|

시장보고서

상품코드

1940725

영국의 산업 자동화 시스템 통합사업자 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United Kingdom Industrial Automation System Integrator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

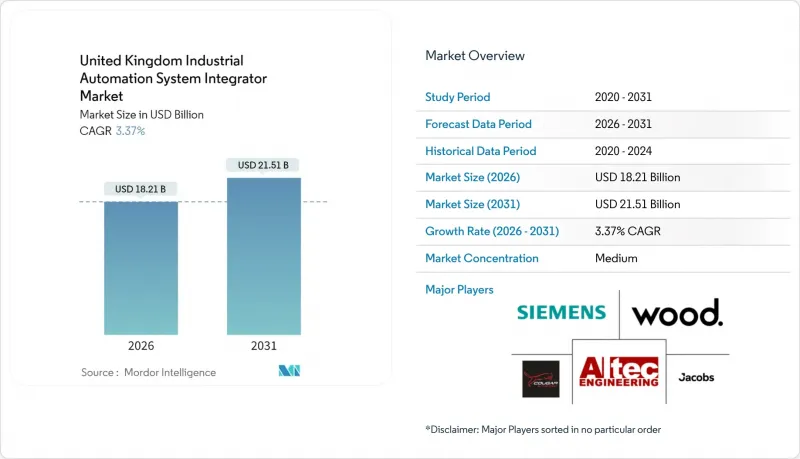

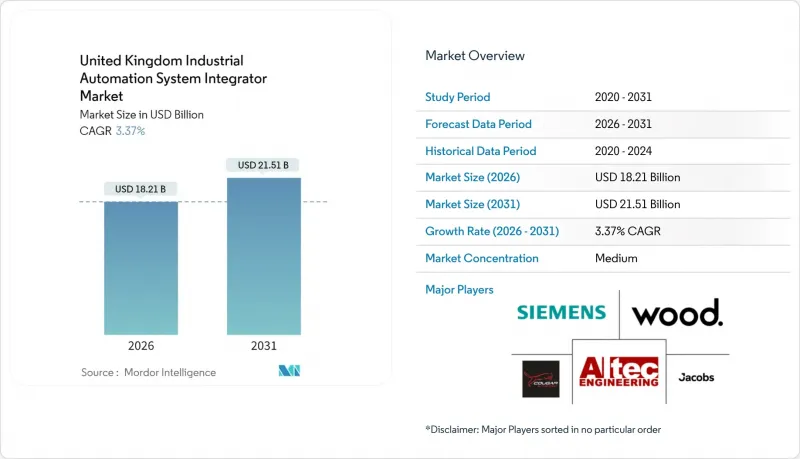

영국의 산업 자동화 시스템 통합사업자 시장 규모는 2025년 176억 2,000만 달러에서 2026년 182억 1,000만 달러로 성장하고, 2031년에는 215억 1,000만 달러에 달할 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR)은 3.37%를 나타낼 것으로 예측됩니다.

이러한 확대는 정부 지원 디지털화 프로그램, 브렉시트 관련 인력 부족으로 인한 생산성 중시 경향 강화, 그리고 개별 산업 및 공정 산업 전반에서 인더스트리 4.0 플랫폼으로의 전환 가속화에 기인합니다. 제조업체들은 수출 의존도가 높은 경제 환경에서 공장 전체의 연결성, 클라우드 분석, 원격 지원을 탄력성(resilience) 구축의 가장 빠른 경로로 인식하고 있습니다. 투자 모멘텀은 디지털 대응력 평가를 위한 'Made Smarter' 보조금을 이용할 수 있는 중견기업에서 가장 강력하게 나타나고 있으며, 대기업은 팬데믹 이후 환경에서 수출 점유율을 지키기 위해 다년간의 리노베이션 일정을 앞당기고 있습니다. 정책 추진과 민간 자본이 결합하여 거시 경제의 혼란 속에서도 자동화 프로젝트 파이프라인을 건전하게 유지하고, 자동차 및 식품 가공의 조달 주기에 대한 시장의 역사적 의존도를 완화하고 있습니다.

영국의 산업자동화 시스템 통합사업자 시장 동향과 인사이트

디지털 전환과 인더스트리 4.0의 도입

제조업체들은 고립된 자동화 아일랜드에서 운영 데이터와 기업 데이터를 통합한 전체 플랜트 통합 업그레이드로 전환하고 있습니다. 국가 차원에서 진행되는 'Made Smarter' 프로그램은 2024년까지 1,600만 파운드(2,030만 달러)를 투입해 1,000개 공장에 진단, 도입 로드맵, 인력 양성 지원을 제공합니다. 기업은 공통 데이터 모델과 안전한 클라우드 게이트웨이를 채택하여 현장 센서를 ERP 시스템에 직접 연결할 수 있습니다. 특히 중소기업이 큰 혜택을 받고 있습니다. 프로그램 어드바이저가 벤더 선정과 표준 준수의 효율성을 높이기 위함입니다. 기계 제조업체들은 현재 ISO 23247을 준수하는 사이버 보안 대응 템플릿을 사전 로드하여 엔지니어링 주기를 단축하고 다양한 기존 설비 사이트 내에서 상호 운용성을 보장하고 있습니다. 더 많은 공장이 디지털 성숙도에 도달함에 따라 통합업체는 PLC 교체, SCADA 혁신, 관리형 분석을 단일 서비스 패키지로 통합하는 다중 사이트 계약을 체결하고 있습니다.

영국 내 노동력 부족으로 인한 생산성 향상에 대한 수요 증가

영국 데이터에 따르면, 2024년 공장 공석이 12만 4,000개에 달하고, 임금 상승률이 6%에 육박하면서 자동 검사, 로봇 팔레타이징, 예측 유지보수로의 전환이 빠르게 진행되고 있습니다. 이를 통해 초과근무 비용을 절감할 수 있습니다. 재무 모델에서 현재 자동화 투자 회수 기간은 18-24개월로 추정되며, 브렉시트 이전 일반적인 기간인 5년과 비교하면 크게 단축된 수치입니다. 물류 사업자들도 이러한 추세에 힘을 보태고 있으며, 풀필먼트 센터의 자율 이동 로봇은 계절적 인력 감소 시에도 안정적인 생산량을 유지할 수 있습니다. 기능협의회는 수작업 중심의 작업장이 아닌 로봇군을 감독하는 관리직으로 현직자를 재교육하고 있습니다. 인티그레이터는 가동률 목표를 보장하는 서비스 계약을 체결하고, 과부하가 걸린 고객을 대신해 인력 확보 리스크를 흡수하고 있습니다.

높은 초기 설비 투자 및 통합 비용

프로젝트 감사에서 레거시 자산 매핑을 통해 문서화되지 않은 코드, 구식 필드버스, 비표준 모터 제어를 발견하여 평균 30%의 예산 초과가 발생합니다. 브렉시트 이후 환율 변동으로 수입 하드웨어 가격이 상승하는 반면, 국내 공급업체들은 소량 생산에 어려움을 겪으며 단가가 고공행진하고 있습니다. 인티그레이터는 마일스톤별로 자금을 조달하는 서비스 패키지를 제공하고, 현금 흐름과 실현된 이익을 연동하여 제공합니다. 그러나 많은 중소기업들이 완전한 디지털화를 미루고 종합적인 업그레이드 대신 센서의 개조를 선택함에 따라 영국 전체 산업 자동화 시스템 통합 업체 시장의 모멘텀이 둔화되고 있습니다.

부문 분석

PLC는 2025년에도 영국의 산업 자동화 시스템 통합사업자 시장 규모에서 32.25%의 점유율을 유지하며, 배치 생산 라인 및 개별 생산 라인의 기본 제어 기반으로서의 역할을 강조하고 있습니다. 로봇 셀과 머신비전을 이용한 피킹 및 검사는 EV 파워트레인 조립 및 최종 공정 포장 수요 증가로 인해 5.45%의 연평균 복합 성장률(CAGR)로 성장을 주도하고 있습니다. 분산 제어 시스템은 화학 및 정제 산업에서 여전히 주류이며, 연속 처리 및 고가용성 아키텍처는 프리미엄 지출을 정당화합니다. SCADA 확장 기능은 실시간 자산 건전성 대시보드를 지원하기 위해 디지털화를 추진하는 유틸리티 분야에서 보급이 진행되고 있습니다.

상호운용성에 대한 압박으로 인해 OEM 업체들은 오픈 API를 공개하는 방향으로 움직이고 있으며, 이를 통해 통합업체들은 PLC, 로봇, 비전, 센서의 각 계층을 하나의 디지털 트윈으로 통합할 수 있습니다. 고객들은 IEC 61508 및 EMC 지침을 준수하는 하드웨어를 선호하여 재승인 주기를 최소화하고 있습니다. 통합 제어 스택은 영국의 산업 자동화 시스템 통합사업자 시장의 성장을 뒷받침하고 있는데, 이는 고객들이 단편적인 패널 변경이 아닌 번들형 업그레이드를 선택하고 있기 때문입니다.

설계 및 엔지니어링 서비스는 2025년 매출의 34.15%를 차지했습니다. 신규 프로젝트에는 시뮬레이션, 위험성 분석, 개념검증 리그가 필요하기 때문입니다. 관리 서비스는 원격 모니터링과 결합하여 5.05%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장세를 보이며 프로젝트 파이프라인을 지속적인 수익원으로 전환하고 고객 평생 가치를 높이고 있습니다. 설치 및 시운전 업무는 여전히 중요하지만, 모듈식 플러그 앤 플레이 하드웨어로 인한 현장 작업의 감소로 그 비중이 줄어드는 추세입니다. 한편, 플랜트 소유주들이 드롭인 I/O 모듈과 클라우드 펌웨어 업데이트를 통해 기존 제어 시스템의 수명을 연장하기 위해 업그레이드 및 리노베이션 수요가 증가하고 있습니다.

엣지 지원 게이트웨이는 암호화된 텔레메트리 데이터를 서비스 제공업체의 분석 센터로 전송하여 베어링의 마모나 신호 드리프트를 고장 전에 감지하여 성과 연동형 계약을 가능하게 합니다. 현재 인티그레이터는 청구 시간이 아닌 처리량 및 폐기물 감소와 연계된 핵심성과지표(KPI)를 협상하여 신뢰를 강화하고 프리미엄 가격 책정을 정당화하고 있습니다. 이러한 서비스 전환은 영국의 산업자동화 시스템 통합사업자 산업을 주기적인 설비투자 변동에서 안정화시키는 지속적인 수익원을 확립하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The United Kingdom industrial automation system integrator market size in 2026 is estimated at USD 18.21 billion, growing from 2025 value of USD 17.62 billion with 2031 projections showing USD 21.51 billion, growing at 3.37% CAGR over 2026-2031.

This expansion arises from government-backed digital programs, Brexit-related labor shortages that sharpen the focus on productivity, and a stepped-up shift to Industry 4.0 platforms across discrete and process industries. Manufacturers view full-plant connectivity, cloud analytics, and remote support as the fastest route to resilience in an export-heavy economy. Investment momentum is strongest among mid-sized firms that now access Made Smarter grants for digital readiness assessments, while large enterprises accelerate multi-year retrofit schedules to protect export share in the post-pandemic environment. The policy push combines with private capital to keep automation pipelines healthy even during macroeconomic turbulence, tempering the market's historical dependence on automotive and food processing procurement cycles.

United Kingdom Industrial Automation System Integrator Market Trends and Insights

Digital Transformation and Industry 4.0 Adoption

Manufacturers have shifted from isolated automation islands to integrated plantwide upgrades that blend operational and enterprise data. The Made Smarter national rollout allocated GBP 16 million (USD 20.3 million) in 2024 to support 1,000 factories with diagnostics, implementation roadmaps, and talent coaching. Firms adopt common data models and secure cloud gateways, allowing shop-floor sensors to link directly to enterprise resource planning suites. Small and medium enterprises benefit most because program advisers streamline vendor selection and standards compliance. Machine builders now preload ISO 23247-aligned, cyber-secure templates, reducing engineering cycles and ensuring interoperability within diverse brownfield sites. As more plants reach digital maturity, integrators win multi-site contracts that bundle PLC replacement, SCADA revamps, and managed analytics into a single service envelope.

Rising Demand for Productivity Amid UK Labor Shortages

UK data shows 124,000 factory vacancies in 2024, and pay inflation near 6% drives a rapid pivot to automated inspection, robotic palletizing, and predictive maintenance, which trims overtime costs. Financial modeling places current automation paybacks at 18-24 months, compared with the five-year horizons that were common before Brexit. Logistics operators reinforce the trend; autonomous mobile robots in fulfillment centers maintain stable output even when seasonal worker pools shrink. Skills councils retrain incumbents for supervisory roles that oversee fleets of robots, rather than manual work centers. Integrators seize service contracts that guarantee uptime targets, absorbing staffing risks on behalf of overstretched customers.

High Initial Capex and Integration Costs

Project audits reveal overruns average 30% because legacy asset mapping uncovers undocumented code, obsolete fieldbuses, and nonstandard motor controls. Currency fluctuations since Brexit have increased the prices of imported hardware, while domestic suppliers struggle with small production runs that keep per-unit costs high. Integrators provide service packages financed over milestones, aligning cash outflows with realized gains. Still, many SMEs defer full digitization, opting for sensor retrofits rather than holistic upgrades, which slows the momentum of the total United Kingdom industrial automation system integrator market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Robotics Uptake in Automotive Re-tooling for EVs

- Network Rail Target 190plus Digital Signaling Rollout

- Scarcity of Skilled Automation Engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PLCs retained a 32.25% share of the United Kingdom industrial automation system integrator market size in 2025, underscoring their role as the default control backbone in batch and discrete lines. Robot cells and machine-vision pick-checks lead the growth slate at a 5.45% CAGR, propelled by EV power-train assembly and end-of-line packaging. Distributed control systems remain dominant in the chemicals and refining industries, where uninterrupted processing and high-availability architectures justify premium spending. SCADA extensions gain traction in utilities undergoing digitization to support real-time asset health dashboards.

Interoperability pressure nudges OEMs to expose open APIs, enabling integrators to blend PLC, robot, vision, and sensor layers into a single digital twin. Customers favor hardware certified to IEC 61508 and EMC directives, minimizing re-approval cycles. The converged control stack underpins the expansion of the United Kingdom industrial automation system integrator market, because customers award bundled upgrades instead of piecemeal panel changes.

Design and engineering services accounted for 34.15% of 2025 revenue, as greenfield projects require simulation, hazard analysis, and proof-of-concept rigs. Managed services, combined with remote monitoring, exhibit the fastest trajectory at a 5.05% CAGR, converting project pipelines into annuities and increasing lifetime customer value. Installation and commissioning remain essential, but they shrink in proportion as modular plug-and-play hardware reduces on-site effort. Upgrades and retrofits increase because plant owners extend the service life of installed controls through drop-in I/O modules and cloud firmware updates.

Edge-enabled gateways stream encrypted telemetry to service-provider analytics centers that detect bearing wear or signal drift ahead of failure, enabling outcome-based contracts. Integrators now negotiate key performance indicators tied to throughput or scrap reduction, rather than hours billed, reinforcing trust and justifying premium pricing. The service shift anchors recurring revenue streams that stabilize the United Kingdom industrial automation system integrator industry against cyclical capex swings.

The UK Industrial Automation System Integrator Market is Segmented by Component (PLC, DCS, and More), Service Type (Design and Engineering, Installation and Commissioning, and More), End-User Industry (Automotive, Food and Beverage, and More), Technology (Industrial Internet of Things (IIoT) Platforms, Artificial Intelligence and Predictive Analytics, and More), and Region. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Wood PLC

- Jacobs U.K. Limited

- Siemens Mobility Limited

- Altec Engineering Limited

- Cougar Automation Limited

- Adsyst Automation Limited

- Au Automation Limited

- Emerson Process Management Limited

- Applied Automation (U.K.) Limited

- Automated Control Solutions Limited

- Cully Automation Limited

- ABB Limited

- Honeywell Control Systems Limited

- Rockwell Automation U.K. Limited

- Schneider Electric Systems U.K. Limited

- Mitsubishi Electric Europe B.V. (U.K. Branch)

- Yokogawa United Kingdom Limited

- Hitachi Rail STS U.K. Limited

- Linbrooke Services Limited

- Adelphi Automation Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital Transformation and Industry 4.0 Adoption

- 4.2.2 Rising Demand for Productivity Amid UK Labor Shortages

- 4.2.3 Accelerated Robotics Uptake in Automotive Re-Tooling for EVs

- 4.2.4 Network Rail's Target 190plus Digital Signaling Rollout

- 4.2.5 Food and Drink "Vanishing-Horizon" Automation Funding

- 4.2.6 Regional 'Smart Machine Hubs' Backed by UK Government

- 4.3 Market Restraints

- 4.3.1 High Initial Capex and Integration Costs

- 4.3.2 Scarcity of Skilled Automation Engineers

- 4.3.3 OEM-Locked Intellectual-Property Barriers in Rail Signaling

- 4.3.4 Fragmented Legacy OT-IT Cybersecurity Standard

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Key Use-cases Across Different Verticals

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Programmable Logic Controllers (PLC)

- 5.1.2 Distributed Control Systems (DCS)

- 5.1.3 Supervisory Control and Data Acquisition (SCADA)

- 5.1.4 Human-Machine Interface (HMI)

- 5.1.5 Industrial Robots and Machine Vision

- 5.1.6 Industrial Sensors and Networks

- 5.2 By Service Type

- 5.2.1 Design and Engineering

- 5.2.2 Installation and Commissioning

- 5.2.3 Maintenance and Support

- 5.2.4 Upgrades and Retrofits

- 5.2.5 Managed Services and Remote Monitoring

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Food and Beverage

- 5.3.3 Pharmaceuticals and Medical Devices

- 5.3.4 Energy and Power

- 5.3.5 Water and Wastewater

- 5.3.6 Metals and Mining

- 5.3.7 Electronics and Semiconductors

- 5.3.8 Oil and Gas

- 5.3.9 Other End-user Industries

- 5.4 By Technology

- 5.4.1 Industrial Internet of Things (IIoT) Platforms

- 5.4.2 Artificial Intelligence and Predictive Analytics

- 5.4.3 Digital Twin and Simulation

- 5.4.4 Edge Computing and 5G Connectivity

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Wood PLC

- 6.4.2 Jacobs U.K. Limited

- 6.4.3 Siemens Mobility Limited

- 6.4.4 Altec Engineering Limited

- 6.4.5 Cougar Automation Limited

- 6.4.6 Adsyst Automation Limited

- 6.4.7 Au Automation Limited

- 6.4.8 Emerson Process Management Limited

- 6.4.9 Applied Automation (U.K.) Limited

- 6.4.10 Automated Control Solutions Limited

- 6.4.11 Cully Automation Limited

- 6.4.12 ABB Limited

- 6.4.13 Honeywell Control Systems Limited

- 6.4.14 Rockwell Automation U.K. Limited

- 6.4.15 Schneider Electric Systems U.K. Limited

- 6.4.16 Mitsubishi Electric Europe B.V. (U.K. Branch)

- 6.4.17 Yokogawa United Kingdom Limited

- 6.4.18 Hitachi Rail STS U.K. Limited

- 6.4.19 Linbrooke Services Limited

- 6.4.20 Adelphi Automation Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment