|

시장보고서

상품코드

1940583

구급차 서비스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Ambulance Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

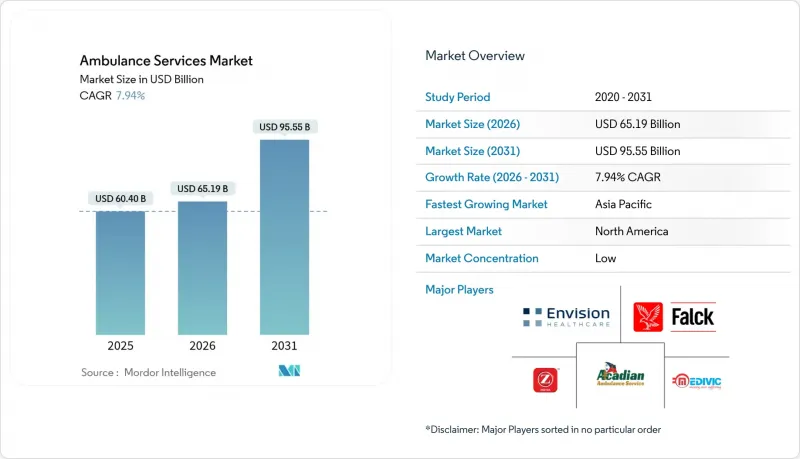

2026년 구급차 서비스 시장 규모는 651억 9,000만 달러로 추정되며, 2025년 604억 달러에서 성장이 전망됩니다.

2031년에는 955억 5,000만 달러에 달할 것으로 예상되며, 2026-2031년 연평균 복합 성장률(CAGR) 7.94%로 성장할 것으로 전망됩니다.

이러한 확대는 신속한 병원 전 진료에 대한 수요 증가, 의료 보험 적용 범위 확대, 커넥티드 케어 기술의 보급을 반영합니다. 아시아태평양은 9.4%로 가장 빠른 성장률을 보이고 있으며, 이는 정부의 응급의료서비스(EMS) 확대와 신흥국 보험사의 보장범위 확대에 기인합니다. 지상 구급차는 여전히 수익의 기반이지만, 장거리 대응 및 저연비 항공기의 도입과 고도의 인명구조 수요 증가로 인해 항공 구급차가 9.2%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장세를 보이고 있습니다. 실시간 데이터 공유 툴을 통해 현장의 구급대원과 원격지의 전문의가 협업할 수 있게 되어 임상 범위의 확대와 경쟁적 차별화를 촉진하고 있습니다. 한편, 인력 부족과 단편적인 규제 프레임워크가 수익률을 압박하고 있으며, 사업자들은 통합과 국경을 초월한 제휴로 나아가고 있습니다.

세계 구급차 서비스 시장 동향 및 인사이트

전 세계적으로 외상, 심혈관계 응급질환 및 기타 시간적 제약이 있는 의료 상태의 발생률 상승

병원외 심정지(OHCA) 및 교통사고 외상 증가 추세는 전개 전술의 재구축을 지속적으로 촉구하고 있습니다. 미국 데이터에 따르면, 연간 약 35만 건의 OHCA가 발생하고 있으며, 응급의료기관은 드론을 이용한 자동심장충격기(AED) 배치를 추진하고 있습니다. 이를 통해 도착 시간을 5분 이내로 단축하고 생존율을 34% 향상시킬 수 있습니다. 도심의 혼잡은 이러한 하이브리드 대응 모델의 필요성을 더욱 강화하고 있으며, 기존 지상 차량을 보완하는 항공 자산에 대한 투자를 촉진하고 있습니다. 사업자는 구급차 서비스 시장이 지자체에 신속대응 플랫폼 라이선싱을 통해 추가 수익을 얻을 수 있을 것으로 예상하고 있습니다.

고령화와 만성질환 증가

65세 이상 노인은 전체 인구의 12%를 차지함에도 불구하고 응급환자의 1/3, 비응급환자의 2/3를 차지합니다. 지방에서는 이용률이 더욱 상승하고 있으며, 고령자를 위한 프로토콜, 비만 환자를 위한 들것, 집에서 병원으로 가는 셔틀 네트워크의 필요성이 가속화되고 있습니다. 시장 진출기업들은 80세 이상 수요가 구급차 서비스 시장 규모에 예측 가능한 베이스라인 요청량을 정착시켜 급성 질환 유행에 따른 주기적 변동성을 완화할 것으로 예상하고 있습니다.

높은 자본 지출 및 운영비

신형 디젤식 I형 구급차는 28만 달러 이상, 배터리식 전기 구급차는 35만 달러 이상의 가격대를 형성하고 있어 지자체 예산에 부담을 주고 있습니다. 2022년 메디케어의 구급차 이용 비용은 39억 달러(전체 진료비의 1%에 불과)에 달하고, 수익과 지출의 불균형이 두드러지게 나타나고 있습니다. 수익성 악화로 인해 소규모 차량 보유 사업자들은 자산 매각에 나서고 있으며, 이는 통합을 촉진하고 궁극적으로 공급업체 선택의 폭을 좁힐 수 있습니다.

부문 분석

항공 부문은 매출 비중은 작지만 CAGR 9.05%를 나타낼 것으로 예측됩니다. 차량 업데이트에서는 신생아 및 심장병 환자 이송 범위를 확대하는 가압 캐빈이 장착된 고정익 항공기를 우선적으로 도입할 예정입니다. 한편, 지상 구급차는 2025년 매출의 약 73.55%를 차지하며 구급차 서비스 시장에서 가장 큰 점유율을 유지할 것으로 예측됩니다. 패터슨 소방서에 90만 8,686달러에 전기 구급차 2대를 공급한 연방 보조금 제도는 지방정부가 저공해 차량으로의 전환을 추진하고 있음을 보여줍니다. 이러한 설비 투자는 지속 가능한 갱신 주기를 촉진하고 전체 구급차 서비스 시장 규모를 보호합니다.

지상군은 엔진 공회전 없이 장비를 구동하는 배터리 내장형 생명유지장치를 늘려 배치하여 디젤 연료 소비를 30% 절감하고 있습니다. 한편, 항공사는 연료 가격 변동 리스크를 줄이기 위해 연료 헤지 대량 계약 협상과 지속 가능한 항공 연료의 시험 도입을 추진하고 있습니다. 애널리스트들은 듀얼 모달리티 사업자(지상과 항공을 모두 지원하는)가 복잡한 시설 간 운송을 장악하고, 배차 소프트웨어와 정비 시설에서 시너지를 창출할 것으로 예측했습니다.

첨단 구급차량은 비록 대수는 적지만, 8.62%의 연평균 복합 성장률(CAGR)로 빠르게 성장하고 있습니다. 각 응급구조사 차량에는 인공호흡기, 수액펌프, 현장 초음파 장치를 탑재하여 이송 중 복잡한 처치를 가능하게 합니다. 구급대원은 의사의 감독 하에 비디오 링크를 통해 신속 도입 약물을 투여할 수 있습니다. 이 기능을 통해 지방 이송 시 환자 안정화를 향상시키고, 유리한 사례 혼합 지불(사례 혼합 지불)을 보장합니다.

한편, 기초 생명 유지(BLS) 부문은 2025년 기준 59.05%의 점유율을 유지하며 일상적인 시설 간 이송 및 투석 셔틀의 기반을 담당하고 있습니다. BLS 인력의 운영 비용이 낮고, 최근 연구에 따르면 특정 조건에서 BLS 환자의 퇴원 시 생존율이 13.1%, ALS 환자의 경우 9.2%로 나타났습니다. 이 발견은 자원 배분에 대한 논의를 불러일으키고 있으며, 일부 시스템에서는 ALS 유닛을 저응급 이송에서 고위험 요청으로 재배치하고 있습니다. 그러나 지불 기관이 비용 효율성을 중시하기 때문에 BLS 구급차 서비스 시장 규모는 여전히 크고 안정적으로 유지되고 있습니다.

지역별 분석

북미가 매출 1위, 세계 점유율 34.05%로 1위를 차지했습니다. 긴급 이송 시 차액 청구를 금지하는 연방 규정에 따라 비용의 투명성이 높아져 회수율이 향상될 것으로 예측됩니다. 규제 시행을 예상한 민간 보험사들은 응급 의료 서비스와 병원에 대한 종합적인 지불 패키지로의 전환을 추진하고 있으며, 차량 소유자의 수익 변동을 완화할 수 있습니다. 메이요 클리닉이 주도하는 원격의료 시범사업은 이 지역이 첨단기술에 대한 열정을 입증하고, 통신 벤더의 수출 기회를 시사하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 9.18%로 가장 빠르게 성장하는 지역으로 부상하고 있습니다. 각국 정부가 차량 확충에 자금을 투입하는 한편, 보험사들은 의료보험 최초 가입자 층으로 확대하여 구급차 이용률을 직접적으로 끌어올리고 있습니다. 중국 14차 5개년 계획에서 응급구조 현대화를 중점 과제로 설정하고, 외상센터 정비에 31억 달러를 책정함. 농촌 지역의 분절된 지형은 여전히 공평한 접근을 방해하고 있으며, 산악 지역에서는 항공 구급이 매력적인 보완 수단으로 작용하고 있습니다.

유럽은 여전히 구급차 서비스 시장에서 큰 점유율을 유지하고 있으며, 지속가능성 관련 규제에서 선도적인 위치를 차지하고 있습니다. 스코틀랜드의 넷 제로 차량 계획은 도시 간 이동을 위한 수소 연료전지 테스트에 자금을 투입하고 있습니다. 한편, EU의 입찰은 점점 더 많은 수명주기 탄소 보고를 요구하고 있으며, 제조업체는 재활용 가능한 복합재 바디를 채택해야 합니다. 고령화를 배경으로 슬로베니아의 예측에 따르면 75세 이상 인구에 연동된 출동 건수가 꾸준히 증가할 것으로 예측됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액, 백만 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

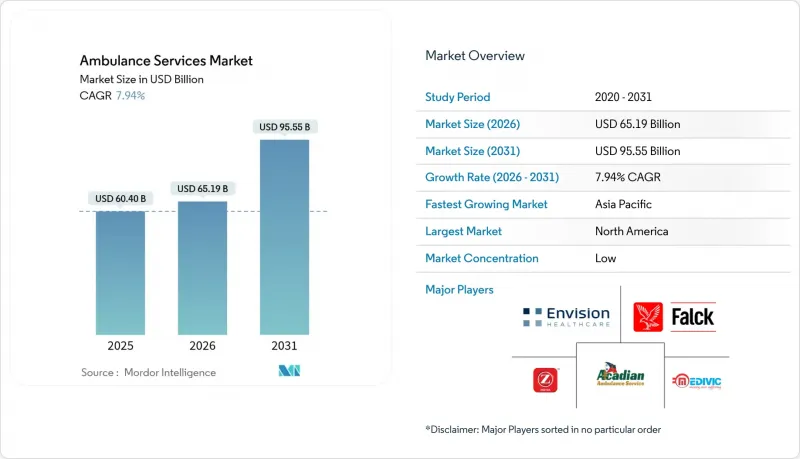

LSH 26.03.10Ambulance services market size in 2026 is estimated at USD 65.19 billion, growing from 2025 value of USD 60.4 billion with 2031 projections showing USD 95.55 billion, growing at 7.94% CAGR over 2026-2031.

Expansion reflects rising demand for rapid pre-hospital care, stronger health-insurance coverage, and widespread uptake of connected-care technology. Asia-Pacific delivers the fastest growth at 9.4% as governments upgrade emergency medical services (EMS) and insurers scale coverage in emerging economies. Ground ambulances remain the revenue anchor, but air ambulances post the quickest gains at 9.2% CAGR, spurred by longer-range, fuel-efficient aircraft and growing appetite for critical-care retrieval. Real-time data-sharing tools now link field paramedics with remote specialists, widening clinical scope and sharpening competitive differentiation. At the same time, staffing shortfalls and fragmented regulatory frameworks weigh on margins, pushing operators toward consolidation and cross-border partnerships.

Global Ambulance Services Market Trends and Insights

Rising Global Incidence of Trauma, Cardiovascular Emergencies, and Other Time-Critical Medical Conditions

The upward trend in out-of-hospital cardiac arrest (OHCA) and road-traffic trauma continues to reshape deployment tactics. U.S. data point to roughly 350,000 OHCA episodes annually, prompting EMS agencies to field drone-delivered automated external defibrillators (AEDs) that can cut arrival times to under five minutes and uplift survival odds by 34%. Urban congestion reinforces the need for such hybrid response models, guiding investment towards complementary airborne assets that augment traditional ground fleets. Operators expect the ambulance services market to derive incremental revenue from licensing rapid-response platforms to city authorities.

Aging Population and Increasing Prevalence of Chronic Diseases

Adults aged 65+ already account for one-third of emergency transports and two-thirds of non-urgent journeys, despite making up 12% of the population . Utilisation rates climb even higher in rural belts, accelerating the need for geriatric-specific protocols, bariatric stretchers, and home-to-hospital shuttle networks. Market participants anticipate that demand from octogenarians will embed predictable baseline call volumes into the ambulance services market size, cushioning cyclical swings linked to acute outbreaks.

High Capital and Operating Expenditures

A new Type I diesel ambulance costs upward of USD 280,000, while battery-electric variants breach the USD 350,000 threshold, straining municipal budgets. Medicare payments for ambulance rides consumed USD 3.9 billion in 2022-just 1% of fee-for-service spending-underscoring a revenue-expense mismatch. Tight margins are nudging smaller fleets toward asset sales, thereby fuelling consolidation that may ultimately narrow supplier choice.

Other drivers and restraints analyzed in the detailed report include:

- Government-Led Public-Private Partnerships and Funding Programs Aimed at Strengthening EMS Networks

- Expansion of Healthcare Infrastructure and Health-Insurance Coverage

- Integration of Telemedicine, Real-Time Monitoring, and Advanced Life-Support Equipment

- Increasing Incidences of Road Accidents

- Shortage of Trained Paramedics, Pilots, and Critical-Care Staff

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The air segment, though holding a smaller revenue slice, is projected to grow at a 9.05% CAGR. Fleet refresh favours fixed-wing airplanes fitted with pressurised cabins that extend retrieval range for neonatal and cardiac cases. At the same time, ground ambulances continue to anchor approximately 73.55% of 2025 revenue, preserving the largest ambulance services market share. The federal grant that supplied the Paterson Fire Department with two electric ambulances at USD 908,686 highlights municipalities' pivot toward low-emission fleets. Such capex drives a sustainable replacement cycle and protects total ambulance services market size.

Ground crews increasingly deploy battery-integrated life-support units that power equipment without engine idling, cutting diesel burn by 30%. Air operators, meanwhile, negotiate bulk fuel hedges and explore sustainable aviation fuel trials to mitigate cost volatility. Analysts predict that dual-modality providers will capture complex inter-facility transfers, unlocking synergies in dispatch software and maintenance facilities.

Advanced life support vehicles captured smaller volume but are scaling faster with an 8.62% CAGR. Each ALS ambulance houses ventilators, infusion pumps, and point-of-care ultrasound, enabling complex interventions in transit. Paramedics can push rapid-sequence induction drugs under physician oversight through video links. This capability improves patient stabilization during rural transfers and secures favorable case-mix payments.

In contrast, the basic life support segment retained 59.05% share in 2025 and anchors routine inter-facility and dialysis shuttles. Operating cost for BLS crews is lower, and recent studies found 13.1% hospital discharge survival among BLS patients versus 9.2% for ALS in select conditions . The findings spark debate on resource allocation, with some systems redeploying ALS units from low-acuity transport to high-risk calls. The ambulance services market size for BLS nonetheless remains large and stable as payers favor its cost efficiency.

The Ambulance Services Market Report Segments the Industry Into by Mode of Transport (Air Ambulance, and More), by Equipment (Basic Life Support Ambulance Services, and More), by Type of Service (Emergency Services, and More), by Ownership (Government/Municipal, and More), Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, South America). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America ranks first by revenue with a 34.05% global share. Federal rulemaking to outlaw balance billing for emergency rides should heighten cost transparency and improve collections. Private insurers, anticipating regulatory enforcement, are moving toward bundled EMS-hospital payment packages, potentially smoothing revenue volatility for fleet owners. Tele-medical pilots led by Mayo Clinic confirm the region's penchant for frontier tech, hinting at export opportunities for communication vendors.

Asia-Pacific emerges as the fastest-growing corridor at 9.18% CAGR through 2031. National governments finance fleet expansion, while insurers expand to first-time buyers of health cover, directly lifting ambulance utilisation. China's 14th Five-Year Plan designates emergency rescue modernisation as a priority, earmarking USD 3.1 billion for trauma-centre upgrades. Fragmented rural terrain still hampers equitable access, making aerial EMS an attractive adjunct in mountainous provinces.

Europe maintains a sizable slice of the ambulance services market and leads on sustainability mandates. Scotland's net-zero fleet blueprint funds hydrogen-fuel-cell trials for inter-city missions. Meanwhile, EU tenders increasingly require life-cycle carbon reporting, pressing manufacturers to adopt recyclable composite bodies. Against a backdrop of ageing demographics, Slovenian projections indicate a steady uptick in dispatch volume tied to population over-75.

- Acadian Ambulance Service

- Air Methods

- American Medical Response

- Envision Healthcare

- Falck A/S

- Dutch Health B.V.

- BVG India

- Ziqitza Health Care Ltd

- GVK Emergency Management & Research Institute

- Medivic Aviation

- Scandinavian AirAmbulance

- Air Medical Group Holdings

- Lifeline Ambulance Services (UK)

- London Ambulance Service NHS Trust

- National Ambulance LLC (UAE)

- Air Charter Services Ltd (Kenya)

- St John Ambulance Australia

- SA Ambulance Service

- EMS Group (Japan)

- Aero Asahi Corporation

- PHI Air Medical

- REVA Air Ambulance

- CareFlight International

- Express Ambulances India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Incidence Of Trauma, Cardiovascular Emergencies, And Other Time-Critical Medical Conditions

- 4.2.2 Aging Population And Increasing Prevalence Of Chronic Diseases

- 4.2.3 Government-Led Public-Private Partnerships And Funding Programs Aimed At Strengthening National And Regional EMS Networks.

- 4.2.4 Expansion Of Healthcare Infrastructure And Health-Insurance Coverage

- 4.2.5 Integration Of Telemedicine, Real-Time Monitoring, And Advanced Life-Support Equipment

- 4.2.6 Increasing Incidencs Of Raod Accidents

- 4.3 Market Restraints

- 4.3.1 High Capital And Operating Expenditures

- 4.3.2 Shortage Of Trained Paramedics, Pilots, And Critical-Care Staff

- 4.3.3 Competitive Pressure From Non-Emergency Medical Transport And Rideshare Health-Transport Services

- 4.3.4 Fragmented Regulatory Accreditation Raising Compliance Costs

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD million)

- 5.1 By Mode of Transport

- 5.1.1 Air Ambulance

- 5.1.1.1 Rotary-Wing

- 5.1.1.2 Fixed-Wing

- 5.1.2 Water Ambulance

- 5.1.3 Ground Ambulance

- 5.1.3.1 Type III Van

- 5.1.3.2 Type I/II Modular

- 5.1.3.3 Hybrid-Electric/EV Ambulance

- 5.1.1 Air Ambulance

- 5.2 By Equipment

- 5.2.1 Basic Life Support (BLS) Ambulance Services

- 5.2.2 Advanced Life Support (ALS) Ambulance Services

- 5.2.3 Specialty Care Transport (SCT)

- 5.3 By Type of Service

- 5.3.1 Emergency Services

- 5.3.2 Non-Emergency Services

- 5.4 By Ownership

- 5.4.1 Government/Municipal

- 5.4.2 Private Corporate

- 5.4.3 Hospital-Based

- 5.4.4 Volunteer/NGO

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Acadian Ambulance Service Inc.

- 6.3.2 Air Methods Corporation

- 6.3.3 American Medical Response

- 6.3.4 Envision Healthcare Corporation

- 6.3.5 Falck A/S

- 6.3.6 Dutch Health B.V.

- 6.3.7 BVG India Ltd

- 6.3.8 Ziqitza Health Care Ltd

- 6.3.9 GVK Emergency Management & Research Institute

- 6.3.10 Medivic Aviation

- 6.3.11 Scandinavian AirAmbulance

- 6.3.12 Air Medical Group Holdings

- 6.3.13 Lifeline Ambulance Services (UK)

- 6.3.14 London Ambulance Service NHS Trust

- 6.3.15 National Ambulance LLC (UAE)

- 6.3.16 Air Charter Services Ltd (Kenya)

- 6.3.17 St John Ambulance Australia

- 6.3.18 SA Ambulance Service

- 6.3.19 EMS Group (Japan)

- 6.3.20 Aero Asahi Corporation

- 6.3.21 PHI Air Medical

- 6.3.22 REVA Air Ambulance

- 6.3.23 CareFlight International

- 6.3.24 Express Ambulances India

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment