|

시장보고서

상품코드

1939733

영국의 포장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United Kingdom Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

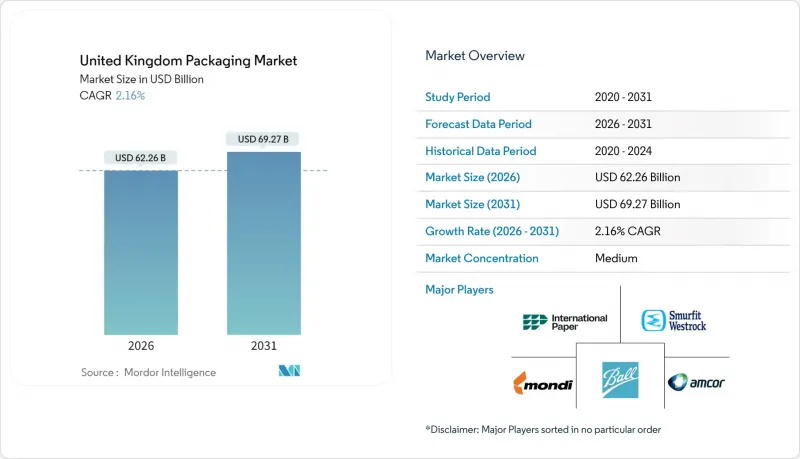

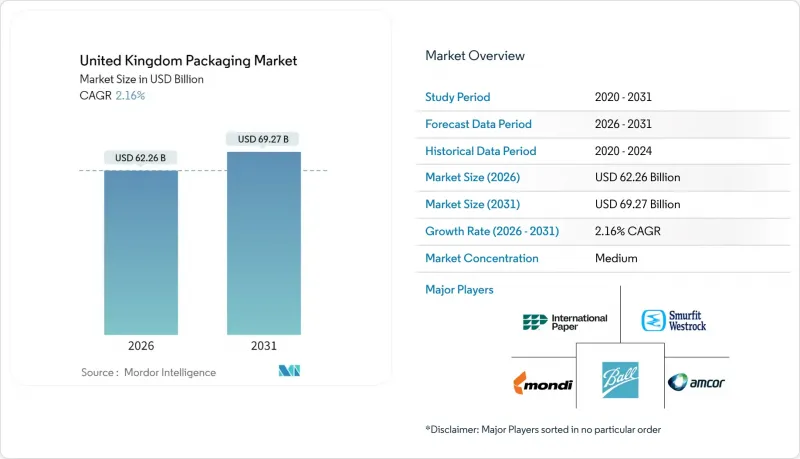

2026년 영국 포장 시장 규모는 622억 6,000만 달러로 추정되며, 2025년 609억 4,000만 달러에서 성장이 전망됩니다. 2031년까지의 예측에서는 692억 7,000만 달러에 달하며, 2026-2031년에 CAGR 2.16%로 확대할 전망입니다.

현재의 모멘텀은 브렉시트 이후 국경 규제, 강화되는 환경 규제, E-Commerce의 가속화, 눈에 띄는 비용 인플레이션으로 형성된 성숙하면서도 꾸준히 진화하는 상황을 반영하고 있습니다. 국경 목표 운영 모델(BTOM)에 기반한 구조 조정으로 인해 컴플라이언스 업무량이 증가하고 리드타임이 연장됨에 따라 생산자는 원자재 현지 조달 및 통관 서류의 자동화를 추진했습니다. 이와 함께 영국의 플라스틱 포장세 확대와 확대 생산자책임제도의 전면 도입이 진행되면서 재활용 가능성에 대한 관심이 높아졌습니다. 이에 따라 종이, 단일 소재 플라스틱, 바이오필름으로 빠르게 대체되고 있습니다. 온라인 소매가 국내 판매의 31.3%를 차지하면서 연포장의 점유율이 확대되고, 부가가치 인쇄 기능을 통해 브랜드는 비용 효율적으로 틈새 고객층을 공략할 수 있게 되었습니다. 업계 재편은 계속되고 있으며, 국제제지가 DS Smith를 75억 4,000만 달러에 인수한 것이 눈에 띕니다. 이로 인해 지역 최대 골판지 공급업체가 탄생하는 한편, 반독점법 감시가 강화되었습니다.

영국 포장 시장 동향 및 인사이트

E-Commerce의 확대가 골판지 플렉서블 메일러 수요를 견인

2024년 온라인 소매 매출은 국내 총매출의 31.3%로 급증했고, 골판지 상자 및 플렉서블 메일러의 출하량은 23% 증가했습니다. 게틸과 같은 퀵커머스 업체들은 변조 방지 기능과 단열성을 겸비한 단품 포장을 장려했습니다. 아마존의 자동 포장 라인은 포장재 사용량을 15% 절감하고, 배송 처리 능력을 가속화하며, 새로운 효율성의 기준을 세웠습니다. HelloFresh의 정기 구매 모델은 반품 가능한 단열재에 대한 수요를 확대시켰고, 마켓플레이스 판매자들은 부피 중량 요금을 억제하기 위해 적정 크기의 우편 봉투를 선택하는 경향이 강해졌습니다. 이러한 추세는 영국 포장 시장에서 골판지 및 연포장의 지속적인 성장을 지원하고 있습니다.

영국의 플라스틱 세금으로 인한 재생 및 바이오소재로의 전환

2024년 확대된 플라스틱 포장세는 재생재 함량이 30% 미만인 폴리머에 대해 톤당 200파운드(263달러)의 세금을 부과하여 재생원료 채택률을 35% 증가시켰습니다. 유니레버, 영국 퍼스널케어 제품 라인에서 재활용 플라스틱 50% 달성,네슬레, 2025년까지 완전 재활용 가능한 솔루션을 약속합니다. 버진 수지 가격이 재생원료 가격보다 18% 이상 차이가 확대되어 수직계열화된 재활용 사업자에게 유리한 상황입니다. 대규모 컨버터의 평균 규제 대응 비용은 230만 파운드(302만 달러)에 달하며, 세척 플레이크 처리 능력과 화학적 재활용 시범 사업에 대한 자본 유입을 촉진하고 있습니다. 이러한 지속가능성 요구사항으로 인해 영국 포장 시장 전체에서 소재 포트폴리오 재구성이 가속화되고 있습니다.

수지 및 종이 원료 가격 급등

폴리에틸렌 수지 가격은 2024년 22% 급등했고, 재생용지도 에너지 비용 상승과 공급 제약으로 인해 18% 상승했습니다. 몬디의 영국 사업부는 340bp의 이익률 하락을 보고했으며, 하류 가격 인상으로 인해 수요 탄력성이 억제되었습니다. 컨버터 업체들은 지속적인 공급을 위해 안전재고 기준을 25-30% 상향 조정했으나, 보관비용이 운전자금을 압박하고 있습니다. 에너지 집약적인 압출 라인은 피크 요금 시간대에 생산을 억제하고, 변동성이 영국 포장 시장의 단기적인 걸림돌로 작용하고 있음을 강조했습니다.

부문 분석

2025년 기준 플라스틱은 영국 포장 시장 점유율의 48.02%를 차지할 것으로 예상되며, 식품, 음료, 퍼스널케어 분야에서의 다용도성이 그 기반이 될 것으로 보입니다. 경질 PET병의 경량화로 지난 10년간 재료 질량이 25% 감소했고, 사용한 수지의 통합으로 재활용 재료 함량의 신뢰성이 향상되었습니다. 그러나 세제 기준 강화와 소매업체들의 플라스틱 제로 선언으로 인해 성장세는 종이 소재로 옮겨가고 있습니다. E-Commerce용 골판지 수요 증가에 따라 종이 소재는 2031년까지 연평균 복합 성장률(CAGR) 4.62%로 가장 빠른 성장세를 보일 것으로 예측됩니다. 단일 소재 설계로 가정 쓰레기 수거가 간소화됨에 따라 영국 포장지 기판 시장 규모는 계속 확대될 것으로 예측됩니다.

유리와 금속은 무한한 재활용 가능성과 높은 품질감으로 고급 음료 분야에서 존재감을 회복하며 각각 3.2%, 4.1%의 연간 성장률을 견인하고 있습니다. 수제 맥주 양조장들이 알루미늄의 경량성과 급속 냉각 특성을 활용하면서 음료 캔 수요가 급증했고, 수량 효율화를 통해 원재료 비용 상승을 상쇄했습니다. 한편, 생분해성 고분자 필름은 퇴비화 가능성이 가격 프리미엄을 창출하는 특수 용도 분야로 진출했습니다. 이러한 변화는 플라스틱의 우위가 지속되는 가운데, 지속가능성 기준이 영국 포장 시장에서의 소재 선택에 영향을 미치면서 플라스틱의 우위가 약간 줄어들고 있음을 보여줍니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05United Kingdom packaging market size in 2026 is estimated at USD 62.26 billion, growing from 2025 value of USD 60.94 billion with 2031 projections showing USD 69.27 billion, growing at 2.16% CAGR over 2026-2031.

Current momentum reflects a mature yet steadily evolving landscape shaped by post-Brexit border rules, tighter environmental mandates, e-commerce acceleration and pronounced cost inflation. Structural adjustments under the Border Target Operating Model raised compliance workloads and stretched lead times, prompting producers to localize inputs and automate customs documentation. Parallel expansion of the United Kingdom Plastic Packaging Tax and full roll-out of Extended Producer Responsibility sharpened the focus on recyclability, driving rapid substitution toward paper, mono-material plastics and bio-based films. Flexible formats gained share as online retail reached 31.3% of national sales, and value-added printing capabilities helped brands target niche audiences cost-effectively. Consolidation continued, highlighted by International Paper's USD 7.54 billion acquisition of DS Smith, which created the region's largest corrugated supplier but intensified antitrust scrutiny.

United Kingdom Packaging Market Trends and Insights

Rising E-commerce Driven Demand for Corrugated and Flexible Mailers

Online retail sales surged to 31.3% of national turnover in 2024, lifting shipment volumes for corrugated boxes and flexible mailers by 23%. Quick-commerce operators such as Getir stimulated single-portion packaging that combines tamper evidence with thermal integrity. Amazon's automated packing lines cut packaging material intensity 15% and accelerated outbound throughput, setting new efficiency benchmarks. Subscription models from HelloFresh amplified demand for returnable insulation, while marketplace sellers gravitated toward right-sized mailers that curb dimensional-weight charges. These developments support continued expansion of corrugated and flexible formats within the United Kingdom packaging market.

Shift Toward Recyclable and Biobased Materials Due to United Kingdom Plastic Tax

The Plastic Packaging Tax extension in 2024 imposed a GBP 200 (USD 263) per-tonne levy on polymers lacking 30% recycled content, encouraging a 35% jump in reclaimed feedstock adoption. Unilever achieved 50% recycled plastic in United Kingdom personal-care lines, while Nestle pledged fully recyclable solutions by 2025. Rising virgin resin differentials 18% above recycled inputs favor vertically integrated recyclers. Average compliance outlays reached GBP 2.3 million (USD 3.02 million) for large converters, prompting capital flows into wash-flake capacity and chemical recycling pilots. Sustainability requirements therefore accelerate material portfolio realignment across the United Kingdom packaging market.

High Raw-Material Price Volatility for Resins and Paper

Polyethylene resin prices jumped 22% in 2024, while recycled paper climbed 18% on energy cost spikes and supply constraints. Mondi's United Kingdom operations reported 340-basis-point margin erosion, triggering downstream price hikes that tempered demand elasticity. Converters raised safety-stock thresholds 25-30% to secure continuity, yet carrying costs strained working capital. Energy-intensive extrusion lines curtailed output during peak tariff windows, underscoring volatility as a short-term drag on the United Kingdom packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization and Luxury Packaging Demand from Millennials and Tourism

- Growing FMCG Private Label Expansion in Discount Channels Requiring Cost-Efficient Packaging

- Strict United Kingdom Regulations on Single-Use Plastics and Extended Producer Responsibility Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic accounted for 48.02% of the United Kingdom packaging market share in 2025, underpinned by its versatility across food, beverage and personal-care categories. Rigid PET bottle light-weighting shaved 25% material mass over the decade while integration of post-consumer resin boosted recycled content credibility. Yet tightening tax thresholds and retailer zero-plastic pledges pivot growth toward paper, which delivers the fastest 4.62% CAGR through 2031 on expanding e-commerce corrugated volumes. The United Kingdom packaging market size for paper substrates will continue to widen as mono-material designs simplify curbside recycling.

Glass and metal regained relevance in premium drinks due to infinite recyclability and high perceived quality, contributing 3.2% and 4.1% respective annual growth. Beverage can volumes surged as craft breweries exploited aluminum's light weight and rapid chilling properties, offsetting higher input costs via volume efficiencies. Meanwhile, bio-polymer films entered specialty applications where compostability commands price premiums. These shifts indicate that plastic's leadership persists but erodes marginally as sustainability criteria increasingly influence material selection within the United Kingdom packaging market.

The United Kingdom Packaging Market Report is Segmented by Packaging Type (Plastic, Paper, Container Glass, Metal Cans), Packaging Format (Flexible, Rigid), End-Use Industry (Food, Beverage, Pharmaceuticals, Personal Care, Industrial, E-Commerce). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- International Paper Company

- Smurfit WestRock

- Amcor plc

- Mondi plc

- Ball Corporation

- Crown Holdings Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Graphic Packaging International LLC

- Greif Inc.

- Silgan Holdings Inc.

- AptarGroup Inc.

- Huhtamaki Oyj

- Tetra Pak International SA

- CAN-PACK UK Ltd.

- Ardagh Group S.A.

- RPC Group Ltd.

- Klckner Pentaplast Ltd.

- Coveris Holdings S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising e Commerce driven demand for corrugated and flexible mailers

- 4.2.2 Shift towards recyclable and biobased materials due to United Kingdom Plastic Tax

- 4.2.3 Premiumization and luxury packaging demand from millennials and tourism

- 4.2.4 Growing FMCG private label expansion in discount channels requiring cost-efficient packaging

- 4.2.5 Growth of dark kitchens and quick commerce creating single-portion packaging needs

- 4.2.6 Adoption of digital printing for short runs enabling customization for SME brands

- 4.3 Market Restraints

- 4.3.1 High raw-material price volatility for resins and paper

- 4.3.2 Strict United Kingdom regulations on single-use plastics and Extended Producer Responsibility costs

- 4.3.3 Supply-chain disruptions post-Brexit impacting imported packaging components

- 4.3.4 Labor shortages in manufacturing and logistics escalating operational costs

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Type

- 5.1.1 Plastic Packaging

- 5.1.1.1 By Type

- 5.1.1.1.1 Rigid Plastic Packaging

- 5.1.1.1.1.1 By Material Type

- 5.1.1.1.1.1.1 Polyethylene (PE)

- 5.1.1.1.1.1.2 Polypropylene (PP)

- 5.1.1.1.1.1.3 Polyethylene Terephthalate (PET)

- 5.1.1.1.1.1.4 Polyvinyl Chloride (PVC)

- 5.1.1.1.1.1.5 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.1.1.1.1.1.6 Other Material Types

- 5.1.1.1.1.2 By Product Type

- 5.1.1.1.1.2.1 Bottles and Jars

- 5.1.1.1.1.2.2 Caps and Closures

- 5.1.1.1.1.2.3 Trays and Containers

- 5.1.1.1.1.2.4 Other Product Types

- 5.1.1.1.1.3 By End-use Industry

- 5.1.1.1.1.3.1 Food

- 5.1.1.1.1.3.2 Beverage

- 5.1.1.1.1.3.3 Pharmaceutical

- 5.1.1.1.1.3.4 Cosmetics and Personal Care

- 5.1.1.1.1.3.5 Industrial

- 5.1.1.1.1.3.6 Other End-use Industry

- 5.1.1.1.1.1 By Material Type

- 5.1.1.1.2 Flexible Plastic Packaging

- 5.1.1.1.2.1 By Material Type

- 5.1.1.1.2.1.1 Polyethylene (PE)

- 5.1.1.1.2.1.2 Biaxially Oriented Polypropylene (BOPP)

- 5.1.1.1.2.1.3 Cast Polypropylene (CPP)

- 5.1.1.1.2.1.4 Other Material Types

- 5.1.1.1.2.2 By Product Type

- 5.1.1.1.2.2.1 Pouches and Bags

- 5.1.1.1.2.2.2 Films and Wraps

- 5.1.1.1.2.2.3 Other Product Types

- 5.1.1.1.2.3 By End-use Industry

- 5.1.1.1.2.3.1 Food

- 5.1.1.1.2.3.2 Beverage

- 5.1.1.1.2.3.3 Pharmaceutical

- 5.1.1.1.2.3.4 Cosmetics and Personal Care

- 5.1.1.1.2.3.5 Industrial

- 5.1.1.1.2.3.6 Other End-use Industry

- 5.1.1.1.2.1 By Material Type

- 5.1.1.1.1 Rigid Plastic Packaging

- 5.1.1.2 By Product Type

- 5.1.1.2.1 Bottles and Jars

- 5.1.1.2.2 Pouches and Bags

- 5.1.1.2.3 Bulk-Grade Products

- 5.1.1.2.4 Other Product Types

- 5.1.1.3 By End-use Industry

- 5.1.1.3.1 Food

- 5.1.1.3.2 Beverages

- 5.1.1.3.3 Cosmetics and Personal Care

- 5.1.1.3.4 Pharamceuticals

- 5.1.1.3.5 Industrial

- 5.1.1.3.6 Other End-use Industry

- 5.1.1.1 By Type

- 5.1.2 Paper Packaging

- 5.1.2.1 By Product Type

- 5.1.2.1.1 Folding Carton

- 5.1.2.1.2 Corrugated Boxes

- 5.1.2.1.3 Liquid Paperboard

- 5.1.2.1.4 Other Product Type

- 5.1.2.2 By End-use Industry

- 5.1.2.2.1 Food

- 5.1.2.2.2 Beverages

- 5.1.2.2.3 E-commerce

- 5.1.2.2.4 Other End-use Industry

- 5.1.2.1 By Product Type

- 5.1.3 Container Glass

- 5.1.3.1 By Color

- 5.1.3.1.1 Green

- 5.1.3.1.2 Amber

- 5.1.3.1.3 Flint

- 5.1.3.1.4 Other Colors

- 5.1.3.2 By End-use Industry

- 5.1.3.2.1 Food

- 5.1.3.2.2 Beverage

- 5.1.3.2.2.1 Alcoholic

- 5.1.3.2.2.2 Non-Alcoholic

- 5.1.3.2.3 Personal Care and Cosmetics

- 5.1.3.2.4 Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.3.2.5 Perfumery

- 5.1.3.1 By Color

- 5.1.4 Metal Cans and Containers

- 5.1.4.1 By Material Type

- 5.1.4.1.1 Steel

- 5.1.4.1.2 Aluminum

- 5.1.4.2 By Product Type

- 5.1.4.2.1 Cans

- 5.1.4.2.2 Drums and Barrels

- 5.1.4.2.3 Caps and Closures

- 5.1.4.2.4 Other Product Type

- 5.1.4.3 By End-use Industry

- 5.1.4.3.1 Food

- 5.1.4.3.2 Beverage

- 5.1.4.3.3 Chemicals and Petroleum

- 5.1.4.3.4 Industrial

- 5.1.4.3.5 Paints and coatings

- 5.1.4.3.6 Other End-use Industry

- 5.1.4.1 By Material Type

- 5.1.1 Plastic Packaging

- 5.2 By Packaging Format

- 5.2.1 Flexible

- 5.2.2 Rigid

- 5.3 By End-use Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceuticals and Healthcare

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Industrial

- 5.3.6 E-commerce

- 5.3.7 Other End-use Industry

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core segments, Financials as available, Strategic information, Market rank/share for key companies, Products and Services, and Recent developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit WestRock

- 6.4.3 Amcor plc

- 6.4.4 Mondi plc

- 6.4.5 Ball Corporation

- 6.4.6 Crown Holdings Inc.

- 6.4.7 Sealed Air Corporation

- 6.4.8 Sonoco Products Company

- 6.4.9 Graphic Packaging International LLC

- 6.4.10 Greif Inc.

- 6.4.11 Silgan Holdings Inc.

- 6.4.12 AptarGroup Inc.

- 6.4.13 Huhtamaki Oyj

- 6.4.14 Tetra Pak International SA

- 6.4.15 CAN-PACK UK Ltd.

- 6.4.16 Ardagh Group S.A.

- 6.4.17 RPC Group Ltd.

- 6.4.18 Klckner Pentaplast Ltd.

- 6.4.19 Coveris Holdings S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment