|

시장보고서

상품코드

1940552

멸균 서비스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Sterilization Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

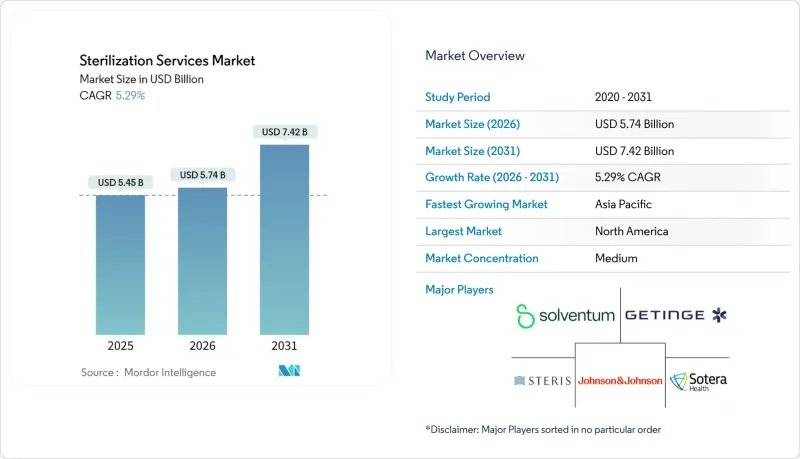

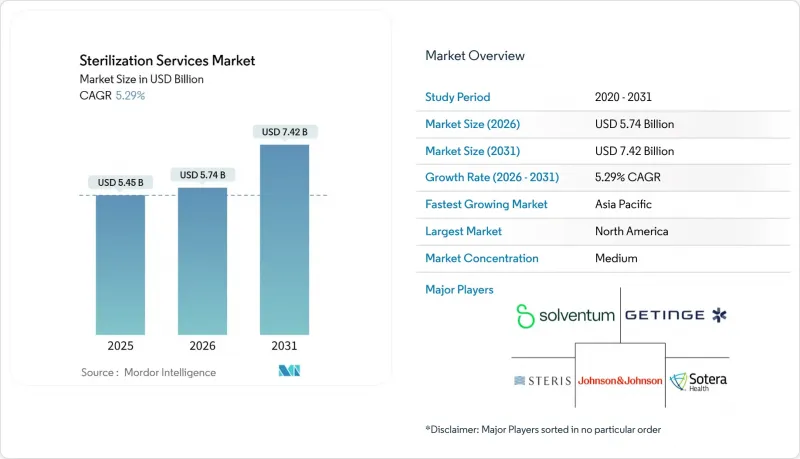

멸균 서비스 시장은 2025년 54억 5,000만 달러에서 2026년에는 57억 4,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 5.29%를 기록하며 2031년까지 74억 2,000만 달러에 달할 것으로 예측됩니다.

엄격한 감염 관리 프로토콜의 지속적인 채택, ISO 13485에 대한 규정의 수렴, 아웃소싱 처리의 급속한 보급이 꾸준한 확장을 뒷받침하고 있습니다. 고배출 에틸렌옥사이드(EtO)에서 엑스레이, 전자빔, 과산화수소 기술로의 전환이 가속화되면서 자본 부담과 혁신의 여지가 모두 생겨나고 있습니다. 또한, 일회용 바이오 공정 부품과 최소침습 의료기기가 전 세계 공급망에 유입됨에 따라 수요도 증가하고 있습니다. 시장 선도 기업들은 인수를 통해 지리적 범위와 검증 전문성을 확장하고, 신생 전문 기업들은 틈새 소재와 디지털화된 모니터링에 집중하고 있습니다. 이러한 요소들이 결합되어 치열한 경쟁 속에서도 가격 결정력을 유지하고 있습니다.

세계 멸균 서비스 시장 동향 및 인사이트

전 세계 병원내 감염 증가가 멸균 수요를 주도합니다

전 세계 의료 시설에서는 입원 기간의 장기화와 비용 증가를 초래하는 감염을 억제하기 위해 제염 프로토콜을 강화하는 추세입니다. 미국 질병예방통제센터(CDC)의 지침에 따르면, 철저한 환경 청소가 최전방 방어책으로 자리매김하고 있으며, 의료기관은 검증된 대용량 멸균 서비스를 채택해야 합니다. 선진국에 비해 감염률이 몇 배나 높은 자원이 부족한 지역에서는 많은 자본 지출 없이 신뢰할 수 있는 멸균 보증을 실현하기 위해 처리 업무의 아웃소싱이 증가하고 있습니다. 보험 지불 기관은 감염 지표와 상환을 연동하여 이러한 흐름을 촉진하고 있습니다. 계약 처리 업체는 의료기기 제조업체가 규제 신청의 효율성을 높이기 위해 생산 로트에 멸균 포장을 통합함으로써 혜택을 받고 있습니다. 이러한 움직임이 합쳐져 연간 멸균 서비스 시장으로 유입되는 시술 건수를 증가시키고 있습니다.

의료기기 및 의약품 제조 거점 세계 확대

의료기기 조립 라인과 생물학적 제제 충전 및 마무리 공장이 아시아태평양으로 이전하는 움직임은 아시아태평양의 검증된 멸균 능력에 대한 수요를 촉진하고 있습니다. 전 세계 공급업체들은 물류 혼란 속에서도 공급망의 탄력성을 유지하기 위해 멀티모달 허브를 구축하고 있습니다. 최고 수준의 멸균 보증이 필요한 주사제 생물학적 제제는 현재 아웃소싱 사이클에서 점점 더 많은 비중을 차지하고 있습니다. 업계 최고 수준의 선량 매핑 및 미생물 챌린지 테스트에 대한 전문성을 갖춘 전문 처리업체는 프리미엄 가격을 받고 있습니다. 외국인 투자를 유치하는 각국 정부는 신규 방사선 멸균 시설 건설에 대한 특혜를 제공하고 있으며, 이를 통해 현지에서의 이용 가능성을 가속화하고 ISO 11137에 대한 준수를 강화하고 있습니다.

컴플라이언스 대응 멸균시설 설립에 따른 높은 자본 및 운영 비용

조사 장치, 진공식 에틸렌옥사이드(EtO) 챔버, 기화 과산화수소 아이솔레이터는 모두 수백만 달러 규모의 초기 투자, 특수 환기 설비, 이중화 모니터링 시스템을 필요로 합니다. 연간 유지보수 비용에는 생물학적 지표 시험, 필터 검증, 규제 감사 등이 포함됩니다. 소규모 지역 병원은 투자를 미루고, 대신 다년간의 외주 계약을 추구합니다. 재정적 장벽은 신규 진입을 제한하고 산업 구조조정을 초래하여 서비스 미충족 지역의 공급 능력 부족을 초래할 수 있습니다.

부문 분석

2025년 기준 에틸렌옥사이드는 멸균 서비스 시장 규모의 49.30%를 차지했으며, 이는 열에 민감하고 내강이 많은 의료기기와 비교할 수 없는 호환성을 반영합니다. 그러나 누적된 규제 압력과 공중 보건에 대한 우려로 인해 다각화가 가속화되고 있습니다. 이미 다양한 제품군에 적용이 검증된 엑스레이 사이클은 2031년까지 12.15%의 CAGR을 기록할 것으로 예상되며, 부문 내에서 가장 빠른 성장세를 보일 것으로 예상됩니다. 선량 균일성 연구를 통해 코발트60의 물류 문제를 피하면서 감마선 조사와 동등한 효과가 입증되었습니다. 감마선 멸균은 이미 확립된 인프라와 신뢰할 수 있는 심부투과 성능을 유지하고 있지만, 동위원소 공급 제약으로 인해 대체 계획 수립이 요구되고 있습니다. 전자선 조사는 고속 처리가 가능하지만, 고밀도 팔레트에는 한계가 있습니다. 과산화수소 플라즈마 및 기체상 시스템은 전자내시경 등 온도에 민감한 물품에 대응하여 고부가가치 수술 키트 분야에서 충성도 높은 고객 기반을 구축하고 있습니다. 재료 과학이 발전함에 따라 방법의 선택은 산화 스트레스 하에서 폴리머의 거동에 점점 더 의존하고 있으며, 가공업체는 멀티모달 기능을 제공해야 합니다.

멸균 서비스 시장에서는 이중 에너지 전환 기능을 갖춘 방사선실에 대한 설비 투자가 지속적으로 재분배되어 동위 원소에서 기계 소스로의 원활한 전환이 가능해졌습니다. 공급업체는 장비 엔지니어와 협력하여 장비 설계 단계에서 선량 매핑을 통합하고, 제조 후 변동을 줄이기 위해 장비 엔지니어와 협력하고 있습니다. 증기 과산화수소가 확립된 카테고리 A 방법으로 규제 당국의 승인을 받음으로써 510(k) 신청이 간소화되고, 양식 점유율이 더욱 분산되고 있습니다. 그 결과, 방법의 다양화로 수익구조를 재구축하고 공급의 연속성을 확보하고 있습니다.

2025년에는 오프사이트 서비스 센터가 멸균 서비스 시장의 67.05%를 차지했으며, 규모의 경제를 활용하여 설비 투자 및 환경 관리 비용을 상각하고 있습니다. 중앙 집중식 허브는 24시간 365일 혼합 부하를 처리하고, 검증된 트랙 경로와 디지털 관리 체인 보고를 제공합니다. 인력 부족과 수술 장비의 적체 문제에 직면한 병원들은 규정 준수와 예측 가능한 납기를 위해 트레이를 지역 내 오프사이트 재처리 센터로 이송하는 사례가 증가하고 있습니다. 한편, 현장 서비스 모델은 10.98%의 CAGR로 성장할 것으로 예상되며, 실시간 릴리스를 통해 재고 일수를 줄일 수 있는 대용량 제약 캠퍼스에서 선호되고 있습니다. 하이브리드 모델이 등장하여, 고객은 초과분 처리를 위한 이동식 에톡사이드 포드와 정기적인 오프사이트 조사를 결합하여 비용과 사이클 타임의 균형을 미세 조정할 수 있게 되었습니다.

지정학적 리스크의 발전은 이중화의 중요성을 강조하고 있습니다. 다국적 제조업체들은 팬데믹과 자연재해에 대한 내성을 확보하기 위해 지리적으로 분산된 공급자들 간에 이중 검증을 할당하고 있습니다. 이에 따라 위탁 가공업체는 미러링된 디지털 문서 시스템을 개발하여 시설 간 및 고객의 품질 포털 간에 사이클 데이터를 즉시 전송할 수 있도록 하고 있습니다.

지역별 분석

북미는 2025년 멸균 서비스 시장에서 39.10%의 점유율을 차지했으며, 견고한 상환 모델, 의료기기 클러스터의 밀집, 적극적인 환경 모니터링에 힘입어 선두를 유지했습니다. 미국 환경보호청(EPA)이 2025년에 최종 결정한 99.99%의 에틸렌옥사이드(EtO) 포집율을 요구하는 규정으로 인해 공급업체들은 제거 기술을 개선해야 하며, 기계식 방사원으로의 전환이 가속화되고 있습니다. 대체 방식에 대한 투자는 컴플라이언스 비용의 증가에도 불구하고 공급의 연속성을 보장하고 지역적 주도권을 유지할 수 있습니다.

아시아태평양은 2031년까지 CAGR 10.82%로 가장 빠르게 성장하는 시장입니다. 중국, 인도, 말레이시아의 의료기기 수탁 제조 기업이 확대됨에 따라 미국 및 EU의 감사 기준을 충족하는 근거리 멸균 능력이 요구되고 있습니다. STERIS사가 2025년 소주에서 X선 시설을 가동한 사례는 다중 에너지 대응을 중심으로 한 시장 진입 전략의 좋은 예입니다. 각국 정부는 수출의 병목현상을 최소화하기 위해 국내 조사를 장려하고 있으며, 현지 규제 당국은 ISO 11137 및 ISO 13408을 준수하여 국경 간 무역의 효율성을 높이고 있습니다.

유럽은 2025년 기준 약 30.20%의 점유율을 유지하고 있으며, 의료기기 규정(MDR)의 엄격한 기기 및 포장 검증 조항이 특징입니다. 공급자는 지속가능성 목표 달성을 위해 초임계 이산화탄소 및 기화 과산화수소 사이클로의 다각화를 추진하고 있습니다. SGS의 MDR 멸균 인증 범위 확대는 공정 폭을 통한 경쟁 우위를 강조하고 있습니다. 기업의 입찰에 포함된 지속가능성 지표가 벤더 선정에 영향을 미치고 있으며, 에너지 효율이 높은 가속기 및 열회수 환기 시스템에 대한 투자를 촉진하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The sterilization services market is expected to grow from USD 5.45 billion in 2025 to USD 5.74 billion in 2026 and is forecast to reach USD 7.42 billion by 2031 at 5.29% CAGR over 2026-2031.

Consistent adoption of stringent infection-control protocols, regulatory convergence toward ISO 13485, and rapid uptake of outsourced processing underpin steady expansion. Accelerating transition away from high-emission ethylene oxide (EtO) toward X-ray, electron-beam, and hydrogen-peroxide technologies adds both capital pressure and innovation headroom. Demand also rises as single-use bioprocess components and minimally invasive devices flood global supply chains. Market leaders leverage acquisitions to broaden geographic reach and validation expertise, while emerging specialists focus on niche materials and digitalized monitoring. Collectively, these forces sustain pricing power even as competitive intensity grows.

Global Sterilization Services Market Trends and Insights

Escalating Global Incidence of Hospital-Acquired Infections Driving Sterilization Demand

Healthcare facilities worldwide are intensifying decontamination protocols to curb infections that prolong hospital stays and inflate costs. Guidance from the Centers for Disease Control and Prevention positions thorough environmental cleaning as a frontline defense, pushing providers to adopt validated, high-capacity sterilization services. Low-resource regions, which report infection rates several times higher than advanced economies, increasingly outsource processing to achieve reliable sterility assurance without heavy capital spending. Insurance payers reinforce the shift by linking reimbursement to infection metrics. Contract processors benefit as device manufacturers bundle sterile packaging with production runs to streamline regulatory submissions. Collectively, these behaviors lift annual procedure volumes flowing into the sterilization services market.

Expansion of Medical Device & Pharmaceutical Manufacturing Footprint Worldwide

Relocation of device assembly lines and biologics fill-finish plants toward Asia-Pacific fuels regional demand for validated sterilization capacity. Global suppliers establish multi-modal hubs so that supply chains stay resilient amid logistics disruption. Injectable biologics, which require the highest sterility assurance level, now represent a growing slice of outsourced cycles. Specialized processors with class-leading dose mapping and microbial challenge expertise capture premium pricing. Governments courting foreign investment offer incentives for greenfield irradiation facilities, accelerating local availability and reinforcing compliance with ISO 11137.

High Capital & Operating Costs of Establishing Compliant Sterilization Facilities

Irradiators, vacuum-draw EtO chambers, and vaporized hydrogen-peroxide isolators each demand multimillion-dollar outlays, specialized ventilation, and redundant monitoring. Annual upkeep includes biological indicators, filter validation, and regulatory audits. Smaller regional hospitals defer investment and instead pursue multiyear outsourcing contracts. Financial barriers also restrict new competitors, leading to industry consolidation that can strain capacity in underserved territories.

Other drivers and restraints analyzed in the detailed report include:

- Tightening & Harmonization of International Sterilization Standards (ISO, FDA, EMA)

- Growing Preference for Outsourced Sterilization to Manage Compliance & Cost Pressures

- Stringent Environmental & Occupational Regulations on EtO and Radio-isotope Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ethylene oxide retained a dominant 49.30% slice of the sterilization services market size in 2025, reflecting unmatched compatibility with heat-sensitive, lumen-rich devices. Yet, cumulative regulatory pressure and public health concerns accelerate diversification. X-ray cycles, already validated for a widening catalog, are forecast to record a 12.15% CAGR through 2031, the fastest within the segment. Dose-uniformity studies show its efficacy equals gamma irradiation while avoiding cobalt-60 logistics. Gamma retains entrenched infrastructure and reliable deep-penetration performance, although isotope supply constraints spur contingency planning. Electron-beam offers rapid throughput but faces limitations with dense pallets. Hydrogen-peroxide plasma and vapor-phase systems capture temperature-sensitive items like electronic endoscopes, building a loyal customer base in high-value surgical kits. As material science evolves, method selection increasingly hinges on polymer behavior under oxidative stress, pushing processors to offer multi-modal capabilities.

The sterilization services market continues reallocating capex toward radiation vaults equipped for dual-energy switching, enabling seamless migration from isotope to machine sources. Providers collaborate with device engineers to embed dose mapping at the design stage, reducing post-production inconsistencies. Regulatory acceptance of vaporized hydrogen-peroxide as an Established Category A method simplifies 510(k) submissions, further fragmenting modal shares. Consequently, method diversification reshapes revenue streams and safeguards supply continuity.

Off-site service centers captured 67.05% of the sterilization services market in 2025, leveraging scale to amortize capital outlays and environmental controls. Centralized hubs process mixed loads 24/7, offering validated truck routes and digital chain-of-custody reporting. Hospitals pressured by staffing shortages and surgical-instrument backlogs increasingly divert trays to regional off-site re-processing centers, citing improved compliance and predictable turnaround. Conversely, on-site service models, projected to advance at an 10.98% CAGR, appeal to high-volume pharma campuses where real-time release trims inventory days. Hybrid models emerge, blending mobile EtO pods for overflow with routine off-site irradiation, permitting clients to fine-tune cost versus cycle time.

Evolving geopolitical risks underscore redundancy. Multinational manufacturers allocate dual validation across geographically separated providers to ensure pandemic or natural-disaster resilience. In response, contract processors develop mirrored digital documentation systems, enabling instant transfer of cycle data between facilities and clients' quality portals.

The Sterilization Services Market Report is Segmented by Method (Ethylene Oxide (ETO) Sterilization, Gamma Irradiation, and More), Mode of Delivery (Off-Site Sterilization, and More), Service Type (Contract Sterilization Services, and More), End User (Medical Device Manufacturers, Hospitals and Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the sterilization services market with a 39.10% share in 2025, underpinned by robust reimbursement models, dense medical-device clusters, and proactive environmental oversight. The Environmental Protection Agency's 2025 final rule demanding 99.99% EtO capture forces providers to retrofit abatement technology and accelerates migration toward machine-source radiation. Investment in alternative modalities safeguards supply continuity and sustains regional leadership despite higher compliance costs.

Asia-Pacific represents the fastest-growing arena at an 10.82% CAGR through 2031. Expanding device contract-manufacturing organizations in China, India, and Malaysia require proximity sterilization capacity that satisfies U.S. and EU audits. STERIS's 2025 commissioning of an X-ray facility in Suzhou exemplifies market-entry strategies oriented toward multi-energy resilience. Governments encourage domestic irradiation to minimize export bottlenecks, and local regulators are aligning with ISO 11137 and ISO 13408, streamlining cross-border trade.

Europe maintains roughly 30.20% share in 2025, characterized by the Medical Device Regulation's stringent device and packaging validation clauses. Providers diversify into super-critical carbon-dioxide and vaporized hydrogen-peroxide cycles to meet sustainability objectives. SGS's expanded MDR sterilization certification scope highlights competitive advantage through process breadth. Sustainability metrics embedded in corporate tenders now influence vendor selection, prompting investment in energy-efficient accelerators and heat-recovery ventilation.

- STERIS

- Sotera Health (Sterigenics, Nordion, Nelson Labs)

- Getinge

- Solventum Corporation

- Johnson & Johnson

- BGS Beta-Gamma-Service GmbH

- E-BEAM Services Inc.

- Medistri

- Noxilizer Inc.

- Stryker

- Prince Sterilization Services LLC

- Advanced Sterilization Products (ASP)

- GERMITECH Srl

- Cosmed Group

- MMM Group

- Belimed

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Incidence of Hospital-Acquired Infections Driving Sterilization Demand

- 4.2.2 Expansion of Medical Device & Pharmaceutical Manufacturing Footprint Worldwide

- 4.2.3 Tightening & Harmonization of International Sterilization Standards (ISO, FDA, EMA)

- 4.2.4 Growing Preference for Outsourced Sterilization to Manage Compliance & Cost Pressures

- 4.2.5 Rising Adoption of Single-Use & Minimally Invasive Devices Increasing Sterilization Volumes

- 4.3 Market Restraints

- 4.3.1 High Capital & Operating Costs of Establishing Compliant Sterilization Facilities

- 4.3.2 Stringent Environmental & Occupational Regulations on EtO and Radio-isotope Use

- 4.3.3 Global Shortage of Certified Sterility Assurance & Validation Professionals

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Method

- 5.1.1 Ethylene Oxide (EtO) Sterilization

- 5.1.2 Gamma Irradiation

- 5.1.3 Electron-Beam (E-beam) Radiation

- 5.1.4 X-ray Radiation

- 5.1.5 Steam (Moist-Heat) Sterilization

- 5.1.6 Dry-Heat Sterilization

- 5.1.7 Hydrogen Peroxide & Plasma Sterilization

- 5.2 By Mode of Delivery

- 5.2.1 Off-site (Service-Center) Sterilization

- 5.2.2 On-site (In-house as a Service) Sterilization

- 5.3 By Service Type

- 5.3.1 Contract Sterilization Services

- 5.3.2 Sterilization Validation & Testing Services

- 5.3.3 Process Advisory & Optimization Services

- 5.4 By End-user

- 5.4.1 Medical Device Manufacturers

- 5.4.2 Pharmaceutical & Biotech Manufacturers

- 5.4.3 Hospitals & Clinics

- 5.4.4 Food & Beverage Industry

- 5.4.5 Laboratory & Research Organizations

- 5.4.6 Other Industrial Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 STERIS PLC

- 6.3.2 Sotera Health (Sterigenics, Nordion, Nelson Labs)

- 6.3.3 Getinge AB

- 6.3.4 Solventum Corporation

- 6.3.5 Johnson & Johnson (Ethicon)

- 6.3.6 BGS Beta-Gamma-Service GmbH

- 6.3.7 E-BEAM Services Inc.

- 6.3.8 Medistri SA

- 6.3.9 Noxilizer Inc.

- 6.3.10 Stryker Corporation

- 6.3.11 Prince Sterilization Services LLC

- 6.3.12 Advanced Sterilization Products (ASP)

- 6.3.13 GERMITECH Srl

- 6.3.14 Cosmed Group

- 6.3.15 MMM Group

- 6.3.16 Belimed AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment