|

시장보고서

상품코드

1940769

다이오드 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Diode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

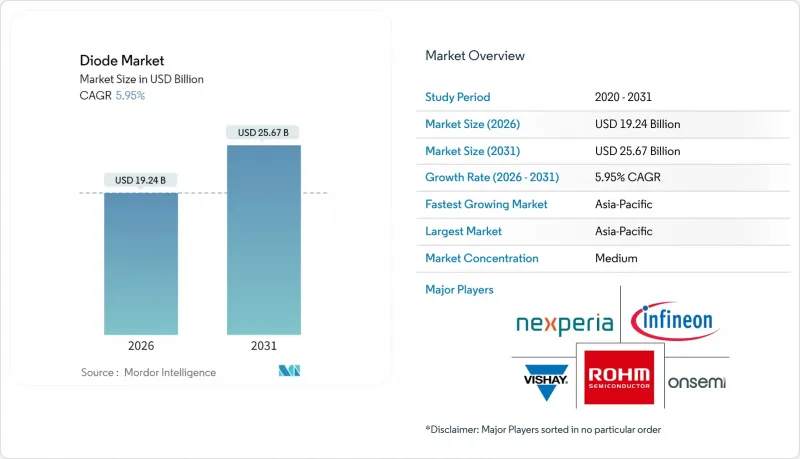

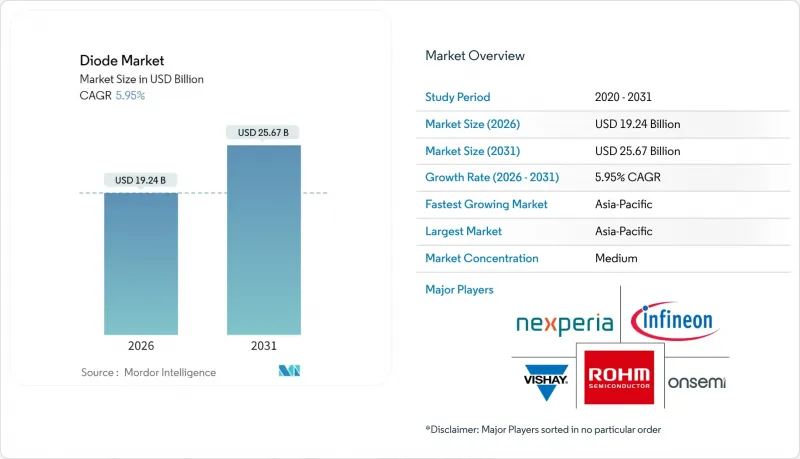

다이오드 시장은 2025년 181억 6,000만 달러에서 2026년에는 192억 4,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 5.95%를 기록하며 2031년까지 256억 7,000만 달러에 달할 것으로 예측됩니다.

소비자 전자기기는 23.2%의 시장 점유율로 가장 큰 최종사용자로 남아 있으며, 전 세계적으로 전기자동차 프로그램이 가속화됨에 따라 자동차 애플리케이션은 6.8%의 가장 높은 CAGR을 보이고 있습니다. 아시아태평양은 전 세계 매출의 58.86%를 차지하며, 중국, 일본, 한국의 밀집된 제조 클러스터 덕분에 6.63%의 속도로 성장하고 있습니다. 표면 실장 패키지는 출하량의 61.2%를 차지하지만, 휴대폰 및 IoT 제조업체들이 이전보다 더 작은 풋프린트를 요구함에 따라 칩 스케일 패키지는 7.1%의 CAGR로 성장하고 있습니다.

세계 다이오드 시장 동향 및 인사이트

가전제품 생태계의 디지털화

스마트폰, 웨어러블 기기, 커넥티드 홈 디바이스는 시스템당 반도체 탑재량이 증가하고 있으며, 신호 조정, 배터리 보호, 데이터 라인 보호를 위한 개별 부품에 대한 수요를 증가시키고 있습니다. 텍사스 인스트루먼트의 ESDS31x 시리즈와 같은 소형 신호 및 정전기 방전 어레이는 최대 5Gbps의 데이터 속도에서 ±30kV의 보호 기능을 제공하며, USB, HDMI, 이더넷 인터페이스를 지원합니다. 아시아태평양 제조업체들은 전 세계 전자기기 하드웨어의 약 60%를 조립하고 있으며, 고속 상호연결을 보호하는 다이오드 어레이에 대한 집중적인 수요를 뒷받침하고 있습니다.

전기자동차 생산 및 차량용 충전기 가속화

전기 파워트레인의 보급률 증가에 따라 자동차용 반도체의 수요가 증가하고 있습니다. 실리콘 카바이드 및 질화 갈륨 다이오드는 트랙션 인버터 및 800V 충전기에서 스위칭 손실을 줄입니다. 온세미의 EliteSiC 플랫폼은 폭스바겐이 차세대 전기자동차에 적용하고 있습니다. 인피니언의 CoolSiC 1200V MOSFET은 추가 절연 없이 DC-DC 스테이지를 900V 이상에서 작동할 수 있어 전력 밀도를 높이면서 시스템 비용을 절감할 수 있습니다.

원자재 가격 변동성(실리콘, 갈륨비소, 질화갈륨)

중국은 갈륨의 1차 원료의 대부분을 공급하고 있으며, 수출 규제가 발생하면 GaAs 및 GaN 소자의 웨이퍼 비용이 급등하게 됩니다. 전 세계 전자폐기물의 20%만이 제대로 재활용되고 있으며, 중요 금속의 손실이 발생하여 공급 부족과 가격 변동이 확대되고 있습니다. SiC 웨이퍼의 수율은 제조 기술의 성숙도와 기판 품질에 따라 달라지며, 여전히 불안정한 상황이 지속되고 있습니다.

부문 분석

레이저 다이오드는 2025년 64억 8,000만 달러로 가장 큰 다이오드 시장 규모를 형성할 것으로 예상되며, 자동차 전방 조명, LiDAR 센싱, 고속 광섬유 통신의 수요 증가로 8.25%의 CAGR을 기록할 것으로 전망됩니다. 정류기 및 쇼트키 소자는 전력변환 분야의 지위를 유지하고 있지만, 그 성장률은 레이저 채용에 비해 한 자릿수 중반으로 저조한 편입니다.

산업용 절단, 프로젝터, 3D 프린팅은 멀티 모드 레이저 다이오드에 대한 수요를 뒷받침하고, 의료용 레이저는 더 엄격한 파장 안정성을 요구하기 때문에 평균 판매 가격이 상승할 것입니다. 서버 전원 분야에서는 인피니언의 GaN 트랜지스터에 쇼트키 다이오드를 통합하여 데드타임 손실을 억제하고 효율을 향상시켰으며, 이는 카테고리 간 협업을 잘 보여주는 좋은 사례입니다.

지역별 분석

아시아태평양은 2025년 세계 매출의 58.30%를 차지할 것이며, 중국, 일본, 한국의 통합 공급망을 배경으로 2031년까지 연평균 6.45%의 CAGR을 유지할 것입니다. 중국은 정부의 특혜와 국내 스마트폰 수출에 힘입어 2023년 전 세계 칩 판매의 대부분을 흡수했습니다. 인도네시아는 98개의 규사 채굴 허가와 면세 조치로 외국인 투자자를 유치하고 기판 생산의 현지화를 목표로 하고 있습니다.

북미의 점유율은 2030년까지 상승할 것으로 예상됩니다. CHIPS법 보조금은 온세미의 텍사스 8인치 SiC 라인을 포함한 5,400억 달러 규모의 민간 팹 투자를 실현할 것으로 예상됩니다. 캐나다는 클린테크 세액공제를 통해 GaN 에피웨이퍼 스타트업 기업을 지원하여 부가가치 공정의 정착을 도모하고 있습니다. 멕시코의 EMS 클러스터는 미국 자동차 공급망에 대한 면세 액세스를 확대하여 정류기 및 서지 보호 장치 조립을 촉진하고 있습니다.

유럽은 2030년까지 세계 생산 점유율 20% 이상을 목표로 하고 있으나, 감사 결과 허가 지연과 숙련공 부족으로 인한 일정 리스크가 지적되고 있습니다. Nexperia의 2억 달러 규모의 함부르크 투자로 유럽의 SiC 생산능력이 확대되는 한편, 폴란드는 인텔의 포스트 팹 테스트 센터를 유치하여 2,000명의 고용을 창출할 예정입니다. 중동 및 아프리카는 아직 개발 중이지만, UAE에서는 1200V SiC 다이오드를 지정하는 파일럿 태양광 인버터 공장이 가동되고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The diode market is expected to grow from USD 18.16 billion in 2025 to USD 19.24 billion in 2026 and is forecast to reach USD 25.67 billion by 2031 at 5.95% CAGR over 2026-2031.

Consumer electronics remains the largest end-user at 23.2% diode market share, while automotive applications show the strongest 6.8% CAGR as electric-vehicle programs accelerate worldwide. Asia-Pacific holds 58.86% of global revenue and grows at a 6.63% pace thanks to dense manufacturing clusters in China, Japan, and South Korea. Surface-mount packaging captures 61.2% of shipments, yet chip-scale packages rise at a 7.1% CAGR because handset and IoT producers need ever-smaller footprints.

Global Diode Market Trends and Insights

Digitization of Consumer Electronics Ecosystems

Smartphones, wearables, and connected-home devices embed higher semiconductor content per system, lifting discrete component volumes for signal conditioning, battery protection, and data-line safeguarding. Small-signal and electrostatic-discharge arrays such as the ESDS31x series from Texas Instruments deliver +-30 kV protection at up to 5 Gbps data rates, supporting USB, HDMI, and Ethernet interfaces.Asia-Pacific manufacturers assemble about 60% of global electronics hardware, feeding clustered demand for diode arrays that secure high-speed interconnects.

Acceleration of EV Production and On-Board Chargers

Automotive semiconductor demand is increasing as electric-powertrain penetration climbs. Silicon-carbide and gallium-nitride diodes deliver lower switching losses for traction inverters and 800 V chargers; onsemi's EliteSiC platform has been adopted by Volkswagen for next-generation EVs.Infineon's CoolSiC 1200 V MOSFETs allow DC-DC stages to operate beyond 900 V without extra insulation, raising power density while trimming system cost.

Raw-Material Price Volatility (Si, GaAs, GaN)

China provides most primary gallium feedstock, and any export curbs rapidly elevate wafer costs for GaAs and GaN devices. Only 20% of global e-waste is properly recycled, causing critical-metal losses that tighten supply and raise pricing swings. SiC wafer yields remain volatile, contingent on manufacturing maturity and substrate quality.

Other drivers and restraints analyzed in the detailed report include:

- 5G Rollout Boosting RF and Microwave Diodes

- Data-Center Efficiency Mandates Raising Power-Diode Demand

- Thermal Limitations in High-Current Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laser diodes generated the largest diode market size at USD 6.48 billion in 2025 and are positioned for an 8.25% CAGR, propelled by automotive front-lighting, LiDAR sensing, and high-speed fiber communications. Rectifier and Schottky devices continue to secure power-conversion sockets, though their mid-single-digit growth trails laser adoption.

Industrial cutting, projectors, and 3D printing sustain multimode laser-diode volumes, while medical-grade lasers require tighter wavelength stability that lifts average selling prices. In server power supplies, Infineon's GaN transistors integrate a Schottky diode that curbs dead-time losses and elevates efficiency, showcasing cross-category partnerships.

The Diode Market Report is Segmented by Product Type (Schottky Diodes, Zener Diodes, and More), End-User Industry (Communications, Consumer Electronics, Automotive, Defense and Aerospace, Computer and Peripherals, and More), Mounting-Package (Through-Hole, Surface-Mount, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 58.30% of global revenue in 2025, and continues at a 6.45% CAGR through 2031 on the back of integrated supply chains in China, Japan, and South Korea. China absorbed a significant share of world chip sales in 2023, buoyed by government incentives and domestic smartphone exports. Indonesia courts foreign investors with 98 silica-sand mining licenses and tax holidays, aiming to localize substrate production.

North America's share is set to rise by 2030 as the CHIPS Act grants unlock USD 540 billion of private fab commitments, including onsemi's new 8-inch SiC line in Texas. Canada supports GaN epi-wafer startups through Clean-Tech credits, seeking to anchor value-add processes. Mexico's EMS clusters extend tariff-free access to the U.S. vehicle supply chain, stimulating rectifier and transient-voltage-suppressor assembly.

Europe targets more than 20% global production share by 2030, though audit findings warn of schedule risk given permitting delays and skilled-labor gaps. Nexperia's USD 200 million Hamburg investment broadens European SiC capacity, while Poland secures Intel's post-fab testing center that creates 2,000 roles. The Middle East and Africa remain nascent but see pilot solar-inverter fabs in the UAE that specify 1200 V SiC diodes.

- Central Semiconductor Corp.

- Diodes Incorporated

- MinebeaMitsumi Power Semiconductor Device Inc.

- Infineon Technologies AG

- Littelfuse Inc.

- MACOM Technology Solutions Holdings Inc.

- Nexperia BV

- onsemi

- Renesas Electronics Corp.

- ROHM Co. Ltd.

- Micross Components Inc.

- Vishay Intertechnology Inc.

- Toshiba Electronic Devices and Storage Corp.

- Mitsubishi Electric Corp.

- Microchip Technology Inc.

- Semikron Danfoss

- Shindengen Electric Manufacturing Co. Ltd.

- STMicroelectronics NV

- Panasonic Holdings Corp.

- Texas Instruments Inc.

- Kyocera AVX Components Corp.

- Skyworks Solutions Inc.

- Cree - Wolfspeed Inc.

- Alpha and Omega Semiconductor Ltd.

- GlobalFoundries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digitization of consumer electronics ecosystems

- 4.2.2 Acceleration of EV production and on-board chargers

- 4.2.3 5G rollout driving demand for RF and microwave diodes

- 4.2.4 Data-center efficiency mandates boosting power diodes

- 4.2.5 Regulatory tailwinds for GaN-on-Si high-voltage diodes

- 4.2.6 E-waste recycling laws increasing replacement rates

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility (Si, GaAs, GaN)

- 4.3.2 Thermal limitations in high-current packages

- 4.3.3 Patent congestion in WBG semiconductor processes

- 4.3.4 Regional capacity imbalance from localization policies

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Schottky Diodes

- 5.1.2 Zener Diodes

- 5.1.3 Rectifier Diodes

- 5.1.4 Laser Diodes

- 5.1.5 Small-Signal Diodes

- 5.1.6 Electrostatic Discharge Protection Diodes

- 5.1.7 Transient Voltage Suppressor Diodes

- 5.1.8 RF and Microwave Diodes

- 5.2 By End-User Industry

- 5.2.1 Communications

- 5.2.2 Consumer Electronics

- 5.2.3 Automotive

- 5.2.4 Defense and Aerospace

- 5.2.5 Computer and Peripherals

- 5.2.6 Industrial

- 5.2.7 Lighting

- 5.2.8 Other End-User Industries

- 5.3 By Mounting - Package

- 5.3.1 Through-Hole

- 5.3.2 Surface-Mount (SMD)

- 5.3.3 Chip-Scale Package

- 5.3.4 Flip-Chip

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 South-East Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank - Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Central Semiconductor Corp.

- 6.4.2 Diodes Incorporated

- 6.4.3 MinebeaMitsumi Power Semiconductor Device Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Littelfuse Inc.

- 6.4.6 MACOM Technology Solutions Holdings Inc.

- 6.4.7 Nexperia BV

- 6.4.8 onsemi

- 6.4.9 Renesas Electronics Corp.

- 6.4.10 ROHM Co. Ltd.

- 6.4.11 Micross Components Inc.

- 6.4.12 Vishay Intertechnology Inc.

- 6.4.13 Toshiba Electronic Devices and Storage Corp.

- 6.4.14 Mitsubishi Electric Corp.

- 6.4.15 Microchip Technology Inc.

- 6.4.16 Semikron Danfoss

- 6.4.17 Shindengen Electric Manufacturing Co. Ltd.

- 6.4.18 STMicroelectronics NV

- 6.4.19 Panasonic Holdings Corp.

- 6.4.20 Texas Instruments Inc.

- 6.4.21 Kyocera AVX Components Corp.

- 6.4.22 Skyworks Solutions Inc.

- 6.4.23 Cree - Wolfspeed Inc.

- 6.4.24 Alpha and Omega Semiconductor Ltd.

- 6.4.25 GlobalFoundries Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment