|

시장보고서

상품코드

1940593

대장 관리 시스템 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Bowel Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

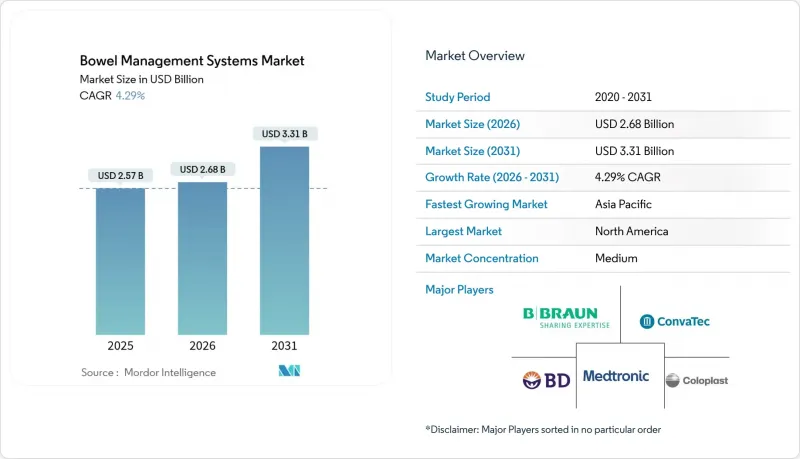

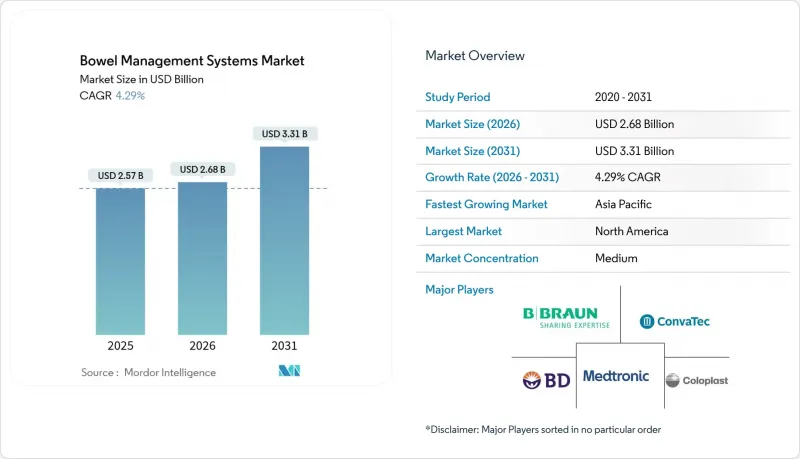

대장 관리 시스템 시장은 2025년에 25억 7,000만 달러로 평가되었고, 2026년 26억 8,000만 달러에서 2031년까지 33억 1,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 4.29%로 예상됩니다.

고령화 인구 증가, 염증성 장질환(IBD)의 유병률 증가, 스마트 센서 장착 장루 및 신경 조절 솔루션의 급속한 보급과 함께 완만하지만 꾸준한 성장 궤도를 형성하고 있습니다. 북미는 탄탄한 상환제도와 빠른 기술 도입으로 수요 주도권을 유지하고 있습니다. 한편, 아시아태평양은 급증하는 IBD 발병률에 대응하기 위해 의료 시스템에 대한 투자가 가장 역동적으로 확대되고 있습니다. 65세 이후 장 기능 장애의 유병률이 급격히 증가하기 때문에 노인 환자가 수요 증가를 주도하고 있습니다. 제품 혁신으로 인해 시장은 수동적인 장루 관리에서 능동적이고 디지털로 모니터링되는 개입, 특히 신경 조절 장치를 중심으로 한 능동적인 개입으로 전환하고 있습니다. 텔레코칭 및 원격 모니터링 플랫폼을 기반으로 한 재택 케어 도입의 병행 성장으로 대장 관리 시스템 시장의 발자취가 더욱 확대되고 있습니다.

세계 대장 관리 시스템 시장 동향과 인사이트

염증성 장질환의 높은 발병률

미국에서는 240만-310만 명이 IBD를 앓고 있으며, 연간 85억 달러의 직접적 비용이 발생하고 있습니다. 식생활과 환경적 요인의 변화에 따라 신흥 아시아 경제권에서 발병률이 가장 빠르게 증가하고 있습니다. 이러한 역학적 전환은 대장 관리 시스템 시장 전체에서 장루 주머니, 세척 시스템, 신경 조절 요법에 대한 장기적인 수요를 뒷받침하고 있습니다. 소아 IBD 증가에 따라 미국 식품의약국(FDA)은 특정 개발 지침을 발표하여 간접적으로 연령에 적합한 의료기기의 혁신을 촉진하고 있습니다. 의료 시스템은 현재 센서 데이터를 통합한 만성 질환 관리 경로를 우선시하고 있으며, 이를 통해 기술을 활용한 솔루션이 일상적인 관리에 더욱 통합되고 있습니다.

급증하는 노인 인구

노화에 따른 대장의 퇴행성 변화, 통증 수용체의 신경 지배력 감소, 동반 질환의 축적으로 인해 65세 이후에는 변비와 요실금이 현저하게 증가합니다. 향후 20년간 대장수술 예측에 따르면 외래수술은 21.3%, 입원수술은 40.6% 증가할 것으로 예상되며, 이는 주로 65-74세 연령층이 92% 확대되는 것이 주요 요인으로 작용할 것으로 보입니다. 이에 따라 의료기기 제조업체들은 장기 요양 시설의 피부염 발생률을 낮추는 간소화된 파우치 시스템, 직관적인 세척 제어, 스마트 기저귀 센서에 중점을 두고 있습니다. 이러한 혁신 기술들은 종합적으로 대장 관리 시스템 시장에서 다년간의 안정적인 수요 증가를 뒷받침하고 있습니다.

환자의 보수적/비침습적 치료에 대한 선호도

식이요법과 약물 치료는 여전히 많은 환자들에게 첫 번째 선택이며, 침습적 장루 및 이식형 솔루션의 도입을 지연시키고 있습니다. 중국의 장루 환자들을 대상으로 한 삶의 질(QOL) 조사에서 수술 수용을 방해할 수 있는 중등도의 심리사회적 부담이 밝혀졌습니다. 따라서 시장 기업들은 환자의 의사를 존중하면서 대장 관리 시스템 시장 전체에서 측정 가능한 증상 완화를 실현할 수 있는 단계적 대안으로 경항문 세척 및 저침습적 신경 자극을 포지셔닝하고 있습니다.

부문 분석

대장 관리 시스템 시장은 2025년 53.21%의 점유율을 차지한 장루 주머니에 대한 핵심 수요에 힘입어 성장하고 있습니다. 병원, 방문간호사, 공급업체들은 장루 주변 피부를 보호하고 밀착력을 유지하는 다층 하이드로콜로이드 및 실리콘 배리어 제품에 계속 의존하고 있습니다. 현재 고급화 제품에는 수증기 투과층과 항균 코팅이 내장되어 있어 가격에 민감한 시장에서 벤더가 수익률을 유지할 수 있도록 하고 있습니다. 또한, 유럽의 일회용 플라스틱 규제 강화에 대응하여 재생가능 수지를 채택함으로써 제품 수명주기를 연장하여 배변관리 시스템 시장에서의 지속적인 수익 유지를 뒷받침하고 있습니다.

신경조절 기기는 천골신경, 경골신경, 척수경로를 활용하여 배변기능 회복을 도모하는 것으로 6.45%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장세를 보이고 있습니다. 보스턴 사이언티픽의 Axionix 37억 달러 인수는 급성기 임플란트 기술과 세계 판매망을 통합하여 제품 포트폴리오의 시너지를 촉진하고, Medtronic과의 경쟁을 강화할 수 있는 계기가 될 것입니다. 대장 관리 시스템 업계의 신경 조절 파이프라인은 현재 배터리가 필요 없는 마이크로 자극기 및 외래수술센터(ASC)를 위해 설계된 외부 펄스 발생기 옵션으로 확장되고 있습니다. 웰스펙트의 나비나 관류 키트와 마그네틱 괄약근 임플란트는 영구적인 배설 경로 변경을 피하면서 기존 파우치를 대체할 수 있는 한 단계 업그레이드된 대안을 제공하면서 활기찬 중간 계층을 형성하고 있습니다.

지역별 분석

북미는 첨단 천골 신경 자극 요법 및 고주파 관류 시스템을 포함하는 상환 정책에 힘입어 전 세계 지출의 37.86%를 차지합니다. 컴버텍은 대장 관리 사업의 매출 성장률 8.2%를 유리한 가격 조정과 피부장벽 제품의 처방 확대에 기인한다고 설명했습니다. 디지털 건강 모니터링의 보험사 채택은 입원 기간을 단축하고, 이 지역을 대장 관리 시스템 시장에서 혁신의 시험대로 확고히 자리매김하고 있습니다.

아시아태평양은 급속한 역학적 전환, 도시화, 현대식 수술실에 대한 공공 부문 투자에 힘입어 2031년까지 연평균 6.83%의 성장률을 보이며 가장 빠르게 성장하는 지역으로 꼽혔습니다. 호주에서 Axonics의 F15 뉴로모듈레이터의 승인은 규제 당국이 첨단 치료법에 대해 긍정적인 태도를 보이고 있음을 보여줍니다. 중국 일류 병원에서는 스마트 파우치 상설화가 표준화되었고, 인도 민간 보험사는 경항문 세척 요법에 대한 종합적인 지불 제도를 시범 도입하는 등 대장 관리 시스템 시장 전체가 기존 소모품에서 기술 지원형 관리로 전환하고 있습니다.

유럽에서는 전국민 의료보험제도와 엄격한 환경지침을 바탕으로 재활용 가능한 파우치 수요를 가속화하여 꾸준한 성장세를 유지하고 있습니다. 독일에서 디지털 IBS 치료제에 대한 영구적인 보험 적용은 소프트웨어를 의료기기로 간주하는 솔루션으로의 광범위한 전환에 박차를 가하고 있습니다. 반면, 중동 및 아프리카 및 남미 지역은 성장세를 보이고 있지만 여전히 작은 점유율을 차지하고 있습니다. 인프라 부족, 전문의 양성의 한계, 보험 적용 범위의 제약이 미개척 환자층이 방대함에도 불구하고 단기적인 보급을 억제하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The Bowel Management Systems Market was valued at USD 2.57 billion in 2025 and estimated to grow from USD 2.68 billion in 2026 to reach USD 3.31 billion by 2031, at a CAGR of 4.29% during the forecast period (2026-2031).

The modest but steady trajectory mirrors a confluence of aging populations, rising inflammatory bowel disease (IBD) prevalence, and rapid uptake of smart, sensor-enabled ostomy and neuromodulation solutions. North America retains demand leadership on the back of robust reimbursement and early technology adoption, while Asia-Pacific shows the most dynamic expansion as health-system investments meet sharply climbing IBD incidence. Geriatric patients drive incremental volumes because bowel dysfunction prevalence rises steeply after 65 years. Product innovation is shifting the market from passive ostomy care toward active, digitally monitored interventions, particularly nerve modulation devices. Parallel growth in home-care adoption, underpinned by tele-coaching and remote monitoring platforms, further broadens the bowel management systems market footprint.

Global Bowel Management Systems Market Trends and Insights

High Incidence of Inflammatory Bowel Disease

IBD affects 2.4-3.1 million people in the United States and drives USD 8.5 billion in direct annual costs. Incidence is rising fastest in newly industrialised Asian economies as dietary and environmental factors evolve. This epidemiological transition sustains long-run demand for ostomy bags, irrigation systems, and neuromodulation therapies across the bowel management systems market. Pediatric IBD growth has prompted the US FDA to issue specific development guidance, indirectly encouraging age-appropriate device innovation. Health systems now prioritise chronic-care pathways that integrate sensor data, which further embeds technology-enabled solutions into routine management.

Rapidly Growing Geriatric Population

Degenerative colonic changes, reduced nociceptor innervation, and comorbidity clustering make constipation and incontinence markedly more common after 65 years. Procedure forecasts show a 21.3% rise in outpatient and 40.6% rise in inpatient colorectal interventions over the next two decades, largely owing to a 92% expansion in the 65-74 year cohort. In response, device makers emphasise simplified pouching systems, intuitive irrigation controls, and smart diaper sensors that cut dermatitis incidence in long-term care settings. Collectively, these innovations anchor stable multi-year volume gains within the bowel management systems market.

Patient Preference for Conservative / Non-Invasive Options

Dietary modification and pharmacotherapy remain first-line choices for many patients, delaying adoption of invasive ostomy or implantable solutions. Quality-of-life studies in Chinese ostomy populations reveal moderate psychosocial burden that can discourage surgical acceptance. Market players are therefore positioning transanal irrigation and mini-invasive nerve stimulation as step-up alternatives that respect patient preferences yet deliver measurable symptom relief across the bowel management systems market.

Other drivers and restraints analyzed in the detailed report include:

- Reimbursement Expansion for Advanced Therapies

- Smart-Sensor Ostomy Pouches

- Post-Operative Infections & Device Complication Recalls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The bowel management systems market rests on the core demand for ostomy bags, which captured 53.21% share in 2025. Hospitals, home-health nurses, and supply distributors continue to rely on multi-layer hydrocolloid and silicone barriers that maintain secure adhesion and protect peristomal skin. Up-market offerings now incorporate moisture-vapour transmission layers and antimicrobial coatings, allowing vendors to defend margins in a price-sensitive space. Product lifecycles also lengthen as recyclable resins answer tightening single-use-plastic rules in Europe, supporting incremental revenue retention in the bowel management systems market.

Nerve modulation devices deliver the fastest expansion at a 6.45% CAGR by leveraging sacral, tibial, and spinal pathways to restore bowel continence. Boston Scientific's USD 3.7 billion purchase of Axonics combined acute implant know-how with global sales reach, fuelling portfolio synergies and intensifying rivalry with Medtronic. The bowel management systems industry's neuromodulation pipeline now spans battery-free microstimulators and externalized pulse-generator options designed for ambulatory surgery centres. Wellspect's Navina irrigation kits and magnetic sphincter implants form a vibrant middle tier, offering step-up alternatives to conventional pouches while avoiding permanent diversion.

The Bowel Management Systems Market Report is Segmented by Product (Ostomy Bags [Colostomy Bags, and More], Transanal Irrigation Systems, Nerve Modulation Devices, Anal Implants & Artificial Sphincters, and More), Patient Type (Pediatric, Adult, Geriatric), End User (Hospitals, Ambulatory Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America steers 37.86% of global spending, supported by reimbursement policies that now cover advanced sacral nerve stimulation and high-frequency irrigation systems. ConvaTec attributed 8.2% Continence Care revenue growth to favourable pricing adjustments and an expanding formulary of skin barriers. Payer embrace of digital health monitoring shortens hospital stays and cements the region's position as an innovation test bed for the bowel management systems market.

Asia-Pacific is the fastest regional climber at a 6.83% CAGR through 2031, driven by rapid epidemiological transition, urbanisation, and public-sector investment in modern surgical suites. Australian clearance of Axonics' F15 neuromodulator showcases regulators' receptiveness to cutting-edge interventions. China's tier-1 hospitals now routinely stock smart pouches, and India's private insurers pilot bundled payments for transanal irrigation, indicating a pivot from legacy consumables to tech-enabled management across the bowel management systems market.

Europe maintains steady growth anchored by universal healthcare and stringent environmental directives that hasten demand for recyclable pouches. Germany's permanent reimbursement of a digital IBS therapeutic adds momentum to a broader shift toward software-as-a-medical-device solutions. Meanwhile, Middle East & Africa and South America contribute a rising but still modest share; infrastructure gaps, limited specialist training, and constrained insurance coverage temper near-term adoption despite sizeable untapped patient pools.

- Coloplast

- ConvaTec Group plc

- Hollister

- Medtronic

- Beckton Dickinson

- B. Braun

- 3M

- Boston Scientific

- Wellspect Healthcare

- Consure Medical Pvt Ltd

- Laborie Medical Technologies

- MacGregor Healthcare Ltd

- Implantica AG

- Cook MyoSite

- Abena A/S

- Cardinal Health

- Cogentix Medical

- Stryker

- Smiths Group

- ABC Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Incidence of Inflammatory Bowel Disease (IBD)

- 4.2.2 Rapidly Growing Geriatric (65+) Population

- 4.2.3 Reimbursement Expansion for Ostomy & Neuromodulation Therapies

- 4.2.4 Smart-Sensor Ostomy Pouches Enabling Remote Monitoring

- 4.2.5 ESG Push Toward Recyclable Single-Use Ostomy Materials

- 4.2.6 Tele-Coaching Platforms for Neurogenic Bowel Management

- 4.3 Market Restraints

- 4.3.1 Patient Preference for Conservative / Non-Invasive Options

- 4.3.2 Post-Operative Infections & Device Complication Recalls

- 4.3.3 High Upfront Cost of Sacral-Nerve Stimulation Implants

- 4.3.4 Regulatory Scrutiny on Single-Use Plastic Waste

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product

- 5.1.1 Ostomy Bags

- 5.1.1.1 Colostomy Bags

- 5.1.1.2 Ileostomy Bags

- 5.1.1.3 Urostomy Bags

- 5.1.2 Transanal Irrigation Systems

- 5.1.2.1 Manual Pump-based Irrigation

- 5.1.2.2 Electronic Smart Irrigation

- 5.1.3 Nerve Modulation Devices

- 5.1.3.1 Sacral Nerve Stimulation Systems

- 5.1.3.2 Tibial Nerve Stimulation Systems

- 5.1.4 Anal Implants & Artificial Sphincters

- 5.1.4.1 Hydraulic Artificial Sphincters

- 5.1.4.2 Magnetic Sphincters

- 5.1.5 Skin Barriers & Accessories

- 5.1.5.1 Skin Barrier Sheets & Rings

- 5.1.5.2 Deodorizing Filters & Pouch Accessories

- 5.1.1 Ostomy Bags

- 5.2 By Patient Type

- 5.2.1 Pediatric (<18 yrs)

- 5.2.2 Adult (18-64 yrs)

- 5.2.3 Geriatric (65+ yrs)

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Home Care Settings

- 5.3.4 Skilled Nursing Facilities

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Coloplast A/S

- 6.3.2 ConvaTec Group plc

- 6.3.3 Hollister Incorporated

- 6.3.4 Medtronic

- 6.3.5 Becton Dickinson & Company

- 6.3.6 B. Braun Melsungen AG

- 6.3.7 3M Company

- 6.3.8 Boston Scientific Corp.

- 6.3.9 Wellspect Healthcare

- 6.3.10 Consure Medical Pvt Ltd

- 6.3.11 Laborie Medical Technologies

- 6.3.12 MacGregor Healthcare Ltd

- 6.3.13 Implantica AG

- 6.3.14 Cook MyoSite

- 6.3.15 Abena A/S

- 6.3.16 Cardinal Health Inc.

- 6.3.17 Cogentix Medical

- 6.3.18 Stryker Corp.

- 6.3.19 Smith & Nephew plc

- 6.3.20 ABC Medical Supply Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment