|

시장보고서

상품코드

1940683

인증기관 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Certificate Authority - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

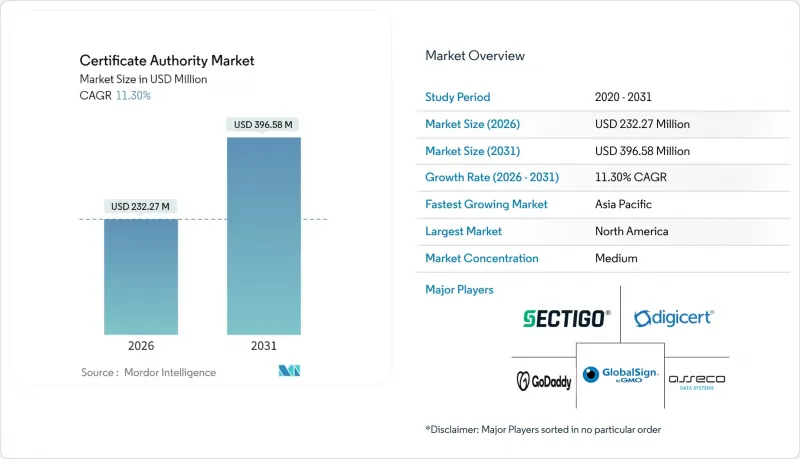

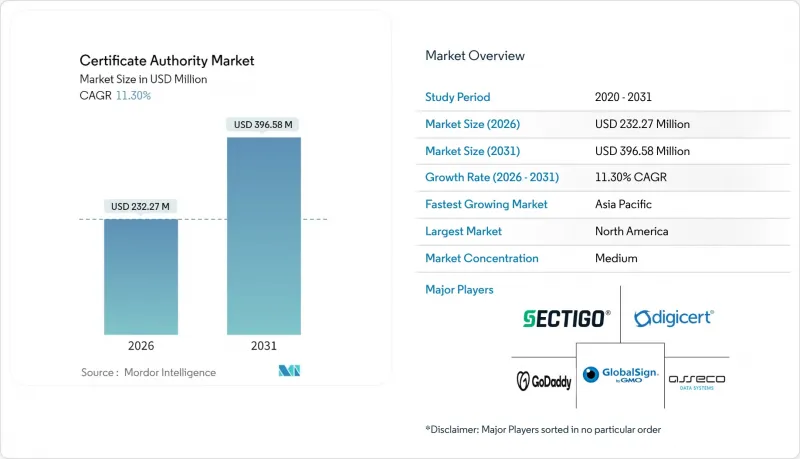

2026년 인증기관(CA) 시장 규모는 2억 3,227만 달러로 추정되며, 2025년 2억 868만 달러에서 성장이 전망됩니다.

2031년에는 3억 9,658만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 연평균 11.3%의 성장률을 보일 것으로 전망됩니다.

조직이 경계 기반 방어에서 모든 디지털 상호 작용에 암호학적 검증에 의존하는 신원 중심 모델로 전환함에 따라 채택이 가속화되었습니다. 인증서 수명주기 단축, 포스트 양자 암호로의 조기 전환, 제로 트러스트의 빠른 도입으로 인해 갱신량이 증가하고 자동화가 이사회 차원의 우선순위로 격상되었습니다. 브라우저 벤더가 사실상 규제기관으로 기능하고, 특히 구글 크롬의 엄격한 루트 프로그램 적용으로 인해 가격이 아닌 컴플라이언스 실적에 따라 공급업체 선정이 재구성되었습니다. 동시에, 클라우드 관리형 PKI 서비스는 아웃소싱된 전문 지식이 수동 프로세스에서는 불가능한 속도와 일관성을 제공할 수 있다는 것을 입증했습니다. 아시아태평양의 급격한 E-Commerce 성장과 각국 정부의 PKI 의무화와 맞물려 아시아태평양은 성숙한 북미와 유럽 시장보다 훨씬 가파른 성장 곡선을 그리며 성장세를 보이고 있습니다.

세계 인증기관 시장 동향 및 인사이트

엄격한 규제 및 규정 준수 의무

브라우저 루트 스토어 소유자는 보다 엄격한 규정 준수를 시행하고 있으며, 그 대표적인 예가 크롬이 2024년 10월 이후 발급되는 엔트러스트 인증서에 대한 신뢰 중단을 발표한 것입니다. 기업 구매자들은 결과적으로 CA의 징계 기록과 기술적 우위를 평가하는 경향이 강해졌고, 이러한 추세는 현재도 인증기관 시장을 재편하고 있습니다. 2029년 3월까지 TLS의 최대 유효기간을 47일로 단축하는 CA/Browser Forum의 새로운 규칙은 갱신량을 증가시키고 실시간 자동화를 갖춘 공급자에게 유리하게 작용할 것입니다. 관리형 PKI 벤더들은 이미 독립적인 감사 결과를 강조하며 컴플라이언스 대응을 위한 준비 태세를 보여주고 있습니다. 한편, 금융, 의료 등 규제 산업에서는 향후 신뢰 상실 위험에 따른 평판 리스크를 피하기 위해 1등급 인증기관과의 계약 갱신에 박차를 가하고 있습니다.

클라우드 기반 PKI 서비스 확대

하드웨어 보안 모듈(HSM), CRL 배포 지점, 감사 관리를 자체적으로 유지하기를 원하지 않는 조직에게 클라우드 제공은 기본 출발점이 되었습니다. 2024년 12월, DigiCert는 주력 플랫폼을 Microsoft Azure 마켓플레이스에 등록하여 클릭 한 번으로 조달 및 종량제 확장을 실현했습니다. Paddy Power Betfair 등의 사례에서 HashCorp Vault-as-a-Service로의 전환으로 인증서 발급 리드 타임이 1주일에서 1시간으로 단축되었습니다. 애플이 47일 유효기간을 추진하는 가운데, 시장이 거의 지속적인 업데이트로 전환됨에 따라 이러한 효율성은 더욱 중요해지고 있습니다. 자동화된 키 갱신, 정책 적용, 즉시 해지 기능으로 차별화를 꾀하는 벤더는 기존 단위 기반 SSL 판매업체에 비해 확실한 가격 결정력을 확보했습니다.

자기서명인증서 보급 현황

레거시 애플리케이션과 예산 제약이 있는 팀은 내부 네트워크는 신뢰할 수 있다는 인식 하에 자체 서명 인증서를 계속 도입했습니다. Dell의 eDellRoot 사건과 같은 주목할 만한 실패 사례는 이러한 인증서가 중간자 공격에 악용될 수 있는 가능성을 부각시켰습니다. 자체 서명형 도입은 인증기관(CA) 비용을 피할 수 있기 때문에 특히 신흥 시장의 소규모 IT 부문에 여전히 매력적입니다. 이를 위해 상용 CA는 숨겨진 자기서명형 자산을 가시화하고, 위험 감소 효과를 금전적으로 산출하는 발견 및 마이그레이션 툴킷을 번들로 제공했습니다.

부문 분석

인증서 유형은 브라우저가 모든 공개 웹 엔드포인트에 강제하는 SSL/TLS 수요를 기반으로 2025년 매출의 67.80%를 차지했습니다. 그러나 서비스 분야가 성장의 원동력이 되어 CAGR 20.35%로 확대되었습니다. 이는 개별 파일 구매보다 운영 효율성의 중요성을 인식했기 때문입니다. 애플의 47일 유효기간이 다가오면서 수동 갱신 프로세스는 유지가 어려워졌고, 기업들은 검색 기능, 정책 적용, 머신 퍼스트 발행 엔진이 통합된 관리형 PKI 구독으로 전환했습니다.

서비스 제공업체는 평균 업데이트 시간을 며칠에서 몇 분으로 단축할 수 있음을 보여줬으며, 규제 당국을 위한 감사 추적도 제공했습니다. 자동화를 통해 키 침해 발생 시 일괄 소멸 및 즉시 재발급도 실현했습니다. 그 결과, 애널리스트들은 2030년까지 서비스 부문의 시장 규모가 인증서 유형 부문을 능가할 것으로 예측하며, 인증기관 시장의 구조적 전환을 시사하고 있습니다. 이러한 진화는 현재 인증기관 업계가 인증서 단가가 아닌 플랫폼의 견고성으로 경쟁하고 있는 이유를 뒷받침합니다.

2025년에는 대기업이 전체 지출의 63.70%를 차지했으며, 이는 다층적인 신뢰 모델을 필요로 하는 복잡한 멀티 클라우드 환경을 반영합니다. 제로 트러스트 개념의 확대에 따라 예산은 계속 증가하여 인증기관 시장의 절대적인 규모를 강화했습니다. 그러나 중소기업 부문은 18.10%의 CAGR로 보다 급격한 성장세를 보였습니다. 클라우드 네이티브 PKI 솔루션은 구독 방식으로 엔터프라이즈급 기능을 제공하며, 하드웨어 보안 모듈이나 공개키 전문가가 필요 없는 클라우드 네이티브 PKI 솔루션입니다.

SaaS 청구 시스템과 사전 통합된 ACME 커넥터를 통해 스타트업 기업은 도메인 등록 후 몇 분 만에 신뢰할 수 있는 인증서를 도입할 수 있게 되었습니다. 예를 들어 인도네시아에서는 QRIS 디지털 결제 프레임워크가 표준화된 PKI 기반을 활용하여 소규모 사업자의 안전한 온라인화를 실현하고 있습니다. 이러한 사용 사례는 사이버 보안 전문 지식과 예산이 부족한 지역에서도 합리적인 가격의 자동화된 PKI가 디지털 상거래의 문을 열 수 있다는 것을 입증했습니다.

인증서 발급기관 시장 보고서는 구성요소별(SSL/TLS 인증서, 코드 서명 인증서 등) 조직 규모(대기업, 중소기업), 최종사용자 업종(BFSI, IT 및 통신, 소매 및 E-Commerce 등), 인증서 검증 수준(도메인 검증, 조직 검증 등), 도입 모델(온프레미스 PKI, 클라우드/관리형 PKI), 지역별로 세분화되어 있습니다. 조직 검증 등), 도입 모델(온프레미스 PKI, 클라우드/관리형 PKI), 지역별로 분류되어 있습니다.

지역별 분석

북미는 성숙한 사이버 보안 예산, 적극적인 제로 트러스트 도입 계획, 3072비트 RSA 키로의 조기 전환을 배경으로 2025년 기준 전 세계 매출의 35.20%를 차지했습니다. 백악관 대통령령 14028호 등 연방정부 지침에 따라 정부 기관은 지속적인 인증서 모니터링을 도입하도록 촉구하고 있으며, 컴플라이언스 툴을 위한 인증기관 시장 규모가 확대되고 있습니다. 이 지역의 성장은 현재 라이프사이클 업무 자동화 및 포스트 양자 알고리즘 시범 프로젝트에 의존하고 있으며, DigiCert가 2025년 4월에 발표한 디리튬 시험용 인증서가 그 증거입니다.

아시아태평양은 16.55%의 가장 빠른 CAGR을 기록했습니다. 이는 현금 없는 결제 확대, 데이터 현지화법, 인도, 베트남, 인도네시아의 정부 주도의 PKI 확산에 힘입은 바 큽니다. 인도 중앙은행의 디지털 결제 트러스트 앵커에 대한 가이드라인은 현지 은행의 인증서 워크플로우 현대화를 촉진했습니다. 국내 클라우드 사업자는 세계 CA와 제휴하여 E-Commerce 플랫폼에 턴키 발급 기능을 탑재하고 있습니다. 이를 통해 수백만 개의 중소기업이 사내 전문 지식 없이도 규정을 준수할 수 있게 되었습니다. 중국이 추진하는 국산 알고리즘은 지역 벤더의 호환성 매트릭스 확장을 촉진하고 공급업체 다양화를 가져왔습니다.

유럽에서는 GDPR의 개인정보 보호 규정이 꾸준히 발전하고 있으며, 데이터 처리 사업자는 암호화 및 키 관리 관행을 문서화해야 합니다. eIDAS 개정은 또한 적격 웹사이트 인증 인증서에 대한 수요를 촉진하여 광범위한 인증 기관 시장 내에서 프리미엄 틈새 시장을 형성하고 있습니다. 한편, 중동 및 아프리카 시장에서는 스마트 시티 및 오픈뱅킹 프로젝트 관련 도입이 증가하는 추세이지만, 인프라의 편차로 인해 대규모 자동 발급이 지연되는 사례도 나타났습니다. 남미의 동향은 완만하지만 견조한 흐름으로 정부기관 포털에 TLS 도입이 의무화되는 한편, 브라질의 핀테크 샌드박스에서는 ACME 호환 발행기관을 활용하여 새로운 서비스를 빠르게 출시했습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 세분화

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10Certificate Authority market size in 2026 is estimated at USD 232.27 million, growing from 2025 value of USD 208.68 million with 2031 projections showing USD 396.58 million, growing at 11.3% CAGR over 2026-2031.

Adoption accelerated as organizations shifted from perimeter-based defenses to identity-centric models that rely on cryptographic validation for every digital interaction. Shorter certificate lifecycles, early moves toward post-quantum cryptography, and rapid zero-trust rollouts increased renewal volumes and elevated automation to a board-level priority. Browser vendors acting as de facto regulators, notably through Google Chrome's stricter root-program enforcement, reshaped supplier selection around compliance history rather than price. At the same time, cloud-managed PKI services demonstrated that outsourced expertise can deliver speed and consistency impossible to match with manual processes. Asia-Pacific's e-commerce boom, combined with government PKI mandates, placed the region on a markedly steeper growth curve than mature North American and European markets..

Global Certificate Authority Market Trends and Insights

Stringent Regulations and Compliance Mandates

Browser root-store owners enforced stricter compliance, best illustrated when Chrome announced distrust of Entrust certificates issued after October 2024. Enterprise buyers consequently evaluated CAs on their disciplinary record as much as on technical merit, a trend that continues to reshape the Certificate Authority Market. The forthcoming CA/Browser Forum rule that cuts TLS maximum validity to 47 days by March 2029 will magnify renewal volumes and favor providers equipped with real-time automation. Managed PKI vendors already highlight independent audit results to demonstrate readiness for this compliance wave. Meanwhile, regulated industries such as finance and healthcare accelerated contract renewals with Tier-1 CAs to avoid the reputational risk tied to potential future distrust events.

Expansion of Cloud-Based PKI Services

Cloud delivery became the default starting point for organizations unwilling to maintain hardware security modules, CRL distribution points, and audit controls in-house. DigiCert placed its flagship platform on Microsoft Azure Marketplace in December 2024, enabling click-through procurement and pay-as-you-go scaling. Case studies such as Paddy Power Betfair cut certificate issuance lead times from one week to one hour after migrating to HashiCorp Vault-as-a-Service. These gains matter even more as Apple's push for 47-day validity moves the market toward almost continuous renewal. Vendors differentiating on automated key-rotation, policy enforcement, and instant revocation earned clear pricing power over legacy, unit-based SSL sellers.

Prevalence of Self-Signed Certificates

Legacy applications and budget-constrained teams continued to deploy self-signed certificates, believing that interior networks remained trustworthy. High-profile failures, such as Dell's eDellRoot incident, illustrated how these certificates can be exploited for man-in-the-middle attacks. Because self-signed deployments avoid CA fees, they still appeal to small IT departments, especially in emerging markets. Commercial CAs, therefore, bundled discovery and migration toolkits to expose hidden self-signed assets and calculate risk savings in monetary terms.

Other drivers and restraints analyzed in the detailed report include:

- DevSecOps-Led Certificate Automation

- Machine-Identity Demand in Zero-Trust Networks

- Regulatory Uncertainty on Post-Quantum Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Certificate Types retained 67.80% of 2025 revenue, anchored by SSL/TLS demand that browsers enforce for every public web endpoint. However, Services generated the momentum, expanding at 20.35% CAGR as customers realized that operational excellence matters more than purchasing individual files. With Apple's 47-day validity on the horizon, manual renewal processes became untenable, pushing enterprises toward managed PKI subscriptions that bundle discovery, policy enforcement, and machine-first issuance engines.

Services providers showed they could shrink mean-time-to-renewal from days to minutes while supplying audit trails for regulators. Automation also enabled bulk revocation and immediate re-issuance during key-compromise events. As a result, analysts projected Services to surpass Certificate Types by value before 2030, marking a structural shift in the certificate authority market. This evolution underscores why the certificate authority industry now competes on platform robustness rather than on certificate unit price.

Large Enterprises generated 63.70% of total spending in 2025, reflecting complex multi-cloud estates that require layered trust models. Their budgets continued to climb as zero-trust initiatives expanded, reinforcing the certificate authority market size in absolute terms. Yet the SME segment exhibited the steeper trajectory at an 18.10% CAGR. Cloud-native PKI offerings delivered enterprise-grade functionality via subscription, removing the need for hardware security modules or public-key specialists.

SaaS invoicing and pre-integrated ACME connectors allowed start-ups to deploy trusted certificates within minutes of domain registration. In Indonesia, for example, QRIS digital payment frameworks used standardized PKI rails to bring micro-merchants online securely. These use cases validated the idea that affordable, automated PKI can unlock digital commerce in regions where cybersecurity expertise and budgets remain limited.

The Certificate Authority Market Report is Segmented by Component (SSL/TLS Certificates, Code-Signing Certificates, and More), Organization Size (Large Enterprises, and SMEs), End-User Vertical (BFSI, IT and Telecom, Retail and E-Commerce, and More), Certificate Validation Level (Domain Validation, Organization Validation, and More), Deployment Model (On-Premise PKI, and Cloud/Managed PKI), and Geography.

Geography Analysis

North America retained 35.20% of global revenue in 2025 on the back of mature cybersecurity budgets, aggressive zero-trust roadmaps, and early migration to 3072-bit RSA keys. Federal directives such as the White House Executive Order 14028 prompted agencies to adopt continuous certificate monitoring, reinforcing the certificate authority market size for compliance tooling. The region's growth now hinges on automating lifecycle tasks and pilot projects for post-quantum algorithms, evidenced by DigiCert's Dilithium test-certificates released in April 2025.

Asia-Pacific posted the swiftest CAGR at 16.55%, sparked by cashless-payment expansion, data-localization statutes, and government PKI rollouts in India, Vietnam, and Indonesia. The Reserve Bank of India's guidelines for digital-payment trust anchors spurred local banks to modernize certificate workflows. Domestic cloud providers partnered with global CAs to embed turnkey issuance into e-commerce platforms, allowing millions of SMEs to comply without in-house expertise. China's push for indigenous algorithms also encouraged regional vendors to expand compatibility matrices, broadening supplier variety.

Europe maintained steady momentum under GDPR's privacy regime, where data processors must document encryption and key-management practices. The eIDAS revision additionally drives demand for qualified website authentication certificates, creating a premium niche within the broader certificate authority market. Meanwhile, Middle East and Africa markets showed rising adoption tied to smart-city and open-banking projects, though uneven infrastructure sometimes slowed large-scale automated issuance. South America's trajectory remained moderate but positive; governments there increasingly required TLS on public-sector portals, while fintech sandboxes in Brazil leveraged ACME-compatible issuers to launch new services rapidly.

- DigiCert Inc.

- Sectigo Ltd.

- GoDaddy Group (Starfield Tech.)

- GlobalSign (KGZ)

- Entrust Corp.

- IdenTrust Services LLC

- Let's Encrypt / ISRG

- Actalis S.p.A

- SSL.com LLC

- Trustwave SecureTrust

- Network Solutions LLC

- WISeKey Intl. Holdings Ltd.

- SwissSign AG

- OneSpan Inc.

- Camerfirma SA

- Buypass AS

- QuoVadis Trustlink (Bermuda) Ltd.

- Certum (Asseco Data Systems SA)

- Amazon Trust Services

- Google Trust Services LLC

- Microsoft Azure TLS

- Oracle Cloud CA

- Cloudflare Inc.

- DigiSigner LLC

- HARICA (Hellenic Academic CA)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing awareness of secure web access

- 4.2.2 Stringent regulations and compliance mandates

- 4.2.3 Surge in e-commerce and online transactions

- 4.2.4 Expansion of cloud-based PKI services

- 4.2.5 DevSecOps-led certificate automation

- 4.2.6 Machine-identity demand in zero-trust networks

- 4.3 Market Restraints

- 4.3.1 Low security-certificate awareness in emerging SMBs

- 4.3.2 Prevalence of self-signed certificates

- 4.3.3 Certificate lifecycle complexity at hyperscale

- 4.3.4 Regulatory uncertainty on post-quantum standards

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact Assessment of Key Stakeholders

- 4.9 Key Use Cases and Case Studies

- 4.10 Impact on Macroeconomic Factors of the Market

- 4.11 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Certificate Types

- 5.1.1.1 SSL/TLS Certificates

- 5.1.1.2 Code-Signing Certificates

- 5.1.1.3 Secure Email Certificates

- 5.1.1.4 Authentication/Client Certificates

- 5.1.2 Services

- 5.1.1 Certificate Types

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises (SMEs)

- 5.3 By End-user Vertical

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Retail and E-commerce

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Government and Public Sector

- 5.4 By Certificate Validation Level

- 5.4.1 Domain Validation (DV)

- 5.4.2 Organization Validation (OV)

- 5.4.3 Extended Validation (EV)

- 5.5 By Deployment Model

- 5.5.1 On-premise PKI

- 5.5.2 Cloud/Managed PKI

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 DigiCert Inc.

- 6.4.2 Sectigo Ltd.

- 6.4.3 GoDaddy Group (Starfield Tech.)

- 6.4.4 GlobalSign (KGZ)

- 6.4.5 Entrust Corp.

- 6.4.6 IdenTrust Services LLC

- 6.4.7 Let's Encrypt / ISRG

- 6.4.8 Actalis S.p.A

- 6.4.9 SSL.com LLC

- 6.4.10 Trustwave SecureTrust

- 6.4.11 Network Solutions LLC

- 6.4.12 WISeKey Intl. Holdings Ltd.

- 6.4.13 SwissSign AG

- 6.4.14 OneSpan Inc.

- 6.4.15 Camerfirma SA

- 6.4.16 Buypass AS

- 6.4.17 QuoVadis Trustlink (Bermuda) Ltd.

- 6.4.18 Certum (Asseco Data Systems SA)

- 6.4.19 Amazon Trust Services

- 6.4.20 Google Trust Services LLC

- 6.4.21 Microsoft Azure TLS

- 6.4.22 Oracle Cloud CA

- 6.4.23 Cloudflare Inc.

- 6.4.24 DigiSigner LLC

- 6.4.25 HARICA (Hellenic Academic CA)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment