|

시장보고서

상품코드

1940735

스페인의 전력 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Spain Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

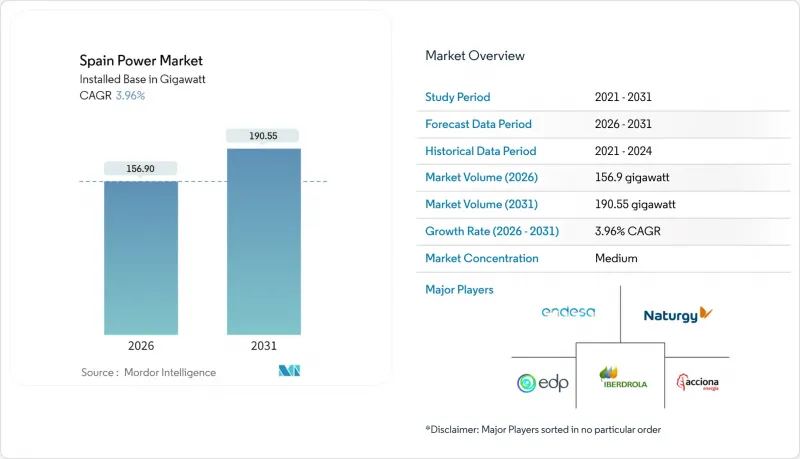

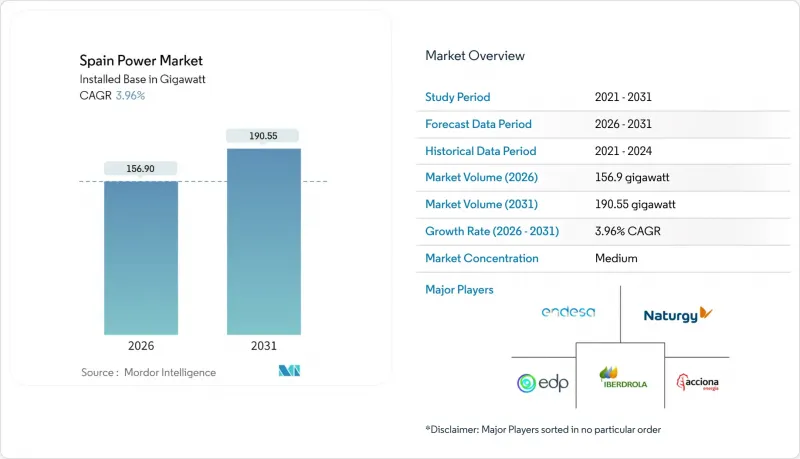

스페인의 전력 시장은 2025년 150.93기가와트에서 2026년에는 156.9기가와트로 성장하고, 2026-2031년 CAGR 3.96%로 성장을 지속하여 2031년까지 190.55기가와트에 이를 것으로 예측되고 있습니다.

이러한 확대는 재생가능에너지의 빠른 도입, EU의 탈탄소화 의무, 그리고 청정 전력 구매 계약에 대한 기업의 강력한 수요에 의해 추진되고 있습니다. 태양광 발전은 2024년 스페인에서 가장 큰 단일 전력 공급원이 되어 스페인의 저탄소 발전으로의 전환을 확고히 했습니다. 초고압 송전회로를 우선시하는 송전망 현대화 계획과 EU 지원의 축전기금으로 간헐적 발전량 연결이 확대되고 있습니다. 한편, 산업 전기화, 전기 이동성 촉진책, 데이터센터 개발은 부하 프로파일을 변화시키고 계통 연계형 재생에너지에 대한 수요를 지속시키고 있습니다. 마지막으로, 원자력 발전의 단계적 폐지 정책의 전환으로 기저부하의 내결함성이 향상되어 송전망의 업그레이드가 따라잡을 때까지 용량 적정성에 대한 우려는 미뤄지고 있습니다.

스페인의 전력 시장 동향 및 분석

가속화되는 계통연계형 태양광 발전 건설

스페인의 태양광 부문은 2024년에 가스 및 풍력을 제치고 스페인에서 가장 큰 전력 공급원이 되는 획기적인 한 해를 맞이했습니다. 당국은 2024년 26,159.2MW의 재생에너지 건설을 승인했으며, 그 중 22,326.1MW가 태양광 발전입니다. 이는 비용 절감, 허가 절차의 효율화, 기업의 재생에너지 크레딧(REC)에 대한 수요 증가를 뒷받침합니다. 카스티야 이 레온, 아라곤, 카스티야 라 만차 지방은 우수한 일사량과 토지 이용 가능성을 바탕으로 가장 많은 할당량을 확보했습니다. 분산형 지붕 설치 시스템도 산업단지에 빠르게 보급되어 에너지 비용 절감과 Scope 2 배출량 감소에 기여하고 있습니다. 대규모 발전소와 온사이트 발전 설비의 시너지 효과로 스페인의 전력 시장의 재생에너지 보급률이 상승하고 있으며, 2030년까지 81%의 친환경 전력 목표 달성을 위한 규정 준수를 촉진하고 있습니다.

하이퍼스케일 데이터센터 진출기업 주도 기업 간 PPA 추진

하이퍼스케일 플랫폼 수요가 스페인의 전력 시장의 수익 모델을 재구성하고 있습니다. 구글의 35MW 10년 계약 풍력 PPA, 아마존의 469MW 태양광 도입 계획, 애플의 105MW 계약은 기술 대기업이 지원하는 개발자 주도의 건설 전환을 여실히 보여줍니다. 데이터센터용량은 2026년 600MW, 2030년까지 3,000MW에 달할 수 있으며, 수 기가와트 규모의 재생에너지 공급 파이프라인을 지속할 수 있습니다. PPA는 은행 대출이 가능한 현금 흐름을 제공하여 자금 조달 비용을 절감하고, 하이퍼스케일러의 넷제로 전략과 연계하여 기존 전력회사 조달량을 초과하는 설비 도입을 가속화할 수 있습니다.

송전망 강화를 위한 설비투자(CAPEX) 증가

스페인 송전망공사(Red Electrica)는 2026년까지 65억 유로의 보강 예산을 책정하고 있지만, 2030년까지 100억 유로의 보강이 필요하며, 35억 유로의 자금이 부족하다고 지적하고 있습니다. 요금 상한으로 인해 연간 가격 인상 폭이 15%로 제한되어 비용 회수가 막혀 있습니다. 변전소 건설은 토지 문제가 발생하여 15기의 400kV 시설 중 8기가 법적 이의제기로 인해 2년이 지연되고 있습니다. 철강 및 구리 가격의 급등으로 송전선로 건설비용은 2020년 120만 유로/km에서 2024년 180만 유로/km로 상승했습니다. 개혁이 이루어지지 않으면 2028년까지 연간 50억kWh의 재생에너지 생산량이 감소할 수 있으며, 태양광 발전의 유효 이용률은 22%까지 떨어질 것으로 예측됩니다.

부문 분석

2025년 기준 재생에너지는 설치 용량의 67.10%를 차지할 것이며, 연간 6.95% 증가율로 스페인의 청정 에너지 시장 규모는 2025년 101.27GW에서 2031년 150.66GW로 확대될 것으로 예측됩니다. 태양광 발전은 2025년 1월 기준 32.0GW로 풍력 발전(32.0GW)을 넘어섰습니다. 이는 낮은 입찰 가격과 24%의 설비 가동률에 힘입은 것입니다. 리파워링은 새로운 토지를 필요로 하지 않고 육상풍력의 생산성을 향상시키는 한편, 2GW 규모의 부유식 해상풍력 임대 계약으로 미개발된 해양 자원을 개발할 수 있습니다. 수력발전은 17기가와트에서 안정적으로 유지되고 있으며, 저수지의 수위 저하로 인해 피크 차단 능력이 제한되는 문제를 안고 있습니다. 2027년까지 석탄화력 폐지와 재생에너지 피크 대응용 무세 용량에 대한 가스화력 전환으로 풍력-태양광 발전이 부진한 날의 예비율은 더욱 악화될 것으로 예측됩니다.

화력 발전 설비는 2025년 총 용량의 25.80%까지 감소했습니다. 엔데사의 석탄화력 폐지로 2GW를 감축하여 연간 1,200만 톤의 CO2 배출량을 줄였습니다. 복합화력 발전은 총 24GW를 유지하되, 재생에너지 확대에 따라 가동시간은 감소. 하이브리드 축전 시스템으로 4시간의 출력 변동에 대응합니다. 원자력 발전은 2035년까지 7.1GW로 동결되며, 이후 폐쇄로 인해 50TWh공급 공백이 발생하여 수입 전력 또는 축전지로 보충해야 합니다. 순환경제 인센티브에 힘입어 바이오매스 발전은 2030년까지 1.2GW에서 1.8GW로 확대될 것으로 예측됩니다. 이러한 변화는 송전망의 유연성 문제가 증가하는 가운데 스페인의 전력 시장이 탈탄소 기술로 전환하고 있음을 보여줍니다.

스페인의 전력 시장 보고서는 전원별(화력, 원자력, 재생에너지) 및 최종사용자별(전력회사, 상업/산업, 주거용)로 분류되어 있습니다. 시장 규모와 예측은 설치 용량(GW) 단위로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The Spain Power Market is expected to grow from 150.93 gigawatt in 2025 to 156.9 gigawatt in 2026 and is forecast to reach 190.55 gigawatt by 2031 at 3.96% CAGR over 2026-2031.

The expansion is propelled by the country's accelerated renewables build-out, EU decarbonization mandates, and strong corporate appetite for clean power purchase agreements. Solar PV became the nation's single largest power source in 2024, confirming Spain's pivot toward low-carbon generation. A grid-modernization agenda that prioritizes extra-high-voltage corridors, alongside EU-backed storage funding, is enabling ever-larger volumes of intermittent output to connect. Meanwhile, industrial electrification, e-mobility incentives, and data-center development are reshaping load profiles and sustaining demand for grid-connected renewables. Finally, the reversal of the nuclear phase-out adds baseload resilience and delays capacity-adequacy concerns while transmission upgrades catch up.

Spain Power Market Trends and Insights

Accelerating Grid-Connected Solar PV Build-Out

Spain's solar segment set a watershed in 2024 when it overtook gas and wind as the country's top power source. Authorities cleared 26,159.2 MW of renewable construction in 2024, 22,326.1 MW of which is PV, underscoring cost declines, streamlined permitting, and corporate REC demand. Castilla y Leon, Aragon, and Castilla-La Mancha garnered the largest quotas, benefiting from superior irradiation and land availability. Distributed rooftop systems are likewise proliferating across industrial estates, cutting energy bills and Scope-2 emissions. Together, utility-scale and on-site arrays are raising the Spain electricity market's renewable penetration, easing compliance with the 81% green-power target for 2030.

Corporate PPAs Led by Hyperscale Data-Center Entrants

Demand from hyperscale platforms is reshaping revenue models in the Spain electricity market. Google's 35 MW, 10-year wind PPA, Amazon's 469 MW solar commitment, and Apple's 105 MW deal illustrate a shift toward developer-financed build-outs backstopped by tech majors. Data-center capacity could hit 600 MW in 2026 and 3,000 MW by 2030, sustaining multi-gigawatt renewable pipelines. PPAs provide bankable cash flows, lower financing costs, and dovetail with hyperscalers' net-zero strategies, accelerating installations beyond traditional utility procurement volumes.

Escalating Transmission Upgrade CAPEX

Red Electrica budgets EUR 6.5 billion for reinforcements through 2026, yet identifies a EUR 10 billion need by 2030, leaving a EUR 3.5 billion gap. Tariff caps limit annual hikes to 15%, throttling cost recovery. Substation builds face land disputes, with 8 of 15 400-kV facilities delayed two years by legal appeals. Steel and copper inflation pushed line costs from EUR 1.2 million /km in 2020 to EUR 1.8 million /km in 2024. Absent reform, 5 TWh of renewable output could be shed each year by 2028, trimming effective solar utilization to 22%.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Electrification of Mobility & Heating

- EU Fit-for-55 & NECP-2030 Decarbonisation Mandates

- Lengthy Environmental & Municipal Permitting

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Renewables accounted for 67.10% of installed capacity in 2025, and their 6.95% yearly advance ensures the Spain power market size for clean sources rises from 101.27 GW in 2025 to 150.66 GW in 2031. Solar photovoltaic eclipsed wind at 32.0 GW versus 32.0 GW in January 2025, propelled by low auction tariffs and 24% capacity factors. Repowering lifts onshore wind productivity without new land, while 2 GW of floating offshore leases open an untapped marine resource. Hydropower remains steady at 17 GW but suffers from lower reservoir levels that curb peak-shaving ability. Coal's exit by 2027 and gas's shift to peaking duty-free capacity for renewables will yet tighten reserve margins on low-wind, low-sun days.

Thermal fleets fell to 25.80% of capacity in 2025. Endesa's coal phase-out removed 2 GW, slashing 12 million tpy of CO2. Combined-cycle gas totals 24 GW but runs fewer hours as renewables scale, with hybrid storage enabling four-hour ramps. Nuclear stays flat at 7.1 GW through 2035, after which closures leave a 50 TWh gap to fill with imports or batteries. Biomass grows from 1.2 GW to a projected 1.8 GW by 2030 under circular-economy incentives. Together, this transformation underlines how the Spain power market pivots toward carbon-free technologies even as grid flexibility challenges mount.

The Spain Power Market Report is Segmented by Power Source (Thermal, Nuclear, and Renewables) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- Endesa S.A.

- Iberdrola S.A.

- Naturgy Energy Group S.A.

- EDP Group (EDP HC Energia)

- Acciona Energia

- Repsol Electricidad y Gas

- Grupo Red Electrica

- Siemens Gamesa Renewable Energy

- Nordex SE

- TotalEnergies SE

- Enel Green Power Espana

- Vestas Mediterranean

- ABO Wind AG

- Engie Espana

- Capital Energy

- Forestalia Renovables

- Grenergy Renovables

- Hive Energy Spain

- Solarpack Corporacion Tecnologica

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating grid-connected solar PV build-out

- 4.2.2 Repowering of 1990s-2000s wind farms

- 4.2.3 Corporate PPAs led by hyperscale data-centre entrants

- 4.2.4 EU Fit-for-55 & NECP-2030 decarbonisation mandates

- 4.2.5 Rapid electrification of mobility & heating

- 4.2.6 EU funding for cross-border HVDC links

- 4.3 Market Restraints

- 4.3.1 Escalating transmission upgrade CAPEX

- 4.3.2 Lengthy environmental & municipal permitting

- 4.3.3 Rising curtailment risk in resource-rich regions

- 4.3.4 Local opposition to on-shore wind siting

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Power Source

- 5.1.1 Thermal (Coal, Natural Gas, Oil and Diesel)

- 5.1.2 Nuclear

- 5.1.3 Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal)

- 5.2 By End User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

- 5.3 By T&D Voltage Level (Qualitative Analysis only)

- 5.3.1 High-Voltage Transmission (Above 230 kV)

- 5.3.2 Sub-Transmission (69 to 161 kV)

- 5.3.3 Medium-Voltage Distribution (13.2 to 34.5 kV)

- 5.3.4 Low-Voltage Distribution (Up to 1 kV)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Endesa S.A.

- 6.4.2 Iberdrola S.A.

- 6.4.3 Naturgy Energy Group S.A.

- 6.4.4 EDP Group (EDP HC Energia)

- 6.4.5 Acciona Energia

- 6.4.6 Repsol Electricidad y Gas

- 6.4.7 Grupo Red Electrica

- 6.4.8 Siemens Gamesa Renewable Energy

- 6.4.9 Nordex SE

- 6.4.10 TotalEnergies SE

- 6.4.11 Enel Green Power Espana

- 6.4.12 Vestas Mediterranean

- 6.4.13 ABO Wind AG

- 6.4.14 Engie Espana

- 6.4.15 Capital Energy

- 6.4.16 Forestalia Renovables

- 6.4.17 Grenergy Renovables

- 6.4.18 Hive Energy Spain

- 6.4.19 Solarpack Corporacion Tecnologica

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment