|

시장보고서

상품코드

1940708

동남아시아의 POS 단말기 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Southeast Asia POS Terminal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

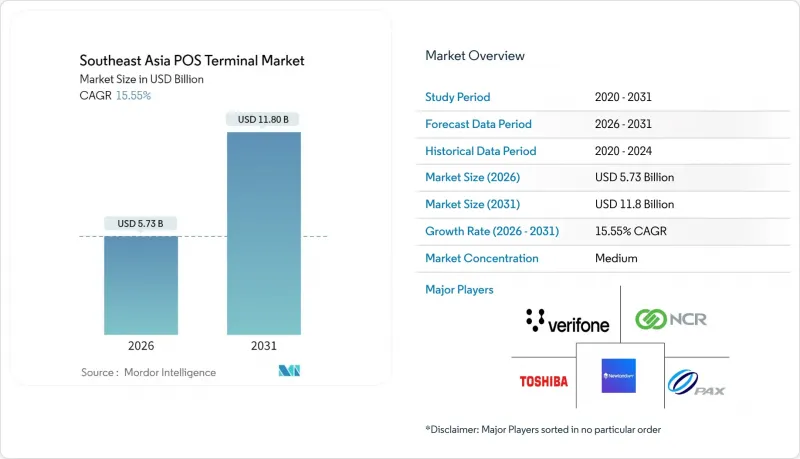

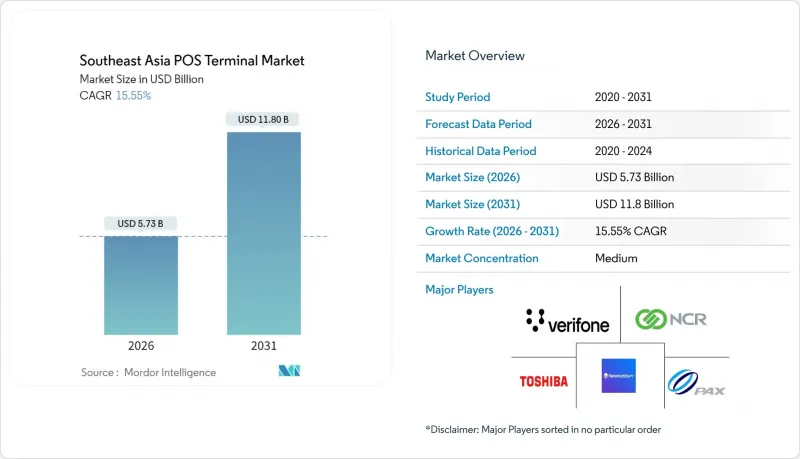

동남아시아의 POS 단말기 시장은 2025년에 49억 6,000만 달러로 평가되었으며, 2026년 57억 3,000만 달러에서 2031년까지 118억 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 15.55%로 예상됩니다.

소비자의 모바일 지갑으로의 전환 가속화, QR코드 보급 확대, 디지털 결제 도입을 의무화하는 정부 규제로 인해 동남아시아의 POS 단말기 시장은 빠르게 성장하고 있습니다. 가맹점은 QR코드, NFC, 카드 기능을 통합한 소프트웨어 정의형 또는 하이브리드 단말기로 자본을 전환하고 있으며, 카운터 위의 기기를 정리하면서 미래를 내다보는 결제 요구에 대응하고 있습니다. 경쟁의 초점은 하드웨어 사양에서 소프트웨어 생태계로 옮겨가고 있으며, 재고관리, CRM, 융자 툴을 클라우드 대시보드에 통합하는 벤더가 우위를 보이고 있습니다. 아세안 지역 결제 연결성 프로그램에 기반한 국경 간 결제 이니셔티브는 인증 주기를 단축할 것을 약속하고 있으며, 이 요소는 2030년까지 동남아시아 POS 단말기 시장 수요 확대의 핵심이 될 것입니다.

동남아시아 POS 단말기 시장 동향과 인사이트

동남아시아 전역의 디지털 결제의 급속한 확대

2024년, 인도네시아, 태국, 필리핀에서 모바일 지갑의 거래 건수가 기존 카드 네트워크를 넘어섰습니다. 이러한 변화로 인해 동남아시아 POS 단말기 시장 전체에서 멀티 모드 단말기 교체 주기가 가속화되고 있습니다. 인도네시아의 QRIS(QR코드 결제)만 해도 160억 건 이상의 거래를 기록하고 있으며, 가맹점은 단기능 카드 리더기에서 통합형 QR/NFC 단말기로의 전환을 강요받고 있습니다. 현재 단말기 제조사들은 옴니채널 API를 탑재한 단말기를 설계하여 매장과 배송 채널을 넘나드는 통일된 결제 처리를 실현하고 있습니다. 이에 따라 결제 처리 사업자는 5년의 단말기 수명 기간 동안 계속 사용할 수 있도록 포인트 프로그램, 재고 관리, BNPL(후불 결제) 등 부가가치 앱을 사전 탑재하고 있습니다. 그 결과, 특히 종이 전표나 현금지급기에서 업그레이드하는 소규모 가맹점을 중심으로 두 자릿수 성장의 하드웨어 교체 수요가 지속되고 있습니다.

정부 주도의 현금 없는 정책 및 전자결제 규제

말레이시아의 'e-Tunai Rakyat', 태국의 'PromptPay', 인도네시아의 중소기업 보조금 제도로 인해 동남아시아 POS 단말기 시장에는 분기마다 수천 대의 보조금 대상 단말기가 공급되고 있습니다. 컴플라이언스 조항은 인증된 NFC 및 EMV 기능 탑재를 의무화하고 있으며, 현지 보안 감사를 통과할 수 있는 중급형 안드로이드 모델의 주문이 가속화되고 있습니다. 보조금으로 초기 하드웨어 비용을 충당하는 경우가 많기 때문에 벤더들은 보조금 종료 후에도 지속적인 수익을 창출하는 SaaS 기반 라이선스 모델로 빠르게 전환하고 있습니다. 지방 도입 프로그램을 통해 수요는 지방 도시로 확대되고, 유통업체는 수도권 외 지역으로의 진출을 유기적인 가맹점 확보보다 훨씬 빠르게 진행할 수 있게 되었습니다.

사이버 보안 및 데이터 프라이버시 취약점

인도네시아 은행의 기록에 따르면, 2024년 POS 관련 사기 시도가 45% 급증할 것으로 예상되며, 미대응 시 신규 도입을 정체시킬 수 있는 실시간 위협이 부각되고 있습니다. 구형 펌웨어를 악용하는 악성코드는 단일 단말기가 침해되면 빠르게 확산되기 때문에 규제 당국은 무선 업데이트를 통한 패치 적용 주기를 의무화하고 있습니다. IT 담당자가 없는 소규모 소매업체는 보안 운영을 벤더에 의존하고 있습니다. 업데이트가 늦어지면 리스크 회피 성향이 강한 가맹점은 구매를 미루게 됩니다. 따라서 공급업체는 동남아시아 POS 단말기 시장의 성장세를 유지하기 위해 관리형 보안 서비스를 번들로 제공해야 합니다.

부문 분석

비접촉식 결제는 2025년 기준 동남아시아 POS 단말기 시장의 매출 점유율 56.97%를 차지하며, 2031년까지 CAGR 17.05%로 확대될 것으로 예상됩니다. 이러한 장점으로 인해 탭 결제는 신규 단말기 SKU의 표준 기능으로 자리매김하고 있습니다. 현재 각 업체들은 2초 미만의 결제 처리를 위해 안테나 배치와 화면 프롬프트 설계에 집중하고 있습니다. 이는 가맹점이 처리 능력의 향상으로 인식하는 특성입니다. QR코드의 대안은 소액 거래를 하는 소규모 가맹점의 사용 사례에서 여전히 필수적이며, 소비자가 지갑의 선택에 의해 결제가 방해받지 않도록 보장합니다.

단말기 제조사들은 엔트리 모델부터 기계식 카드 슬롯을 폐지하여 부품비 절감을 꾀하는 한편, 화면상의 비밀번호 입력(PIN-on-glass) 거래를 위한 SoftPOS를 추진하고 있습니다. 이러한 발전은 비접촉식 솔루션과 연계된 동남아시아 POS 단말기 시장 규모가 2020년 중반까지 카드 전용 하드웨어의 폐업 규모를 넘어설 것임을 시사합니다. 이러한 움직임은 또한 통신사들에게 상시 접속으로 인한 펌웨어 업데이트 및 분석 데이터 전송의 트래픽 급증에 따라 mPOS 구독에 대용량 LTE 데이터 요금제를 번들로 제공하도록 유도하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The Southeast Asia POS Terminal Market was valued at USD 4.96 billion in 2025 and estimated to grow from USD 5.73 billion in 2026 to reach USD 11.8 billion by 2031, at a CAGR of 15.55% during the forecast period (2026-2031).

Strong consumer migration to mobile wallets, rising ubiquity of QR codes, and government mandates that compel digital payment acceptance are keeping the Southeast Asia POS Terminal market on a steep growth trajectory. Merchants are shifting capital toward software-defined or hybrid devices that consolidate QR, NFC, and card functions, trimming counter clutter while future-proofing acceptance needs. Competitive focus has moved from hardware specifications to software ecosystems, favoring vendors that bundle inventory, CRM, and financing tools into cloud dashboards. Cross-border payment initiatives under the ASEAN Regional Payment Connectivity program promise faster certification cycles, a factor set to unlock incremental demand for the Southeast Asia POS Terminal market through 2030.

Southeast Asia POS Terminal Market Trends and Insights

Rapid Expansion of Digital Payments Across Southeast Asia

Mobile wallets processed more transactions than traditional card networks in Indonesia, Thailand, and the Philippines during 2024, a shift that has amplified replacement cycles for multi-modal devices across the Southeast Asia POS Terminal market. QRIS in Indonesia alone logged more than 16 billion transactions, forcing merchants to ditch single-function card readers in favor of integrated QR/NFC units. Device makers now design terminals with omnichannel APIs, enabling unified reconciliation across storefront and delivery channels. Payment processors, in turn, preload value-added apps loyalty, inventory, BNPL to keep devices sticky over a five-year lifespan. The net effect is sustained double-digit hardware refresh demand, particularly from micro-merchants upgrading from paper or cash registers.

Government Cash-less Initiatives and E-payment Regulations

Malaysia's e-Tunai Rakyat, Thailand's PromptPay, and Indonesia's SME subsidy schemes collectively inject thousands of subsidized terminals into the Southeast Asia POS Terminal market every quarter. Compliance clauses require certified NFC and EMV functionality, accelerating orders for mid-range Android models able to pass local security audits. Because subsidies often cover up-front hardware costs, vendors increasingly pivot to SaaS-based licensing that drives recurring revenue even after grants expire. Rural onboarding programs extend demand into second-tier cities, helping distributors expand beyond capital regions much faster than organic merchant acquisition would allow.

Cyber-security and Data-privacy Vulnerabilities

Bank Indonesia recorded a 45% jump in POS-linked fraud attempts during 2024, highlighting real-time threats that could stall new deployments if unaddressed. Malware that exploits outdated firmware spreads quickly once a single device is breached, prompting regulators to mandate over-the-air patch cycles. Smaller retailers, lacking IT staff, depend on vendors for security orchestration; when updates lag, risk-averse merchants defer purchases. Consequently, suppliers must bundle managed security services to keep the Southeast Asia POS Terminal market growth momentum intact.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of mPOS Among SMEs and Micro-merchants

- Integration of BNPL Capabilities into POS Hardware

- High Total Cost of Ownership for Modern POS Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contactless payments controlled 56.97% revenue share within the Southeast Asia POS Terminal market in 2025, and the segment is forecast to widen at a 17.05% CAGR through 2031. That dominance positions tap-to-pay as the baseline capability for every new device SKU. Vendors now engineer antenna placement and screen prompts to accelerate sub-two-second checkouts, an attribute that merchants equate with higher throughput. QR fallback remains essential for low-value micro-merchant use cases, ensuring no consumer gets blocked by wallet preference.

Terminal makers are stripping mechanical card slots from entry-level units, dropping component costs while promoting SoftPOS for PIN-on-glass transactions. This evolution underlines how the Southeast Asia POS Terminal market size tied to contactless solutions will eclipse card-only hardware retirements by mid-decade. The push also drives telcos to bundle higher LTE data caps with mPOS subscriptions, reflecting traffic spikes from always-connected firmware updates and analytics pings.

The Southeast Asia POS Terminal Market Report is Segmented by Mode of Payment Acceptance (Contact-Based and Contactless), POS Type (Fixed Point-Of-Sale System and Mobile/Portable Point-Of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Worldline SA (Ingenico)

- Verifone Systems LLC

- PAX Technology Ltd.

- NCR Corporation

- Toshiba TEC Corporation

- Newland Payment Technology Co., Ltd.

- HP Inc.

- Samsung Electronics Co., Ltd.

- Fujian Newland Computer Co., Ltd. (Urovo)

- SUNMI Technology Co., Ltd.

- SZZT Electronics Co., Ltd.

- Diebold Nixdorf, Incorporated

- NEC Corporation

- Fujitsu Limited

- BBPOS International Limited

- Centerm Information Co., Ltd.

- New POS Technology Ltd.

- Castles Technology Co., Ltd.

- SUNAR Technology Co., Ltd.

- Squareup International Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid expansion of digital payments across Southeast Asia

- 4.2.2 Government cash-less initiatives and e-payment regulations

- 4.2.3 Rising adoption of mPOS among SMEs and micro-merchants

- 4.2.4 Integration of BNPL capabilities into POS hardware

- 4.2.5 Tourism-driven omnichannel retail recovery post-COVID

- 4.2.6 Migration to Android-based open-OS terminals and app stores

- 4.3 Market Restraints

- 4.3.1 Cyber-security and data-privacy vulnerabilities

- 4.3.2 High total cost of ownership for modern POS devices

- 4.3.3 Fragmented certification rules across SEA nations

- 4.3.4 Weak device-servicing networks beyond tier-1 cities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Payment Acceptance

- 5.1.1 Contact-based

- 5.1.2 Contactless

- 5.2 By POS Type

- 5.2.1 Fixed Point-of-Sale Systems

- 5.2.2 Mobile / Portable Point-of-Sale Systems

- 5.3 By End-User Industry

- 5.3.1 Retail

- 5.3.2 Hospitality

- 5.3.3 Healthcare

- 5.3.4 Transportation and Logistics

- 5.3.5 Other End-User Industries

- 5.4 By Country

- 5.4.1 Singapore

- 5.4.2 Malaysia

- 5.4.3 Thailand

- 5.4.4 Indonesia

- 5.4.5 Philippines

- 5.4.6 Vietnam

- 5.4.7 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Worldline SA (Ingenico)

- 6.4.2 Verifone Systems LLC

- 6.4.3 PAX Technology Ltd.

- 6.4.4 NCR Corporation

- 6.4.5 Toshiba TEC Corporation

- 6.4.6 Newland Payment Technology Co., Ltd.

- 6.4.7 HP Inc.

- 6.4.8 Samsung Electronics Co., Ltd.

- 6.4.9 Fujian Newland Computer Co., Ltd. (Urovo)

- 6.4.10 SUNMI Technology Co., Ltd.

- 6.4.11 SZZT Electronics Co., Ltd.

- 6.4.12 Diebold Nixdorf, Incorporated

- 6.4.13 NEC Corporation

- 6.4.14 Fujitsu Limited

- 6.4.15 BBPOS International Limited

- 6.4.16 Centerm Information Co., Ltd.

- 6.4.17 New POS Technology Ltd.

- 6.4.18 Castles Technology Co., Ltd.

- 6.4.19 SUNAR Technology Co., Ltd.

- 6.4.20 Squareup International Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment