|

시장보고서

상품코드

1940630

알루미늄 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Aluminum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

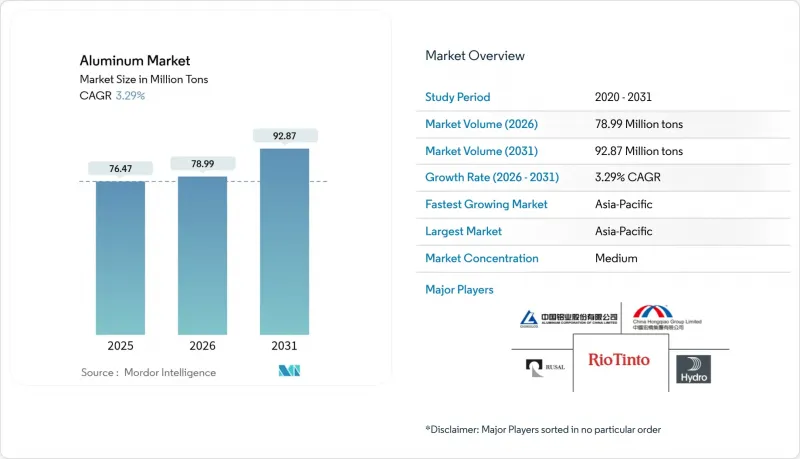

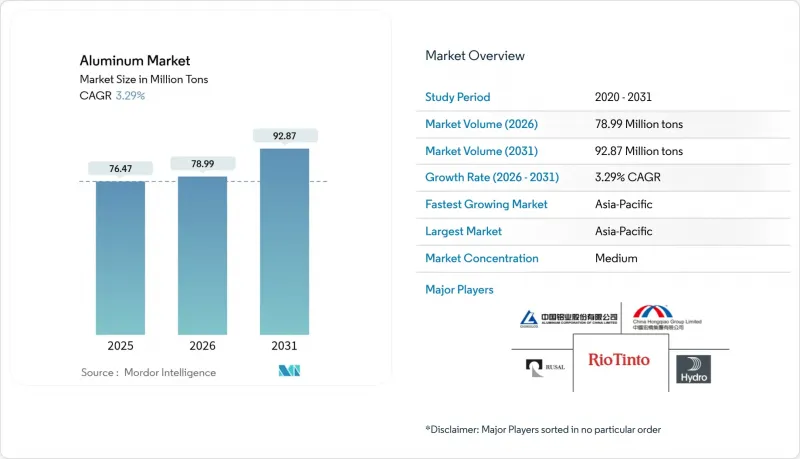

알루미늄 시장은 2025년 7,647만 톤에서 2026년에는 7,899만 톤으로 성장하여 2026년부터 2031년까지 CAGR 3.29%를 기록하며 2031년까지 9,287만 톤에 달할 것으로 예측됩니다.

이러한 견고한 성장은 알루미늄이 세계에서 두 번째로 많이 사용되는 금속이라는 점, 비교할 수 없는 강도 대 중량 비율, 그리고 지금까지 생산된 금속의 75%를 순환시키는 폐쇄형 재활용 특성으로 인해 가능했습니다. 급속한 전기화, 재생에너지 확대, 지속가능한 포장 의무화로 인해 수요가 증가하는 반면, 생산자들은 탈탄소화 목표, 변동하는 전력 가격, 무역 정책의 변화에 직면해 있습니다. 주요 기업들은 그린 제련과 스크랩 회수에 자본을 집중하는 한편, 다운스트림 고객들은 원자재 쇼크에 대비하기 위해 장기 공급 계약을 체결하고 있습니다. 아시아태평양이 현재 생산량을 주도하며 가장 빠른 성장세를 유지하고 있지만, 지역 내 생산능력 상한선, 지정학적 리스크, 탄소국경조정 조치로 인해 북미와 걸프 지역으로의 신규 투자가 증가하고 있습니다. 저탄소 빌릿, 재활용 깊이, 다공정 유연성을 갖춘 통합형 사업자는 알루미늄 시장에서 점유율 확대가 예상됩니다.

세계 알루미늄 시장 동향 및 인사이트

전기자동차 중심의 경량화 수요 급증

배터리 전기자동차(BEV)는 내연기관차 대비 알루미늄 사용량이 3배에 달하며, 2024년에는 북미에서 대당 885파운드(약 402kg)에 달할 것으로 예상됩니다. 무게가 10% 감소할 때마다 항속거리가 약 7% 늘어나기 때문에 자동차 제조업체들은 현재 차체, 배터리 트레이, 충돌 구조물, 열 관리 시스템에 알루미늄을 지정하고 있습니다. 성숙 시장에서는 2028년 이후 전기자동차 보급률이 정점을 찍을 가능성이 있지만, 모델 믹스의 진화에 따라 단위당 금속 사용량은 계속 증가할 것이며, 자동차 총 판매량 변동에도 불구하고 알루미늄 시장의 성장 경로가 유지될 것입니다.

아시아태평양의 인프라 붐

아시아태평양의 메가 프로젝트 계획은 장기적인 수요 전망을 뒷받침하고 있습니다. 중국의 소비량은 2000년 이후 연간 약 16%의 속도로 확대되어 다른 지역의 1%대를 크게 상회하고 있습니다. 스마트 시티 전력망, 고속철도, 국경 간 송전망은 알루미늄의 전기 전도성과 내식성에 의존하고 있으며, 이 지역의 1차 잉곳과 가공 제품 모두에 대한 수요를 보장하고 있습니다. 구조적 둔화는 주기적 위험을 초래하지만, 역사적으로 볼 때 경기 부양책 지출은 경기 침체를 완화하고 장기적으로 알루미늄 시장을 높은 수준으로 유지해 왔습니다.

에너지 가격 변동성

전력 비용은 제련 현금 비용의 약 40%를 차지합니다. 2024년 유럽 현물 전력 가격 급등으로 인해 여러 차례의 생산 억제 조치가 발생하여 연간 100만 톤 이상의 공급이 사라졌습니다. 제련소는 용해로의 동결로 인한 영구적인 손상 위험으로 인해 생산량을 저렴하게 축소할 수 없고, 일중 가격 변동에 대한 노출이 증가하고 있습니다. 재생에너지는 장기적인 안정성을 제공하지만, 과도기적 자금 조달과 전력망 병목 현상이 단기적인 마진을 압박하고 알루미늄 산업 전반에 걸쳐 고비용 지역에서의 확장 의지를 억제하고 있습니다.

부문 분석

압출 제품은 건축용 프로파일, 방열판, 자동차 충돌 안전 부품을 배경으로 2025년 알루미늄 시장 점유율의 35.05%를 차지했습니다. 저탄소 빌렛을 대규모로 공급할 수 있는 압출업체는 프리미엄 가격 조건으로 장기 공급 계약을 체결하고 있습니다. 주조품은 자동차 차체 구조에 기가주조 채택에 힘입어 2031년까지 3.5%로 가장 빠른 성장률을 보이고 있습니다. 장비 제조업체들은 2027년까지 다이캐스팅 라인에 대한 주문이 가득 차 있다고 보고하고 있으며, 이는 파워트레인 및 섀시 애플리케이션의 알루미늄 시장 규모가 지속적으로 확대될 수 있는 생산능력의 급격한 증가를 강조하고 있습니다.

평강제품은 음료용 강판과 자동차 패널 시트에서 확고한 입지를 유지하고 있습니다. 선진 제철소에서는 폐쇄형 스크랩 시스템을 도입하여 탄소 배출량을 줄이고 원료 확보의 안정화를 꾀하고 있습니다. 단조품은 랜딩 기어와 군용 차량에 공급되며, 엄격한 품질 기준을 바탕으로 고수익의 틈새시장을 유지하고 있습니다. 안료-분말은 전자기기 및 적층 가공(3D 프린팅)에 대응하며, 그 성장 궤도는 항공우주-의료기기 분야의 프린터 보급률에 따라 달라집니다. 다양한 가공 공정은 알루미늄의 적응성을 보여주며, 종합 제조업체가 압출 프레스, 압연기, 다이캐스팅 셀에 대한 전략적 투자를 지속하여 광범위한 알루미늄 시장에서 점유율을 확보하는 이유를 설명합니다.

이 알루미늄 보고서는 가공 유형별(주조, 압출, 단조, 평강, 안료 및 분말), 최종사용자 산업별(자동차, 항공우주 및 방위, 건축 및 건설, 전기 및 전자, 포장, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 구분하여 조사하였습니다. 시장 예측은 톤 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 세계 물량의 69.58%를 차지하며 2031년까지 CAGR 3.51%를 기록할 것으로 예상됩니다. 중국의 4,500만 톤 상한제련소 건설은 둔화되고 있지만, 다운스트림 가공업은 계속 확대되어 국내 빌릿 수입 수요를 늘리고, 말레이시아 및 인도네시아의 2차 알루미늄 거점에 대한 투자를 촉진하고 있습니다. 인도에서는 스마트 시티 주택 및 철도 전기화 수요에 대응하기 위해 새로운 주조공장 프로젝트가 확대되고 있으며, 이 지역이 알루미늄 시장에 미치는 영향력을 더욱 강화하고 있습니다.

북미에서는 2024년 알루미늄 제품 생산량이 3.4% 증가했지만, 여전히 400만 톤의 공급 부족이 발생하고 있습니다. 연방정부의 특혜로 EGA의 오클라호마주 40억 달러 규모의 60만 톤급 제련소와 Century Aluminum의 5억 달러 규모의 그린애노드 공장이 추진되어 1980년 이후 미국 본토에서 처음으로 신규 1차 생산능력 증설이 이루어졌습니다. 유럽의 점유율은 에너지 쇼크와 제련소 폐쇄의 영향을 받아 빌릿 프리미엄 상승과 수입 의존도 증가를 초래하고 있습니다. 그러나 CBAM(Carbon Border Adjustment Mechanism)의 특혜와 보조금을 수반하는 재생 가능 전력이 리오틴토의 아이슬란드 ELYSIS 셀 도입 등 업계 전체가 2020년대 후반까지 탄소 없는 금속을 실현할 수 있는 개조 프로젝트를 유치하고 있습니다.

GCC 국가들은 저비용 전력을 활용하여 부가가치가 높은 압출용 빌렛을 수출하고 있습니다. 한편, 아프리카 보크사이트 파이프라인은 알루미늄 시장 가치사슬의 현지화를 목표로 하는 제련 사업으로 흘러들어가고 있습니다. 남미의 생산량은 알루미나가 풍부한 브라질을 중심으로 안정적이지만, 물류 문제와 자본 부족으로 인해 제약을 받고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The Aluminum market is expected to grow from 76.47 million tons in 2025 to 78.99 million tons in 2026 and is forecast to reach 92.87 million tons by 2031 at 3.29% CAGR over 2026-2031.

Robust growth follows aluminum's position as the second most used metal, its unbeatable strength-to-weight ratio, and a closed-loop recyclability profile that keeps 75% of all metal ever produced in circulation. Rapid electrification, renewable-energy build-outs, and sustainable packaging mandates are converging to lift demand even as producers confront decarbonization targets, volatile power prices, and trade policy shifts. Top players are channeling capital toward green smelting and scrap recovery, while downstream customers lock in long-run supply to shield themselves from raw material shocks. Asia-Pacific dominates current volumes and retains the fastest trajectory, yet regional capacity ceilings, geopolitical risks, and carbon-border fees are driving fresh investments in North America and the Gulf. Integrated operators with low-carbon billet, recycling depth, and multi-process flexibility stand to capture a growing share of the Aluminum market.

Global Aluminum Market Trends and Insights

Surging EV-led Lightweighting Demand

Battery electric vehicles house triple the aluminum content of internal-combustion models, hitting 885 lb per car in North America during 2024. Every 10% mass cut extends driving range by roughly 7%, so automakers now specify aluminum for body-in-white, battery trays, crash structures, and thermal systems. EV penetration may plateau in mature markets after 2028, yet model-mix evolution keeps per-unit metal intensity rising, preserving a growth channel for the Aluminum market even as total auto sales fluctuate.

APAC Infrastructure Boom

Asia-Pacific's megaproject pipeline underpins long-cycle demand visibility. Chinese consumption expanded nearly 16% per year since 2000, dwarfing 1% rates elsewhere. Smart-city grids, high-speed rail, and cross-border power links rely on aluminum's conductivity and corrosion resistance, ensuring the region's pull on both primary ingot and fabricated products. Structural slowdowns pose cyclical risk, but stimulus outlays historically cushion downturns, keeping the Aluminum market on an elevated base in the long horizon.

Energy-Price Volatility

Electricity accounts for nearly 40% of smelting cash costs. European spot power spikes in 2024 forced multiple curtailments that erased over 1 million tons of annualized supply. Smelters cannot ramp down cheaply because frozen pots risk permanent damage, amplifying exposure to intraday price swings. Renewables add long-term stability, but transition financing and grid bottlenecks clamp near-term margins, trimming expansion appetite in high-tariff regions across the aluminium industry.

Other drivers and restraints analyzed in the detailed report include:

- Sustainable Packaging Shift

- Hydrogen-Ready Green Smelting Capacity

- Carbon-Border Tariffs and ESG Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Extrusions represented 35.05% of Aluminum market share in 2025 on the back of architectural profiles, heat sinks, and vehicle crash-management parts. Extruders able to deliver low-carbon billet at scale are capturing long-term supply contracts with premium pricing clauses. Castings follow as the fastest riser at 3.5% through 2031, buoyed by giga-casting adoption in automotive body structures. Equipment builders report booked-out die-casting lines until 2027, highlighting a capacity sprint that keeps the Aluminum market size expanding within powertrain and chassis applications.

Flat-rolled products hold a solid slot across beverage can stock and auto panel sheet. Forward-looking mills integrate closed-loop scrap systems, shrinking carbon footprints and locking in feedstock surety. Forgings serve landing-gear and military vehicles, sustaining a high-margin niche underpinned by stringent quality standards. Pigments and powders cater to electronics and additive manufacturing; their trajectory depends on printer penetration rates in aerospace and medical device sectors. The multi-process spectrum underscores aluminum's adaptability and explains why integrated producers maintain strategic investments across extrusion presses, rolling mills, and die-casting cells to secure wallet share within the broader Aluminum market.

The Aluminum Report is Segmented by Processing Type (Castings, Extrusions, Forgings, Flat-Rolled Products, and Pigments and Powders), End-User Industry (Automotive, Aerospace and Defense, Building and Construction, Electrical and Electronics, Packaging, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific retained 69.58% of global volume in 2025 and is tracking a 3.51% CAGR through 2031. While Beijing's 45 million-ton ceiling slows greenfield smelters, downstream fabrication keeps expanding, propelling internal billet import needs and stimulating investment in secondary aluminum hubs across Malaysia and Indonesia. India scales new cast-house projects to meet smart-city housing and railway electrification, reinforcing the region's gravitational pull on the Aluminum market.

North America produced 3.4% more aluminum products in 2024, yet still logged a 4 million-ton supply deficit. Federal incentives now underpin EGA's USD 4 billion, 600,000-ton Oklahoma smelter and Century Aluminum's USD 500 million green-anode plant, marking the first primary capacity additions stateside since 1980. Europe's share is influenced by energy shocks, shuttered smelters, driving up billet premiums, and elevating import reliance. Yet CBAM incentives and subsidized renewable electricity are luring retrofit projects, such as Rio Tinto's ELYSIS cell roll-out in Iceland, that promise carbon-free metal by late-decade across the aluminium industry.

The GCC leverages low-cost power to export value-added extrusion logs, while Africa's bauxite pipelines flow toward refining ventures that seek to capture more of the Aluminum market value chain locally. South American volumes remain steady around alumina-rich Brazil but are constrained by logistics hurdles and capital scarcity.

- Alcoa Corporation

- AluminIum BahraIn B.S.C. (Alba)

- Aluminum Corp of China (Chalco)

- China Hongqiao Group Limited

- East Hope Group

- Emirates Global Aluminium PJSC

- Novelis Inc.

- Norsk Hydro ASA

- Rio Tinto

- RUSAL

- Xinfa Group

- Vedanta Aluminium

- Century Aluminum Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging EV-Led Lightweighting Demand

- 4.2.2 APAC Infrastructure Boom

- 4.2.3 Renewable-Energy Aluminum Demand

- 4.2.4 Sustainable Packaging Shift

- 4.2.5 Hydrogen-Ready Green Smelting Capacity

- 4.3 Market Restraints

- 4.3.1 Energy-Price Volatility

- 4.3.2 Carbon-Border Tariffs and ESG Scrutiny

- 4.3.3 Graphene-Coated Steel Threat in Cans

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Import-Export Trends

- 4.7 Pricing Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Processing Type

- 5.1.1 Castings

- 5.1.2 Extrusions

- 5.1.3 Forgings

- 5.1.4 Flat-Rolled Products

- 5.1.5 Pigments and Powders

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Packaging

- 5.2.6 Industrial

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alcoa Corporation

- 6.4.2 AluminIum BahraIn B.S.C. (Alba)

- 6.4.3 Aluminum Corp of China (Chalco)

- 6.4.4 China Hongqiao Group Limited

- 6.4.5 East Hope Group

- 6.4.6 Emirates Global Aluminium PJSC

- 6.4.7 Novelis Inc.

- 6.4.8 Norsk Hydro ASA

- 6.4.9 Rio Tinto

- 6.4.10 RUSAL

- 6.4.11 Xinfa Group

- 6.4.12 Vedanta Aluminium

- 6.4.13 Century Aluminum Company.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment