|

시장보고서

상품코드

1940746

미국의 시니어 리빙 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Senior Living - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

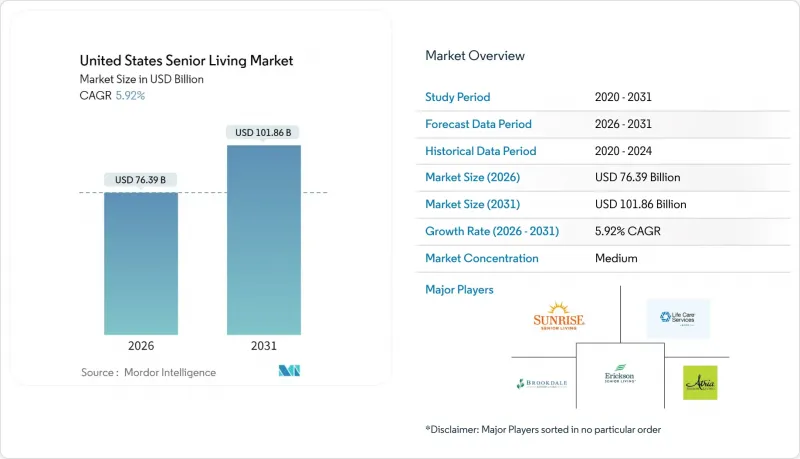

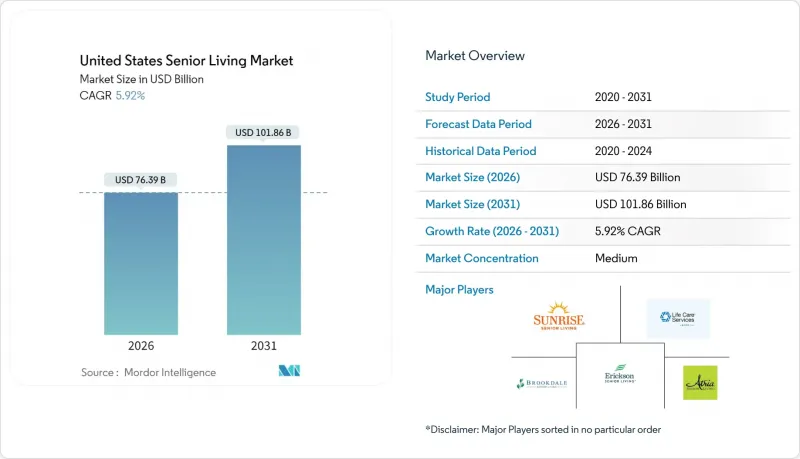

2026년 미국 시니어 리빙 시장 규모는 763억 9,000만 달러로 추정되며, 2025년 721억 1,000만 달러에서 성장이 전망됩니다.

2031년에는 1,018억 6,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 연평균 5.92%로 성장할 것으로 전망됩니다.

고령화에 따른 지속적인 수요, 신규 공급의 제약, 고도의 자본 유입이 맞물리면서 사업자에게 가격 결정력이 생겨 안정적인 입주율 상승을 뒷받침하고 있습니다. 의료와의 통합은 경쟁 우위를 더욱 공고히 합니다. 왜냐하면, 일차의료와 재활 서비스를 통합한 커뮤니티는 더 높은 수익률을 얻고, 체류 기간을 연장하고, 병원으로의 전원을 줄일 수 있기 때문입니다. 임대료 설정의 유연성을 통해 운영사는 임금 상승과 규제 비용에 신속하게 대응할 수 있으며, 인력 부족의 압박 속에서도 영업 이익률을 유지할 수 있습니다. 기관투자자, 특히 의료 REIT는 합작투자 및 세일앤리스백을 통해 개발 파이프라인을 유지하고, 높은 금리에도 불구하고 업계 구조조정을 촉진하고 있습니다. 전자의무기록에서 예측 분석에 이르는 기술 도입은 거주자의 성과와 비용 효율성을 더욱 향상시킬 수 있습니다.

미국 시니어 리빙 시장 동향 및 인사이트

베이비붐 세대의 고령화가 모든 케어 레벨에서 지속적인 수요를 견인하고 있습니다.

약 6,900만 명의 베이비붐 세대의 거의 전원이 2033년까지 70세 이상이 되어 미국 시니어 리빙 시장의 입주자층이 크게 확대될 것입니다. 이 세대의 높은 주택 소유율과 순자산은 민간 부담금을 지불할 수 있는 능력을 뒷받침하고, 기술의 광범위한 수용은 디지털을 활용한 케어에 대한 수용성을 높이고 있습니다. 고급 간호 및 치매 치료를 필요로 할 가능성이 가장 높은 85세 이상 인구는 2040년까지 두 배로 증가할 것으로 예상되며, 고급 의료 서비스에 대한 수요가 보장됩니다. 텍사스, 플로리다 등 유리한 세제와 기후로 은퇴자들을 끌어들이는 주에서는 특히 강한 성장이 예상됩니다. 이 부유하고 기술에 정통한 세대를 위해 시설, 결제 계획, 마케팅을 최적화하는 사업자는 평생 가치를 창출할 수 있는 위치에 있습니다. 그린스트리트의 추산에 따르면, 40% 이상의 노인이 자산을 매각하지 않고도 노인 주택 비용을 충당할 수 있기 때문에 잠재적 수요가 매우 크다는 것을 알 수 있습니다.

개발 및 통합을 지원하는 자본시장과 헬스케어 REIT 활성화 지원

헬스케어 리츠는 미국 시니어 리빙 시장 자산에 사상 최대 규모의 자금을 투입하고 있습니다. 벤타스는 2024년 20억 달러를 운용한 후 2025년 투자 목표를 15억 달러로 상향 조정하며 해당 섹터의 펀더멘털에 대한 장기적인 확신을 드러냈습니다. 웰타워의 32억 달러 규모의 Amica Senior Lifestyles 인수는 REIT가 우량 포트폴리오를 확보하기 위해 얼마나 큰 규모의 거래를 실행하는지를 잘 보여주고 있습니다. 부채 자본은 여전히 풍부하며, Walker & Dunlop은 2024년에 6억 달러의 시니어 리빙 대출을 준비했습니다. 포트리스 등 대형 사모펀드들의 경쟁으로 평가액이 상승하고, 운영의 질적 개선이 촉진되고 있습니다. 높은 유동성은 공급이 부족한 도시 지역의 신규 건설을 지원하고, 지역 소유자 및 운영자에게 퇴출 경로를 제공함으로써 전체 생태계의 통합과 전문화를 가속화하고 있습니다.

인력 부족과 임금 상승으로 이윤율과 서비스 수준에 압박을 가져옵니다.

거의 모든 요양시설에서 심각한 인력난이 발생하고 있으며, 시설들은 시급 인상, 복리후생 확대, 파견노동에 대한 의존도 증가를 강요받고 있습니다. CMS(의료보험-의료보조서비스센터)가 도입한 '입소자 1인당 1일 3.48시간'의 간호시간 기준은 유자격 간호사 쟁탈전을 통해 요양병원과 자립생활시설로까지 파급되고 있습니다. 현재 24시간 간호사 배치 의무를 충족하는 요양시설은 6%에 불과해 업계 전반의 입찰경쟁을 유발하고 수익률을 압박하고 있습니다. 네바다 주에서 시간당 16달러에서 20달러로 인상하는 등 간병인 임금 인상 운동은 인플레이션 압력을 부각시키고 있습니다. 연방거래위원회(FTC)가 검토 중인 경업금지 조항 금지는 이직률을 더욱 높이고, 진료의 연속성을 해칠 우려가 있습니다. 지방의 운영자들은 가장 어려운 상황에 직면해 있으며, 의무화된 직원 대 입소자 비율을 유지하기 위해 입소 제한을 해야 하는 경우도 있습니다.

부문 분석

2025년 기준, 요양시설은 미국 노인요양시설 시장 규모의 40.62%를 차지하며 2031년까지 CAGR 6.29%로 가장 높은 성장률을 보일 것으로 예상됩니다. 수요는 여러 만성질환을 앓고 있는 입주민들이 병원으로 옮기지 않고 지속적인 케어 환경 속에서 그 자리에서 노후를 보내길 원하는 입주자들로부터 발생하고 있습니다. 요양주택은 여전히 주류의 진입점이지만, 운영사업자들은 입주자 유지와 가치 창출을 위해 기억요양 및 아급성기 서비스용 동 개보수를 진행하고 있습니다. 자립생활형 커뮤니티는 자율성을 중시하는 젊은 층 시니어를 위해 라이프스타일 어메니티, 피트니스 센터, 셰프 감수 식단, 문화 프로그램에 중점을 두고 있습니다. 안전대책을 갖춘 레이아웃과 치매 전문 교육을 받은 직원으로 구성된 메모리 케어 유닛의 성숙은 주거 환경을 유지하면서 고도의 의료적 요구를 충족시키는 방향으로의 전환을 보여줍니다. 지속적 케어 노인 커뮤니티는 틈새시장이지만, 여러 수준의 케어에 대한 계약적 접근을 원하는 부유층 시니어들 사이에서 지지를 얻고 있습니다.

요양 서비스의 우위로 인해 임상 직원 교육, 음압실, 시설 내 치료실에 대한 자본 투자가 요구되고 있습니다. 운영사는 전자처방전 관리 시스템, 스마트 리프트 등을 도입하여 안전성과 효율성을 높이고 있습니다. 중증화 추세는 재입원율 감소를 목표로 하는 보험사와의 제휴를 촉진하고, 미국 시니어 리빙 시장에 지불자 중심의 수익원을 추가하고 있습니다. 그러나 인력 배치 비율, 감염 관리, 보수의 적정성 등에 대한 규제 모니터링은 여전히 엄격하며, 고도의 컴플라이언스 체제를 요구하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트와 동향

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10United States senior living market size in 2026 is estimated at USD 76.39 billion, growing from 2025 value of USD 72.11 billion with 2031 projections showing USD 101.86 billion, growing at 5.92% CAGR over 2026-2031.

Continued demand from an aging population, constrained new-build supply, and sophisticated capital inflows combine to create pricing power for operators while supporting steady occupancy gains. Healthcare integration deepens competitive moats because communities that embed primary care and rehabilitation services capture higher margins, lift length of stay, and reduce hospital transfers. Rental pricing flexibility lets operators respond quickly to wage inflation and regulatory costs, helping to maintain operating margins despite labor pressures. Institutional investors, especially healthcare REITs, sustain development pipelines through joint ventures and sale-leasebacks, fueling consolidation even as interest rates remain elevated. Technology adoption, from electronic health records to predictive analytics, further enhances resident outcomes and cost efficiency.

United States Senior Living Market Trends and Insights

Aging Baby-Boomer Cohort Driving Sustained Demand Across Care Levels

Nearly all 69 million baby boomers will be 70 or older by 2033, dramatically enlarging the resident pool for the United States senior living market. Higher home ownership and net worth among this cohort underpin private-pay affordability, while broader acceptance of technology raises comfort with digitally enabled care. The 85-plus population, most likely to require skilled nursing and memory care, is set to double by 2040, guaranteeing demand for high-acuity services. States attracting retirees through favorable taxes and climate, such as Texas and Florida, will see especially strong growth. Operators that tailor amenities, payment plans, and marketing to this wealthier, tech-savvy generation are positioned to capture lifetime value. Green Street estimates show more than 40% of seniors can pay for senior housing without liquidating assets, indicating significant latent demand.

Deep Capital Markets and Active Healthcare REITs Supporting Development and Consolidation

Healthcare REITs are pouring record funds into United States senior living market assets. Ventas lifted its 2025 investment target to USD 1.5 billion after deploying USD 2 billion in 2024, signaling long-term conviction in sector fundamentals. Welltower's USD 3.2 billion acquisition of Amica Senior Lifestyles illustrates the scale REITs will transact to secure premier portfolios. Debt capital remains abundant, with Walker & Dunlop arranging USD 600 million in seniors-housing loans during 2024. Private equity heavyweights such as Fortress add further competition for assets, driving valuations and spurring operational upgrades. Strong liquidity supports new builds in undersupplied metros and offers exit paths for regional owner-operators, accelerating consolidation and professionalization across the ecosystem.

Labor Shortages and Wage Inflation Pressuring Margins and Service Levels

Severe staffing shortages plague virtually every care level, forcing communities to raise hourly wages, expand benefits, and rely heavily on agency labor. New CMS nursing-home staffing rules requiring 3.48 nursing hours per resident per day ripple into assisted and independent living through competition for licensed nurses. Only 6% of nursing homes currently meet the 24/7 RN mandate, driving cross-sector bidding wars that compress margins. Caregiver wage campaigns, such as Nevada's push from USD 16 to USD 20 per hour, spotlight inflationary pressures. The FTC's pending ban on non-compete clauses may further elevate turnover, undermining continuity of care. Operators in rural areas confront the steepest hurdles, sometimes restricting admissions to maintain mandated staff-resident ratios.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Healthcare-Integrated Models Enhancing Value Proposition and Resident Outcomes

- Home-Sale Equity and Retirement Savings Enabling Private-Pay Affordability

- State-by-State Regulatory Complexity Increasing Compliance Costs and Development Timelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nursing care facilities controlled 40.62% of the United States senior living market size in 2025 and will post the quickest 6.29% CAGR through 2031. Demand stems from residents with multiple chronic conditions who prefer aging in place within a continuum-of-care setting instead of hospital transfers. Assisted-living remains the mainstream entry point, yet operators retrofit wings for memory-care or sub-acute services to retain residents and capture value. Independent-living communities focus on lifestyle amenities, fitness centers, chef-led dining, and cultural programs, geared toward younger seniors who prize autonomy. The maturation of memory-care units, complete with secured layouts and dementia-trained staff, illustrates the sector's pivot to higher acuity while preserving residential ambience. Continuing-care retirement communities, though niche, gain traction among affluent seniors desiring contractual access to multiple care levels.

Nursing-care dominance compels capital investment in clinical staff training, negative-pressure rooms, and on-site therapy suites. Operators deploy electronic medication-administration records and smart lifts to boost safety and efficiency. Rising acuity also attracts insurer partnerships seeking reduced readmissions, adding payer-driven revenue to the United States senior living market. However, regulatory scrutiny on staffing ratios, infection control, and reimbursement adequacy remains intense, requiring sophisticated compliance infrastructures.

The United States Senior Living Market Report is Segmented by Property Type (Assisted Living, Independent Living, Memory Care, Nursing Care), by Business Model (Outright Sale (Freehold), Long-Lease / Rental, Hybrid (Sale + Lease)), by Age (55 To 64 Years, 65 To 74 Years, and More), and by States (Texas, California, Florida, New York, Illinois, Rest of US). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Brookdale Senior Living Inc.

- Atria Senior Living Inc.

- LCS (Life Care Services)

- Erickson Senior Living

- Sunrise Senior Living

- Five Star Senior Living

- Holiday by Atria

- Kisco Senior Living

- Sonida Senior Living

- Watermark Retirement Communities

- Silverado Senior Living

- Trilogy Health Services

- Benchmark Senior Living

- Ensign Group Inc.

- Ventas Inc.

- Welltower Inc.

- Capital Senior Living (Grace Management)

- Pegasus Senior Living

- Frontier Management

- Merrill Gardens

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging baby-boomer cohort driving sustained demand across independent, assisted, and memory care

- 4.2.2 Deep capital markets and active healthcare REITs supporting development and consolidation

- 4.2.3 Shift to healthcare-integrated models (primary care, rehab, memory care) enhancing value proposition

- 4.2.4 Home-sale equity and retirement savings enabling private-pay affordability in many metros

- 4.2.5 Technology adoption (remote monitoring, EHRs, fall detection) elevating care quality and efficiency

- 4.3 Market Restraints

- 4.3.1 Labor shortages and wage inflation pressuring margins and service levels

- 4.3.2 State-by-state regulatory complexity increasing compliance costs and timelines

- 4.3.3 Affordability gaps and uneven occupancy recovery in certain secondary markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Policy & Regulatory Framework (state guidelines, licensing, incentives)

- 4.6 Insight on Upcoming and Ongoing Projects

- 4.7 Insights on Digital & Tech Enablers (telemedicine, smart amenities)

- 4.8 Insights on Business Model & Operator Evolution

- 4.9 Insights on Investment & Financing Trends

- 4.10 Insights Sustainability & Design Innovation

- 4.11 Porter's Five Forces

- 4.11.1 Bargaining Power of Suppliers

- 4.11.2 Bargaining Power of Buyers/Consumers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Property Type

- 5.1.1 Assisted Living

- 5.1.2 Independent Living

- 5.1.3 Memory Care

- 5.1.4 Nursing Care

- 5.2 By Business Model

- 5.2.1 Outright Sale (Freehold)

- 5.2.2 Long-Lease / Rental

- 5.2.3 Hybrid (Sale + Lease)

- 5.3 By Age

- 5.3.1 55 to 64 years

- 5.3.2 65 to 74 years

- 5.3.3 75 to 85 years

- 5.3.4 Above 85 years

- 5.4 By States

- 5.4.1 Texas

- 5.4.2 California

- 5.4.3 Florida

- 5.4.4 New York

- 5.4.5 Illinois

- 5.4.6 Rest of US

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Brookdale Senior Living Inc.

- 6.3.2 Atria Senior Living Inc.

- 6.3.3 LCS (Life Care Services)

- 6.3.4 Erickson Senior Living

- 6.3.5 Sunrise Senior Living

- 6.3.6 Five Star Senior Living

- 6.3.7 Holiday by Atria

- 6.3.8 Kisco Senior Living

- 6.3.9 Sonida Senior Living

- 6.3.10 Watermark Retirement Communities

- 6.3.11 Silverado Senior Living

- 6.3.12 Trilogy Health Services

- 6.3.13 Benchmark Senior Living

- 6.3.14 Ensign Group Inc.

- 6.3.15 Ventas Inc.

- 6.3.16 Welltower Inc.

- 6.3.17 Capital Senior Living (Grace Management)

- 6.3.18 Pegasus Senior Living

- 6.3.19 Frontier Management

- 6.3.20 Merrill Gardens

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment