|

시장보고서

상품코드

1940568

데이터센터 스위치 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Data Center Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

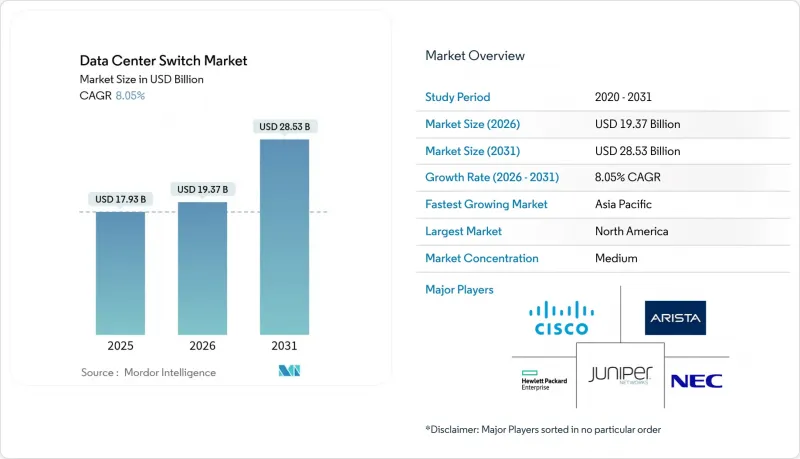

데이터센터 스위치 시장은 2025년에 179억 3,000만 달러로 평가되며, 2026년 193억 7,000만 달러에서 2031년까지 285억 3,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 8.05%로 예상됩니다.

인공지능 트레이닝 클러스터 도입 증가, 클라우드 네이티브 워크로드로의 꾸준한 전환, 하이퍼스케일 캠퍼스의 급속한 확장, 고 대역폭 스위치 인프라에 대한 설비투자가 지속적으로 증가하고 있습니다. 3계층 구조에서 리프 스파인 구조로 전환하여 네트워크 토폴로지를 평탄화하여 병렬 처리에서 낮은 지연과 예측 가능한 성능을 실현하고 있습니다. 이더넷 실리콘의 혁신으로 장치당 포트 밀도가 51.2Tbps를 넘어섰고, 기가비트당 전력 소비가 감소하여 400G 및 800G 광모듈의 채택이 확대되고 있습니다. 데이터 거주성에 대한 규제 요건은 지역내 용량 증설을 촉진하는 한편, 엣지 시설의 확장은 제한된 설치 공간을 수용할 수 있는 컴팩트하고 원격으로 관리 가능한 스위치에 대한 추가 수요를 창출하고 있습니다. 수직 통합형 벤더들이 실리콘, 광모듈, 소프트웨어를 번들로 묶어 도입 주기를 단축하고 운영을 간소화하면서 경쟁이 심화되고 있습니다.

세계 데이터센터 스위치 시장 동향 및 인사이트

클라우드 및 엣지 컴퓨팅의 워크로드 급증

5G, IoT, 실시간 분석 워크로드를 처리하는 엣지 사이트가 급증하면서 공간이 제한된 랙에서 작동하는 컴팩트한 고처리량 스위치에 대한 수요가 증가하고 있습니다. 하이퍼스케일러는 현재 소비자 용도의 지연을 10밀리초 미만으로 낮추기 위해 지역 에지 노드를 설계하고 있으며, 이로 인해 스위치 하드웨어는 열악한 환경, 종종 무인화된 장소에 설치됩니다. 프로그래머블 전송 플레인을 통해 운영자는 수동으로 배선하지 않고도 메트로 에지와 코어 캠퍼스 간 트래픽을 동적으로 유도할 수 있습니다. 하드웨어 기반의 시간 민감형 네트워킹 기능은 확정적인 지연이 필요한 산업용 로봇과 자율주행 차량을 지원하는 데에도 기여합니다. 엣지 설치 면적이 확대됨에 따라 멀티 테넌트 코로케이션 프로바이더는 중복 액세스 계층을 추가하여 저전력 스위치의 잠재적 시장 규모를 확대하고 있습니다.

고 대역폭 스위칭이 필요한 AI/ML 트레이닝 클러스터

거대 언어 모델 훈련은 표준 데이터센터 트래픽 패턴에 비해 24-32배의 동서방향 트래픽이 발생합니다. 이에 하이퍼스케일 사업자는 GPU 간 단일 홉 경로를 유지하는 102.4Tbps ASIC을 도입하고, 혼잡도 제어 알고리즘을 통해 패킷 손실을 거의 제로에 가깝게 억제하고 있습니다. 각 벤더들은 링크 레벨 텔레메트리를 이용한 마이크로 버스트 예측과 마이크로초 단위의 플로우 리루팅에 대한 실험을 진행하고 있습니다. 초기 필드 테스트 결과, 동일한 패브릭 내에서 100G 링크를 400G 링크로 교체했을 때 모델 훈련 시간이 1.6배 단축되었습니다. 이러한 성능 향상은 GPU 활용률 향상으로 수백만 달러 규모의 비용 절감으로 이어져 고속 스위치 도입의 투자 대비 효과를 더욱 강화합니다.

차세대 스위치 업그레이드시 높은 설비 투자(CAPEX) 및 운영 비용(OPEX)

10G 또는 40G에서 400G로 업그레이드하려면 새로운 스위치뿐만 아니라 고급 파이버, 전력 강화, 고급 냉각 시스템도 필요하며, 기업 규모의 구축은 총 프로젝트 예산이 1,000만 달러에서 5억 달러로 늘어납니다. 많은 중견기업이 리뉴얼을 미루고 대신 코로케이션 사업자로부터 용량을 임대하는 경우가 많아 스위치의 직접 판매는 둔화되고 있습니다. 포트 속도 향상에 따라 전력 소비가 증가하므로 지속적인 운영 비용이 상승합니다. 다만, 차세대 ASIC의 효율성 향상으로 일부 상쇄될 수 있습니다. 포춘지 선정 500대 기업 이외의 예산 제약이 있는 조직은 여전히 자금 조달의 장벽이 가장 심각합니다.

부문 분석

2025년 코어 스위치는 하이퍼스케일 캠퍼스내 수천 개의 리프 링크를 통합하는 역할로 인해 데이터센터 스위치 시장 점유율의 47.35%를 차지했습니다. 수만 대의 서버에 걸쳐 확정적인 지연을 요구하는 스케일아웃 패브릭에서 여전히 필수적입니다. AI 워크로드가 높은 라딕스 아키텍처를 필요로 하고, 섀시 기반 설계에 유리하므로 핵심 플랫폼 관련 데이터센터 스위치 시장 규모는 꾸준히 확대될 것으로 예측됩니다. 액세스 스위치는 단가가 낮고, 엣지노드 및 마이크로 데이터센터 보급에 따라 8.86%의 가장 높은 CAGR을 기록했습니다. 벤더들은 액세스 장비에 심층 버퍼링 및 온디바이스 분석 기능을 통합하여 운영자가 네트워크 엣지에서 QoS 정책을 적용할 수 있도록 지원하고 있습니다. 신흥 시장에서는 전력망이 취약한 지역에서도 저전력 액세스 모델을 통한 도입이 가능합니다. 종합적인 성장 패턴은 하이퍼스케일 환경에서의 고부가가치 코어 갱신 주기와 분산형 시설에서의 대량 액세스 판매라는 두 가지 궤적을 동시에 진행하는 두 가지 궤적의 진화입니다.

100GbE 부문은 2025년에도 데이터센터 스위치 시장 점유율의 38.40%를 차지할 것으로 예상되며, 이는 주류 워크로드에서 뛰어난 비용 대비 성능의 균형을 반영합니다. 그러나 AI 클러스터가 400G 오버 구독 임계치를 초과하는 비차단 패브릭을 필요로 하므로 800GbE 장비의 데이터센터 스위치 시장 규모는 급격하게 확대될 것으로 예측됩니다. 초기 파일럿에서 800GbE 스핀과 400GbE 리프의 조합은 높은 대역폭의 바이섹션 특성을 통해 생성 모델 훈련 시간을 30% 단축할 수 있는 것으로 입증되었습니다. HPC 센터, 금융 거래소 등 일찍부터 업그레이드를 진행한 고객층에서 200-400GbE에 대한 관심은 여전히 높은 수준을 유지하고 있습니다. 한편, 서버 NIC의 속도 향상에 따라 레거시 10GbE 이하의 출하량은 지속적으로 감소하는 추세이며, 업계 수요는 더욱 빠른 속도로 이동하고 있습니다.

지역별 분석

북미는 지속적인 하이퍼스케일 확장, 풍부한 자본, 디지털 인프라 지원 정책 프레임워크로 인해 가장 규모가 큰 지역 매출을 차지하고 있습니다. 주요 클라우드 프로바이더들은 버지니아와 오하이오 주에 걸쳐 멀티 기가 와트 규모의 캠퍼스 건설을 계속하고 있습니다. CHIPS법에 기반한 국내 반도체 우대조치는 ASIC 생산의 국산화를 목표로 해외 팹에 대한 의존도를 낮추기 위한 조치입니다. 캐나다와 멕시코는 재생에너지와 세제혜택을 원하는 사업자들의 2차 건설을 유치하여 이중화 및 지연 분산화를 제공합니다.

아시아태평양은 전체 성장률이 가장 높은 지역으로, 2030년까지 데이터센터용량이 두 배로 증가할 것으로 예측됩니다. 중국 시장은 여전히 지배적이지만, 엄격한 데이터 현지화 규제로 인해 크로스보더 클라우드 설계가 복잡해지고 있습니다. 인도에서는 제조거점이 강화되고, 알리바바 등 벤더들이 조립 라인을 가동하여 공급망 단축과 관세 회피를 위해 노력하고 있습니다. 일본과 한국은 밀집된 도시 지역에서의 배치를 관리하기 위해 해저 케이블 연장 및 액체 냉각 기술 연구에 투자하고 있습니다. 지역내 규정의 다양성으로 인해 벤더는 국가별로 컴플라이언스 기능을 조정해야 합니다.

유럽에서는 디지털 주권이 화두로 떠오르면서 84%의 기업이 지역 제한형 클라우드 솔루션을 추구하고 있습니다. FLAPD 도시권이 신규 메가와트 증설의 대부분을 흡수하는 반면, 북유럽 국가들은 풍부한 재생에너지로 사업자를 유치하고 있습니다. 현지 벤더들은 차별화 요소로 컴플라이언스 인증을 중요시합니다. 중동 및 아프리카에서는 국가 AI 전략에 따라 급속한 인프라 확충이 진행되고 있으며, 아랍에미리트와 사우디아라비아가 주도하고 있습니다. 외국 하이퍼스케일러에게 수십억 달러 규모의 특혜와 유리한 부동산 조건을 제공합니다. 가혹한 기후 조건으로 인해 에너지 효율을 유지하기 위한 액체 냉각 기술의 채택이 가속화되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

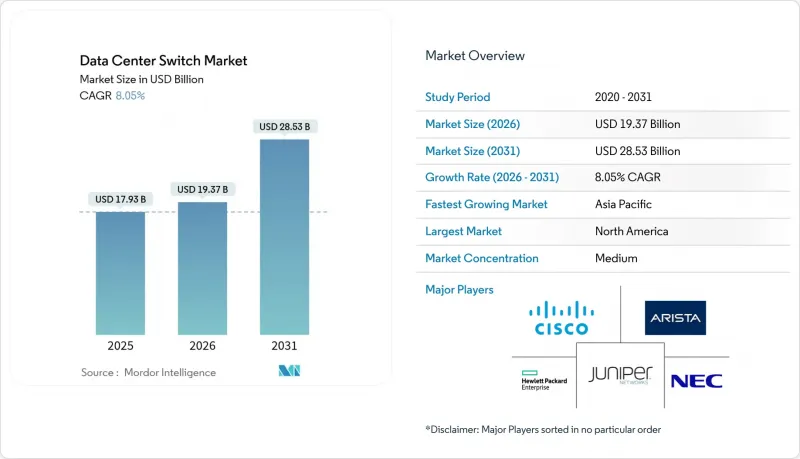

KSA 26.03.06The data center switches market was valued at USD 17.93 billion in 2025 and estimated to grow from USD 19.37 billion in 2026 to reach USD 28.53 billion by 2031, at a CAGR of 8.05% during the forecast period (2026-2031).

Rising deployment of artificial-intelligence training clusters, steady migration toward cloud-native workloads, and rapid scaling of hyperscale campuses continue to drive capital spending on high-bandwidth switch infrastructure. The shift from three-tier to leaf-spine fabrics is flattening network topologies, enabling lower latency and more predictable performance for parallel processing. Ethernet silicon innovation is pushing port density past 51.2 Tbps per device, trimming power draw per gigabit and widening adoption of 400G and 800G optics. Regulatory mandates on data residency spur in-region capacity additions, while expanding edge facilities create incremental demand for compact, remotely managed switches that can tolerate constrained footprints. Competitive intensity is heightening as vertically integrated vendors bundle silicon, optics, and software to shorten deployment cycles and simplify operations.

Global Data Center Switch Market Trends and Insights

Cloud and Edge Computing Workload Surge

Edge sites that process 5G, IoT, and real-time analytics workloads are proliferating, boosting demand for compact, high-throughput switches able to function in space-limited racks. Hyperscalers now design regional edge nodes to keep latency under 10 milliseconds for consumer applications, which places switch hardware in harsh, often unmanned locations. Programmable forwarding planes allow operators to steer traffic dynamically between metro edge and core campuses without manual recabling. Hardware-based time-sensitive networking features also help support industrial robots and autonomous vehicles that require deterministic latency. As edge footprints grow, multi-tenant colocation providers are adding redundant access layers, enlarging the addressable pool for low-power switches.

AI/ML Training Clusters Requiring High-Bandwidth Switching

Training large language models generates east-west traffic that is 24-32 times higher than standard data-center traffic patterns. Hyperscale operators therefore deploy 102.4 Tbps ASICs that maintain single-hop paths between GPUs, while congestion-control algorithms keep packet loss near zero. Vendors experiment with link-level telemetry to predict micro-bursts and reroute flows within micro-seconds. Early field results show a 1.6 times reduction in model training duration when 400G links replace 100G links in the same fabric. These performance gains translate into millions of dollars in GPU utilization savings, reinforcing the ROI for faster switches.

High CAPEX and OPEX for Next-Gen Switch Upgrades

Upgrading from 10G or 40G to 400G demands not just new switches but also higher-grade fiber, power upgrades, and advanced cooling, pushing total project budgets from USD 10 million to USD 500 million for enterprise-scale builds. Many mid-size firms postpone overhauls and instead lease capacity from colocation providers, slowing direct switch sales. Ongoing operating expenses rise as higher port speeds increase electricity draw, although newer ASICs partially offset this through efficiency gains. Financing hurdles remain most acute for budget-constrained organizations outside the Fortune 500.

Other drivers and restraints analyzed in the detailed report include:

- Mandates on Data Residency and Sovereign Clouds

- 400G/800G Optics Driving Port USD/Gb Down

- Skills Shortage in Managing Leaf-Spine Fabrics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Core switches accounted for 47.35% of the data center switches market share in 2025 due to their role in aggregating thousands of leaf links within hyperscale campuses. They remain essential for scale-out fabrics that demand deterministic latency across tens of thousands of servers. The data center switches market size associated with core platforms is projected to expand steadily as AI workloads require higher radix architectures that favor chassis-based designs. Access switches, while smaller ticket items, post the highest 8.86% CAGR as edge nodes and micro data centers proliferate. Vendors integrate deep buffering and on-device analytics into access gear, letting operators enforce quality-of-service policies at the network edge. In emerging markets, low-power access models enable deployments where utility grids remain fragile. The combined growth pattern shows a dual-track evolution, with high-value core refresh cycles in hyperscale settings and high-volume access sales in distributed estates.

The 100 GbE segment retained 38.40% data center switches market share in 2025, reflecting its favorable cost-performance trade-off for mainstream workloads. Yet the data center switches market size for 800 GbE gear is projected to rise sharply as AI clusters require non-blocking fabrics that exceed 400G oversubscription thresholds. Early pilots demonstrate that 800 GbE spines paired with 400 GbE leaves reduce training time for generative models by 30% through higher bisectional bandwidth. Customer interest in 200-400 GbE remains healthy among HPC centers and financial exchanges that upgraded earlier. Meanwhile, legacy <=10 GbE shipments continue to taper as server NIC speeds climb, further tilting industry demand toward high-speed segments.

The Data Center Switch Market is Segmented by Switch Type (Core Switches, Access Switches, and More), Bandwidth Class (<=10 GbE, 25-100 GbE, and More), Switching Technology (Ethernet, Infiniband, and More), Data Center Type (Hyperscale Cloud, Colocation, and More), End-User Industry (IT and Telecom, BFSI, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounts for the largest regional revenue thanks to sustained hyperscale expansion, abundant capital, and supportive digital-infrastructure policy frameworks. Major cloud providers continue to break ground on multi-giga-watt campuses across Virginia and Ohio. Domestic semiconductor incentives under the CHIPS Act aim to localize ASIC production, reducing dependence on overseas fabs. Canada and Mexico attract secondary builds as operators seek renewable energy and tax incentives, providing redundancy and latency diversification.

Asia-Pacific registers the fastest aggregate growth, with data center capacity expected to double before 2030. China's market remains dominant yet constrained by strict data-localization rules that complicate cross-border cloud designs. India gains manufacturing traction as vendors such as Arista launch assembly lines that shorten supply chains and bypass tariffs. Japan and South Korea invest in submarine cable extensions and liquid-cooling research to manage dense urban deployments. Regulatory diversity across the region forces vendors to tailor compliance features on a country-by-country basis.

Europe centers on digital sovereignty, with 84% of enterprises pursuing region-bound cloud solutions. The FLAPD metros absorb most new megawatt additions, yet Nordic states lure operators with abundant renewable power. Local vendors emphasize compliance certifications as differentiators. Middle East and Africa witness rapid build-out aligned with national AI strategies. The United Arab Emirates and Saudi Arabia lead, offering multi-billion-dollar incentives and favorable real-estate terms to foreign hyperscalers. Harsh climates accelerate adoption of liquid-cooling to maintain energy efficiency.

- Cisco Systems, Inc.

- Arista Networks, Inc.

- Juniper Networks, Inc.

- Hewlett Packard Enterprise Development LP

- Dell Technologies, Inc.

- Huawei Technologies Co., Ltd.

- H3C Holding Limited

- Lenovo Group Limited

- NEC Corporation

- Extreme Networks, Inc.

- NVIDIA Corporation (Mellanox and Cumulus)

- Fortinet, Inc.

- Broadcom Inc.

- ZTE Corporation

- Quanta Cloud Technology

- D-Link Corporation

- Edgecore Networks (Accton)

- Super Micro Computer, Inc.

- Pluribus Networks, Inc.

- Silicom Ltd.

- Netgear, Inc.

- Chelsio Communications, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud and Edge Computing Workload Surge

- 4.2.2 AI/ML Training Clusters Requiring High-Bandwidth Switching

- 4.2.3 Mandates on Data Residency and Sovereign Clouds

- 4.2.4 400G / 800G Optics Driving Port $/Gb Down

- 4.2.5 Data-Center Disaggregation and Open Networking Adoption

- 4.2.6 Liquid-Cooling-Enabled Ultra-Dense Switching

- 4.3 Market Restraints

- 4.3.1 High CAPEX and OPEX for Next-Gen Switch Upgrades

- 4.3.2 Skills Shortage in Managing Leaf-Spine Fabrics

- 4.3.3 Supply-Chain Disruptions for Advanced ASICs

- 4.3.4 Regulatory Delays in 5 nm / 3 nm Chip Production

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Technology Snapshot

- 4.8.1 Bandwidth

- 4.8.2 Switching Technology

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Switch Type

- 5.1.1 Core Switches

- 5.1.2 Distribution Switches

- 5.1.3 Access Switches

- 5.2 By Bandwidth Class

- 5.2.1 <=10 GbE

- 5.2.2 25-100 GbE

- 5.2.3 100-200 GbE

- 5.2.4 200-400 GbE

- 5.2.5 800 GbE and Beyond

- 5.3 By Switching Technology

- 5.3.1 Ethernet

- 5.3.2 Fiber Channel

- 5.3.3 InfiniBand

- 5.4 By Data Center Type

- 5.4.1 Hyperscale Cloud Providers

- 5.4.2 Colocation Providers

- 5.4.3 Enterprise / On-Premise

- 5.5 By End-User Industry

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Government and Defense

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Media and Entertainment

- 5.5.6 Retail and E-Commerce

- 5.5.7 Education and Research

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.2.1 Cisco Systems, Inc.

- 6.2.2 Arista Networks, Inc.

- 6.2.3 Juniper Networks, Inc.

- 6.2.4 Hewlett Packard Enterprise Development LP

- 6.2.5 Dell Technologies, Inc.

- 6.2.6 Huawei Technologies Co., Ltd.

- 6.2.7 H3C Holding Limited

- 6.2.8 Lenovo Group Limited

- 6.2.9 NEC Corporation

- 6.2.10 Extreme Networks, Inc.

- 6.2.11 NVIDIA Corporation (Mellanox and Cumulus)

- 6.2.12 Fortinet, Inc.

- 6.2.13 Broadcom Inc.

- 6.2.14 ZTE Corporation

- 6.2.15 Quanta Cloud Technology

- 6.2.16 D-Link Corporation

- 6.2.17 Edgecore Networks (Accton)

- 6.2.18 Super Micro Computer, Inc.

- 6.2.19 Pluribus Networks, Inc.

- 6.2.20 Silicom Ltd.

- 6.2.21 Netgear, Inc.

- 6.2.22 Chelsio Communications, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment