|

시장보고서

상품코드

1940742

미국의 전기 인클로저 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Electrical Enclosures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

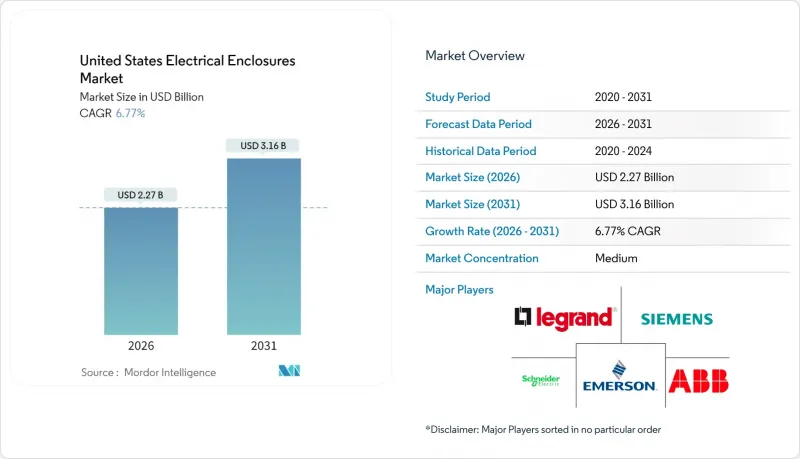

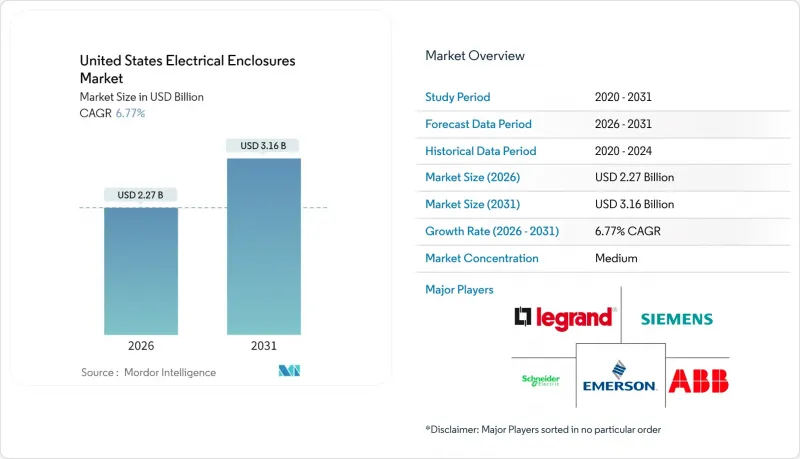

미국의 전기 인클로저 시장은 2025년 21억 3,000만 달러에서 2026년에는 22억 7,000만 달러에 이르고, 2026-2031년 CAGR 6.77%로 성장을 지속하여 2031년까지 31억 6,000만 달러에 달할 것으로 예측됩니다.

송전망의 내결함성 강화, 대규모 태양광 발전 프로젝트, 전기 트럭 충전소에 대한 견조한 설비투자와 함께 두 자릿수 단위 수요가 지속될 것으로 예측됩니다. 전력회사만 2024년 송배전 설비에 1,790억 달러의 예산을 책정했으며, 이 예산은 내후성 및 사이버 보안 대응 캐비닛을 직접 지정하는 예산입니다. 연간 299억 9,000만 달러 규모로 진행되는 데이터센터 건설은 고밀도 전력 분배에 적합한 독립형 대용량 하우징에 대한 수요 구성을 변화시키고 있습니다. 캘리포니아주가 2030년까지 중대형 충전기 15만 7천대 설치를 의무화하는 정책은 메가와트급 신규 인클로저 수요를 촉진하고 있습니다. 이러한 인프라 구축의 흐름과 맞물려 미국 내 전기 인클로저의 잠재적 시장은 유틸리티, 재생에너지, 교통, 디지털 인프라 등 다양한 분야에서 지속적으로 확대되고 있습니다.

미국의 전기 인클로저 시장 동향 및 인사이트

미국의 송전망 강화 프로그램 설비투자 급증

전력 사업자들은 5개년 자본 계획을 235억 달러 증액하고 있으며, PPL만 해도 예산이 40% 증가한 200억 달러로 늘어났습니다. 배전 변전소 지출은 2023년 61억 달러에 달하고, 2003년 대비 3배 이상 증가했습니다. 각 개조 공사에는 NEMA 4X 또는 IP66 규격의 캐비닛이 지정되어 있어 바람에 의한 파편과 침수를 방지하고 스마트 릴레이를 보호할 수 있습니다. 강화된 열 관리와 EMI 차폐가 기본 요건이 되어 평균 판매 가격을 높이고 있습니다. 이상기후가 심해짐에 따라 전력회사들은 다년간의 인클로저 계약을 체결하고 있으며, 미국의 전기 인클로저 시장은 지속적인 수주 전망을 가지고 있습니다.

유틸리티 규모의 태양광 발전소 및 전력 저장 시설의 급속한 건설 확대

미 국방부 가이드 사양은 -25℃-+57℃ 범위를 견딜 수 있는 NEMA 3R 컴바이너 박스와 NEMA 4X 제어 캐비닛의 사용을 의무화하고 있습니다. Solar Electric Supply의 Class I Div 2 시스템에서 볼 수 있듯이, 축전지 어레이에 대한 요구사항은 더욱 엄격해졌으며, 통기식 가스 관리 섹션과 밀폐형 전자기기 베이 등이 요구되고 있습니다. 1MW 이상의 프로젝트가 급증하면서 설치 면적이 확대되고, 모듈식 및 적층형 인클로저의 채택이 촉진되고 있습니다. 텍사스와 플로리다 주가 조달 속도를 주도하고 있으며, 태양광 발전 용량 1기가와트당 보통 15,000-20,000개의 신규 캐비닛이 필요합니다. 이에 따라 미국의 전기기기 인클로저 시장은 더 크고 사전 설계된 조립품, 높은 방진 방수 등급(IP 표준)을 갖춘 제품으로 이동하고 있습니다.

철강-알루미늄 원자재 가격 변동

캐나다와 멕시코 수입품에 대한 25%의 새로운 관세로 인해,2025년 3월까지 철강 도관의 평균 비용은 14% 상승했습니다. 한편, 알루미늄 부족으로 인해 패널 가격이 22% 급등하고 있습니다. 중국의 생산 상한선인 4,500만 톤과 가뭄에 시달리는 제련소들이 세계 프리미엄 상승을 불러일으키고 있으며, 세계은행은 2025년까지 공급 부족이 지속될 것으로 전망하고 있습니다. 미국 제조업체들은 캐나다에 비해 약 2배의 전기요금에 직면해 가공비용이 상승하고 있습니다. 제조업체들은 가격 인상 조항을 계약서에 포함시켜 원자재 재고를 늘리고 있으며, 이는 운전 자금을 압박하고 단기적으로 미국의 전기 인클로저 시장의 확장을 억제할 것으로 예측됩니다.

부문 분석

2025년 기준 금속 캐비닛은 미국의 전기 인클로저 시장의 70.54%를 차지할 것으로 예상되며, 강철의 기계적 강도와 알루미늄의 전자파 차폐 특성이 이를 뒷받침하고 있습니다. 316L 등 스테인리스 강종은 해양 및 식품가공 분야 수주를 주도하는 반면, 탄소강은 양산 수요를 주도하고 있습니다. 비금속 제품군은 CAGR 7.33%로 성장하고 있으며, 폴리카보네이트 및 유리 강화 폴리머(GRP) 인클로저를 사용하여 무게를 줄이고 부식을 방지하는 것이 특징입니다. 신흥 무선 계측 기기에서는 2.4GHz 신호의 충실도 유지를 위해 GRP가 채택되어 IIoT 도입에 있어 실용성이 확대되고 있습니다.

NEMA 4X 및 IP68 규격의 폴리카보네이트 박스는 해안가 태양광 발전 콤비네이터 어레이에 적용되며, 강철의 절반 무게로 자외선 안정성과 실리콘 개스킷 밀봉을 실현합니다. OEM 제조업체는 UL 508A 패널 구조와의 호환성을 높이 평가하여 설계 변경에 따른 마찰을 최소화합니다. 관세로 인한 금속 원재료 비용 상승으로 가격 경쟁력이 높아지고 있으며, 대응 가능한 용도가 확대되고 있습니다. 복합재료로의 지속적인 다변화는 비금속 제품의 보급률 향상과 미국의 전기 인클로저 시장 전망 재료 구성 변화를 약속합니다.

프리사이즈 또는 풀사이즈(50리터 이상)의 출하량은 전체의 33.01%를 차지하여 공장에서 분산형 PLC와 센서의 역할을 반영하고 있습니다. 변전소 개보수 및 데이터센터 배전반에 대한 수요 증가로 인해 모듈형 또는 구성 가능한 시스템 시장은 CAGR 7.55%를 나타낼 것으로 예측됩니다. AI 워크로드 증가에 따라 랙 전력 밀도가 600kW에 육박하고, 800V 고전압 직류 배전이 필수적이기 때문에 대형의 열 관리 기능을 갖춘 인클로저가 필요합니다.

전력 부문에서는 릴레이, 배터리, 통신 장비를 하나의 구조물에 통합한 워크인 제어 쉘터를 채택하여 현장 배선 시간을 단축합니다. 모듈형 캐비닛 생태계는 부하 증가에 따라 베이를 추가 설치할 수 있어 자본 예산을 보호할 수 있습니다. 이러한 확장성 특성은 대형 제품의 전략적 가치를 확고히 하며, 미국의 전기 인클로저 시장에서의 수익 구성 비율을 높이고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The United States Electrical Enclosures Market is expected to grow from USD 2.13 billion in 2025 to USD 2.27 billion in 2026 and is forecast to reach USD 3.16 billion by 2031 at 6.77% CAGR over 2026-2031.

Robust capital outlays for grid resilience, utility-scale solar projects, and electric truck charging depots are converging to sustain double-digit unit demand. Utilities alone budgeted USD 179 billion in 2024 for transmission and distribution hardware, a spending pool that directly specifies weather-sealed, cyber-secure cabinets. Data center construction running at a USD 29.99 billion annual rate is shifting the mix toward free-standing, large-volume housings suited for high-density power distribution. California's mandate for 157,000 medium- and heavy-duty chargers by 2030 underpins a new class of megawatt-rated enclosures. These infrastructure themes collectively expand the addressable market for US electrical enclosures across utilities, renewables, transportation, and digital infrastructure.

United States Electrical Enclosures Market Trends and Insights

Surging CAPEX in U.S. Grid-Hardening Programs

Utility owners are boosting five-year capital plans by USD 23.5 billion, with PPL alone lifting its budget 40% to USD 20 billion. Distribution substation spend hit USD 6.1 billion in 2023, more than tripling 2003 levels. Each retrofit specifies NEMA 4X or IP66 cabinets able to endure wind-borne debris and flood exposure while sheltering smart relays. Enhanced thermal management and EMI shielding now form baseline requirements, pushing average selling prices higher. As extreme-weather events intensify, utilities are locking in multi-year enclosure contracts, giving the US electrical enclosures market durable order visibility.

Rapid Build-Out of Utility-Scale Solar and Storage Farms

Department of Defense guide specs obligate NEMA 3R combiner boxes and NEMA 4X control cabinets that tolerate -25 °C to +57 °C ranges. Storage arrays impose stricter demands, including vented gas management sections and sealed electronics bays, as illustrated by Class I Div 2 systems from Solar Electric Supply. The boom in projects above 1 MW is enlarging physical footprints, spurring uptake of modular, stackable enclosures. Texas and Florida are setting procurement pace, and each gigawatt of solar capacity typically translates to 15,000-20,000 new cabinets. Consequently, the US electrical enclosures market is pivoting toward larger, pre-engineered assemblies with higher ingress-protection ratings.

Commodity Price Volatility for Steel and Aluminum

New 25% tariffs on Canadian and Mexican inputs drove average steel conduit costs up 14% by March 2025, while aluminum shortages pushed panel prices 22% higher. China's output cap at 45 million tonnes and drought-hit smelters lift global premiums, and the World Bank expects tightness to persist through 2025. U.S. producers face power rates almost double those in Canada, inflating conversion costs. Manufacturers are inserting escalation clauses and carrying larger raw-material inventories, which strains working capital and tempers the US electrical enclosures market expansion over the near term.

Other drivers and restraints analyzed in the detailed report include:

- Electrification of Commercial Vehicle Depots

- Federal Tax Incentives for Domestic Panel Manufacturing

- Sluggish Non-Residential Construction in 2024-2025

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metallic cabinets retained 70.54% command of the US electrical enclosures market in 2025, underpinned by steel's mechanical resilience and aluminum's EMI shielding. Stainless grades such as 316L headline offshore and food-processing orders, whereas carbon steel dominates volume buyers. The non-metallic cohort, expanding at 7.33% CAGR, features polycarbonate and glass-reinforced polymer housings that slash weight and eliminate corrosion. Emerging wireless instrumentation uses GRP to preserve 2.4 GHz signal fidelity, broadening utility in IIoT rollouts.

Polycarbonate boxes rated NEMA 4X and IP68 now serve coastal PV combiner arrays, delivering UV stability and silicone-gasket sealing at half the weight of steel. OEMs appreciate drop-in compatibility with UL 508A panel builds, minimizing redesign friction. As tariffs inflate metal input costs, price parity is approaching, expanding addressable applications. Continued diversification into composites promises to lift non-metallic penetration and reshape future material splits within the US electrical enclosures market.

Free-size or full-size (above 50 L) accounted for 33.01% of the shipments, mirroring distributed PLC and sensor duties in factories. Modular or configurable systems are projected to grow at a 7.55% CAGR, propelled by substation retrofits and data-center switchboards. AI workloads push rack power densities toward 600 kW, obliging 800 V HVDC distribution that demands bigger, thermally managed housings.

Utility segments adopt walk-in control shelters that bundle relays, batteries, and communications inside one structure, cutting field wiring time. Modular cabinet ecosystems let operators bolt incremental bays as loads grow, safeguarding capital budgets. This scalability theme cements the strategic value of large-format offerings and increases their revenue mix inside the US electrical enclosures market.

The United States Electrical Enclosures Market Report is Segmented by Material Type (Metallic, and Non-Metallic), Form Factor (Small, Compact, Free-Size, and Modular), Mounting Type (Wall-Mounted, Floor-Mounted, Underground, and Pole-Mounted), End-User Industry (Energy and Power, Oil and Gas, Industrial Manufacturing and Robotics, Data Centers and Telecom, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Schneider Electric SE

- ABB Ltd

- Eaton Corporation plc

- Hubbell Inc.

- nVent Electric plc

- Rittal GmbH and Co. KG

- Legrand SA

- Siemens AG

- Emerson Electric Co.

- Hammond Manufacturing Ltd.

- AZZ Inc.

- Adalet (Scott Fetzer Co.)

- Austin Electrical Enclosures, LLC

- Bison ProFab, Inc.

- Saginaw Control and Engineering, Inc.

- Stahlin Enclosures (Atkore Inc.)

- Allied Moulded Products, Inc.

- Pentair plc (Schroff)

- Integra Enclosures, LLC

- Fibox USA, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging CAPEX in U.S. grid-hardening programs

- 4.2.2 Rapid build-out of utility-scale solar and storage farms

- 4.2.3 Electrification of commercial vehicle depots

- 4.2.4 Federal tax incentives for domestic panel manufacturing

- 4.2.5 AI-enabled predictive maintenance enclosures

- 4.2.6 Growing demand for cyber-secure IIoT ready enclosures

- 4.3 Market Restraints

- 4.3.1 Commodity price volatility for steel and aluminum

- 4.3.2 Sluggish non-residential construction in 2024-2025

- 4.3.3 High certification costs for UL 508A/NEMA 4X smart enclosures

- 4.3.4 Limited interoperability standards for wireless sensors inside metal cabinets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Electrical Enclosure Standards

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Metallic (Carbon Steel, Stainless Steel, Aluminum)

- 5.1.2 Non-metallic (Polycarbonate, Fiberglass, Polyester, ABS)

- 5.2 By Form Factor

- 5.2.1 Small (less than or equal to 10 L)

- 5.2.2 Compact (10-50 L)

- 5.2.3 Free-size / Full-size (above 50 L)

- 5.2.4 Modular / Configurable systems

- 5.3 By Mounting Type

- 5.3.1 Wall-mounted

- 5.3.2 Floor-mounted / Free-standing

- 5.3.3 Underground / Pad-mounted

- 5.3.4 Pole-mounted

- 5.4 By End-user Industry

- 5.4.1 Energy and Power

- 5.4.2 Oil and Gas

- 5.4.3 Industrial Manufacturing and Robotics

- 5.4.4 Metals and Mining

- 5.4.5 Transportation (Rail, Road, Air, EV-charging)

- 5.4.6 Data Centres and Telecom

- 5.4.7 Food and Beverage and Pharmaceuticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 ABB Ltd

- 6.4.3 Eaton Corporation plc

- 6.4.4 Hubbell Inc.

- 6.4.5 nVent Electric plc

- 6.4.6 Rittal GmbH and Co. KG

- 6.4.7 Legrand SA

- 6.4.8 Siemens AG

- 6.4.9 Emerson Electric Co.

- 6.4.10 Hammond Manufacturing Ltd.

- 6.4.11 AZZ Inc.

- 6.4.12 Adalet (Scott Fetzer Co.)

- 6.4.13 Austin Electrical Enclosures, LLC

- 6.4.14 Bison ProFab, Inc.

- 6.4.15 Saginaw Control and Engineering, Inc.

- 6.4.16 Stahlin Enclosures (Atkore Inc.)

- 6.4.17 Allied Moulded Products, Inc.

- 6.4.18 Pentair plc (Schroff)

- 6.4.19 Integra Enclosures, LLC

- 6.4.20 Fibox USA, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment