|

시장보고서

상품코드

1940717

수의학 안과 치료 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Veterinary Eye Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

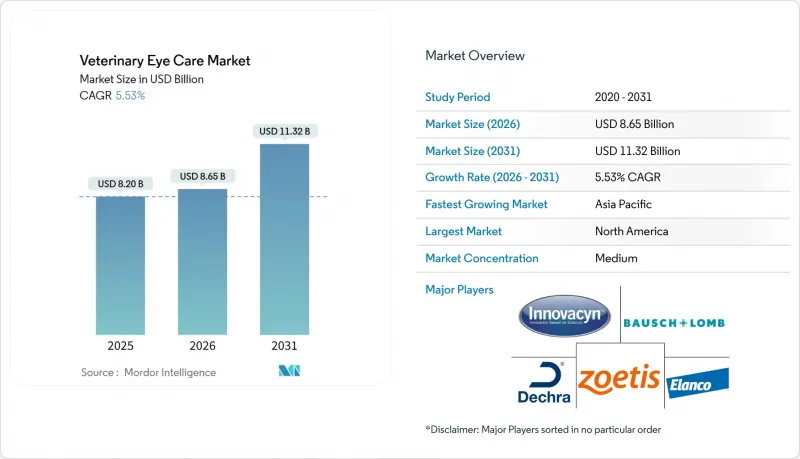

2026년 수의학 안과 치료 시장 규모는 85억 5,000만 달러로 추정되며, 2025년 82억 8,000만 달러에서 성장이 전망됩니다.

2031년 예측치는 100억 7,000만 달러로 2026-2031년 연평균 복합 성장률(CAGR) 3.31%를 나타낼 것으로 예측됩니다.

반려동물 양육 인구 증가, 고급 치료에 대한 지출 의향 증가, 국소 안과용 의약품의 유형 확대 등이 수의학 안과 치료 시장의 꾸준한 성장세를 뒷받침하고 있습니다. 안구건조증(KCS), 녹내장 등 안질환 발생률 증가가 수요를 견인하는 한편, AI를 활용한 영상진단 기술과 줄기세포 치료의 발전으로 진단 및 치료의 적용 범위가 확대되고 있습니다. 수익 기여도에서는 북미가 1위이지만, 도시 경제권에서 반려동물의 인간화가 진행되고 있는 아시아태평양이 가장 빠른 성장세를 보이고 있습니다. 특정 기업이 모든 치료 분야를 독점하고 있지 않기 때문에 경쟁의 강도는 중간 정도이지만, 주요 기업들은 의약품, 의료기기, 데이터를 통합하는 전략을 통해 참여를 강화하고 있습니다.

세계 수의학 안과 치료 시장 동향과 인사이트

반려동물 사육 수 증가와 고급 수의학에 대한 지출 확대

세계적으로 반려동물의 인간화로 인해 치료에 대한 기대와 지출이 증가하고 있습니다. 평균 안과 수술 비용은 개 1,100달러, 고양이 안과 치료는 700-2,000달러에 달할 전망입니다. 아시아태평양의 밀레니얼 및 Z세대 반려동물 보호자들로 인해 아시아태평양의 반려동물 의료비 지출은 매년 10%씩 성장하고 있으며, 수의 안과 시장은 프리미엄 진단 및 재생의료 분야로 이동하고 있습니다. 원격 선별검사, 웨어러블 모니터, AI 스크리닝 도구는 예방적 워크플로우를 통합하고 조기 의뢰를 촉진하여 서비스량을 증가시키고 있습니다. 이에 따라 병원은 안과 부문을 확장하고, 공급업체는 선택적 지출을 확보하기 위해 반려동물용 의약품 라인을 확장하고 있습니다.

안질환(건성각결막염, 궤양, 녹내장) 증가 추세

개 품종 유전적 요인, 반려동물의 수명 연장, 환경 자극 물질로 인해 질병 발생 건수가 증가하고 있습니다. 건성각막증(KCS)은 현재 전 세계 개 22마리 중 1마리가 앓고 있는 질환입니다. 녹내장은 실명 사례의 8.47%를 차지하며, 외상이나 포도막염의 합병증에 이어 발병하는 경우가 많습니다. 각막궤양은 전방각막실질천공술로 좋은 치유율을 보이며, 표준적인 데브리드만(병변조직 제거)의 치유율 50%에 비해 80%의 치유율이 확인되고 있습니다. 전 세계적으로 공인된 수의 안과 전문의가 600명 미만으로 부족하여 의뢰 환자의 대기 시간이 길어지고 있습니다. 질병에 대한 인식 제고와 미충족 수요는 제약회사나 수술 장비 공급업체에게 예측 가능한 수익원이 될 수 있습니다.

첨단 안과 장비 및 수술의 높은 비용

초음파 유화흡입기, 망막전위도 시스템, OCT 스캐너는 진료소당 10만 달러 이상의 투자 부담이 추가됩니다. 백내장 수술은 고양이의 경우 한 눈당 2,500-5,500달러, 개의 경우 1,000-3,000달러로 고가여서 가격에 민감한 보호자들의 진료가 제한되고 있습니다. 신흥 시장 지역의 진료소에서는 복잡한 케이스를 도시 전문병원에 의뢰하는 경우가 많아 수술 건수가 도시에 집중되어 지역으로의 확산이 막혀있는 실정입니다.

부문 분석

2025년 매출의 76.83%는 제품 부문이 차지할 것으로 예상되며, 안과용 의약품, 진단기기, 수술기구, 안구 내 임플란트가 핵심입니다. 검진부터 수술까지 모든 안과 진료가 소모품과 약품에 의존하고 있기 때문에 이러한 우위를 점할 수 있습니다. AI가 탑재된 영상진단기기와 1회용 항생제 및 스테로이드 점안제는 제품 회전주기를 연장합니다. 한편, 서비스 부문은 CAGR 4.02%로 가장 빠르게 성장하고 있습니다. 전문 수술, 진단영상검사 확대, 원격진료 도입으로 회당 평균 수익이 증가하고 있으며, 구독형 기술을 도입하는 병원의 설비투자 장벽이 완화되고 있습니다. 클리닉에서는 수술 후 검진을 패키지로 묶어 각 시술의 수익화를 더욱 촉진하고 있습니다. 저침습 기술이 보급됨에 따라 일회용 수술 팩과 안구 내 렌즈에 대한 수요가 꾸준히 증가하여 전체 수의 안과 시장에서의 교차 판매 시너지 효과가 강화되고 있습니다.

서비스 분야의 성장은 백내장 교정의 보급에 기인하며, 치료를 받은 동물의 최대 80%가 30개월 이상 기능적 시력을 회복하고 있습니다. 병원 네트워크는 AI 영상 워크플로우와 연계된 통합 수술 전후 케어 라인으로 대응하고 있으며, 인력을 크게 늘리지 않고도 처리 능력을 향상시키고 있습니다. 원격 안과 플랫폼은 경증 환자를 선별하고 수술이 필요한 환자를 지역 센터로 안내하여 지역별로 용량 병목현상을 해소하고 병원 파이프라인에 안정적으로 의뢰할 수 있도록 돕고 있습니다.

개 시장 규모는 2025년 매출의 51.76%를 차지할 것으로 예상되며, 이는 선진국과 신흥국을 막론하고 가장 보편적인 반려동물로서의 지위를 반영합니다. 단두종안증후군, 유전성 백내장 등의 유전적 소인으로 인해 반려견의 발병 건수는 높은 수준을 유지하고 있으며, KCS(각막각막염증후군) 및 녹내장 치료제 수요를 안정적으로 창출하고 있습니다. 말의 하위 부문은 절대값은 작지만 3.34%의 연평균 복합 성장률(CAGR)을 보이고 있습니다. 경기용 말의 소유자는 경기용 말의 가치를 유지하기 위해 고도의 수술과 영상진단에 투자합니다. 진료소에서는 말 전용 마취 프로토콜과 대형 영상진단 장비를 정비하여 부가서비스 수익 기회를 창출하고 있습니다. 고양이는 안정적인 2차적 틈새 시장을 차지하고 있으며, 호산구성 각막염에 대한 맞춤형 줄기세포 치료제 수요가 증가하고 있습니다.

품종 특화형 유전자 검사 키트는 예방 경로를 확장하고, 육종가의 선택에 정보를 제공함으로써 미래의 안질환 발생률에 직접적인 영향을 미칩니다. 관련 전문 보험사는 고가의 시술 비용을 상쇄하는 말용 시력 특약을 설계하여 경기마 마구간에서 초음파 유화흡입술과 녹내장 판막 임플란트의 조기 도입을 촉진하고 있습니다. 종합적으로 볼 때, 확대되고 있는 품목별 특화 파이프라인은 수의 안과 시장에서 수익의 다양성을 균형 있게 유지하고 있습니다.

지역별 분석

북미는 2025년 매출의 37.88%를 차지할 것으로 예상되며, 동물 한 마리당 높은 반려동물 의료비 지출과 탄탄한 보험 보급률이 이를 뒷받침하고 있습니다. 미국 FDA 동물용의약품센터는 안전성-유효성 심사를 2-4년에 걸쳐 진행하며, 과학적 엄격함으로 이해관계자들의 합의를 도출하는 한편, 시판 주기를 연장하고 있습니다. 기업들은 AI 업그레이드와 의료기기 펌웨어의 단계적 업데이트를 신속하게 시장에 출시하여 새로운 분자가 규제 당국의 승인을 받을 때까지 관여를 지속하고 있습니다. 캘리포니아, 텍사스, 온타리오의 학술 클러스터에는 저명한 안과 레지던트 프로그램이 존재하며, 수술 기술의 혁신을 빠르게 보급하고 있습니다.

아시아태평양은 반려동물 수의 급증, 가처분 소득 증가, 가족 가구보다 1인 가구를 선호하는 인구 통계학적 변화로 인해 3.92%의 연평균 복합 성장률(CAGR)로 가장 높은 성장세를 보이고 있습니다. 중국의 소동물 진료소는 5년 만에 두 배로 늘어났으며, 광저우에만 150개 시설에 약 400명의 수의사가 배치되어 있습니다. 지역 스타트업은 반려동물 소매점 내에 모바일 원격진료 키오스크를 설치하여 1차 검진 진입장벽을 낮추고, 사례를 도시형 병원으로 유도하고 있습니다. 인도와 태국의 정부 산하 수의과대학에서는 안과 전문 과정의 정원을 확대하여 전문의 부족을 점차 완화하고 있습니다. 이러한 인프라 구축과 소비자 수용성 양 측면의 성장이 맞물리면서 이 지역의 동물용 안과 시장은 수혜를 받고 있습니다.

유럽은 성숙한 2차 의료 시장으로, 일반 진료와 유럽수의안과학회(ECVO) 인증 전문의들을 연결하는 의뢰 문화가 정착되어 있습니다. 독일, 네덜란드, 영국의 레지던트 프로그램이 새로운 전문의를 양성하고 있지만, 퇴직자 수를 완전히 보충하지 못해 원격진료에 대한 수요는 여전히 높은 수준을 유지하고 있습니다. 남미와 중동 및 아프리카는 신흥 시장으로 비용 장벽과 보험의 한계로 인해 보급에 어려움을 겪고 있지만, 국경을 넘나드는 원격 안과 진료가 접근성 격차를 해소하고 있습니다. 다국적 제약사들은 단계적 가격 전략과 기부 프로그램을 시범적으로 도입하여 의약품 보급의 기반을 마련하고, 소득 수준 상승에 따른 장기적인 판매량 증가를 예상하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10Veterinary eye care market size in 2026 is estimated at USD 8.55 billion, growing from 2025 value of USD 8.28 billion with 2031 projections showing USD 10.07 billion, growing at 3.31% CAGR over 2026-2031.

Rising pet ownership, growing willingness to spend on premium treatments, and expanding portfolios of topical ophthalmic drugs position the veterinary eye care market for steady performance. Demand is buoyed by a higher incidence of ocular disorders such as keratoconjunctivitis sicca (KCS) and glaucoma, while breakthroughs in AI-enabled imaging and stem-cell therapies widen diagnostic and therapeutic reach. North America leads revenue contribution, yet Asia-Pacific delivers the fastest growth as pet humanization accelerates in urban economies. Competitive intensity remains moderate because no single company dominates every therapeutic class, though large players leverage integrated drug-device-data strategies to deepen engagement.

Global Veterinary Eye Care Market Trends and Insights

Growing Pet Ownership & Spend on Advanced Vet Care

Global pet humanization lifts treatment expectations and spending. Average ocular procedure outlays reach USD 1,100 for canine surgeries and USD 700-2,000 for feline eye treatments. Millennial and Gen Z owners in Asia-Pacific spur 10% yearly growth in regional pet health outlays, pushing the veterinary eye care market toward premium diagnostics and regenerative modalities. Tele-triage, wearable monitors, and AI screening tools integrate preventive workflows and encourage earlier referral, increasing service volumes. Hospitals respond by widening ophthalmic wings, and suppliers expand companion-animal drug lines to capture discretionary spend.

Rising Prevalence of Ocular Disorders (KCS, Ulcers, Glaucoma)

Breed genetics, longer pet lifespans, and environmental irritants lift disease caseloads. KCS now affects 1 in 22 dogs worldwide. Glaucoma contributes 8.47% of blindness presentations and often follows trauma or uveitis complications. Corneal ulcers respond better to anterior stromal puncture, which secures 80% healing, compared with 50% for standard debridement. The shortage of fewer than 600 board-certified veterinary ophthalmologists globally intensifies referral wait times. Higher disease visibility and unmet need translate into predictable revenue streams for drug manufacturers and surgical device suppliers.

High Cost of Advanced Ocular Equipment & Surgery

Phacoemulsification units, electroretinogram systems, and OCT scanners add investment burdens topping USD 100,000 per practice. Cataract removal runs USD 2,500-5,500 per eye in cats and USD 1,000-3,000 in dogs, limiting uptake among price-sensitive owners. Emerging-market clinics often refer complex cases to urban centers, concentrating procedure volumes and dampening regional diffusion.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Portfolio of Topical Ophthalmic Drugs & Ointments

- AI-Enabled Imaging & Tele-Ophthalmology Adoption

- Shortage of Board-Certified Veterinary Ophthalmologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Products delivered 76.83% of 2025 revenue, anchored by ophthalmic drugs, diagnostic devices, surgical instruments, and ocular implants. This dominance arises because every ophthalmic encounter-screening or surgery-relies on consumables and medications. AI-infused imaging devices and single-dose antibiotic-steroid drops extend product turnover cycles. The services arm, however, is the fastest climber at a 4.02% CAGR. Specialty surgeries, expanded diagnostic imaging, and virtual consultations lift average revenue per visit and soften the capital-equipment hurdle for clinics adopting subscription-based technology. Clinics package bundled postoperative checkups, further monetizing each procedure. As minimally invasive techniques propagate, disposable surgical packs and implantable lenses grow steadily, reinforcing cross-selling synergies across the veterinary eye care market.

Services momentum stems from widening cataract correction, which restores functional sight in up to 80% of treated animals over 30 months. Hospital networks respond with integrated perioperative care lines linked to AI imaging workflows, raising throughput without heavy manpower additions. Tele-ophthalmology platforms triage minor issues and route surgical candidates to regional centers, flattening geography-based capacity bottlenecks and prompting steady referrals into hospital pipelines.

Dogs captured 51.76% of 2025 revenue, consistent with their status as the most commonly owned companion animal in developed and emerging economies alike. Genetic predispositions, such as brachycephalic ocular syndrome and inherited cataracts, keep canine caseloads high, creating predictable drug volumes for KCS and glaucoma. The equine subsegment, although smaller in absolute terms, exhibits a 3.34% CAGR. Performance horse owners finance advanced surgeries and diagnostic imaging to preserve athletic value. Clinics tailor equine-specific anesthesia protocols and larger-format imaging accessories, opening bolt-on service revenues. Cats occupy a steady secondary niche with rising demand for tailored stem-cell therapies addressing eosinophilic keratitis.

Breed-targeted genetic testing kits expand preventive pathways and inform breeders' selections, directly influencing future ocular disease incidence. Allied specialty insurers design equine vision riders to offset high procedure costs, promoting early adoption of phacoemulsification and glaucoma valve implants in performance stables. Collectively, widening species-specific pipelines balance revenue diversity within the veterinary eye care market.

The Veterinary Eye Care Market Report is Segmented by Type (Eye Care Products and Eye Care Services), Indication (Ocular Surface Disorders, Glaucoma, Cataract, Infectious Diseases, and Other Indications), Application (Dog, Cat, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Report Offers the Value (in USD) for the Above Segments.

Geography Analysis

North America contributed 37.88% of 2025 revenue, underpinned by high pet healthcare outlay per animal and robust insurance penetration. The U.S. FDA Center for Veterinary Medicine oversees safety and efficacy reviews that take 2-4 years, aligning stakeholders on scientific rigor but lengthening launch cycles. Companies counterbalance by rolling AI upgrades and incremental device firmware to market within shorter notice periods, sustaining engagement until new molecules clear regulators. Academic clusters in California, Texas, and Ontario host renowned ophthalmology residencies, facilitating rapid dissemination of procedural innovations.

Asia-Pacific delivers the strongest growth at 3.92% CAGR on surging pet numbers, rising disposable income, and shifting demographics favoring single-person households over families. China's small-animal clinics have doubled within five years; Guangzhou alone fields about 400 veterinarians across 150 sites. Regional startups deploy mobile tele-consult kiosks inside pet retail outlets, lowering entry barriers for primary screening and funneling cases to urban hospitals. Government veterinary colleges in India and Thailand expand postgraduate ophthalmology seats, gradually easing specialist scarcity. The region's veterinary eye care market thus benefits from intersectional growth in both infrastructure and consumer readiness.

Europe comprises a mature secondary market with an entrenched referral culture linking general practices to ECVO diplomates. Residency programs across Germany, the Netherlands, and the United Kingdom collectively train new specialists but cannot fully offset retirements, keeping demand for tele-consults high. South America and Middle East & Africa represent emerging frontiers where cost hurdles and limited insurance stifle adoption, yet cross-border tele-ophthalmology fills access gaps. Multinational pharmaceutical companies pilot tiered-pricing strategies and donation programs to seed drug uptake, positioning for long-term volume gains as income levels rise.

- Zoetis

- Merck & Co., Inc. (MSD Animal Health)

- Dechra Pharmaceuticals

- Bausch + Lomb Corporation

- Domes Pharma

- I-Med Animal Health

- Vetoquinol S.A.

- Santicare LLC

- Innovacyn

- Ceva Sante Animale S.A.

- Epicur Pharma

- Neogen

- Tarsus Pharmaceuticals Inc.

- Topcon

- Covetrus

- Disop, S.A.

- OCuSOFT Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing pet ownership & spend on advanced vet care

- 4.2.2 Rising prevalence of ocular disorders (KCS, ulcers, glaucoma)

- 4.2.3 Expanding portfolio of topical ophthalmic drugs & ointments

- 4.2.4 Demand for minimally-invasive ophthalmic surgeries

- 4.2.5 AI-enabled imaging & tele-ophthalmology adoption

- 4.2.6 Stem-cell/regenerative therapies for corneal repair

- 4.3 Market Restraints

- 4.3.1 High cost of advanced ocular equipment & surgery

- 4.3.2 Limited insurance reimbursement for vet eye care

- 4.3.3 Stringent regulatory approval timelines for vet drugs

- 4.3.4 Shortage of board-certified veterinary ophthalmologists

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Products and Services

- 5.1.1 Product

- 5.1.1.1 Ophthalmic Drugs

- 5.1.1.2 Surgical Instruments

- 5.1.1.3 Diagnostic Devices & Imaging

- 5.1.1.4 Ocular Implants & Disposables

- 5.1.2 Services

- 5.1.2.1 Ophthalmic Surgical Services

- 5.1.2.2 Diagnostic Imaging Services

- 5.1.2.3 Tele-Ophthalmology & Consultation

- 5.1.2.4 Post-operative Care Services

- 5.1.1 Product

- 5.2 By Animal Type

- 5.2.1 Dogs

- 5.2.2 Cats

- 5.2.3 Horses

- 5.2.4 Other Companion Animals

- 5.3 By Application

- 5.3.1 Keratoconjunctivitis Sicca (Dry Eye)

- 5.3.2 Conjunctivitis

- 5.3.3 Corneal Ulcers & Injuries

- 5.3.4 Glaucoma

- 5.3.5 Uveitis & Retinal Disorders

- 5.3.6 Others

- 5.4 By End-user

- 5.4.1 Veterinary Hospitals

- 5.4.2 Veterinary Clinics

- 5.4.3 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Zoetis Inc.

- 6.3.2 Merck & Co., Inc. (MSD Animal Health)

- 6.3.3 Dechra Pharmaceuticals PLC

- 6.3.4 Bausch + Lomb Corporation

- 6.3.5 Domes Pharma

- 6.3.6 I-Med Animal Health

- 6.3.7 Vetoquinol S.A.

- 6.3.8 Santicare LLC

- 6.3.9 Innovacyn Inc.

- 6.3.10 Ceva Sante Animale S.A.

- 6.3.11 Epicur Pharma

- 6.3.12 Neogen Corporation

- 6.3.13 Tarsus Pharmaceuticals Inc.

- 6.3.14 Topcon Corporation

- 6.3.15 Covetrus, Inc.

- 6.3.16 Disop, S.A.

- 6.3.17 OCuSOFT Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment