, 가속화되는 스마트 그리드 계획, 레거시 메인프레임의 폐기 압력으로 인해 현대적 플랫폼에 대한 지속적인 투자가 추진되고 있습니다. 클라우드 우선 배포 전략, 탄력적인 분석 워크로드, 거의 실시간에 가까운 요금 엔진은 지자체 및 투자자 소유의 유틸리티 회사 모두에서 벤더의 빠른 채택을 지원하고 있습니다. VertexOne의 최근 자금 조달과 인수합병으로 대표되는 통합 활동은 유틸리티 빌링 소프트웨어 시장에 대한 사모펀드의 신뢰가 높아졌음을 보여줍니다. 동시에, 유틸리티 사업자들은 증가하는 사이버 위험에 직면하고 있으며, 보안 기능이 옵션에서 핵심 구매 기준으로 격상되고 있습니다. 전력, 수도, 가스, 통신 서비스 전반에 걸친 통합 청구에 대한 수요는 플랫폼 벤더의 잠재 고객 기반을 더욱 확장하고 있습니다.

세계 유틸리티 빌링 소프트웨어 시장 동향 및 인사이트

스마트그리드/AMI 도입 투자 확대

AMI(Advanced Metering Infrastructure) 프로그램은 기존 일괄 처리 시스템으로는 관리할 수 없는 고빈도 사용 데이터를 유틸리티 사업자에게 대량으로 제공함으로써 지속적인 플랫폼 수요를 창출하고 있습니다. 인도의 '배전 부문 개혁 계획'만 해도 2026년까지 2억 5,000만개 도입을 목표로 하고 있으며, 150억 달러의 투자 약속이 지원되고 있습니다. DBFOOT(Design, Build, Finance, Operate, Own, Transfer) 모델은 자본 위험을 서비스 프로바이더에게 이전하여 유틸리티 빌링 소프트웨어 시장에서 지속적인 SaaS 수입원을 보장합니다. 각 가정용 스마트미터는 연간 3만 5,000건 이상의 계측값을 생성하므로 유틸리티 사업자는 탄력적으로 확장 가능한 클라우드 네이티브 청구 엔진을 우선시할 수밖에 없습니다.

클라우드 우선의 유틸리티 비즈니스 IT 아키텍처로 빠르게 전환

유틸리티 사업자들이 고객 정보 시스템 및 요금 부과 엔진을 멀티테넌트 SaaS 환경으로 전환하는 가운데, Oracle의 클라우드 매출은 2025년 2분기 전년 동기 대비 24% 증가한 59억 달러에 달했습니다. 클라우드 프레임워크는 새로운 요금제 도입 주기를 몇 개월에서 몇 주 단위로 단축시켜 규제 당국이 동적 시간대별 요금을 승인할 때 중요한 이점을 제공합니다. 초기 비용 절감으로 중규모 지자체 전력회사도 기존에는 민간 기업만 사용할 수 있었던 고급 기능을 사용할 수 있게 되면서 유틸리티 과금 소프트웨어 시장은 롱테일 고객층으로 확대되고 있습니다.

높은 초기 통합 및 데이터 마이그레이션 비용

레거시 CIS를 변환하려면 수십 년간의 기록 정리와 스키마 조정이 필요하므로 프로젝트 예산의 40-60%를 소비하는 경우가 많습니다. 5만 명 미만의 고객을 보유한 소규모 전력 사업자는 전담 IT 인력이 부족하고, 외부 컨설턴트에 의존할 수밖에 없어 총 도입 비용이 두 배로 증가합니다. 이러한 비용 장벽은 구독형 SaaS 솔루션으로 상쇄되지 않는 한 현대화를 지연시키며, 이러한 추세는 자본 지출에서 운영 예산으로 비용이 이동하는 결과를 초래하고 있습니다.

부문 분석

클라우드 플랫폼은 2025년 매출의 43.62%를 차지하고 2031년까지 연평균 복합 성장률(CAGR) 13.52%를 나타낼 것으로 예측되며, 유틸리티 빌링 소프트웨어 시장의 주요 성장 동력이 될 것으로 예측됩니다. 대규모 투자자 소유의 유틸리티 기업에서는 기존 데이터센터 투자가 매몰비용으로 작용하여 On-Premise 도입이 지속되고 있지만, 그 확대는 제한적입니다. 하이브리드 배포는 브리지 아키텍처 역할을 하며, 규제 대상 유틸리티 회사가 민감한 고객 데이터를 On-Premise에서 보호하면서 공공 클라우드에서 계량기 데이터 처리를 확장할 수 있도록 지원합니다.

비용 탄력성과 항상 최신 기능 세트가 지자체 사업자들이 SaaS로 전환하는 이유입니다. MuniBilling에 따르면 하드웨어 업데이트 주기 없이 실시간 보고를 원하는 수도 유틸리티 수요가 증가하고 있다고 합니다. Oracle 클라우드 인프라의 2025년 매출 52% 증가는 기업 규모의 전환 모멘텀을 보여주며, 유틸리티 청구 소프트웨어 시장에서 하이퍼스케일러의 역할을 강화하고 있습니다.

2025년 기준 전력 유통 사업자는 40.41%의 매출 점유율을 차지할 것으로 예상되며, 이는 레거시 시스템의 복잡성과 스마트그리드 투자 의무화를 반영하고 있습니다. 한편, 통신사업자는 5G 확산에 따른 데이터, 음성, 에너지 서비스를 단일 청구서로 통합하는 과금 시스템에 대한 수요로 인해 12.71%의 연평균 복합 성장률(CAGR)로 성장을 주도하고 있습니다. 수도사업자는 스마트미터 보급이 늦어지면서 뒤쳐져 있지만, 안정적인 갱신 수요가 존재합니다.

초기 통신사업자를 위해 개발된 실시간 요금 계산 엔진(예: Neural Technologies의 플랫폼)은 현재 시간대별 요금 체계에도 전환되어 대응 가능한 기능 범위가 확대되고 있습니다. 이러한 융합을 통해 유틸리티 빌링 소프트웨어 산업은 업계 전반의 사업자들이 통합된 고객 경험을 추구하면서 강화되고 있습니다.

지역별 분석

북미는 2025년 전 세계 매출의 37.62%를 차지할 것으로 예상되며, 이는 첨단 규제 프레임워크와 노후화된 전력망 자산의 갱신 주기가 기반이 되고 있습니다. 스마트 미터의 광범위한 보급과 각 주별 투명성 확보 규칙이 높은 지출 수준을 유지하고 있습니다. 캐나다의 전국적인 계량기 교체 계획과 멕시코의 배전 부문 개혁이 수요를 증가시키고 있지만, 미국은 여전히 핵심 수입원입니다. 디지털 퍼스트 벤더에 대한 벤처캐피털의 유입은 이 지역의 성숙도와 기능 로드맵에 대한 과도한 영향력을 지원합니다.

아시아태평양은 10.02%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장을 기록했습니다. 인도의 2억 5,000만 미터 계획과 중국의 AI 중심 송배전망 현대화가 그 견인차 역할을 하고 있습니다. 정부 주도의 자금 조달 메커니즘은 조달 장벽을 낮추고, 적극적인 일정은 입찰 물량을 가속화하고 있습니다. 일본의 요금 자유화와 호주의 지붕 설치형 태양광 붐은 환태평양 지역의 유틸리티 과금 소프트웨어 시장을 더욱 확대시킬 것입니다.

유럽에서는 전력회사들이 재생에너지의 높은 보급률에 대응하고 GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정)을 준수하는 가운데 꾸준한 갱신 수요가 발생하고 있습니다. 독일, 네덜란드, 북유럽 국가들의 광범위한 프로슈머 결제 및 V2G(차량에서 그리드로의 전력 공급) 시범 사업은 과금 업무의 복잡성을 증가시키고 있습니다. 엄격한 개인정보 보호 규정은 조달 주기를 연장시키지만, 인증된 데이터 처리 프로세스를 가진 기존 벤더를 우대하여 경쟁 우위를 강화하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 동향

KSA 26.03.06The utility billing software market was valued at USD 6.22 billion in 2025 and estimated to grow from USD 6.71 billion in 2026 to reach USD 9.79 billion by 2031, at a CAGR of 7.86% during the forecast period (2026-2031).

Tight regulatory timelines, accelerating smart-grid programs, and pressure to retire legacy mainframes propel sustained investments in modern platforms. Cloud-first deployment strategies, elastic analytics workloads, and near-real-time tariff engines underpin rapid vendor adoption among both municipal and investor-owned utilities. Consolidation activity-exemplified by VertexOne's recent financing and acquisition spree-signals growing private-equity confidence in the utility billing software market. At the same time, utilities confront mounting cyber-risk exposures that elevate security features from optional extras to core buying criteria. Demand for convergent billing across electricity, water, gas, and telecom services further widens the addressable base for platform vendors.

Global Utility Billing Software Market Trends and Insights

Growing Investment in Smart-Grid / AMI Roll-outs

Advanced metering infrastructure programs generate sustained platform demand by flooding utilities with high-frequency usage data that legacy batch systems cannot manage. India's Revamped Distribution Sector Scheme alone targets 250 million installations by 2026, supported by USD 15 billion investment commitments. The design-build-finance-operate-own-transfer model shifts capital risk to service providers, guaranteeing recurring SaaS revenue streams for the utility billing software market. Each residential smart meter produces more than 35,000 readings annually, forcing utilities to favor cloud-native billing engines that scale elastically.

Rapid Shift Toward Cloud-First Utility IT Architectures

Oracle's cloud revenue climbed to USD 5.9 billion in Q2 FY2025-up 24% year on year-as utilities migrate customer information systems and tariff engines into multi-tenant SaaS environments. Cloud frameworks shorten new-tariff launch cycles from months to weeks, a critical advantage when regulators approve dynamic time-of-use pricing. Lower upfront costs enable mid-sized municipal utilities to access feature depth once reserved for investor-owned enterprises, expanding the utility billing software market footprint among long-tail customers.

High Upfront Integration and Data-Migration Costs

Legacy CIS conversion often consumes 40-60% of project budgets because decades-old records require cleansing and schema alignment. Small public-power utilities serving fewer than 50 000 customers lack dedicated IT staff, pushing them toward external consultants that double total implementation expense. These cost hurdles delay modernization unless offset by subscription-based SaaS alternatives, a trend that nonetheless shifts expense from capital to operating budgets.

Other drivers and restraints analyzed in the detailed report include:

- Compliance Pressure for Itemised, Near-Real-Time Billing

- AI-Based Anomaly Detection Reducing Non-Technical Losses

- Escalating Cyber-Security and Data-Privacy Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud platforms captured 43.62% of 2025 revenue and will post a 13.52% CAGR to 2031, underscoring their status as the primary growth engine for the utility billing software market. On-premise implementations persist among large investor-owned utilities with sunk-cost datacenters, yet expansion remains muted. Hybrid rollouts act as bridge architectures, allowing regulated utilities to protect sensitive customer data on-premise while scaling meter-data crunching in public clouds.

Cost elasticity and always-current feature sets explain why municipal operators pivot toward SaaS. MuniBilling reports rising demand from water districts seeking real-time reporting without hardware refresh cycles. Oracle Cloud Infrastructure's 52% revenue jump in fiscal 2025 illustrates enterprise-scale migration momentum, reinforcing the role of hyperscalers in the utility billing software market.

Electricity distributors held 40.41% revenue share in 2025, reflecting legacy complexity and mandatory smart-grid investments. Telecommunications utilities, however, lead growth at 12.71% CAGR as 5G rollouts demand convergent charging systems that reconcile data, voice, and energy services on a single invoice. Water utilities trail due to slower smart-meter penetration, but present stable replacement demand.

Real-time rating engines originally built for telcos-such as Neural Technologies' platform-are now repurposed for time-of-use energy tariffs, widening addressable functionality. This convergence bolsters the utility billing software industry as cross-sector operators seek unified customer journeys.

The Utility Billing Software Market Report is Segmented by Deployment Mode (On-Premise, Cloud, Hybrid), End-User Industry (Water Utilities, and More), Utility Type (Electricity, Water, and More), Billing-Function Module (Customer Information System, Meter Data Management, and More), Organisation Size (Investor-Owned Utilities, Municipal, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 37.62% of global revenue in 2025, anchored by advanced regulatory frameworks and aging grid assets that mandate upgrade cycles. Widespread smart-meter penetration and state-specific transparency rules keep spending elevated. Canada's nationwide meter refresh and Mexico's distribution-sector reforms add incremental demand, though the United States remains the core revenue pool. Venture capital inflows into digital-first vendors underscore the region's maturity and its outsized influence on functional roadmaps.

Asia-Pacific posts the fastest growth at 10.02% CAGR, propelled by India's 250 million-meter program and China's AI-centric grid modernization. Government-led funding mechanisms lower procurement barriers, while aggressive timelines accelerate tender volumes. Japan's tariff liberalization and Australia's rooftop solar boom further expand the utility billing software market across the Pacific Rim.

Europe delivers steady replacement demand as utilities integrate high renewable penetration and comply with GDPR. Extensive prosumer settlements and vehicle-to-grid pilots in Germany, the Netherlands, and the Nordics elevate billing complexity. Stringent privacy rules lengthen procurement cycles but favor established vendors with certified data processes, fortifying competitive moats.

- Oracle Corporation

- SAP SE

- Hansen Technologies Limited

- N. Harris Computer Corporation

- VertexOne, LLC

- Tyler Technologies, Inc.

- EnergyCAP, LLC

- Bynry Technologies Pvt. Ltd.

- Starnik Systems, Inc.

- MuniBilling, LLC

- Gentrack Group Limited

- Itineris NV

- Fluentgrid Limited

- Open International LLC

- Paymentus Holdings, Inc.

- ePsolutions, Inc.

- Utilibill Pty. Ltd.

- Jayhawk Software, Inc.

- Banyon Data Systems, Inc.

- Exceleron Software, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Improvement in legacy billing systems and IT infrastructure

- 4.2.2 Growing investment in smart-grid / AMI roll-outs

- 4.2.3 Rapid shift toward cloud-first utility IT architectures

- 4.2.4 Compliance pressure for itemised, near-real-time billing

- 4.2.5 Rise of "prosumer" and V2G settlement requirements

- 4.2.6 AI-based anomaly detection reducing non-technical losses

- 4.3 Market Restraints

- 4.3.1 Digital-skills gap at small and mid-size utilities

- 4.3.2 High upfront integration and data-migration costs

- 4.3.3 Escalating cyber-security and data-privacy risks

- 4.3.4 Workforce resistance from unionised meter-reading staff

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By End-user Industry

- 5.2.1 Water Utilities

- 5.2.2 Electricity and Power Distribution

- 5.2.3 Gas Utilities

- 5.2.4 Telecommunications

- 5.2.5 Multi-service Municipal Utilities

- 5.3 By Utility Type

- 5.3.1 Electricity

- 5.3.2 Water

- 5.3.3 Gas

- 5.3.4 District Heating and Cooling

- 5.4 By Billing-Function Module

- 5.4.1 Customer Information System (CIS)

- 5.4.2 Meter Data Management (MDM)

- 5.4.3 Payment Processing and Collections

- 5.4.4 Analytics and Reporting

- 5.4.5 Tariff and Rate Management

- 5.5 By Organisation Size

- 5.5.1 Investor-Owned Utilities (IOU)

- 5.5.2 Municipal / Cooperative Utilities

- 5.5.3 Private Retail Energy Providers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level overview, Market-level overview, Core segments, Financials as available, Strategic information, Market rank/share, Products and services, Recent developments)

- 6.4.1 Oracle Corporation

- 6.4.2 SAP SE

- 6.4.3 Hansen Technologies Limited

- 6.4.4 N. Harris Computer Corporation

- 6.4.5 VertexOne, LLC

- 6.4.6 Tyler Technologies, Inc.

- 6.4.7 EnergyCAP, LLC

- 6.4.8 Bynry Technologies Pvt. Ltd.

- 6.4.9 Starnik Systems, Inc.

- 6.4.10 MuniBilling, LLC

- 6.4.11 Gentrack Group Limited

- 6.4.12 Itineris NV

- 6.4.13 Fluentgrid Limited

- 6.4.14 Open International LLC

- 6.4.15 Paymentus Holdings, Inc.

- 6.4.16 ePsolutions, Inc.

- 6.4.17 Utilibill Pty. Ltd.

- 6.4.18 Jayhawk Software, Inc.

- 6.4.19 Banyon Data Systems, Inc.

- 6.4.20 Exceleron Software, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment