|

시장보고서

상품코드

1940662

아시아태평양의 콜드체인 물류 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

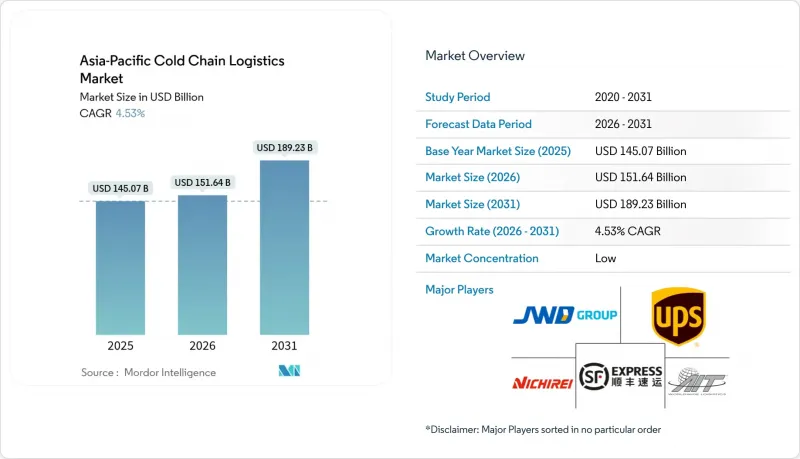

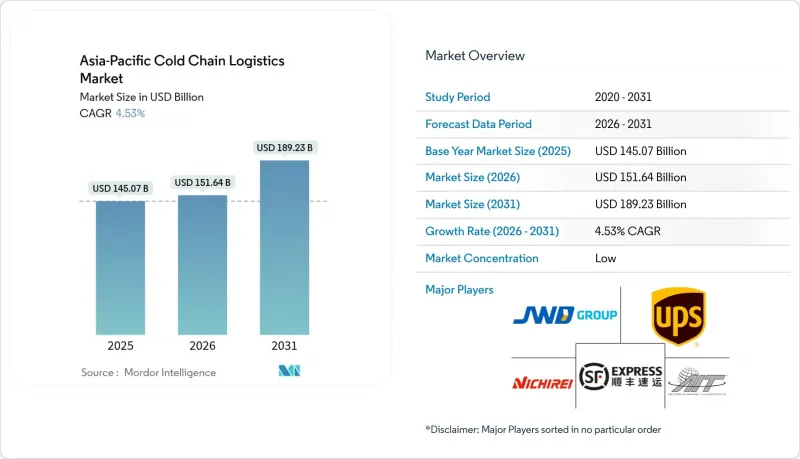

아시아태평양의 콜드체인 물류 시장은 2025년 1,450억 7,000만 달러에서 2026년에는 1,516억 4,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 4.53%를 기록하며 2031년까지 1,892억 3,000만 달러에 달할 것으로 예측됩니다.

가처분 소득의 증가, 전자 식료품 유통의 급속한 보급, 의약품 공급망의 고도화로 인해 수요는 꾸준한 상승세를 유지하고 있습니다. 한편, 전체 창고 건설은 급격한 확장에서 기술 주도의 효율적인 최적화로 전환되고 있습니다. 중국이 규모면에서 주도권을 쥐고 있지만, 인도의 분산형 물류창고의 급속한 구축은 당일 배송이 가능한 근접형 네트워크로의 결정적인 전환을 보여주고 있습니다. 사업자는 AI, 로봇 공학, 자연 냉매 시스템을 도입하여 에너지 소비와 노동력을 절감합니다. 이에 따라 아시아태평양 콜드체인 물류 시장에서 운영 우수성이 새로운 성장 동력으로 변모하고 있습니다. 경쟁 환경은 여전히 중간 정도의 분산 상태를 유지하고 있으며, 세계 통합 기업은 기술 역량 확보를 위해 M&A를 가속화하고 있습니다. 반면, 지역 전문 기업들은 어렵게 획득한 현지 허가와 퍼스트마일 노하우를 활용해 틈새시장을 지키고 있습니다.

아시아태평양 콜드체인 물류 시장 동향 및 인사이트

가공식품 및 냉동식품 소비 확대

아시아 중산층 가구는 조리 시간이 짧은 식사, 냉동 수산물, 다일분 단백질 팩에 대한 수요가 증가하고 있으며, 아시아태평양 콜드체인 물류 시장에서 지속적인 핵심 수요를 형성하고 있습니다. 이에 따라 슈퍼마켓 체인은 공장에서부터 매장까지 -18℃의 엄격한 관리가 필요한 냉동 메인 요리나 반조리 반죽 등 재고 관리 단위(SKU)의 전환을 추진하고 있습니다. 시설 소유주는 냉장-냉동-초저온 팔레트를 분리하기 위해 고층 보관 구역에 자동 셔틀 시스템을 도입하여 이동 시간과 에너지 손실을 줄였습니다. 스마트 라벨은 시간 온도 곡선을 기록하여 소매업체가 진열하기 전에 위험성이 있는 로트를 선별할 수 있도록 합니다. 이를 통해 폐기물을 줄이고 식품 안전 컴플라이언스를 강화할 수 있습니다. 도시 지역의 가구 규모가 계속 줄어들고 있으며, 소포장 상품 구매를 촉진하고 있습니다. 이는 저장 네트워크 내 유통 주기가 빠르기 때문에 팔레트 회전 속도가 빨라져 입방 미터당 수익이 증가합니다.

E-Commerce 음식 배달의 성장

즉시 배송 플랫폼은 15-30분 내 배송을 약속하며, 모듈식 냉각 장치를 갖춘 차세대 마이크로 풀필먼트 '다크 스토어'를 추진하고 있습니다. 에너지 절약형 가변속 컴프레서와 AI 구동 공조 시스템을 결합하여 엄격한 ±0.5℃ 범위를 유지하면서 전력 소비를 30% 절감합니다. 하이브리드형 패시브/액티브 젤팩 박스는 습한 방콕의 오후에도 아이스크림을 스쿠터로 배달할 수 있도록 도와줍니다. IoT 모니터가 소비자 앱으로 데이터를 전송하여 온도 투명성을 신뢰의 증표로 바꿉니다. 식료품 앱이 제2의 도시로 확장됨에 따라 수요는 도시 주변의 거대한 창고에서 인구가 밀집된 교외에 위치한 스포크형 창고로 이동하여 아시아태평양의 콜드체인 물류 시장의 발자취를 넓혀가고 있습니다.

냉장시설의 에너지 및 부동산 비용 상승

전력비는 운영비용의 70%를 차지하는 경우가 많으며, 도쿄와 시드니의 경우 데이터센터 수요 증가로 전력망에 대한 압박이 심해져 요금 상승으로 창고 수익률이 압박을 받고 있습니다. 태양광 패널 개보수를 통해 전기요금을 25% 절감할 수 있지만, 막대한 설비투자와 긴 허가 절차가 필요하기 때문에 대규모 옥상이나 신규 개발 프로젝트에 한정하여 도입이 가능합니다. 동시에 도심에서 10km 이내의 땅값이 급등하고 있어 개발업체들은 교외로 진출할 수밖에 없는 상황입니다. 이로 인해 저렴한 토지는 최종 배송 거리를 연장하고, 연료비를 증가시킵니다. 에너지 절약형 단열 패널과 가변 용량 압축기는 전력 비용 상승을 일부 상쇄하지만, 투자 회수 기간이 5년 이상 걸리기 때문에 소규모 사업자에게는 ROI 계산이 복잡해집니다.

부문 분석

2025년 기준, 냉장 창고는 아시아태평양 콜드체인 물류 시장의 40.55%를 차지했습니다. 현대식 고상식 냉동창고는 높이가 40미터에 달하며, 셔틀 로봇이 60초 이내에 팔레트를 운반할 수 있습니다. 이를 통해 인건비를 절반으로 줄이고, 창고 내 온도 관리의 정확성을 유지하고 있습니다. 사업자는 압축기 진동과 냉각수 압력을 모니터링하는 예지보전 소프트웨어를 도입하여 예기치 못한 가동 중단을 15% 줄였습니다.

부가가치 서비스는 규모는 작지만 브랜드 소유주가 재포장, 급속냉동, 제품 조정을 단일 3자 물류업체(3PL)에 위탁하는 움직임으로 인해 4.71%의 가장 높은 CAGR을 기록했습니다. 서비스 번들화를 통해 인수인계 횟수가 감소하고, 온도 편차 및 책임 분쟁을 최소화할 수 있습니다. 공공창고에서는 체류시간과 온도대에 따른 유연한 슬롯 가격 설정을 채택하여 부정기적인 출하를 고려하는 중소 식품 수출업체에 어필하고 있습니다. 한편, 전용 전용 시설은 검증된 레이아웃과 24시간 365일 감사 액세스를 요구하는 백신 제조업체를 끌어들이고 있습니다. 사일로화 된 창고에서 턴키 솔루션으로의 전환은 아시아태평양의 콜드체인 물류 시장이 종합적인 공급망 조정으로 전환하고 있음을 보여줍니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The Asia-Pacific Cold Chain Logistics Market is expected to grow from USD 145.07 billion in 2025 to USD 151.64 billion in 2026 and is forecast to reach USD 189.23 billion by 2031 at 4.53% CAGR over 2026-2031.

Rising disposable incomes, rapid e-grocery penetration, and pharmaceutical supply-chain upgrades keep demand on a steady upward course even as overall warehouse builds move from hyper-expansion to disciplined, technology-led optimization. China retains scale leadership, yet India's faster build-out of distributed depots signals a decisive pivot toward proximity-based networks designed for same-day fulfillment. Operators embed AI, robotics, and natural-refrigerant systems to compress energy intensity and labor exposure, turning operational excellence into the new growth lever for the Asia-Pacific cold chain logistics market. Competition remains moderately fragmented; global consolidators accelerate M&A to secure tech capabilities while regional specialists leverage hard-won local permits and first-mile know-how to guard niche positions.

Asia-Pacific Cold Chain Logistics Market Trends and Insights

Rising Consumption of Processed & Frozen Foods

Asia's middle-income households increasingly favor quick-prep meals, frozen seafood, and multi-day protein packs, creating a durable core of throughput for the Asia-Pacific cold chain logistics market. Supermarket chains respond by shifting stock-keeping units toward frozen entrees and par-baked dough that demand precise -18 °C handling from plant to shelf. Facility owners retrofit high-bay zones with automatic shuttle systems to segregate chilled, frozen, and deep-frozen pallets, trimming travel time and energy loss. Smart labels record time-temperature curves, letting retailers cull at-risk lots before display, which reduces write-offs and tightens food-safety compliance. Urban family sizes continue to shrink, spurring purchases of portioned packs that cycle through storage networks faster, raising pallet-turn velocity and amplifying revenue per cubic meter.

Growth in E-Commerce Grocery Delivery

Instant delivery platforms pledge 15- to 30-minute drop-offs, propelling a new generation of micro-fulfillment "dark" stores furnished with modular coolers. Energy-saving variable-speed compressors paired with AI-driven HVAC trim power draw by 30% while preserving tight +-0.5 °C bands. Hybrid passive-active gel-pack boxes allow ice-cream to survive scooter rides across humid Bangkok afternoons, and IoT monitors feed data to consumer apps, turning temperature transparency into a trust signal. As grocery apps expand into Tier-2 cities, demand shifts from mega-warehouses on city fringes to spoke depots embedded in densely populated suburbs, broadening the Asia-Pacific cold chain logistics market footprint.

High Energy & Real-Estate Cost of Cold Facilities

Electricity often represents 70% of opex, and data-center demand crowds grids across Tokyo and Sydney, driving tariff spikes that erode warehouse margins. Solar-panel retrofits cut bills 25% but entail high capex and lengthy permitting, restricting adoption to larger rooftops or greenfield projects. In parallel, land prices within 10 km of CBDs climb steeply, forcing developers outward where cheaper plots lengthen final-mile legs and elevate fuel spend. Energy-efficient insulation panels and variable-capacity compressors partially offset power hikes, but payback stretches past five years, complicating ROI math for smaller operators.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Pharmaceutical Cold Chain

- Harmonised SPS e-Certification & Paperless Customs Integration

- Rural First-Mile Infrastructure Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated storage contributed 40.55% to the Asia-Pacific cold chain logistics market in 2025. Modern high-bay freezers now rise 40 meters, using shuttle robots to pull pallets in under 60 seconds, halving manual labor and maintaining chamber integrity. Operators invest in predictive maintenance software that monitors compressor vibration and coolant pressure, cutting unplanned downtime by 15%.

Value-added services, though smaller, capture the strongest 4.71% CAGR as brand owners outsource repackaging, blast-freezing, and product conditioning to a single 3PL. Service bundling reduces handoffs, thereby minimizing temperature excursions and liability disputes. Public warehouses embrace flexible slot-pricing based on dwell time and temperature band, appealing to SME food exporters eyeing sporadic shipments. Conversely, private dedicated sites attract vaccine manufacturers that demand validated layouts and 24/7 audit access. The shift from siloed warehousing to turnkey solutions underscores how the Asia-Pacific cold chain logistics market pivots toward holistic supply-chain orchestration.

The Asia-Pacific Cold Chain Logistics Market Report is Segmented by Service Type (Refrigerated Storage, Refrigerated Transportation, and Value-Added Services), Temperature Type (Chilled, Frozen, Ambient, and Deep-Frozen/Ultra-Low), Application (Fruits & Vegetables, Meat & Poultry, Fish & Seafood, and More), Country (China, Japan, India, South Korea, Indonesia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- United Parcel Service (UPS)

- JWD Group

- Nichirei Logistics Group Inc

- SF Express

- AIT Worldwide Logistics Inc

- CWT Pte Ltd

- Rokin Logistics

- Lineage Logistics

- Kerry Logistics Network Ltd

- Snowman Logistics Ltd

- ColdEX Logistics Pvt Ltd

- Linfox Pty Ltd

- Yusen Logistics Co Ltd (Part of NYK Line)

- Kuehne + Nagel

- DHL Group

- DSV

- Nippon Express

- Yamato Transport Co. Ltd

- CEVA Logistics

- Konoike Transport Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising consumption of processed & frozen foods

- 4.2.2 Growth in e-commerce grocery delivery

- 4.2.3 Expansion of pharmaceutical cold chain

- 4.2.4 Harmonised SPS e-Certification & Paperless Customs Integration

- 4.2.5 Retailer-led captive cold warehousing

- 4.2.6 Multilateral Infrastructure Corridors Expanding Refrigerated Capacity

- 4.3 Market Restraints

- 4.3.1 High energy & real-estate cost of cold facilities

- 4.3.2 Rural first-mile infrastructure gaps

- 4.3.3 Shortage of low-GWP refrigerant engineers

- 4.3.4 Divergent ESG disclosure burdens on emissions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Emission Standards on the Industry

- 4.9 Impact of COVID-19 and Geo-Political Events on the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Refrigerated Storage

- 5.1.1.1 Public Warehousing

- 5.1.1.2 Private Warehousing

- 5.1.2 Refrigerated Transportation

- 5.1.2.1 Road

- 5.1.2.2 Rail

- 5.1.2.3 Sea

- 5.1.2.4 Air

- 5.1.3 Value-Added Services

- 5.1.1 Refrigerated Storage

- 5.2 By Temperature Type

- 5.2.1 Chilled (0-5 °C)

- 5.2.2 Frozen (-18-0 °C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.3 By Application

- 5.3.1 Fruits & Vegetables

- 5.3.2 Meat & Poultry

- 5.3.3 Fish & Seafood

- 5.3.4 Dairy & Frozen Desserts

- 5.3.5 Bakery & Confectionery

- 5.3.6 Ready-to-Eat Meals

- 5.3.7 Pharmaceuticals & Biologics

- 5.3.8 Vaccines & Clinical Trial Materials

- 5.3.9 Chemicals & Specialty Materials

- 5.3.10 Other Perishables

- 5.4 By Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 South Korea

- 5.4.5 Indonesia

- 5.4.6 Thailand

- 5.4.7 Australia

- 5.4.8 Singapore

- 5.4.9 Malaysia

- 5.4.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 United Parcel Service (UPS)

- 6.4.2 JWD Group

- 6.4.3 Nichirei Logistics Group Inc

- 6.4.4 SF Express

- 6.4.5 AIT Worldwide Logistics Inc

- 6.4.6 CWT Pte Ltd

- 6.4.7 Rokin Logistics

- 6.4.8 Lineage Logistics

- 6.4.9 Kerry Logistics Network Ltd

- 6.4.10 Snowman Logistics Ltd

- 6.4.11 ColdEX Logistics Pvt Ltd

- 6.4.12 Linfox Pty Ltd

- 6.4.13 Yusen Logistics Co Ltd (Part of NYK Line)

- 6.4.14 Kuehne + Nagel

- 6.4.15 DHL Group

- 6.4.16 DSV

- 6.4.17 Nippon Express

- 6.4.18 Yamato Transport Co. Ltd

- 6.4.19 CEVA Logistics

- 6.4.20 Konoike Transport Co., Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment