|

시장보고서

상품코드

1940614

중정석 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Barite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

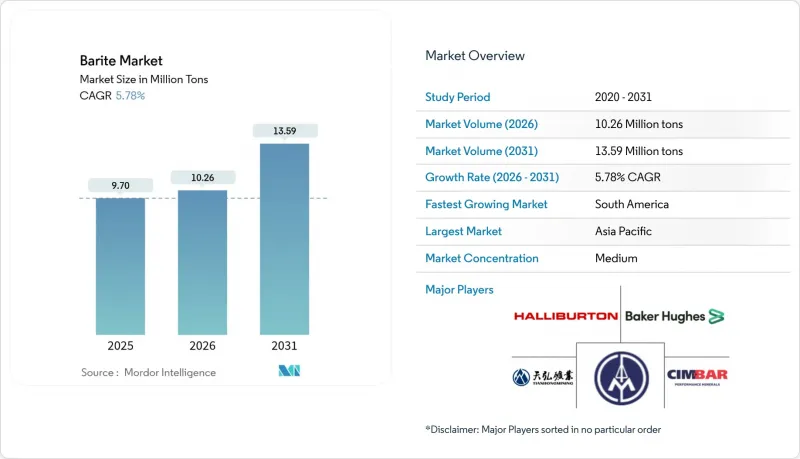

중정석 시장은 2025년 970만 톤에서 2026년에는 1,026만 톤으로 성장하고, 2026-2031년 2026-2031년 CAGR5.78%로 성장을 지속하여 2031년까지 1,359만 톤에 이를 것으로 예측됩니다.

채굴량의 약 80%를 소비하는 유전 서비스 사업자의 견조한 구매가 수요를 뒷받침하고 있으며, 초심해 및 고압 유정의 신규 해양 시추 프로젝트가 물량 성장을 가속화하고 있습니다. 중국, 인도 등 주요 생산국의 수출 규제 강화로 가격 규율이 강화되어 시추업체들의 재고 헤징이 촉진되고 있습니다. 의료용 영상진단, 코팅, 폴리머 컴파운딩과 같은 틈새 분야의 급속한 수요 증가는 성장의 탄력성을 더욱 뒷받침하고 있습니다. 이들 분야는 원유 연동형 시추 활동이 둔화될 때 고품질 황산 바륨을 흡수합니다. 또한, 미분화 고비중 등급에서 하이브리드 수계 시스템에 이르기까지 엔지니어링 시추 유체의 지속적인 발전으로 공급처는 부가가치 사양으로 전환하고 있으며, 이는 톤당 실현 가격의 상승으로 이어지고 있습니다. 따라서 경쟁도는 대규모의 안정적인 광상에 대한 접근성과 다운스트림 공정의 배합 기술에 따라 좌우되며, 수직 통합형 대형 유전 서비스 기업이 분산된 광산업체들에 대한 협상력을 발휘하고 있습니다.

세계 중정석 시장 동향과 인사이트

라틴아메리카의 심해 및 고압 고온 시추의 급성장

브라질, 멕시코, 가이아나의 초심해 프로젝트에서는 수심 2,500m, 수온 200°C 이상의 환경을 견딜 수 있는 시추 유체가 요구되고 있습니다. 지층 압력을 제어하기 위해 더 높은 진흙장 비중이 필요하기 때문에 이러한 우물에서는 표준 육상 프로젝트보다 더 많은 중정석을 소비합니다. SLB가 우드사이드사의 트리온 유전에 공급한 18개 유정 패키지는 이러한 높은 수요를 보여주며, 우수한 현탁 안정성을 위해 10미크론 이하의 미세 분말화 중정석으로 전환이 진행되고 있음을 보여줍니다. 브라질의 프리솔트층 클러스터와 아르헨티나의 바카 무에르타 셰일 클러스터는 동시에 인프라 자본을 유치하여 고급 광석에 대한 지역적 창고 및 분쇄 능력을 확장하고 있습니다. 중요 광물 공급망의 현지화를 장려하는 정부의 인센티브는 수요 전망을 더욱 강화할 것입니다. 이러한 요인들이 복합적으로 작용하여 라틴아메리카는 중기적으로 세계 중정석 시장에서 중기적으로 성장하여 고비중 등급의 프리미엄 가격을 지지하고 있습니다.

북미에서 비재래식 탄화수소의 부상

셰일 사업자들은 시추 리그 수는 정체되어 있음에도 불구하고, 유정당 가중제 소비량을 늘리기 위해 유정 연장 및 스테이지 수 고밀도화를 지속하고 있습니다. 우량 광구의 고갈로 인해 활동은 2급 지역으로 이동하고 있습니다. 이 지역은 더 높은 압력 창을 보여주기 때문에 더 높은 비중의 진흙탕이 필요합니다. Halliburton의 Barahib 및 Baker Hughes의 PERFORMAX 수성 시스템은 유성 진흙탕과 동등한 성능을 유지하면서 중정석 함량을 15-20% 증가시켜 동등한 비중을 달성하는 방법을 입증했습니다. 자본 지출 억제에도 불구하고 리버티 에너지의 2025년 2분기 완공 수익이 10억 4,200만 달러에 달한 것은 셰일 관련 사업의 지속적인 규모를 입증하고 있습니다. 이에 공급망은 리드타임 단축을 위해 서부 텍사스 및 록키 산맥 지역에 철도 연결형 트랜스로드 터미널을 증설하여, 바륨 시장의 지속 가능한 베이스라인 수요를 확립하고 있습니다.

합성 헤마타이트 진흙장 대체품

헤마타이트나 일메나이트와 같은 산화철계 가중제는 비중 4.95-5.10을 달성할 수 있으며, 동등한 밀도에서 더 낮은 점도의 진흙탕을 가능하게 합니다. 킹파하드 대학의 연구에 따르면, 유성 진흙탕에서 중정석의 40%를 일메나이트(ilmenite)로 대체했을 때 침강 제로가 확인되었고, 유변학적 특성과 전기적 안정성이 모두 향상되었습니다. 서비스 대기업들은 중정석 부족에 대한 헤지 수단인 복합가중제 블렌드 개발을 위한 연구개발 프로그램을 통해 대응하고 있습니다. 철광석의 현지 처리가 가능한 지역(특히 캐나다와 스칸디나비아)에서는 비용 경쟁력이 향상되어 이들 지역에서 중정석 시장 점유율이 감소하는 추세입니다. 환경 규제 당국도 중금속 침출수가 적다는 점에서 적철광을 긍정적으로 평가하고 있으며, 생태계에 민감한 지역에서는 대체가 가속화될 수 있는 요인으로 작용할 수 있습니다.

부문 분석

2025년 기준, 층상 광상이 전 세계 생산량의 74.65%를 공급하고 있으며, 이는 규모의 경제와 안정적인 광석 품질을 반영합니다. 이 부문의 우위는 장기 계약의 안정성으로 이어지고 있으며, 특히 중국 구이저우성 생산자와 인도 안드라프라데시주 광산회사가 중정석 시장의 물류 기반을 뒷받침하고 있습니다. 잔류광상은 규모는 작지만 6.03%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장세를 보이고 있습니다. 이는 더 높은 본질적 품위가 선광 비용을 낮추기 때문입니다. 파키스탄의 쿠즈다르 광맥 시스템(볼란 마이닝 엔터프라이즈 운영)은 4.30 SG 이상의 고급 광석을 프리미엄 용도로 공급함으로써 소규모 사업자가 경쟁력을 유지하는 좋은 사례입니다. 따라서 지역이 위험과 수익의 계산을 좌우한다: 아시아의 층상 광산은 대량 시추 수요에 대응하는 반면, 광맥 및 잔류 광상은 페인트 및 의료 분야의 틈새 시장을 포착하고 있습니다.

점유율 우위를 유지하고 있는 층상광산도 API 13A 규격에 맞추기 위해 여러 단계의 선별 공정을 거쳐야 하는 품위 변동에 직면해 있습니다. 따라서 자본 예산은 고밀도화 회로, 자기분리, 광학 선별에 투입되어 고정비 레버리지가 향상되었습니다. 바레이트 시장에서는 규모와 부문 간 주문에 대응하는 유연한 처리 메뉴를 겸비한 사업자가 우위를 점할 수 있습니다. 반면, 모로코와 네바다주의 맥석광상은 소량의 고순도 용도에 공급되며, 시추 사이클에 연동된 가격 변동에 영향을 덜 받는 특성을 가지고 있습니다. 대규모 층상 광상 사업과 전문 맥석 공급업체가 공존함으로써 공급의 탄력성이 강화되어 장기적인 수요의 안정적 공급을 뒷받침하고 있습니다.

중정석 시장 보고서는 광상 유형(층상, 맥상 및 공동 충전, 잔류), 최종 이용 산업(석유 및 가스, 화학, 필러, 의료 및 진단, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카) 별로 분류됩니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 세계 톤수의 41.35%를 차지할 것으로 예상되며, 주로 중국과 인도의 기여에 의해 주도될 것입니다. 심천, 방성, 비샤카파트남을 경유하는 탄탄한 해상 물류가 환태평양 지역으로의 수출을 촉진하고 있습니다. 2025년 3월에 시행된 톤당 200위안(RMB)의 정책적 가격 인상은 이 지역의 가격 결정에 대한 영향력을 입증하고 있습니다. 남미는 5.98%로 가장 높은 성장률을 보였습니다. 브라질의 프리솔트층 투자와 아르헨티나의 셰일가스 개발로 인해 국내 공급량이 제한적인 상황에서 수입 수요가 증가하고 있기 때문입니다.

북미는 수요량의 약 2/3를 수입에 의존하고 있으며, 퍼미안 분지와 헤인즈빌 분지로공급원으로 철도 운송 터미널을 활용하고 있습니다. 유럽은 수입 의존도가 높고, 중금속 함량에 대한 선별 기준이 엄격해짐에 따라 바이어들은 고순도 모로코산과 튀르키예산 광석을 선호하는 경향이 있습니다. 중동 및 아프리카은 초대형 유전과 인접한 이점이 있지만, 대규모 채굴 능력이 부족하여 인도와 중국으로부터의 수입에 의존하고 있습니다. 호주에서는 해양 시추에 대한 전망이 감소하고 지역 내 수요가 억제되고 있지만, 중요 광물에 대한 집중은 지역 한정의 고순도 생산을 촉진할 수 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The Barite market is expected to grow from 9.70 million tons in 2025 to 10.26 million tons in 2026 and is forecast to reach 13.59 million tons by 2031 at 5.78% CAGR over 2026-2031.

Strong purchasing by oilfield service operators, who consume nearly 80% of all mined tonnage, anchors demand, while fresh offshore campaigns in ultra-deepwater and high-pressure wells amplify volume growth. Tight export policies from leading producers, especially China and India, have elevated price discipline and encouraged inventory hedging among drilling contractors. Growth resilience is further supported by rapid gains in medical imaging, coatings, and polymer compounding, niches that absorb premium-grade barium sulfate when crude-linked drilling activity moderates. Ongoing advances in engineered drilling fluids-ranging from micronized high-gravity grades to hybrid water-based systems-are shifting procurement toward value-added specifications that translate into higher realized prices per metric ton. Competitive dynamics, therefore, hinge on access to large, consistent ore bodies and on downstream formulation know-how, with vertically integrated oilfield service majors wielding notable bargaining power over fragmented miners.

Global Barite Market Trends and Insights

Booming Deep-Water and HPHT Drilling in Latin America

Ultra-deepwater projects in Brazil, Mexico, and Guyana now require drilling fluids that can withstand water depths of 2,500 m and bottom-hole temperatures exceeding 200 °C. Each such well consumes more barite than standard onshore programs because a higher mud weight is necessary to control formation pressures. SLB's USD 18-well package for Woodside's Trion field illustrates this intensity and showcases a shift to micronized barite below 10 µm for superior suspension stability. Brazil's pre-salt cluster and Argentina's Vaca Muerta shale simultaneously attract infrastructure capital, expanding regional warehousing and grinding capacity for high-grade ore. Government incentives to localize critical mineral supply chains further reinforce the outlook for demand. Together, these forces contribute to the mid-term growth of Latin America in the global barite market and underpin premium pricing for high-gravity grades.

Rise of Unconventional Hydrocarbons in North America

Shale operators continue to lengthen laterals and densify stage counts, actions that increase per-well weighting-agent consumption even as rig numbers remain flat. Top-tier acreage depletes, prompting activity to shift to Tier 2 locales that exhibit higher pressure windows and therefore require heavier muds. Halliburton's BaraHib and Baker Hughes' PERFORMAX water-based systems demonstrate how operators can replicate the performance of oil-based mud while increasing barite loading by 15-20% to achieve the same density. Despite disciplined capital spending, Q2 2025 completion revenue of USD 1.042 billion at Liberty Energy confirms the scale of ongoing shale work. Supply chains respond by building more rail-served transload terminals in West Texas and the Rockies to shorten lead times, thereby establishing a sustainable baseline demand in the barite market.

Synthetic Hematite Mud Substitutes

Iron-oxide weighting agents such as hematite and ilmenite reach SG values of 4.95-5.10, enabling thinner muds at equivalent densities. Academic work from King Fahd University documented zero sag when 40% barite was replaced with ilmenite in oil-based fluids, while rheology and electrical stability both improved. Service majors have responded with research and development programs aimed at composite weighting blends that hedge against barite scarcity. Cost competitiveness improves where iron-ore processing is local, notably in Canada and Scandinavia, shrinking barite's addressable share in such basins. Environmental regulators also view hematite favorably due to lower heavy-metal leachate, a factor that could accelerate substitution in ecologically sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Stimulus in India's Oilfield Services

- Use of Barite-Polymer Composites in 3-D Printing Filaments

- Volatility in Crude-Linked Drilling Budgets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bedded deposits supplied 74.65% of global tonnage in 2025, reflecting economies of scale and consistent ore quality. The segment's dominance translates into secure long-cycle contracts, notably for Chinese producers in Guizhou and Indian miners in Andhra Pradesh, who together anchor the logistics backbone of the barite market. Residual deposits, although smaller, exhibit the quickest expansion at a 6.03% CAGR, as higher intrinsic grades lower beneficiation costs. Pakistan's Khuzdar vein systems, managed by Bolan Mining Enterprises, illustrate how smaller operations sustain competitiveness by targeting more than 4.30 SG ore for premium applications. Geography, therefore, shapes the risk-return calculus: Asian bedded miners cater to bulk drilling demand, whereas vein and residual sources capture niches in the coatings and medical arenas.

Despite their share supremacy, bedded mines still navigate grade variability that mandates multiple cleaning stages to meet API 13A standards. Capital budgets thus flow to densification circuits, magnetic separation, and optical sorting, lifting fixed-cost leverage. The barite market, hence, rewards operators who marry scale with flexible processing menus that accommodate cross-segment orders. Meanwhile, vein deposits in Morocco and Nevada channel smaller volumes into high-purity end-uses, insulating them from price swings tied to drilling cycles. The coexistence of large-scale bedded operations and specialized vein suppliers enhances supply resiliency and underpins long-term demand coverage.

The Barite Market Report is Segmented by Deposit Type (Bedded, Vein and Cavity Filling, and Residual), End-Use Industry (Oil and Gas, Chemical, Fillers, Medical and Diagnostics, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region captured 41.35% of global tonnage in 2025, driven primarily by the contributions of China and India. Robust seaborne logistics via Shenzhen, Fangcheng, and Visakhapatnam facilitate exports across the Pacific Rim. Policy-driven price hikes of CNY 200 per ton, enacted in March 2025, underscore the region's pricing influence. South America posted the fastest growth at 5.98%, as Brazil's pre-salt investments and Argentina's shale build-out drive up import demand, given the limited indigenous supply.

North America imports roughly two-thirds of its requirement, relying on rail-fed terminals to feed the Permian and Haynesville plays. Europe remains import-dependent and increasingly selective on heavy-metal content, nudging buyers toward high-purity Moroccan and Turkish ore. The Middle East and Africa benefit from proximity to super-giant oil fields but lack sizable mining capacity, prompting the import of inbound cargoes from India and China. Australia's declining offshore drilling outlook tempers regional offtake, yet its focus on critical minerals may catalyze localized high-purity production.

- Andhra Pradesh Mineral Development Corporation (APMDC)

- Ashapura Group

- Baker Hughes Inc.

- Baribright Co. Ltd.

- Bracco

- Cimbar Performance Minerals

- Desku Group Inc.

- Guizhou Saboman Import & Export Co. Ltd.

- Guizhou Tianhong Mining Co.

- Halliburton Energy Services Inc.

- International Earth Products LLC

- Luhua Group

- New Riverside Ochre

- Newpark Resources Inc.

- Pulapathuri

- PVS Global Trade Private Limited

- Sachtleben Minerals GmbH & Co. KG

- Schlumberger Limited

- Shaanxi Fuhua Chemical Co., Ltd.

- The Kish Company Inc.

- Zhongrun Barium Industry Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming deep-water and HPHT drilling in Latin America mainstream

- 4.2.2 Rise of unconventional hydrocarbons in North America mainstream

- 4.2.3 Infrastructure stimulus in India's oilfield services mainstream

- 4.2.4 High-gravity barite grades enabling lower mud volumes under-radar

- 4.2.5 Use of barite-polymer composites in 3-D printing filaments under-radar

- 4.3 Market Restraints

- 4.3.1 Synthetic hematite mud substitutes mainstream

- 4.3.2 Volatility in crude-linked drilling budgets mainstream

- 4.3.3 Radio-opacity regulations curbing filler grades under-radar

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Pricing Overview

- 4.7 Trade Overview

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Deposit Type

- 5.1.1 Bedded

- 5.1.2 Vein and Cavity Filling

- 5.1.3 Residual

- 5.2 By End-use Industry

- 5.2.1 Oil and Gas

- 5.2.2 Chemical (Barium Salts)

- 5.2.3 Fillers (Paints, Plastics, Rubber)

- 5.2.4 Medical and Diagnostics

- 5.2.5 Others (Radiation Shielding, 3-D Printing)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 South Africa

- 5.3.5.6 Nigeria

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Andhra Pradesh Mineral Development Corporation (APMDC)

- 6.4.2 Ashapura Group

- 6.4.3 Baker Hughes Inc.

- 6.4.4 Baribright Co. Ltd.

- 6.4.5 Bracco

- 6.4.6 Cimbar Performance Minerals

- 6.4.7 Desku Group Inc.

- 6.4.8 Guizhou Saboman Import & Export Co. Ltd.

- 6.4.9 Guizhou Tianhong Mining Co.

- 6.4.10 Halliburton Energy Services Inc.

- 6.4.11 International Earth Products LLC

- 6.4.12 Luhua Group

- 6.4.13 New Riverside Ochre

- 6.4.14 Newpark Resources Inc.

- 6.4.15 Pulapathuri

- 6.4.16 PVS Global Trade Private Limited

- 6.4.17 Sachtleben Minerals GmbH & Co. KG

- 6.4.18 Schlumberger Limited

- 6.4.19 Shaanxi Fuhua Chemical Co., Ltd.

- 6.4.20 The Kish Company Inc.

- 6.4.21 Zhongrun Barium Industry Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment