|

시장보고서

상품코드

1940709

초음파 유량계 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Ultrasonic Flow Meters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

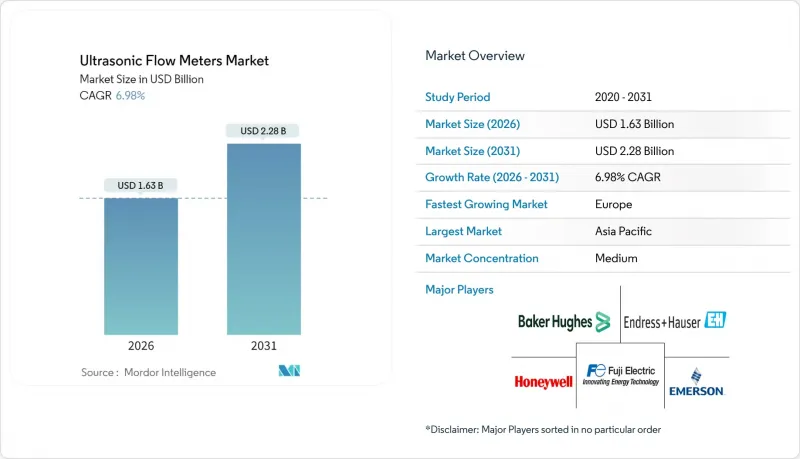

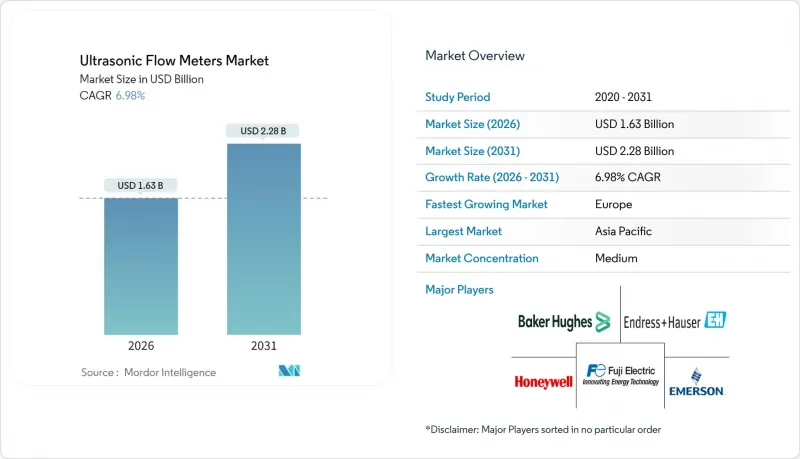

2026년 초음파 유량계 시장 규모는 16억 3,000만 달러로 추정되며, 2025년 15억 2,000만 달러에서 성장이 전망됩니다.

2031년까지 22억 8,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 6.98%로 확대될 것으로 전망됩니다.

대구경 가스 파이프라인의 검침용 유량계 도입 확대, 노후화된 상수도 네트워크의 클램프온 장치 개조 수요, 수소 인프라에 대한 초기 단계 투자로 인해 공정 산업 전반에 걸쳐 거의 두 자릿수에 가까운 수요가 지속되고 있습니다. 운영자는 차압식 및 터빈식 유량계와 비교하여 평생 운영 비용을 절감하고, 압력 손실 제로, 예측 유지보수, IIoT 통합과 같은 초음파 설계를 선호합니다. 화학 처리의 액체 배출 제로화 의무화, 도시 상수도 시스템의 누수 감소 프로그램 등 환경 규제가 엄격한 유량 관리를 요구하는 분야에서는 채택이 가속화되고 있습니다. 경쟁 차별화는 엣지 AI 진단, 멀티패스 리던던던시 등 까다로운 거래용 유량 측정 조건에서도 ±0.15%의 재현성을 유지하는 기술에 점점 더 초점이 맞춰지고 있습니다.

세계 초음파 유량계 시장 동향과 인사이트

대구경 가스 파이프라인에서 계량용 초음파 유량계로의 전환 가속화

파이프라인 사업자는 터빈식 유량계를 단계적으로 폐지하기 시작했습니다. 초음파 방식은 압력 손실로 인한 손실을 없애고, 압축기의 에너지 소비를 최대 15%까지 절감하며, 최소한의 유지보수로 20년의 수명을 보장하기 때문입니다. 멀티패스 설계로 API 준수 정확도를 실현하고, 소용량 프로버를 통한 현장 검증을 가능하게함으로써 교정을 위한 다운타임을 제한합니다. 이러한 채택은 북미 셰일가스 운송 경로와 중동 수출 파이프라인에서 특히 두드러지는데, 이 지역에서는 운송량의 변동성으로 인해 넓은 레이놀즈 수 허용 오차가 요구됩니다.

물 스트레스 지역에서 비침습적 클램프온 유량계의 급속한 개보수 수요 증가

비침습적 클램프온 장치를 통해 유틸리티 사업자는 프리스트레스트 콘크리트 원통형 파이프라인을 절단하지 않고도 계측 장비를 설치할 수 있습니다. 이를 통해 신흥 경제국에서 처리된 물 손실의 20-30%를 차지하는 누수 지점을 찾아내어 치명적인 파손의 위험을 줄입니다. 지자체 프로젝트에서는 몇 주 만에 수백 개의 계량기를 설치할 수 있으며, 구역별 계량 영역 분석을 통해 압력을 최적화하고 무수익 수량을 줄일 수 있습니다.

기존 차압식/터빈식 계량기 대비 높은 초기 설비 투자 비용

초음파식 설치비용은 시운전과 교육을 포함하면 차압식 대체품에 비해 3-5배 정도 높으며, 수명주기 운영비용 절감 효과에도 불구하고 소규모 지자체의 예산으로서는 부담이 될 수 있습니다. 자금 조달의 제약으로 인해 개발도상국에서는 첨단 진단 기능의 도입이 늦어지고 있으며, 기능성이 첨단 진단 기능보다 우선시되는 경향이 있습니다.

부문 분석

2025년 기준 초음파 유량계 시장 점유율에서 인라인 설계가 65.60%를 차지했습니다. 반면, 클램프온 유닛은 8.18%의 CAGR을 기록했으며, 이는 아시아태평양 유틸리티의 리노베이션 프로그램 확장을 반영합니다. 클램프온 부문은 -200°C에서 +630°C의 공정 온도 범위를 견딜 수 있는 WaveInjector 트랜스듀서 하우징의 혜택을 누릴 수 있습니다. 비침습적 장치는 생산 중단을 피하기 위해 산업 플랜트에서 긴급 누출 조사 및 임시 감사에 대한 수요가 가속화되고 있습니다.

2세대 커플링 패드와 자동 설치 리그를 통해 설치 시간을 절반으로 줄이고, 정지 비용이 계측기 가격보다 높은 환경에서 경제적 우위를 강화했습니다. 스마트워터 프로그램을 시범 도입한 유틸리티 사업자들은 클램프온 설치 후 수개월 내에 누수율 감소를 확인했으며, 이는 투자 회수 기간을 단축하고 자본 제약 환경 하에서 초음파 유량계 시장이 더욱 확산될 수 있도록 돕고 있습니다.

2025년에는 전파식 유량계가 82.10%의 점유율을 차지했으며, 2031년까지 CAGR 8.36%로 확대될 것으로 전망됩니다. 음속 측정 능력은 수소가스 혼합에 필요한 조성 모니터링을 지원하며, 탈탄소화가 진행됨에 따라 가치 제안을 향상시키고 있습니다. 머신러닝을 통한 프로파일 보정을 통해 변동하는 온도 환경에서도 ±0.5%의 정확도를 유지합니다.

반면, 도플러식 장비는 정확도가 낮기 때문에 오염된 유체 환경에서의 사용으로 제한됩니다. 단일 기법의 한계가 두드러지는 다상 흐름 파이프라인을 위해 도풀러와 전파시간 측정을 결합한 하이브리드 플랫폼이 등장하고 있습니다. 원리를 전환할 수 있는 모듈식 전자장치를 통해 운영자는 단일 송신기 제품군으로 표준화를 실현할 수 있으며, 용도가 다양해짐에 따라 재고를 줄일 수 있습니다.

지역별 분석

아시아태평양은 중국의 일대일로 파이프라인 프로젝트와 고정밀 계측을 의무화하는 인도의 스마트 시티 구상에 힘입어 2025년 세계 매출의 41.25%를 차지했습니다. 일본과 한국 현지 업체들은 IoT 대응 트랜스미터와 온도 보상형 트랜스듀서를 통해 경쟁력을 강화하고, 지역 공급 안정성을 높이고 있습니다. 각국 정부는 폐수 재이용을 위한 인프라 부양책에 초점을 맞추고 있으며, 이는 지자체 프로젝트에서 초음파 유량계 도입을 촉진하고 있습니다.

유럽에서는 EU 정책으로 인한 수소 대응 파이프라인 개조 및 계량기 지침의 엄격한 준수가 추진되면서 10.11%의 CAGR이 예상됩니다. 독일의 한 화학 산업 거점에서는 톤당 에너지 소비를 줄이기 위해 공정 강화 프로그램에 초음파 유량계를 도입했습니다. 네덜란드에서는 소유권급 질량 조정이 필요한 수소 충전소 시범사업에 박차를 가하고 있습니다. 지역 공급업체는 수직적 통합을 활용하고, 계측 장비와 클라우드 분석을 결합하여 엄격한 지속가능성 감사에 대응하고 있습니다.

북미에서는 셰일가스 거래량 측정 업그레이드와 가뭄이 심한 서부 지역의 상수도 누수 방지 프로젝트를 바탕으로 한 자릿수 성장세를 유지하고 있습니다. 연방 인프라 법안은 노후화된 연성철관에 클램프온식 계량기를 채택한 스마트 수도 시스템 도입을 보조하고 있습니다. 남미 및 중동 및 아프리카는 신흥 수요 지역이지만 DN1000 이상의 공인 교정시설이 한정되어 있어 신규 파이프라인의 인허가가 지연되는 경우가 있습니다. 이에 반해, 공급업체들은 모바일 제공업체와 원격 지원 거점 구축을 통해 서비스 장벽을 완화하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10Ultrasonic flow meters market size in 2026 is estimated at USD 1.63 billion, growing from 2025 value of USD 1.52 billion with 2031 projections showing USD 2.28 billion, growing at 6.98% CAGR over 2026-2031.

The growing deployment of custody-transfer-grade meters in large-diameter gas pipelines, retrofit demand for clamp-on devices in aging water networks, and early-stage investments in hydrogen infrastructure sustain near-double-digit demand across the process industries. Operators favor ultrasonic designs for zero pressure loss, predictive maintenance, and IIoT integration, which reduce lifetime operating expenditure compared with differential-pressure or turbine meters. Adoption accelerates where environmental compliance drives high-accuracy flow control, such as zero-liquid-discharge mandates in chemical processing and leakage-reduction programs in municipal water systems. Competitive differentiation is increasingly centered on edge-AI diagnostics and multi-path redundancy, which maintain +-0.15% repeatability in demanding custody-transfer conditions.

Global Ultrasonic Flow Meters Market Trends and Insights

Accelerated shift to custody-transfer-grade ultrasonic meters in large-diameter gas pipelines

Pipeline operators have begun phasing out turbine meters because ultrasonic units eliminate pressure-drop penalties, reducing compressor energy consumption by up to 15% while offering 20-year lifetimes with minimal maintenance. Multi-path designs now deliver API-compliant accuracy and enable field verification through small-volume provers, limiting downtime for calibration. Adoption is most visible in North American shale gas corridors and Middle Eastern export pipelines, where throughput variability requires wide Reynolds-number tolerance.

Rapid retrofit demand for non-invasive clamp-on meters in water-stress hotspots

Non-invasive clamp-on devices enable utilities to instrument prestressed concrete cylinder pipelines without cutting, thereby mitigating the risk of catastrophic failure while identifying leaks responsible for 20-30% of treated-water losses in emerging economies. Municipal projects can deploy hundreds of meters in weeks, enabling district-metered-area analytics that optimize pressure and drive down non-revenue water.

High initial CAPEX vs. legacy DP/turbine meters

Ultrasonic installations cost three to five times more than differential-pressure alternatives once commissioning and training are included, challenging smaller municipal budgets despite lifecycle OPEX savings. Financing constraints slow the adoption of advanced diagnostics in developing regions, where functionality often takes precedence over advanced diagnostics.

Other drivers and restraints analyzed in the detailed report include:

- Hydrogen-ready ultrasonic designs enable early-mover advantage in energy transition

- Edge-AI self-diagnostics cut OPEX for utilities and boost predictive maintenance adoption

- Accuracy drift in multiphase/slurry service without advanced signal conditioning

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In-line designs accounted for 65.60% of the ultrasonic flow meters market share in 2025. Clamp-on units, however, are projected to register an 8.18% CAGR, reflecting expanding retrofit programs across APAC utilities. The clamp-on segment benefits from WaveInjector transducer housings that can tolerate process ranges of -200 °C to +630 °C. As non-invasive devices avoid production outages, demand accelerates for emergency leak surveys and temporary audits in industrial plants.

Second-generation coupling pads and automated mounting rigs halve installation time, reinforcing economic advantages where shutdown costs exceed instrument price. Utilities piloting smart-water programs confirm leak-rate reductions within months of clamp-on deployments, supporting rapid investment payback and further penetration of the ultrasonic flow meters market in constrained capital environments.

Transit-time units held an 82.10% share in 2025 and are set to grow at an 8.36% CAGR through 2031. Their capability to capture sonic velocity supports composition monitoring needed for hydrogen-gas blends, elevating their value proposition as decarbonization momentum builds. Machine-learning-driven profile correction now sustains +-0.5% accuracy even under variable temperature regimes.

Doppler devices remain confined to dirty-fluid contexts due to their lower precision, while hybrid platforms combining Doppler and transit-time measurements are emerging for multiphase pipelines where shortfalls of single-method approaches are apparent. Modular electronics that switch between principles enable operators to standardize on one transmitter family, reducing inventory even as application diversity expands.

The Ultrasonic Flow Meters Market Report is Segmented by Mounting Method (Clamp-On, In-Line), Measurement Technology (Transit-Time, Doppler, Hybrid/Multipath), End-User Industry (Oil and Gas, Water and Wastewater, Chemical and Petrochemical, Industrial, Other Industries), Number of Paths (Single-Path, Multi-Path), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 41.25% of global revenue in 2025, fueled by China's Belt and Road pipeline projects and India's Smart Cities Mission that mandates high-accuracy metering. Local producers in Japan and South Korea enhance competitiveness through IoT-ready transmitters and temperature-compensating transducers, reinforcing regional supply security. Governments channel infrastructure stimulus toward wastewater reuse, thereby elevating the adoption of ultrasonic flow meters in municipal projects.

Europe is projected to expand at a 10.11% CAGR as EU policy drives hydrogen-ready pipeline retrofits and rigorous conformance to the Measuring Instruments Directive. Germany's chemical heartland embeds ultrasonic meters within process intensification programs to reduce energy consumption per ton of output, while the Netherlands accelerates hydrogen injection pilots that require custody-grade mass reconciliation. Regional suppliers leverage vertical integration, combining instruments with cloud analytics to satisfy stringent sustainability audits.

North America sustains mid-single-digit growth, anchored by shale gas custody-transfer upgrades and water utility leakage projects in drought-prone western states. Federal infrastructure bills subsidize smart-water deployments that favor clamp-on meters for aging ductile-iron mains. South America and the Middle East-Africa represent emerging demand pockets, though limited accredited calibration facilities above DN 1000 slow some greenfield pipeline approvals. Suppliers counter by deploying mobile providers and remote support hubs, easing service barriers.

- Baker Hughes Company

- Endress+Hauser Group Services AG

- Fuji Electric Co., Ltd.

- Honeywell International Inc.

- Emerson Electric Co.

- ABB Ltd.

- Aichi Tokei Denki Co., Ltd.

- Apator SA

- Arad Group

- Badger Meter Inc.

- Bronkhorst High-Tech BV

- Diehl Metering GmbH

- FLEXIM Instruments GmbH

- Itron Inc.

- Kamstrup A/S

- KOBOLD Messring GmbH

- KROHNE Group

- Landis+Gyr AG

- Mueller Systems LLC

- Neptune Technology Group Inc.

- Omega Engineering Inc.

- SICK AG

- Siemens AG

- Sensus USA Inc.

- WEIHAI Ploumeter Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Accelerated shift to custody-transfer-grade ultrasonic meters in large-diameter gas pipelines

- 4.3.2 Rapid retrofit demand for non-invasive clamp-on meters in water-stress hotspots

- 4.3.3 Hydrogen-ready ultrasonic designs enable early-mover advantage in energy transition

- 4.3.4 Edge-AI self-diagnostics cut OPEX for utilities and boost predictive maintenance adoption

- 4.3.5 Mandatory zero-liquid-discharge policies push high-accuracy flow control in chemicals

- 4.3.6 OEM-embedded ultrasonic transmitters in smart pumps expand addressable OEM market

- 4.4 Market Restraints

- 4.4.1 High initial CAPEX vs. legacy DP/turbine meters

- 4.4.2 Accuracy drift in multiphase / slurry service without advanced signal conditioning

- 4.4.3 Scarcity of accredited calibration labs above DN 1000 in emerging regions

- 4.4.4 Cyber-security concerns over IIoT-connected meters in critical infrastructure

- 4.5 Industry Supply Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook (IoT-enabled, hydrogen-ready, AI)

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mounting Method

- 5.1.1 Clamp-on

- 5.1.2 In-line

- 5.2 By Measurement Technology

- 5.2.1 Transit-time

- 5.2.2 Doppler

- 5.2.3 Hybrid / Multipath

- 5.3 By End-User Industry

- 5.3.1 Oil and Gas

- 5.3.2 Water and Wastewater

- 5.3.3 Chemical and Petrochemical

- 5.3.4 Industrial (F&B, Aerospace, Automotive)

- 5.3.5 Other Industries (Life Sciences, Mining and Metals)

- 5.4 By Number of Paths

- 5.4.1 Single-path

- 5.4.2 Multi-path (3-Path, 4-Path, 5+-Path)

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Baker Hughes Company

- 6.4.2 Endress+Hauser Group Services AG

- 6.4.3 Fuji Electric Co., Ltd.

- 6.4.4 Honeywell International Inc.

- 6.4.5 Emerson Electric Co.

- 6.4.6 ABB Ltd.

- 6.4.7 Aichi Tokei Denki Co., Ltd.

- 6.4.8 Apator SA

- 6.4.9 Arad Group

- 6.4.10 Badger Meter Inc.

- 6.4.11 Bronkhorst High-Tech BV

- 6.4.12 Diehl Metering GmbH

- 6.4.13 FLEXIM Instruments GmbH

- 6.4.14 Itron Inc.

- 6.4.15 Kamstrup A/S

- 6.4.16 KOBOLD Messring GmbH

- 6.4.17 KROHNE Group

- 6.4.18 Landis+Gyr AG

- 6.4.19 Mueller Systems LLC

- 6.4.20 Neptune Technology Group Inc.

- 6.4.21 Omega Engineering Inc.

- 6.4.22 SICK AG

- 6.4.23 Siemens AG

- 6.4.24 Sensus USA Inc.

- 6.4.25 WEIHAI Ploumeter Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment