|

시장보고서

상품코드

1940784

교류 전동기(AC 모터) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Alternating Current (AC) Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

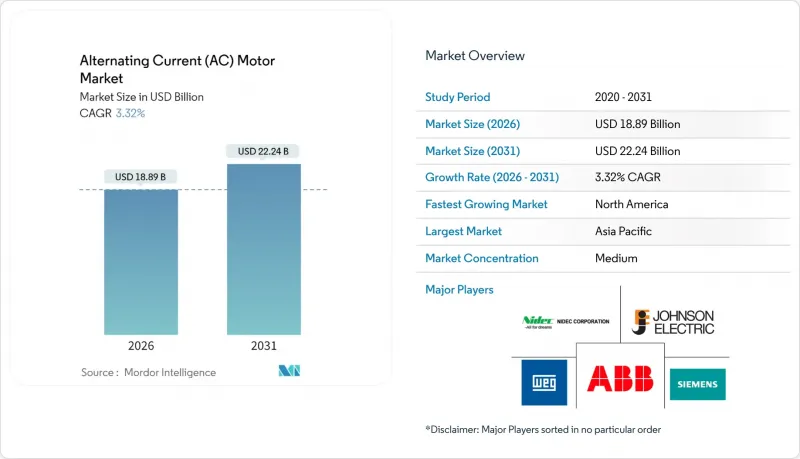

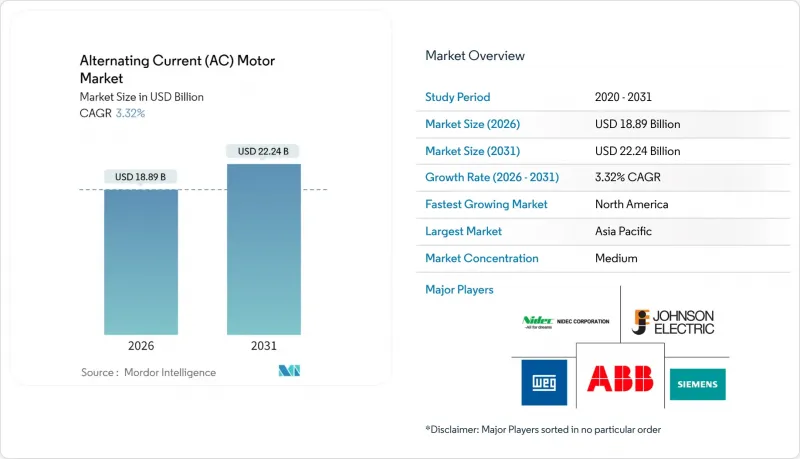

교류 전동기(AC 모터) 시장 규모는 2025년 182억 9,000만 달러에서 2026년 188억 9,000만 달러, 2031년에는 222억 4,000만 달러에 달할 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR)은 3.32%를 나타낼 것으로 예측됩니다.

이러한 성장 궤적은 신규 설비 증설보다는 IE3 및 IE4 규제에 따른 효율성 위주의 교체 주기에 의해 형성되고 있습니다. 프리미엄 효율 설계의 채택은 개별 제조, 재생 에너지, HVAC 부문에서 확대되고 있으며, 아시아 지역의 자동화 프로그램과 북미의 리쇼어링 노력이 기준 수요를 뒷받침하고 있습니다. 벤더 전략은 원자재 가격 변동과 반도체 부족에 대한 대응책으로 구리 권선, 전자기 강판, 파워일렉트로닉스의 수직계열화를 중심으로 전개되고 있습니다. 석유 및 가스 등 성숙한 최종 사용자 분야가 여전히 수익의 기반이 되고 있지만, 수처리, 데이터센터, 풍력 터빈 보조 장치로 빠르게 성장하고 있으며, 이들 분야는 수명 기간 동안 에너지 절약 효과가 프리미엄 가격 책정을 정당화하고 있습니다.

세계 교류 전동기(AC 모터) 시장 동향과 인사이트

의무화된 에너지 절약 규정으로 프리미엄 모터 채택 촉진

IE3는 세계 최저 기준이 되었고, 유럽과 미국에서 IE4의 채택이 가속화되고 있으며, 저효율 구식 모델은 사실상 조달 목록에서 제외되고 있습니다. 제조업체들은 보다 엄격한 손실 제한에 대응하기 위해 자동 적층 프레스 라인과 정밀 자석 조립 라인으로 공장 설비를 업데이트하고 있습니다. 이러한 변화는 새로운 툴에 대한 투자 자금이 부족한 중소형 지역 기업에 부담을 주는 한편, 세계 기존 기업들에 대한 점유율 집중을 촉진하고 있습니다. 조달팀은 현재 75% 및 50% 부하 지점에서 전체 부하 효율로 모터를 평가하고 있으며, 이는 영구 자석 동기 모터 설계의 가치 제안을 강화하고 있습니다. 프리미엄 모터 도입으로 전력회사로부터 리베이트를 받은 최종 사용자는 투자 회수 기간을 2년 이내로 단축할 수 있어 규제 추진에 더욱 박차를 가하고 있습니다.

산업 자동화는 중출력 모터 수요를 가속화하고 있습니다.

자동차, 전자기기, 물류시설에서는 정밀하게 제어되는 1-100kW 모터를 필요로 하는 협동로봇군이 확대되고 있습니다. 인코더가 탑재된 서보급 동기기는 로봇 용접, 픽앤플레이스, 무인운반차(AGV)에 요구되는 서브mm 단위의 정밀도를 실현합니다. 통합 드라이브와 모터 내장 센서에 의한 토크 벡터 제어로 다운타임을 최소화합니다. 중국, 일본, 한국의 스마트 팩토리에 대한 지역별 인센티브가 업그레이드 프로젝트를 앞당기는 한편, 북미 공장도 리쇼어링 계획에 따라 유사한 아키텍처를 채택하고 있습니다. 드라이브, 컨트롤러, 분석 소프트웨어를 번들링할 수 있는 공급업체는 높은 수익률을 달성할 수 있습니다.

원자재 가격 변동으로 제조 경제성에 압박을 가합니다.

구리 권선은 모터 재료 비용의 최대 4분의 1을 차지하기 때문에 2024년 런던금속거래소 가격 18% 변동은 OEM 업체들의 분기별 이익률을 압박했습니다. 네오디뮴-디스프로슘 영구 자석 등급도 중국 수출 정책의 불확실성으로 인해 급등. 제조업체는 슬롯 충진율 최적화, 알루미늄 로터 케이지, 페라이트 고함량 자석 구성 등 대체 방안을 채택했습니다. 대형 제조업체들은 다년간공급 계약이나 자체적인 자석 재활용 프로그램을 통해 헤징을 실시했습니다.

부문 분석

유도 전동기는 견고한 구조와 낮은 초기 비용으로 인해 2025년에도 교류 전동기(AC 모터) 시장에서 69.12%의 점유율을 유지했습니다. 그러나 영구 자석의 자속 밀도 향상과 제어 장치 가격 하락에 따라 동기 전동기의 대체품은 5.53%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 따라서 동기전동기 유형의 교류전동기(AC 모터) 시장 규모는 기존 유도전동기 기반의 대체 수요를 상회하는 성장이 예상됩니다.

고효율은 에너지 집약형 플랜트에 매력적이며, 내장된 위치 피드백은 로봇 공학 및 컨베이어 인덱스 제어를 지원합니다. OEM 제조업체는 동기기를 현장 지향형 구동 장치와 번들로 묶어 시운전을 간소화합니다. 단상 유도 유닛은 주거용 에어컨에서 여전히 주류이지만, 다상 동기 모터는 자동차 도장 공장 및 SMT 라인에 침투하고 있습니다. 두 기술의 교류 모터 시장 점유율 차이는 향후 10년간 축소될 것으로 예측됩니다.

저전압(1kV 미만) 모터는 2025년 일반 제조업 및 HVAC 분야에서 매출의 60.88%를 차지했습니다. 그러나 고전압(11kV 이상) 모델은 풍력발전소 및 해수담수화 플랜트에서 수 메가와트급 보조기기 수요로 인해 5.14%의 가장 높은 CAGR을 보이고 있습니다. 따라서 고전압 교류 모터 시장 규모는 중전압 부문보다 더 빠른 속도로 확대될 것으로 예측됩니다.

OEM 제조업체는 고전압 하에서 부분 방전을 관리하기 위해 소형 고정자 슬롯 설계를 표준화하고, 에폭시 운모 절연 시스템은 습한 해양 나셀 환경에서 수명 연장을 위해 에폭시 운모 절연 시스템을 채택하고 있습니다. 그리드 코드 준수는 또한 우수한 역률 성능을 가진 동기 모터의 채택을 촉진하고 있습니다. 브라질과 베트남의 EPC 계약자들은 장거리 케이블 배선에서 전류 손실과 케이블 손실을 최소화하기 위해 고전압 모터의 채택을 늘리고 있으며, 이 등급의 교류 모터 시장 점유율을 확대하고 있습니다.

지역별 분석

2025년 아시아태평양은 세계 매출의 44.10%를 차지했습니다. 중국에서는 하이테크 제조업의 회복으로 정밀 모터 수입이 촉진되었고, 인도에서는 재생에너지 도입으로 풍력 및 태양광 자산을 위한 대규모 구동장치가 필요하게 되었습니다. 베트남, 태국 등 동남아시아 국가에서는 서보 생산라인의 현지화가 진행되어 수입 리드타임이 단축되고 있습니다. 한국과 일본에서는 고효율 모터 비용의 최대 20%를 지원하는 정부 보조금 지원으로 교체가 가속화되고 있습니다.

남미는 2031년까지 연평균 복합 성장률(CAGR) 4.02%로 가장 빠르게 성장하는 지역입니다. 브라질에서는 국가개발은행의 자금이 산업 현대화에 투입되면서 석유화학 클러스터에서 IE3 플러스 모터의 수주가 증가하고 있습니다. 아르헨티나의 RenovAr 입찰 제도는 풍력발전소 투자를 촉진하고 500kW 이상의 동기식 유닛에 대한 수요를 불러일으키고 있습니다. 환율 변동으로 설비투자 타이밍이 좁아지고 있지만, 멕시코와 브라질에 조립공장을 보유한 OEM 업체들은 환위험을 헤지하고 대량 주문 계약을 확보하고 있습니다.

북미와 유럽은 여전히 갱신 수요가 주도하는 시장입니다. 미국의 CHIPS법 및 IRA법에 근거한 국내 회귀 장려책은 중형 서보 어레이를 필요로 하는 신규 공장 건설을 촉진하고 있습니다. 캐나다의 오지 광산에서는 내빙 베어링이 장착된 견고한 고출력 모터를 선호합니다. 유럽의 에코 디자인 지침에 따라 기존 플랜트 전체에서 IE4 표준으로의 업그레이드가 추진되고 있습니다. 스칸디나비아 국가에서는 지역난방용 펌프에 IE5 표준을 지정하는 한편, 독일 자동차 산업에서는 스마트 모터와 드라이브 패키지의 통합이 진행되어 높은 가격대를 유지하고 있습니다. 두 지역 모두 판매량 성장 둔화를 평균 판매가격 상승으로 만회하며, 기존 브랜드 간 교류 모터 시장 점유율을 안정화시키고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The alternating current motor market size in 2026 is estimated at USD 18.89 billion, growing from 2025 value of USD 18.29 billion with 2031 projections showing USD 22.24 billion, growing at 3.32% CAGR over 2026-2031.

This growth trajectory is shaped less by green-field capacity additions and more by efficiency-driven replacement cycles mandated by IE3 and IE4 regulations. Premium-efficiency design adoption is expanding across discrete manufacturing, renewable-energy, and HVAC segments, while automation programs in Asia and reshoring efforts in North America sustain baseline demand. Vendor strategies revolve around vertical integration in copper winding, electrical steel, and power electronics to buffer raw-material volatility and semiconductor shortages. Mature end-user sectors such as oil and gas continue to anchor revenues, yet faster growth is migrating toward water treatment, data centers, and wind-turbine auxiliaries, where lifetime energy savings justify premium pricing.

Global Alternating Current (AC) Motor Market Trends and Insights

Mandatory Energy-Efficiency Regulations Drive Premium Motor Adoption

IE3 has become the global compliance floor, and IE4 adoption is accelerating across Europe and the United States, effectively eliminating low-efficiency legacy models from procurement lists. Manufacturers are therefore retooling plants with automated lamination stamping and precision magnet-assembly lines to meet stricter loss limits. The shift burdens smaller regional firms that lack capital for new tooling, consolidating share with global incumbents. Procurement teams now evaluate motors on full-load efficiency at 75% and 50% duty points, which strengthens the value proposition of synchronous permanent-magnet designs. End-users capturing utility rebates for premium motors shorten payback periods to under two years, further reinforcing the regulatory push.

Industrial Automation Accelerates Mid-Range Motor Demand

Automotive, electronics, and logistics facilities are scaling collaborative robot fleets that rely on precision-controlled 1-100 kW motors. Servo-grade synchronous machines equipped with encoders deliver the sub-millimeter accuracy required in robotic welding, pick-and-place, and automated guided vehicles. Integrated drives and on-motor sensors enable torque-vector control, minimizing downtime. Regional incentives for smart factories in China, Japan, and Korea are pulling forward upgrade projects, while North American plants adopt similar architectures under reshoring schemes. Suppliers able to bundle drives, controllers, and analytics software capture premium margins.

Raw-Material Price Volatility Pressures Manufacturing Economics

Copper winding accounts for up to one-quarter of motor material cost, so London Metal Exchange price swings of 18% in 2024 drove quarterly margin compression among OEMs. Permanent-magnet grades of neodymium and dysprosium likewise spiked amid Chinese export policy uncertainty. Manufacturers adopted substitution tactics such as optimized slot fills, aluminum rotor cages, and ferrite-rich magnet compositions. Larger players hedge with multiyear supply contracts and proprietary magnet recycling programs.

Other drivers and restraints analyzed in the detailed report include:

- Renewable-Energy Infrastructure Expands High-Power Motor Applications

- Commercial HVAC Modernization

- Premium Motor Cost Barriers in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Induction motors retained 69.12% share of the alternating current motor market in 2025 due to their rugged construction and low initial cost. Yet synchronous alternatives are projected at a 5.53% CAGR as permanent-magnet flux densities climb and controller prices fall. The alternating current motor market size for synchronous variants is therefore set to outpace replacements in the installed induction base.

Their premium efficiency appeals to energy-intensive plants, while built-in position feedback supports robotics and conveyor indexing. OEMs bundle synchronous machines with field-oriented drives that simplify commissioning. Although single-phase induction units remain dominant in residential air conditioners, multi-phase synchronous motors now permeate automotive paint shops and SMT lines. The alternating current motor market share gap between the two technologies is expected to narrow over the decade.

Low-voltage (<1 kV) machines delivered 60.88% revenue in 2025 across general manufacturing and HVAC. High-voltage (>11 kV) models, however, show the strongest 5.14% CAGR as wind farms and desalination plants demand multi-megawatt auxiliaries. The alternating current motor market size in high-voltage will therefore rise faster than the mid-voltage segment.

OEMs standardize compact stator slot designs to manage partial-discharge at high voltages, while epoxy-mica insulation systems extend lifetimes in damp offshore nacelles. Grid-code compliance further drives synchronous options with leading power-factor capability. EPC contractors in Brazil and Vietnam increasingly specify high-voltage motors to minimize current and cable losses across long cable runs, enlarging the alternating current motor market share for this class.

The Alternating Current (AC) Motor Market Report is Segmented by Motor Type (Induction AC Motors, and Synchronous AC Motors), Voltage Class (Low, Medium, and High Voltage), Power Rating (less Than 1 KW, 1-100 KW, 100-500 KW, and More), Efficiency Class (IE1-IE5), End-User Industry (Oil and Gas, Chemicals, Power Generation, Water Treatment, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 44.10% of global revenue in 2025. China's high-tech manufacturing rebound spurred precision-motor imports, whereas India's renewable-energy rollout necessitated utility-scale drives for wind and solar assets. Southeast Asian countries such as Vietnam and Thailand are now localizing servo production lines, shrinking import lead times. Government subsidies covering up to 20% of premium-efficiency motor cost accelerate replacements in Korea and Japan.

South America is the fastest-growing region at 4.02% CAGR through 2031. Brazil channels National Development Bank funding toward industrial modernization, lifting orders for IE3-plus motors in petrochemical clusters. Argentina's RenovAr auctions foster wind-farm investment, triggering demand for >500 kW synchronous units. Currency volatility narrows capex windows, but OEMs with Mexican or Brazilian assembly plants hedge exchange-rate risks and secure volume contracts.

North America and Europe remain replacement-driven markets. U.S. reshoring incentives under the CHIPS and IRA acts stimulate greenfield factories requiring mid-range servo arrays. Canada's remote mining operations favor rugged high-power motors with ice-rated bearings. Europe's Ecodesign mandates drive IE4 upgrades across legacy plants. Scandinavian countries specify IE5 for district-heating pumps, while Germany's automotive sector integrates smart-motor plus drive packages, sustaining premium price points. Both regions compensate for slower unit growth with higher average selling prices, stabilizing alternating current motor market share among established brands.

- ABB Ltd.

- Siemens AG

- WEG Equipamentos Eletricos S.A.

- Nidec Corporation

- Johnson Electric Holdings Limited

- Yaskawa Electric Corporation

- Regal Rexnord Corporation

- Rockwell Automation, Inc.

- Franklin Electric Co., Inc.

- Bosch Rexroth AG

- Kirloskar Electric Company Ltd.

- SEVA-tec GmbH

- Toshiba Corporation

- Mitsubishi Electric Corporation

- TECO Electric & Machinery Co., Ltd.

- Leroy-Somer Holding (Nidec)

- ATB Austria Antriebstechnik AG

- Getriebebau NORD GmbH & Co. KG

- Oriental Motor Co., Ltd.

- Brook Crompton UK Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory energy-efficiency regulations (IE3/IE4)

- 4.2.2 Rapid industrial automation and robotics uptake

- 4.2.3 Expansion of renewable-energy assets (wind, solar)

- 4.2.4 HVAC/R build-out in commercial real estate

- 4.2.5 Rise of axial-flux PM AC motors in e-mobility

- 4.2.6 AI-enabled predictive-maintenance ecosystems

- 4.3 Market Restraints

- 4.3.1 Volatile copper and rare-earth metal prices

- 4.3.2 High upfront cost of premium-efficiency motors

- 4.3.3 Power-electronics (IGBT) supply-chain bottlenecks

- 4.3.4 End-of-life recycling and take-back compliance

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape and Standards

- 4.6 Technological Outlook (Edge and AI analytics)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 Induction AC Motors

- 5.1.1.1 Single-phase

- 5.1.1.2 Poly-phase

- 5.1.2 Synchronous AC Motors

- 5.1.2.1 DC-excited Rotor

- 5.1.2.2 Permanent-Magnet

- 5.1.2.3 Hysteresis

- 5.1.2.4 Reluctance

- 5.1.1 Induction AC Motors

- 5.2 By Voltage Class

- 5.2.1 Low Voltage (<=1 kV)

- 5.2.2 Medium Voltage (>1-11 kV)

- 5.2.3 High Voltage (>11 kV)

- 5.3 By Power Rating

- 5.3.1 Less than 1 kW

- 5.3.2 1-100 kW

- 5.3.3 100-500 kW

- 5.3.4 Greater than 500 kW

- 5.4 By Efficiency Class

- 5.4.1 IE1 (Standard)

- 5.4.2 IE2 (High)

- 5.4.3 IE3 (Premium)

- 5.4.4 IE4 (Super-Premium)

- 5.4.5 IE5 (Ultra-Premium)

- 5.5 By End-user Industry

- 5.5.1 Oil and Gas

- 5.5.2 Chemicals and Petrochemicals

- 5.5.3 Power Generation

- 5.5.4 Water and Wastewater

- 5.5.5 Metals and Mining

- 5.5.6 Food and Beverage

- 5.5.7 Discrete Manufacturing

- 5.5.8 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Ranking Analysis

- 6.5 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.5.1 ABB Ltd.

- 6.5.2 Siemens AG

- 6.5.3 WEG Equipamentos Eletricos S.A.

- 6.5.4 Nidec Corporation

- 6.5.5 Johnson Electric Holdings Limited

- 6.5.6 Yaskawa Electric Corporation

- 6.5.7 Regal Rexnord Corporation

- 6.5.8 Rockwell Automation, Inc.

- 6.5.9 Franklin Electric Co., Inc.

- 6.5.10 Bosch Rexroth AG

- 6.5.11 Kirloskar Electric Company Ltd.

- 6.5.12 SEVA-tec GmbH

- 6.5.13 Toshiba Corporation

- 6.5.14 Mitsubishi Electric Corporation

- 6.5.15 TECO Electric & Machinery Co., Ltd.

- 6.5.16 Leroy-Somer Holding (Nidec)

- 6.5.17 ATB Austria Antriebstechnik AG

- 6.5.18 Getriebebau NORD GmbH & Co. KG

- 6.5.19 Oriental Motor Co., Ltd.

- 6.5.20 Brook Crompton UK Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment