|

시장보고서

상품코드

1940738

데향 프린터(LFP) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Large Format Printers (LFP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

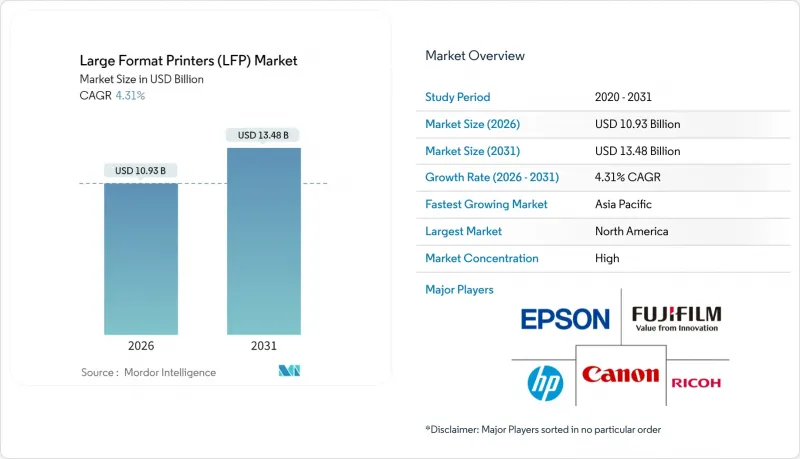

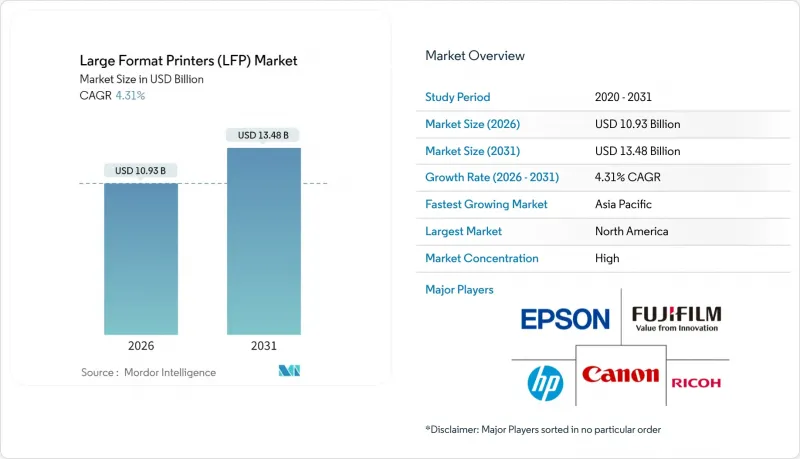

데향 프린터 시장 규모는 2025년 104억 8,000만 달러에서 2026년에는 109억 3,000만 달러에 이를 것으로 예측됩니다.

2031년까지 예측에 따르면, 2031년까지 134억 8,000만 달러에 달할 것으로 예상되며, 2026-2031년 연평균 복합 성장률(CAGR) 4.31%를 나타낼 것으로 예측됩니다.

이러한 성장 경로는 급속한 확장기를 지나 포장의 디지털화, 텍스타일의 개인화, 임팩트 있는 광고판 수요의 융합 속에서 계속 자리를 잡아가고 있는 산업을 반영합니다. 고속 UV 경화 시스템, 지속 가능한 수성 잉크의 혁신, AI를 활용한 워크플로우 자동화를 통해 프린터의 수명주기를 연장하는 동시에 운영비용을 절감하고 있습니다. 지역별로는 북미가 여전히 선두를 유지하고 있지만, 아시아태평양의 가속화된 설비투자와 확대되는 제조거점은 향후 5년간 세력 구도의 변화를 예고하고 있습니다. 경쟁적 차별화는 하드웨어, 소프트웨어, 인증된 에코 잉크를 통합한 엔드투엔드 솔루션에 달려 있으며, 이를 통해 인쇄 서비스 제공업체는 품질 저하 없이 빠른 납기와 가변 데이터 작업에 신속하게 대응할 수 있습니다.

세계 대형 프린터(LFP) 시장 동향 및 인사이트

포장, 광고, 섬유 분야 급성장

인쇄 포장 시장은 2024년 5,120억 달러에서 2029년까지 6,950억 달러로 연평균 6.3% 성장하여 대형 프린터 시장에서 가장 영향력 있는 수요 동인이 될 것으로 예측됩니다. 동시에 패션 브랜드가 점점 더 빠른 배송 맞춤화를 채택함에 따라 디지털 섬유 생산량은 2024년 31억 달러에서 2030년 79억 달러에 달하고, CAGR 14.9%로 증가할 것으로 예측됩니다. 아웃도어 미디어 예산이 회복세를 보이면서 고내구성 기판에 대한 수요가 증가하고 있습니다. 이러한 추세에 따라 각 업체들은 골판지, 플렉서블 필름, 폴리에스테르 원단을 한 번에 처리할 수 있는 모듈식 프린터의 개발을 추진하고 있습니다. 캐논의 화이트 잉크를 탑재한 'Colorado M 시리즈'는 시제품 제작부터 양산까지 원활하게 전환할 수 있는 하이브리드 기능의 가치를 입증하고 있습니다.

UV 경화형 및 고속 잉크젯 채택

즉시 경화, 다양한 기판 대응, 저배출 특성으로 북미와 유럽에서는 UV 경화형 장비의 도입이 활발히 이루어지고 있습니다. 캐논의 UVgel 시스템과 후지필름의 AQUAFUZE 시스템은 마무리 시간을 단축하고 휘발성 용매를 제거하여 공장의 생산성을 향상시킵니다. 리코는 사인 및 그래픽 수요가 급증하면서 2024년 1분기 산업용 인쇄 하드웨어가 32% 성장했다고 밝혔습니다. 오프셋 품질에 근접한 인쇄 속도와 디지털 유연성을 겸비한 고속 잉크젯 기술은 특히 빠른 작업 전환이 중요한 대량 상업용 인쇄에서 매력적입니다. 그 결과, 기존의 용제식 장비에서 자동 색조 관리 기능을 갖춘 UV 경화형 및 수성 기술로의 전환이 꾸준히 진행되고 있습니다.

디지털 사이니지의 대안

인쇄 사이니지 시장은 2018년부터 2023년까지 연평균 복합 성장률(CAGR) 2.2%로 축소되어 409억 달러 규모에 달할 것으로 예측됩니다. 한편, 유럽의 디지털 디스플레이 시장은 매년 약 11%씩 성장하고 있습니다. 디지털 옥외광고(DOOH)는 이미 옥외광고(OOH) 총 수익의 37%를 차지하고 있으며, 호주에서는 76%의 보급률을 달성했습니다. 광고주들은 인쇄물에서는 구현할 수 없는 실시간 컨텐츠 업데이트와 시청자 분석을 중요하게 생각합니다. 그 결과, 교통량이 많은 교통 거점에서는 인쇄량이 감소하고 있지만, 비용 중심적이거나 일시적인 캠페인에서는 여전히 종이와 비닐이 선호되고 있습니다. 이러한 억제요인은 대형 프린터 시장에 영향을 미치고 있으며, 정적 배경과 동적 LED 오버레이를 결합한 하이브리드 캠페인의 혁신을 촉진하고 있습니다.

부문 분석

2025년 프린터는 매출의 76.92%를 차지하며 대형 프린터 시장의 기반을 다졌습니다. UV 경화형 엔진, 하이브리드 플랫베드 롤 시스템, 다양한 소재를 원패스로 처리할 수 있는 라텍스 플랫폼으로 하드웨어 수요는 안정적으로 유지되고 있습니다. 캐논, 엡손, HP는 화이트 잉크와 네온 안료의 선택 폭을 넓혀 인쇄업체가 보다 수익성 높은 장식 및 포장 업무를 추구할 수 있도록 돕고 있습니다. 지속적인 업데이트 주기로 인해 대형 프린터 시장 규모는 자본 예산의 핵심으로 유지되고 있습니다.

소프트웨어 매출은 규모는 작지만, AI 기반 잡깅, 자동 임포징, 원격 기기 상태 모니터링의 보급과 함께 CAGR 5.63%로 증가하고 있습니다. HP PrintOS, 캐논 PRISMA, 리코 TotalFlow의 각 제품군은 독립형 프린터를 클라우드 연계형 생산 노드로 전환합니다. 이러한 전환은 대형 프린터 시장이 인더스트리 4.0과 어떻게 조화를 이루고 있는지 보여주며, 그 가치는 기계적인 출력뿐만 아니라 데이터 기반 효율성에 있습니다.

잉크젯은 온디맨드 기술을 통한 범용성과 넓은 색 영역을 바탕으로 2025년에도 대형 프린터 시장에서 47.74%의 점유율을 유지했습니다. 수성, 라텍스, 솔벤트, UV 잉크의 다양한 유형을 통해 사용자는 용도에 따라 잉크를 선택할 수 있으며, 간판 및 장식용 기본 기술로 자리매김하고 있습니다.

토너 및 레이저 플랫폼은 규모는 작지만, 차세대 전자 사진식 인쇄기가 B2XL 크기에 도달함에 따라 2031년까지 연평균 복합 성장률(CAGR) 5.52%를 나타낼 것으로 예측됩니다. 리코의 Pro C9500 시리즈는 복잡한 작업에서 정격 속도의 97%를 달성할 수 있으며, 롤투롤 미디어의 자유도를 능가하는 가동 시간 안정성이 대량 상업 인쇄에서 매력적인 선택이 될 수 있습니다. 잉크젯과 토너의 공존은 대형 프린터 시장이 단일 주류 방식이 아닌 다양한 작업 프로파일에 대응하고 있음을 입증합니다.

지역별 분석

북미는 2025년 매출의 40.86%를 차지했습니다. 이는 AI 지원 워크플로우의 조기 도입과 저배출 프린터를 우대하는 NESHAP(40 CFR Part 63)의 엄격한 환경 기준이 주도하고 있습니다. 예지보전에 대한 투자로 10-35%의 운영비 절감을 실현하고, 인쇄부수 감소에도 불구하고 수익률의 안정성을 유지하고 있습니다. 워싱턴 주를 비롯한 여러 주에서 PFAS 규제가 시행됨에 따라 수성 시스템으로의 전환이 가속화되고 있으며, 대형 프린터 시장을 뒷받침하는 프리미엄 부문이 더욱 견고해지고 있습니다. 아시아태평양은 가장 빠르게 성장하는 지역으로 2031년까지 5.48%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. FAPGA의 보고서에 따르면, 상업용 인쇄 시장은 2022년 1,846억 달러에서 2031년 2,826억 달러로 확대될 것으로 예측됩니다.

유럽은 지속가능성의 트렌드 리더로 자리매김하고 있습니다. 지침 2024/825는 모호한 환경 주장을 금지하고, 재활용 가능성에 대한 임계치를 의무화하여 구매자를 PFAS 프리 잉크 및 FSC 인증 기판으로 유도하고 있습니다. ESG 보고를 위한 감사 추적이 필요한 브랜드 소유주들 사이에서 인라인 분광광도계와 폐루프 컬러 엔진이 장착된 인쇄기가 받아들여지고 있습니다. 성숙한 수요로 인해 전반적인 성장은 완만하지만, 초기 컴플라이언스 투자가 서비스 계약과 개조 키트를 지원하여 총 잠재 시장 규모를 확대하고 있습니다.

남미, 중동 및 아프리카는 기여도는 낮지만, 전압 변동과 고온에 견딜 수 있는 견고한 장비를 제공할 수 있는 공급업체에게 기회가 있습니다. 걸프 지역의 경기장, 관광단지 등 대형 프로젝트에서는 하이엔드 UV 하이브리드 장비를 선호하는 반면, 브라질의 컨버터는 비용 효율적인 솔벤트 유형의 유닛을 원하고 있습니다. 자금 조달 수단이 확대됨에 따라 이들 지역은 대형 프린터 시장에 생산량 증가를 가져올 것입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10Large-format printers market size in 2026 is estimated at USD 10.93 billion, growing from 2025 value of USD 10.48 billion with 2031 projections showing USD 13.48 billion, growing at 4.31% CAGR over 2026-2031.

The growth path reflects a sector that has moved beyond rapid expansion yet continues to gain ground as packaging digitization, textile personalization, and high-impact signage demand converge. Faster UV-curable systems, sustainable water-based ink innovations, and AI-enabled workflow automation are extending printer lifecycles while keeping operating costs in check. Regional leadership remains with North America, but Asia Pacific's accelerating capital investment and expanding manufacturing base signal a shift in power over the next five years. Competitive differentiation hinges on end-to-end solutions that integrate hardware, software, and certified eco-inks, enabling print service providers to respond promptly to short-run, variable-data jobs without compromising quality.

Global Large Format Printers (LFP) Market Trends and Insights

Packaging, advertising and textile boom

Printed packaging is projected to expand from USD 512 billion in 2024 to USD 695 billion by 2029, at a 6.3% CAGR, making packaging the most influential demand driver for the large-format printers market. Simultaneously, digital textile output is projected to rise from USD 3.1 billion in 2024 to USD 7.9 billion in 2030, at a 14.9% CAGR, as fashion brands increasingly adopt short-run customization. Outdoor media budgets are rebounding, which elevates the need for high-durability substrates. Together, these trends push vendors to develop modular printers capable of handling corrugated board, flexible films, and polyester fabric in a single shift. Canon's Colorado M-series with white ink showcases the value of hybrid capability that seamlessly transitions between prototyping and production.

UV-curable and high-speed inkjet adoption

Immediate curing, broad substrate support, and low emissions drive the adoption of UV-curable installations in North America and Europe. Canon UVgel and Fujifilm AQUAFUZE systems reduce finishing times and eliminate volatile solvents, enhancing shop throughput. Ricoh reports that its industrial printing hardware grew 32% in Q1 2024, driven by surging sign-graphics demand. Print speeds that approach offset quality while retaining digital flexibility make high-speed inkjet technology attractive for high-volume commercial work, especially where quick job changeovers are crucial. The outcome is a steady migration away from legacy solvent machines toward UV-curable and aqueous technologies with automated color control.

Digital signage substitution

Printed signage contracted at a -2.2% CAGR between 2018 and 2023 to USD 40.9 billion, while digital displays gained roughly 11% annually in Europe. Digital out-of-home already secures 37% of total OOH revenue and holds 76% penetration in Australia. Advertisers value real-time content updates and audience analytics that print cannot match. As a result, print volumes fall in high-traffic transit hubs, although cost-sensitive or temporary campaigns still favor paper or vinyl. The restraint pulls on the large-format printers market yet sparks innovation in hybrid campaigns that pair static backdrops with active LED overlays.

Other drivers and restraints analyzed in the detailed report include:

- ESG-driven shift to water-based inks

- AI-automated workflow for SMB print shops

- High cap-ex and opex of industrial LFPs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Printers generated 76.92% of revenue in 2025, anchoring the large format printers market. Hardware demand remains stable, thanks to UV-curable engines, hybrid flatbed-roll systems, and latex platforms that handle diverse substrates in a single pass. Canon, Epson, and HP expand their white-ink and neon pigment options, allowing print shops to pursue higher-margin decor and packaging work. Ongoing replacement cycles sustain the large-format printers market size at the core of capital budgets.

Software revenue, though smaller, is rising at a 5.63% CAGR as AI-driven job ganging, automatic imposition, and remote device health monitoring gain traction. HP PrintOS, Canon PRISMA, and Ricoh TotalFlow suites convert stand-alone printers into cloud-linked production nodes. The shift illustrates how the large-format printers market aligns with Industry 4.0, where value resides in data-enabled efficiency as much as in mechanical output.

Inkjet maintained a 47.74% market share of the large-format printers market in 2025, driven by the versatility of drop-on-demand technology and its wide color gamut. Water-based, latex, solvent, and UV variations enable users to tailor fluids to meet end-use requirements, making inkjet the default technology for signage and decor.

Toner and laser platforms, although smaller, are projected to show a 5.52% CAGR through 2031 as next-generation electrophotographic presses reach B2XL sizes. Ricoh's Pro C9500 series achieves a 97% rated speed on complex jobs, making it an attractive option for high-volume commercial runs where uptime consistency outweighs the benefits of roll-to-roll media freedom. The coexistence of inkjet and toner confirms that the large-format printers market serves multiple job profiles rather than a single dominant method.

The Large Format Printers Market Report is Segmented by Offering (Printers, Software, and Services), Printing Technology (Inkjet, and Toner/Laser), Ink Type (Aqueous, Solvent and Eco-Solvent, UV-Curable, Latex, and Dye-Sublimation), End-User Industry (Signage and Outdoor Advertising, Apparel and Textiles, Decor and Interior Graphics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 40.86% of revenue in 2025, driven by the early adoption of AI-enabled workflows and stringent environmental standards under NESHAP 40 CFR Part 63, which rewards low-emission printers. Investments in predictive maintenance deliver 10-35% operating cost reductions, keeping profit margins resilient even as print runs shrink. PFAS limits in states such as Washington accelerate upgrades to compliant water-based systems, solidifying a premium segment that underpins the large-format printers market. The Asia Pacific is the fastest-growing region, with a 5.48% CAGR projected to 2031. FAPGA reports that commercial printing is expected to expand from USD 184.6 billion in 2022 to USD 282.6 billion in 2031.

Europe remains a sustainability trendsetter. Directive 2024/825 bans vague green claims and enforces recyclability thresholds, steering buyers toward PFAS-free inks and FSC-certified substrates. Printers equipped with inline spectrophotometers and closed-loop color engines gain acceptance among brand owners who require audit trails for ESG reporting. While mature demand keeps overall growth modest, early compliance spend supports service contracts and retrofit kits, enriching the total addressable opportunity.

South America, the Middle East, and Africa contribute smaller shares, yet present opportunities for suppliers that can deliver rugged devices tolerant of voltage swings and heat. Mega-projects in the Gulf, such as stadiums and tourism complexes, favor high-end UV hybrids, whereas Brazilian converters seek cost-effective solvent units. As financing options widen, these territories will add incremental tonnage to the large-format printers market.

- HP Inc.

- Canon Inc.

- Seiko Epson Corporation

- Roland DG Corporation

- Mimaki Engineering Co., Ltd.

- Ricoh Company, Ltd.

- Agfa-Gevaert NV

- Durst Group AG

- Electronics For Imaging, Inc. (EFI)

- Konica Minolta, Inc.

- Kyocera Corporation

- Mutoh Holdings Co., Ltd.

- Fujifilm Holdings Corporation

- ColorJet Group

- SwissQprint AG

- JHF Group

- DGI Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Packaging, Advertising and Textile Boom

- 4.2.2 UV-curable and High-speed Inkjet Adoption

- 4.2.3 ESG-Driven Shift to Water-based Inks

- 4.2.4 AI-Automated Workflow for SMB Print Shops

- 4.2.5 Rise of Localised "Micro-Factory" Print Hubs

- 4.2.6 Aseptic cold-fill for dairy-alternatives

- 4.3 Market Restraints

- 4.3.1 Digital Signage Substitution

- 4.3.2 High Cap-Ex and Opex of Industrial LFPs

- 4.3.3 Looming PFAS-Free Ink Compliance Gap

- 4.3.4 Lightweight glass tech eroding weight edge

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Printers

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Printing Technology

- 5.2.1 Inkjet

- 5.2.2 Toner / Laser

- 5.3 By Ink Type

- 5.3.1 Aqueous

- 5.3.2 Solvent and Eco-Solvent

- 5.3.3 UV-curable

- 5.3.4 Latex

- 5.3.5 Dye-Sublimation

- 5.4 By End-user Industry

- 5.4.1 Signage and Outdoor Advertising

- 5.4.2 Apparel and Textiles

- 5.4.3 Decor and Interior Graphics

- 5.4.4 CAD and Technical

- 5.4.5 Packaging and Labels

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Malaysia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 HP Inc.

- 6.4.2 Canon Inc.

- 6.4.3 Seiko Epson Corporation

- 6.4.4 Roland DG Corporation

- 6.4.5 Mimaki Engineering Co., Ltd.

- 6.4.6 Ricoh Company, Ltd.

- 6.4.7 Agfa-Gevaert NV

- 6.4.8 Durst Group AG

- 6.4.9 Electronics For Imaging, Inc. (EFI)

- 6.4.10 Konica Minolta, Inc.

- 6.4.11 Kyocera Corporation

- 6.4.12 Mutoh Holdings Co., Ltd.

- 6.4.13 Fujifilm Holdings Corporation

- 6.4.14 ColorJet Group

- 6.4.15 SwissQprint AG

- 6.4.16 JHF Group

- 6.4.17 DGI Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment