|

시장보고서

상품코드

1940615

초박형 유리 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Ultra-Thin Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

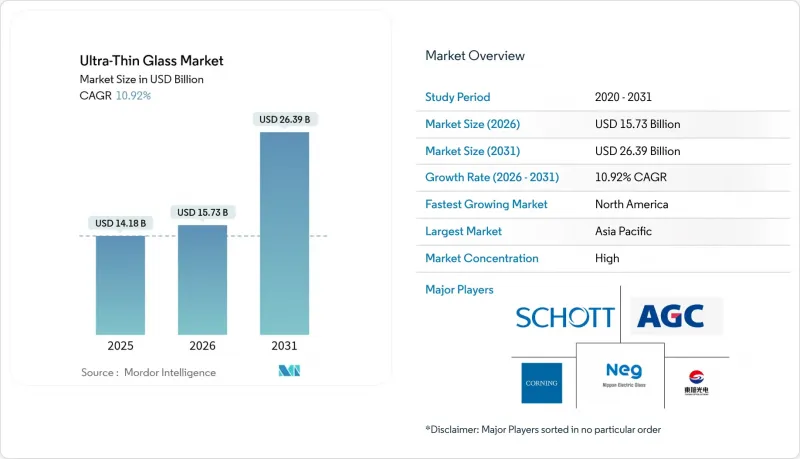

초박형 유리 시장은 2025년에 141억 8,000만 달러로 평가되었으며, 2026년 157억 3,000만 달러에서 2031년까지 263억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 10.92%로 예상됩니다.

접이식 소비자 기기에는 구부릴 수 있는 커버 렌즈가 필요하고, 전기자동차에는 배터리 부하를 줄이기 위해 경량 유리가 요구되며, 칩렛 기반 프로세서에는 점점 더 고밀도화되는 I/O에서 신호 충실도를 유지하기 위한 유리 인터포저가 요구됩니다. 하는 유리 인터포저가 요구됩니다. 1mm 미만의 두께는 마이크로 LED 및 플렉서블 OLED 디스플레이를 위한 새로운 광학 스택의 가능성을 열어줍니다. 한편, 화학적 강화 패널은 프리미엄 스마트폰의 낙하 방지 및 스크래치 방지 기능을 향상시킵니다. 반도체 업체들의 유리 기판에 대한 설비 투자 증가와 자동차 제조업체들의 파노라마 헤드업 디스플레이로의 전환이 맞물리면서 세 가지 고부가가치 가치사슬 전반에 걸쳐 잠재적 수요가 증가하고 있습니다. 원료의 순도 요구 사항과 정밀 성형은 여전히 비용 구조를 높이고 있지만, 연속 플로트 방식과 용융 인발 라인의 지속적인 업그레이드로 인해 기존 판유리와의 가격 차이가 줄어들고 있습니다.

세계 초박형 유리 시장 동향과 전망

가전제품 수요 확대

스마트폰, 태블릿, 웨어러블 기기의 출하량 급증으로 초박형 유리 시장은 여전히 소비자 전자기기에 크게 의존하고 있습니다. 삼성 갤럭시 Z 폴드6는 100µ&m 미만의 화학 강화유리를 채택하여 수십만 번의 굽힘을 견디면서 광학적인 투명도를 유지합니다. 코닝의 Gorilla Glass Ceramic 2는 투명성을 유지하면서 경도를 높이는 나노결정체를 통합했습니다. 디바이스 제조사들은 또한 5G의 처리량을 극대화하기 위해 얇은 유리 안테나 창을 내장하여 부품 간의 상호 수요를 강화하고 있습니다. 베트남과 인도에서의 공급망 현지화는 배송 속도를 더욱 향상시키고, 패널 제조업체와 유리 공급업체 간의 협력을 더욱 긴밀하게 하고 있습니다. 이러한 요인들이 복합적으로 작용하여 유닛 성장 둔화에도 불구하고 대당 평균 유리 면적을 증가시켜 초박형 유리 시장의 다년간 안정적인 수익 기반을 공고히 하고 있습니다.

접이식 스마트폰과 노트북의 급속한 보급에 따른 빠른 확산

유연한 형태는 면적 증가를 견인합니다. 접이식 디스플레이 한 대당 유리 사용 면적이 기존 스마트폰의 2-3배에 달하기 때문입니다. SCHOTT의 초박형 유리는 30µm 두께를 실현하여 반경 1mm에서 30만회 이상의 굽힘 테스트를 견디는 업계 최고 기록을 달성했습니다. 노트북 제조업체들은 현재 17인치 접이식 모델을 13인치 크기로 접을 수 있는 프로토타입을 개발하여 기기당 기판 수요를 증가시키고 있습니다. 공동 개발한 방폭 코팅은 표면 응력을 분산시켜 조립업체가 폴리이미드 필름에서 더 단단한 유리 표면 재료로 전환할 수 있도록 도와줍니다. 가격 차이가 줄어들면서 2027년까지 폴더블 단말기의 보급률은 플래그십 모델 출하량 기준 두 자릿수 점유율을 기록할 것으로 예상되며, 초박형 유리 시장에 강력한 물량적 추동력을 제공할 것으로 전망됩니다.

고순도 원료와 정밀 가공의 고비용

반도체 등급의 모래는 99.999%의 순도를 달성해야 합니다. 노스캐롤라이나 주 스프루스파인 광상은 몇 안되는 공급원 중 하나이며, 공급업체 가격표에 따르면 톤당 1만 달러에 거래되고 있습니다. 용융 인발로에는 백금 로듐 채널과 초청정 대기가 필요하며, 10세대 디스플레이 크기의 라인 당 자본 집약도는 3억 5,000만 달러에 달합니다. 소규모 신규 진입 기업들은 이러한 지출을 상각하는 데 어려움을 겪고 있으며, 이는 생산능력의 보급을 늦추고 단기 계획 주기의 초박형 유리 시장의 성장률을 억제하는 요인으로 작용하고 있습니다.

부문 분석

소다석회 조성물은 규모와 성장을 가져왔으며, 2025년에는 45.52%의 점유율을 차지하며 11.55%의 CAGR 전망을 유지합니다. 녹는점이 알루미노실리케이트에 비해 낮아 용광로의 에너지 소비를 최대 15%까지 줄일 수 있어 탈탄소화 약속에 부합합니다. NSG의 UFF 플로트 유리는 35% 칼렛을 통합하면서도 AMOLED 커버 렌즈의 광학 평탄도를 충족합니다. 코닝의 고릴라 글래스 등 알루미노실리케이트 신제품은 800 비커스 경도에 이르며, 하이엔드 휴대폰과 자동차 내장재에 사용되고 있습니다. 붕규산 및 무알칼리 변종은 우수한 내열충격성으로 반도체의 유전체를 지지하고 있습니다.

프리미엄 부문은 평균 판매 가격을 높이고, 소다석회의 견고한 생산 기반은 대량 생산 휴대폰 모델에 비용 우위를 가져와 초박형 유리 시장의 기반이 될 수 있도록 보장합니다. 제조업체는 내구성의 격차를 메우기 위해 소다석회 시트에 이온 교환 처리를 하고 있습니다. 한편, 특수 리튬 알루미노실리케이트 등급은 웨이퍼 레벨의 광학 및 AR 도파관 용도에 대응하고 있습니다.

플로트 및 마이크로 플로트 라인은 2025년 매출의 50.12%를 차지하며 12.24%의 가장 높은 CAGR을 달성할 것으로 예상됩니다. 이는 현대의 주석 욕조가 0.4mm 두께, 표면 파형도 0.1µm 미만의 리본을 생산할 수 있게 되었기 때문입니다. 필킨톤의 최신 플랜트에서는 역류식 질소 커튼을 채택하여 주석의 부착을 억제하여 광학급에 가까운 표면을 실현하고 있습니다. 코닝이 선도적으로 개발한 용융 인발법은 연삭이나 연마가 필요 없는 무결점 표면을 구현하여 고해상도 디스플레이에 필수적인 기술입니다. 다운 인발 기술은 30µm 두께 제어가 가능하며, 접이식 커버글라스 라인에 대응. 한편, 롤투롤 슬릿 인발은 웨어러블 센서를 위한 연속적인 플렉서블 유리 웹을 생성합니다.

플로트 방식의 손익분기점 생산량은 여전히 가장 낮은 수준이며, 초박형 유리 시장 신규 진입자의 진입 경로로서 입지를 확고히 하고 있습니다. 그러나 퓨전 방식의 무결점 표면은 점점 더 높은 가격대를 요구하고 있으며, 공급업체는 하이브리드 운영을 통해 응용 분야 간 위험을 분산시켜야 하는 상황에 처해 있습니다.

지역별 분석

아시아태평양은 중국, 한국, 일본의 고도로 통합된 디스플레이 및 반도체 생태계로 인해 2025년 매출의 49.08%를 차지했습니다. 삼성디스플레이의 Gen-8.6 OLED 공장 및 TSMC의 첨단 패키징 라인 등의 확장 계획이 플로트 및 퓨전 기판에 대한 안정적인 수요를 뒷받침하고 있습니다. 일본 기업은 증강현실 광학용 특수 유리를 추가하고, 대만 조립업체는 파일럿 생산을 통해 유리관통기술(TG)의 양산을 추진하고 있습니다. 그러나 지정학적 무역 규제가 강화되는 가운데 지역 분산 필요성이 대두되면서 한국과 일본의 공급업체들은 물류 리스크를 줄이기 위해 동남아시아 지역에 라인 공동투자를 진행하고 있습니다.

북미는 반도체 회귀와 전기자동차용 유리 채용으로 인해 2031년까지 CAGR 11.32%로 가장 높은 성장률을 보일 것으로 예상됩니다. 인텔의 애리조나 주 유리기판 캠퍼스는 2026년 양산을 목표로 이미 특수 용융 설비를 도입했습니다. 코닝의 2025년 1분기 실적은 AI용 데이터센터 광학 부품의 특수 소재가 주도하여 핵심 매출이 13% 증가한 37억 달러로 집계됐습니다. 또한, 미국 중서부 주정부의 보조금으로 오하이오 주에 설립된 '유리기술연구센터'에서는 순환형 재활용 시험을 지원하고 있으며, 초박판유리 시장의 폐기물 병목현상 해소를 위한 첫걸음을 내딛고 있습니다.

유럽은 기술력은 높지만 성장 속도는 완만한 지역입니다. AGC유리 유럽은 0.3mm 판유리를 활용한 진공 단열유리 라인에 투자하여 창호의 열관류율(U값)을 0.5W/m2K 이하로 낮추고 있습니다. 가디언과 벨룩스는 넷제로 건축용 강화 진공 단열 유리판을 공동 개발하여 정책 주도형 수요를 뒷받침하고 있습니다. 독일과 핀란드의 자동차 유리 전문 제조업체는 프리미엄 EV 플랫폼용 파노라마 루프를 공급하며 균형 잡힌 성장 궤도를 유지하면서 규제 당국과 구매자 모두에게 공감을 불러일으키는 지속가능성에 대한 신뢰성을 확립하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The Ultra-Thin Glass Market was valued at USD 14.18 billion in 2025 and estimated to grow from USD 15.73 billion in 2026 to reach USD 26.39 billion by 2031, at a CAGR of 10.92% during the forecast period (2026-2031).

Multiple technology transitions propel this expansion: foldable consumer devices need bendable cover lenses, electric vehicles specify lightweight glazing that trims battery load, and chiplet-based processors require glass interposers that preserve signal fidelity at ever-higher I/O densities. Thinness below 1 millimeter also unlocks new optical stacks for micro-LED and flexible OLED displays, while chemical-strengthened panels extend drop and scratch resistance in premium handsets. Rising capital outlays by semiconductor leaders for glass substrates, combined with automakers' shift toward panoramic head-up displays, broaden addressable demand across three high-value supply chains. Raw-material purity requirements and precision forming still elevate cost structures, yet continuous float and fusion draw line upgrades are narrowing the delta with conventional sheet glass.

Global Ultra-Thin Glass Market Trends and Insights

Growing Demand from Consumer Electronics

Surging smartphone, tablet, and wearable volumes keep the ultra-thin glass market firmly anchored to consumer electronics. Samsung's Galaxy Z Fold6 employs sub-100 µm chemically strengthened glass that bends hundreds of thousands of times while retaining optical clarity. Corning's Gorilla Glass Ceramic 2 integrates nanocrystals for higher hardness without compromising transparency. Device makers also embed thin-glass antenna windows to maximise 5G throughput, reinforcing cross-component pull. Supply-chain localisation within Vietnam and India further raises shipment velocity, tightening collaboration between panel makers and glass suppliers. These factors collectively push average glass area per handset upward even as unit growth moderates, cementing a stable multi-year revenue foundation for the ultra-thin glass market.

Rapid Adoption in Foldable Smartphones & Notebooks

Flexible form factors drive incremental square metres because each foldable display uses two to three times the glass area of a bar-type phone. SCHOTT's ultra-thin glass reached 30 µm thickness while withstanding over 300,000 bends at 1 mm radius, an industry record. Notebook makers now prototype 17-inch fold-outs that collapse into 13-inch footprints, multiplying substrate demand per device. Co-developed anti-shatter coatings distribute surface stress, letting assemblers trade polyimide films for harder glass facings. With price premiums narrowing, foldable penetration is expected to hit double-digit share of flagship shipments by 2027, embedding strong volume tailwinds within the ultra-thin glass market.

High Cost of High-Purity Raw Materials & Precision Processing

Semiconductor-grade sand must achieve 99.999% purity; deposits in Spruce Pine, North Carolina are one of the few sources and regularly command USD 10,000 per ton according to supplier price lists. Fusion draw furnaces require platinum-rhodium channels and ultra-clean atmospheres, inflating capital intensity to USD 350 million per line for Gen-10 display sizes. Smaller entrants struggle to amortise such outlays, slowing capacity diffusion and tempering the ultra-thin glass market growth rate in near-term planning cycles.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Flexible OLED & Micro-LED Display Lines

- Weight-Reduction Needs in Automotive Glazing & HUDs

- Brittleness & Yield Loss During Large-Area Handling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soda-lime compositions delivered scale and growth, posting a 45.52% share in 2025 while maintaining a 11.55% CAGR outlook. Their lower melting temperatures cut furnace energy by up to 15% versus aluminosilicate, aligning with decarbonisation pledges. NSG's UFF float glass now integrates 35% cullet yet meets optical flatness for AMOLED cover lenses. Aluminosilicate entrants like Corning's Gorilla Glass reach 800 Vickers hardness, serving premium phones and automotive interiors. Borosilicate and alkali-free variants underpin semiconductor dielectrics owing to superior thermal shock resistance.

Premium segments lift average selling prices, but soda-lime's entrenched production base provides cost leverage for mass handset models, ensuring it remains the anchor of the ultra-thin glass market. Manufacturers layer ion-exchange treatments on soda-lime sheets to bridge durability gaps, while specialized lithium-aluminosilicate grades address wafer-level optics and AR waveguide applications.

Float and microfloat lines generated 50.12% of 2025 revenue and enjoy the highest 12.24% CAGR because modern tin baths now output ribbons as thin as 0.4 mm with surface waviness under 0.1 µm. Pilkington's latest plant leverages counter-current nitrogen curtains to suppress tin pick-up, delivering near-optical-grade surfaces. Pioneered by Corning, fusion draw methods yield defect-free surfaces without grinding or polishing, crucial for high-resolution displays. Down-draw techniques allow 30 µm thickness control, servicing foldable cover glass lines, while roll-to-roll slit draw opens continuous flexible glass webs for wearable sensors.

Break-even throughput for float remains the lowest, cementing its status as the entry route for new participants in the ultra-thin glass market. Yet fusion's pristine surfaces increasingly command premium price tiers, pushing suppliers to run hybrid operations and diversify risk across application buckets.

The Ultra-Thin Glass Market Report Segments the Industry by Glass Type (Aluminosilicate, Soda-Lime Ultra-Thin, and More), Manufacturing Process (Fusion Draw, Down-Draw / Overflow, and More), Application (Semiconductor Substrate, Touch Panel Displays, and More), End-User Industry (Automotive, Biotechnology, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 49.08% of 2025 revenue thanks to densely integrated display and semiconductor ecosystems in China, South Korea, and Japan. Expansion programs such as Samsung Display's Gen-8.6 OLED fab and TSMC's advanced packaging lines provide stable pull for float and fusion substrates. Japanese firms add specialised glass for augmented-reality optics, while Taiwanese assemblers ramp through-glass via pilot runs. Regional diversification, though, gains urgency as geopolitical trade rules tighten, prompting Korean and Japanese suppliers to co-invest in lines within Southeast Asia to derisk logistics.

North America is projected to register the fastest 11.32% CAGR through 2031 due to semiconductor reshoring and electric-vehicle glass adoption. Intel's Arizona glass substrate campus targets risk production in 2026 and has already procured specialised fusion equipment. Corning's 2025 first-quarter results showed 13% core sales growth to USD 3.7 billion, buoyed by specialty materials for generative-AI data-centre optics. Midwest state incentives also fund a Glass Centre of Excellence in Ohio that supports circular recycling trials, an early step toward easing waste bottlenecks for the ultra-thin glass market.

Europe remains a technology-rich yet moderately paced terrain. AGC Glass Europe invests in vacuum-insulated glass lines that leverage 0.3 mm panes to hit <0.5 W/m2K window U-factors. Guardian and VELUX co-develop tempered VIG panes for net-zero buildings, underscoring policy-driven demand. Automotive glazing specialists in Germany and Finland supply panoramic roofs for premium EV platforms, sustaining a balanced growth path and embedding sustainability credentials that resonate with regulators and buyers alike.

- AGC Inc.

- Central Glass Co., Ltd.

- Changzhou Almaden Co., Ltd.

- Corning Incorporated

- CSG Holding Co., Ltd.

- Emerge Glass

- Fraunhofer

- Irico Group New Energy Company Limited

- Nippon Electric Glass Co., Ltd.

- Nippon Sheet Glass Co., Ltd.

- Nitto Denko Corporation.

- OFILM

- Samsung

- SCHOTT AG

- Taiwan Glass Ind. Corp.

- Tunghsu Optoelectronic Technology

- Xinyi Glass Holdings Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from consumer electronics

- 4.2.2 Rapid adoption in foldable smartphones & notebooks

- 4.2.3 Advancements in flexible OLED & micro-LED display lines

- 4.2.4 Weight-reduction needs in automotive glazing & HUDs

- 4.2.5 Glass interposers for chiplet packaging

- 4.3 Market Restraints

- 4.3.1 High cost of high-purity raw materials & precision processing

- 4.3.2 Brittleness & yield loss during large-area handling

- 4.3.3 Limited recycling streams for greater than 0.3 mm glass waste

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Glass Type

- 5.1.1 Aluminosilicate (e.g., Gorilla, Dragontrail)

- 5.1.2 Borosilicate / Alkali-Free

- 5.1.3 Soda-Lime Ultra-Thin

- 5.1.4 Others (Lithium-Aluminosilicate, etc.)

- 5.2 By Manufacturing Process

- 5.2.1 Fusion Draw

- 5.2.2 Down-Draw / Overflow

- 5.2.3 Float & Microfloat

- 5.2.4 Slit Draw / Roll-to-Roll

- 5.3 By Application

- 5.3.1 Semiconductor Substrate

- 5.3.2 Touch Panel Displays

- 5.3.3 Fingerprint Sensors

- 5.3.4 Automotive Glazing

- 5.3.5 Other Applications (Automotive Displays and Glazing, etc.)

- 5.4 By End-User Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive

- 5.4.3 Biotechnology

- 5.4.4 Other End-User Industries (Energy and Power, etc.)

- 5.5 By Region

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 Central Glass Co., Ltd.

- 6.4.3 Changzhou Almaden Co., Ltd.

- 6.4.4 Corning Incorporated

- 6.4.5 CSG Holding Co., Ltd.

- 6.4.6 Emerge Glass

- 6.4.7 Fraunhofer

- 6.4.8 Irico Group New Energy Company Limited

- 6.4.9 Nippon Electric Glass Co., Ltd.

- 6.4.10 Nippon Sheet Glass Co., Ltd.

- 6.4.11 Nitto Denko Corporation.

- 6.4.12 OFILM

- 6.4.13 Samsung

- 6.4.14 SCHOTT AG

- 6.4.15 Taiwan Glass Ind. Corp.

- 6.4.16 Tunghsu Optoelectronic Technology

- 6.4.17 Xinyi Glass Holdings Limited.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Development of Advanced Glass for Solar Energy Projects