|

시장보고서

상품코드

1940621

협동 로봇 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Collaborative Robot - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

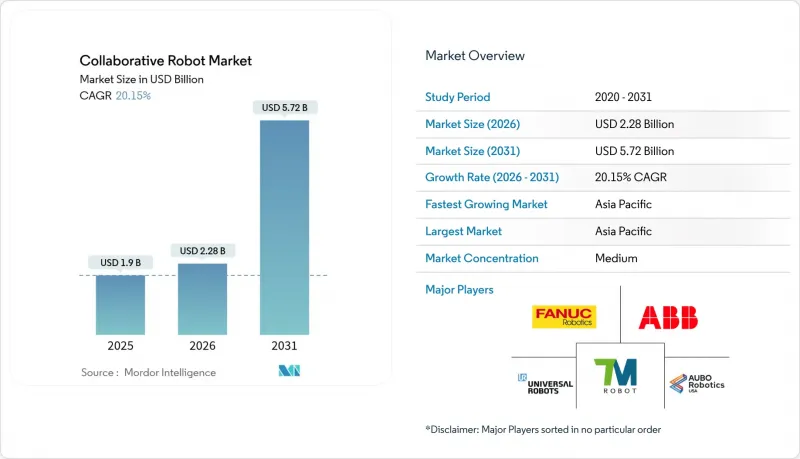

협동 로봇 시장은 2025년에 19억 달러로 평가되었으며, 2026년 22억 8,000만 달러에서 2031년까지 57억 2,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 20.15%로 예상됩니다.

업데이트된 ISO/TS 15066 표준에 따른 안전 요건 명확화, 세제 혜택으로 인한 투자 회수 기간 단축, 노동력 부족으로 인한 유연한 자동화의 시급성 증가로 인해 수요가 가속화되고 있습니다. 제조업체들은 작업자 대체가 아닌 생산성 향상을 위해 협동 로봇을 도입하는 추세이며, 소프트웨어의 성숙과 프로그래밍의 간소화로 도입 주기가 단축되고 있습니다. 적재 능력 향상, 창고 자동화 요구, 서비스 분야에서의 사용 사례 확대로 인해 전 세계 밸류체인 전반에 걸쳐 도입 모멘텀이 강화되고 있습니다.

세계 협동 로봇 시장 동향 및 인사이트

다품종 소량 생산에서 비용 효율적인 재배치 가능

유럽과 북미 공장에서는 현재 코봇을 같은 교대 근무 시간 내에 조립 셀 간 로테이션으로 운영하여 전환 시간을 몇 주에서 몇 시간으로 단축하고 있습니다. 이러한 민첩성을 통해 자동차 부품 공급업체는 자동화의 이점을 유지하면서 소규모의 고수익성 주문을 받아들일 수 있게 되었습니다.

중소기업용 플러그 앤 플레이형 협동 로봇에 대한 OEM 추진

새로운 컨트롤러, 캡이 달린 배선, 사전 로드된 작업 라이브러리를 통해 중소 제조업체는 전문 통합업체 없이도 협동 로봇을 도입할 수 있습니다. 유니버설로봇의 UR 시리즈 리뉴얼은 사이클 타임 단축과 직관적인 핸드 가이딩을 통해 총소유비용을 절감하고, 수천 명의 첫 사용자들에게 협동 로봇 시장을 열어주었습니다.

기존 PLC 아키텍처의 통합 병목 현상

레거시 PLC는 실시간 이더넷이나 안전 작동 채널이 부족한 경우가 많으며, 수십 년 된 라인에 협동 로봇을 추가할 때 고가의 컨트롤러 업그레이드를 해야 하는 경우가 많습니다. 이 비용 부담으로 인해 일부 자동차 공장에서는 전체 라인의 개보수까지 도입을 미루는 사례도 볼 수 있습니다.

부문 분석

2025년 기준 5kg 미만 모델이 협동 로봇 시장의 52.40%를 차지했습니다. 이는 정밀도가 최우선시되는 전자기기 및 의료기기 조립 분야가 주요 원인입니다. 한편, 10-20kg 구간은 22.95%의 CAGR로 확대되고 있으며, 팔레타이징, 기계 관리, 자동차 서브어셈블리 분야에서 관심이 높아지고 있습니다. 중간 중량급은 작업 범위가 확대되어 작업자가 새로운 안전 구역으로 이동하지 않고도 라인 사이드 작업을 할 수 있습니다. 중량급(20kg 이상) 협동 로봇은 틈새시장이지만 방폭 인증이 필수인 도장 및 화학 환경에서 가치를 발휘하고 있습니다. 로봇 제조사들이 동적 토크 감지 기술을 고도화하면서 2028년 이후 중중량급 협동 로봇 시장 규모는 경량급보다 더 크게 성장할 것으로 예상됩니다.

5-9kg급에서는 각 벤더들이 1초 미만의 픽앤플레이스 사이클을 실현하는 비전과 AI를 패키징하여 반도체 후공정 업무에 대응하고 있습니다. 이러한 변화는 손재주와 강도를 겸비하고 장비의 복잡성을 줄이는 유닛을 원하는 구매자의 요구를 반영하고 있습니다. 협동 로봇 시장을 활용하는 제조업체는 페이로드 클래스 간 그리퍼 및 컨트롤러의 표준화를 통해 예비 부품 관리 및 작업자 교육을 간소화할 수 있습니다.

2025년 기준 하드웨어가 매출의 71.35%를 차지했지만, 사용자들이 기계적인 성능보다 지능화를 중시하는 추세에 따라 소프트웨어 분야는 연간 27.15%의 성장률로 확대되고 있습니다. 비전 가이드를 통한 경로 계획, 차량 오케스트레이션, 예지보전 모듈은 일회성 하드웨어 판매를 지속적인 라이선스 수익으로 전환하여 벤더의 수익원을 디지털 서비스로 전환하고 있습니다. 협동 로봇은 현재 ROS 호환 API와 클라우드 커넥터가 표준으로 장착되어 있어 애플리케이션을 빠르게 통합할 수 있습니다.

컨설팅 및 라이프사이클 서비스의 성장은 중소기업이 외부 전문 지식에 의존하는 것을 반영합니다. 벤더들은 안전 평가, 프로그래밍, 작업자 기술 향상을 구독 모델에 포함시켜 협동 로봇 시장을 더욱 확장하고 있습니다. 향후 소프트웨어 정의 페이로드 업그레이드를 통해 교체 주기를 단축하고, 플랜트 관리자는 프레임의 수명을 늘리면서 펌웨어 강화로 성능을 향상시킬 수 있게 될 것입니다.

협동 로봇 시장 보고서는 페이로드(5kg 미만, 5-9kg, 10-20kg, 20kg 이상), 구성요소(하드웨어 등), 용도별(자재 취급, 픽앤플레이스 등), 최종사용자 산업별(전자기기, 자동차 등), 프로그래밍 방법별(핸드 가이딩 등), 지역별로 분류되어 있습니다. 핸드 가이딩 등), 지역별로 분류되어 있습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

지역별 분석

아시아 지역은 2025년 매출의 40.55%를 차지하며, 중국의 14차 5개년 계획에 따른 1조 위안 규모의 로봇 산업 진흥책과 AI, IoT, 차세대 자동화를 융합한 일본의 'Society 5.0' 구상이 주도하고 있습니다. 중국의 전자기기 및 배터리 공장에서는 정밀접착 및 셀 적층용 협동 로봇을 도입하고, 일본 병원에서는 노인 간병용 서비스 로봇의 실증 실험이 진행되고 있습니다. 국내에서는 '제4차 지능형 로봇 기본계획'을 통해 국내 중소기업이 협동 로봇 솔루션을 도입할 수 있는 자금이 지원되어 공급망 강화가 진행되고 있습니다.

북미는 2위입니다. 미국의 리쇼어링 혜택과 기록적인 노동력 부족이 시장을 부추기고 있습니다. CHIPS 법의 지원을 받은 반도체 공장에서는 웨이퍼 이송에 듀얼 암 협동 로봇을 도입하여 운송 시 오염 위험을 줄이고 있습니다. 캐나다의 자동차 부품 공급업체는 다이캐스팅 부품 마무리에 중하중 장치를 도입하고, 멕시코의 마킬라도라는 임금 상승과 수출 경쟁력의 균형을 맞추기 위해 협동 로봇을 도입했습니다. 국경을 초월한 표준화를 통해 통합업체는 셀 설계를 재사용할 수 있으며, 도입이 가속화되고 있습니다.

유럽에서는 독일의 인더스트리 4.0 등대 프로젝트가 견인차 역할을 하면서 MES 데이터와 협동 로봇군을 연계하는 도입이 활발하게 진행되고 있습니다. 호라이즌 유럽 보조금은 인간과 기계의 인터페이스 연구를 지원하고, 덴마크와 이탈리아에서는 AI 동작 계획 스택을 개발하는 스타트업이 활발히 활동하고 있습니다. 프랑스 항공우주 공장은 경량화와 인체공학적 이점을 이유로 탄소섬유 트리밍에 협동 로봇을 선택했습니다. 에너지 비용의 상승으로 공장은 보다 효율적인 레이아웃을 모색하고 있으며, 코봇은 울타리가 있는 로봇에 비해 설치 면적을 줄일 수 있습니다. 환경 규제 역시 유압 프레스기에 비해 코봇의 대기 전력 소비가 적은 점을 높이 평가하고 있으며, 지속가능성을 중시하는 지역에서의 협동 로봇 시장 확대에 기여하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The Collaborative Robot Market was valued at USD 1.9 billion in 2025 and estimated to grow from USD 2.28 billion in 2026 to reach USD 5.72 billion by 2031, at a CAGR of 20.15% during the forecast period (2026-2031).

Demand accelerates as updated ISO/TS 15066 standards clarify safety requirements, tax incentives lower payback periods, and labor shortages raise the urgency of flexible automation. Manufacturers increasingly deploy cobots to lift productivity rather than replace workers, while maturing software and simplified programming shorten deployment cycles. Growing payload capacities, warehouse automation needs, and widening service-sector use cases strengthen adoption momentum across global value chains.

Global Collaborative Robot Market Trends and Insights

Cost-effective Redeployment in High-mix Manufacturing

European and North American factories now rotate cobots across assembly cells within a single shift, cutting changeover from weeks to hours This agility lets automotive suppliers accept smaller, high-margin orders while retaining automation gains.

OEM Push Toward Plug-and-Play Cobots for SMEs

New controllers, capped wiring, and pre-loaded task libraries allow small manufacturers to install cobots without specialist integrators. Universal Robots' UR-series refresh shows how cycle-time gains and intuitive hand-guiding shrink total cost of ownership, opening the collaborative robot market to thousands of first-time users

Integration Bottlenecks with Brownfield PLC Architectures

Legacy PLCs often lack real-time Ethernet or safe-motion channels, forcing costly controller upgrades when cobots are added to decades-old lines . The expense pushes some automotive plants to defer adoption until full line overhauls.

Other drivers and restraints analyzed in the detailed report include:

- Rapid E-commerce Fulfilment Drives Warehouse Cobots

- ISO/TS 15066 Updates Easing Liability Concerns

- Payload-Speed Trade-offs Limiting Heavy-duty Tasks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sub-5 kg models controlled 52.40% of the collaborative robot market in 2025, largely in electronics and medical device assembly where precision is paramount. The 10-20 kg band, however, is pacing a 22.95% CAGR, signaling rising interest in palletizing, machine tending, and automotive sub-assembly. Mid-range units also integrate longer reaches, enabling line-side work without moving humans to new safety zones. Heavy-duty (>20 kg) cobots remain niche but prove valuable in paint and chemical environments where explosion-proof certification is essential. As robot makers refine dynamic torque sensing, the collaborative robot market size for mid-payloads is projected to outgrow light units after 2028.

Within 5-9 kg, vendors package vision and AI for pick-and-place cycles under one second, catering to semiconductor back-end operations. The shift reflects buyers' search for units that bridge dexterity and strength, reducing fleet complexity. Manufacturers leveraging the collaborative robot market gain the option to standardize grippers and controllers across payload classes, simplifying spare-parts management and operator training.

Hardware generated 71.35% of revenue in 2025, yet software is advancing 27.15% annually as users emphasize intelligence over mechanics. Vision-guided path planning, fleet orchestration, and predictive maintenance modules convert one-time hardware sales into recurring licenses, moving vendor profit pools toward digital services. Cobots now ship with ROS-compatible APIs and cloud connectors, allowing quick app integrations.

Growth in consulting and lifecycle services reflects SME reliance on external expertise. Vendors bundle safety assessment, programming, and operator up-skilling into subscription models, further enlarging the collaborative robot market. Over time, software-defined payload upgrades may lower replacement cycles, letting plant managers keep frames in service longer while lifting performance through firmware enhancements.

Collaborative Robots Market Report is Segmented Into by Payload (Less Than 5Kg, 5-9 Kg, 10-20 Kg, More Than 20 KG), Component (Hardware and More), Application (Material Handling, Pick and Place and More), End-User Industry (Electronics, Automotive, and More), Programming Method (Hand-Guiding and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia generated 40.55% of 2025 revenue, propelled by China's 1-trillion-yuan robotics push under the 14th Five-Year Plan and Japan's Society 5.0 roadmap that blends AI, IoT, and next-generation automation . Chinese electronics and battery plants install cobots for precision gluing and cell stacking, while Japanese hospitals test service robots for elder care. South Korea's Fourth Intelligent Robot Basic Plan funds local SMEs to adopt collaborative solutions, reinforcing domestic supply chains.

North America ranks second. U.S. reshoring incentives combined with record labor scarcity elevate the market. Semiconductor fabs subsidized by the CHIPS Act integrate dual-arm cobots for wafer loading, shrinking transport contamination risk. Canadian auto parts suppliers adopt mid-payload units for die-casting part finishing, while Mexican maquiladoras deploy cobots to balance wage inflation with export competitiveness. Cross-border standardization allows integrators to reuse cell designs, accelerating rollout.

Europe shows robust uptake led by Germany's Industrie 4.0 lighthouse projects linking MES data to cobot fleets. Horizon Europe grants finance human-machine interface research, spurring startups in Denmark and Italy that build AI motion-planning stacks. French aerospace plants choose cobots for carbon-fiber trimming, citing weight reduction and ergonomic gains. Rising energy costs push factories toward leaner layouts where cobots save floor space relative to fenced robots. Environmental regulations also favor cobots' lower idle power draw compared with hydraulic presses, aiding the collaborative robot market size in sustainability-conscious regions.

- Universal Robots AS

- FANUC Corp.

- ABB Ltd.

- KUKA AG

- Yaskawa Electric Corp.

- Techman Robot Inc.

- Doosan Robotics Inc.

- AUBO Robotics

- Kawasaki Heavy Industries Ltd.

- Omron Corporation

- Epson Robots

- Precise Automation Inc.

- Staubli International AG

- Hanwha Robotics

- Denso Wave Inc.

- Comau SpA

- Hyundai Robotics

- Festo SE and Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-effective Re-deployment in High-mix Manufacturing (Europe)

- 4.2.2 OEM Push Toward Plug-and-Play Cobots for SMEs (North America)

- 4.2.3 Rapid E-Commerce Fulfilment Drives Warehouse Cobots (Asia)

- 4.2.4 ISO/TS 15066 Updates Easing Liability Concerns (Global)

- 4.2.5 Tax Incentives for Reshoring Automation (United States)

- 4.3 Market Restraints

- 4.3.1 Integration Bottlenecks with Brownfield PLC Architectures

- 4.3.2 Payload-Speed Trade-offs Limiting Heavy-duty Tasks

- 4.3.3 Fragmented Component Ecosystem Inflates TCO for SMEs

- 4.3.4 Insurance Underwriting Gaps for HumanRobot Workcells

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porters Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Intensity of Competitive Rivalry

- 4.6.5 Threat of Substitute Products

- 4.7 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Payload

- 5.1.1 Less than 5 kg

- 5.1.2 5 - 9 kg

- 5.1.3 10 - 20 kg

- 5.1.4 More than 20 kg

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.2.3.1 Consulting and Integration

- 5.2.3.2 Maintenance and Training

- 5.3 By Application

- 5.3.1 Material Handling

- 5.3.2 Pick and Place

- 5.3.3 Assembly

- 5.3.4 Palletizing and De-palletizing

- 5.3.5 Welding and Soldering

- 5.3.6 Quality Testing and Inspection

- 5.3.7 Packaging

- 5.3.8 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Electronics and Semiconductors

- 5.4.3 General Manufacturing

- 5.4.4 Food and Beverage

- 5.4.5 Chemicals and Pharmaceuticals

- 5.4.6 Logistics and E-commerce

- 5.4.7 Healthcare and Life Sciences

- 5.4.8 Metals and Machining

- 5.4.9 Other Industries

- 5.5 By Programming Method (qualitative only)

- 5.5.1 Hand-Guiding / Direct Teaching

- 5.5.2 Lead-through Teaching

- 5.5.3 Offline Programming and Simulation

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Nordics

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Universal Robots AS

- 6.4.2 FANUC Corp.

- 6.4.3 ABB Ltd.

- 6.4.4 KUKA AG

- 6.4.5 Yaskawa Electric Corp.

- 6.4.6 Techman Robot Inc.

- 6.4.7 Doosan Robotics Inc.

- 6.4.8 AUBO Robotics

- 6.4.9 Kawasaki Heavy Industries Ltd.

- 6.4.10 Omron Corporation

- 6.4.11 Epson Robots

- 6.4.12 Precise Automation Inc.

- 6.4.13 Staubli International AG

- 6.4.14 Hanwha Robotics

- 6.4.15 Denso Wave Inc.

- 6.4.16 Comau SpA

- 6.4.17 Hyundai Robotics

- 6.4.18 Festo SE and Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment