|

시장보고서

상품코드

1940785

영국의 IT 서비스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United Kingdom IT Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

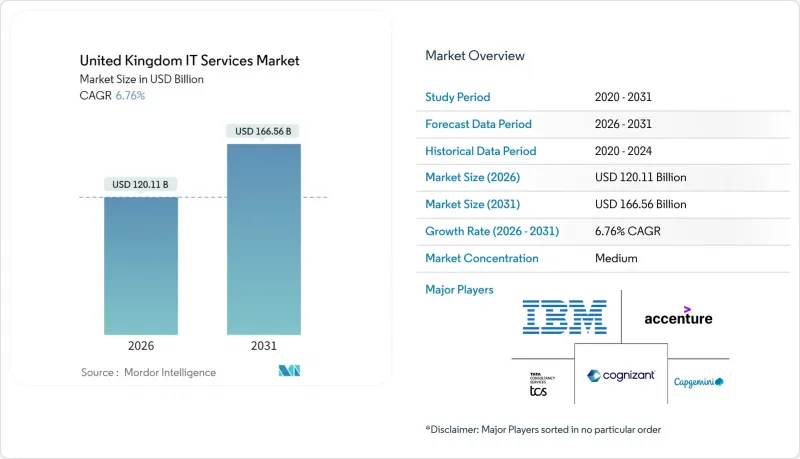

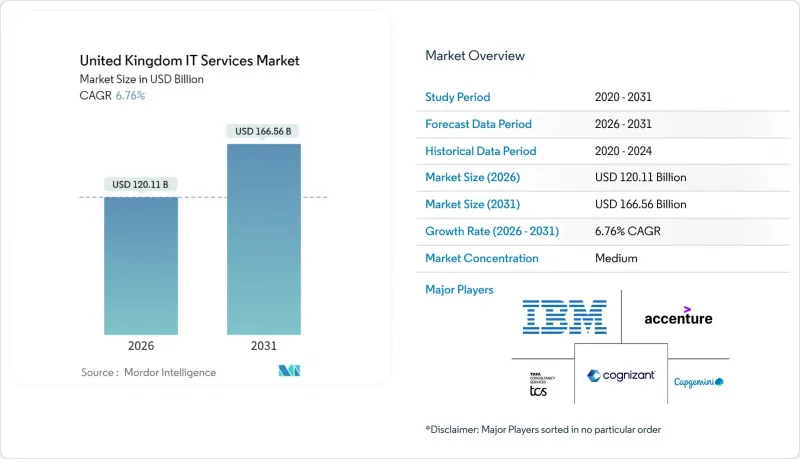

영국의 IT 서비스 시장은 2025년에 1,125억 달러로 평가되었으며, 2026년 1,201억 1,000만 달러에서 2031년까지 1,665억 6,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 6.76%로 예상됩니다.

이러한 성장 궤적은 공공 및 민간 부문의 디지털 전환 가속화, AI 인프라에 대한 지속적인 공공 투자, 사이버 보안 분야의 컴플라이언스 요건 확대에 힘입어 영국 IT 서비스 시장의 회복력을 뒷받침하고 있습니다. 공공부문 클라우드 프레임워크, 생성형 AI 관련 계약 수주액이 사상 최고치를 기록했고, 지역 기술 허브의 성장이 수요를 계속 자극하고 있지만, 임금 인플레이션과 거시경제에 대한 경계감은 여전히 억제요인으로 남아있습니다. 세계 컨설팅 기업들은 대규모 다년 계약을 따내기 위해 AI 분야 실적 강화에 집중하고 있습니다. 반면, 중견 업체들은 관리형 보안이나 인더스트리 4.0 통합과 같은 전문 분야에 특화되어 있습니다. 현지 인력 공급 부족으로 니어쇼어 딜리버리 도입이 증가하고 있지만, 금융, 정부기관 등 규제가 엄격한 업종에서는 여전히 온프레미스 환경의 근접성을 중요시하는 경향이 있습니다.

영국 IT 서비스 시장 동향과 인사이트

AI가 주도하는 디지털 혁신의 물결

영국은 현재 세계 3위의 AI 경제 규모를 자랑하며, AI 도입으로 인한 연간 생산성 향상률 1.5%를 목표로 하고 있습니다. 열의는 있지만, 제조업체 중 16%만이 AI에 대한 지식이 충분하다고 답해 서비스 제공업체에게 컨설팅 기회가 열려 있습니다. 40억 달러의 공공 투자와 140억 달러의 민간 투자가 AI 중심 이니셔티브를 위한 지속적인 파이프라인을 형성하고 있습니다. 액센츄어만 해도 2025년 2분기 생성형 AI 관련 수주액 14억 달러를 확보해 기업의 수요가 활발함을 보여주고 있습니다. 정부가 지정한 AI 성장 지역(옥스퍼드셔 주 칼햄을 기점으로)에서는 대규모 시스템 통합과 클라우드 용량이 필요합니다. 이러한 요인들이 복합적으로 작용하여 영국 IT 서비스 시장은 지속적으로 성장하고 있습니다.

클라우드 우선의 정부 조달 정책

G-Cloud 14가 4,000개 공급업체로부터 46,000개의 서비스를 제공하는 카탈로그에서 보여준 '클라우드 퍼스트' 정책은 공공부문의 조달구조를 변화시키고 있습니다. 2012년 이후 23억 달러의 절감 효과를 통해 경제적인 이점을 입증하고 중소기업의 참여를 촉진하고 있습니다. 향후 진행될 160억 달러 규모의 '기술 서비스 4' 경쟁은 벤더들에게 가장 큰 단일 기회로 작용할 것입니다. 클라우드 도입은 '디지털 기술 분야 계획'에 기반한 전략적 파트너십으로 확대되고 있으며, 조달과 혁신의 경계가 모호해지고 있습니다. 규제 산업이 공공 부문의 기준을 모방하는 형태로 민간 부문으로의 파급효과가 두드러지게 나타나면서 영국 IT 서비스 시장 전체에서 플랫폼 서비스가 두 자릿수 성장을 유지하는 요인이 되고 있습니다.

기술 인력 풀의 임금 상승

2024년에는 기술직의 급여가 7-10% 상승할 것으로 예상되며, 76%의 고용주가 심각한 기술력 부족을 지적하고 있습니다. 2025년 4월 국민보험료율 인상(13.8%에서 15%)으로 인해 고용주의 비용이 증가합니다. 브렉시트 이후 EU 출신 전문가 30만 명의 이직으로 60만 명의 결원이 발생하여 경제에 연간 630억 달러의 손실을 초래하고 있습니다. 기업들은 니어쇼어 전략과 자동화 확대로 부족한 부분을 보완하고 있지만, 치솟은 인건비가 수익률을 압박하며 영국 IT 서비스 시장의 성장을 억제하고 있습니다.

부문 분석

2025년 기준, 클라우드 및 플랫폼 서비스는 영국 IT 서비스 시장 점유율의 28.15%를 차지하고 있으며,G-Cloud 14의 카탈로그 확장 및 레거시 자산의 지속적인 퍼블릭 클라우드 전환을 통해 선도적인 위치를 유지하고 있습니다. 이 부문의 영국 IT 서비스 시장 규모는 160억 달러 규모의 'Technology Services 4' 프레임워크를 배경으로 꾸준한 성장이 예상됩니다. 동시에, 관리형 보안 서비스는 사이버 보안 복원력 법안에 따른 의무적 컴플라이언스를 반영하여 2031년까지 CAGR 9.38%를 기록할 것으로 예측됩니다. IT 컨설팅은 기업용 AI 프로그램으로 견조한 성장세를 유지하고 있으며, IT 아웃소싱과 BPO는 자동화 속에서 균형 잡힌 성장을 경험하고 있습니다.

클라우드 마이그레이션과 보안 강화의 상호 촉진은 공급자의 수익 확대를 지원하고 있습니다. 기관이 온프레미스 시스템을 대체할 때, 플랫폼 계약에 관리형 보안 계약이 번들로 제공되면 지갑 점유율이 확대됩니다. 14억 달러 규모의 NHS 입찰 사례는 산업 특화형 프레임워크가 생태계 공급업체를 견인하는 메커니즘을 보여줍니다. 따라서 영국 IT 서비스 시장에서는 하이퍼스케일 기술과 제로 트러스트 아키텍처를 결합한 벤더가 우위를 점하게 될 것입니다.

2025년 기준, 대기업은 영국 IT 서비스 시장 규모의 64.25%를 차지하며, 멀티 클라우드 구축, 생성형 AI 파일럿, 규제 대응 현대화에 많은 예산을 투자하고 있습니다. 지배적인 위치에 있는 것, 변화 로드맵이 성숙함에 따라 그 성장 속도는 완만 해지고 있습니다. 한편, 중소기업 부문은 중소기업 디지털 도입 태스크포스의 10단계 행동계획에 힘입어 2031년까지 CAGR 8.98%로 확대될 것으로 예상됩니다. 영국 IT 서비스 시장에서 중소기업의 점유율은 여전히 미미하지만, AI를 통한 생산성 향상으로 781억 달러의 경제적 가치 창출이 기대되는 등 유망한 시장 기반이 형성되고 있습니다.

서비스 모델은 중소기업이 선호하는 짧은 판매 주기와 성과 기반 가격 설정에 적응해야 합니다. 지역 AI 혁신 허브, 세액공제, 클라우드 마켓플레이스는 진입장벽을 낮추고, 공급자가 재현 가능한 패키지를 개발할 수 있도록 지원합니다. 이에 따라 영국 IT 서비스 시장에서는 런던 외의 소규모 기업들을 위한 맞춤형 구독형 솔루션이 증가하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The UK IT services market was valued at USD 112.5 billion in 2025 and estimated to grow from USD 120.11 billion in 2026 to reach USD 166.56 billion by 2031, at a CAGR of 6.76% during the forecast period (2026-2031).

This trajectory underscores the resilience of the UK IT services market, powered by accelerating digital transformation in both public and private sectors, sustained public investment in AI infrastructure, and expanding compliance mandates in cybersecurity. Public-sector cloud frameworks, record generative-AI contract bookings, and growing regional tech hubs continue to stimulate demand, while wage inflation and macro-economic caution remain moderating influences. Global consulting firms are reinforcing their AI credentials to secure large multi-year deals, whereas mid-tier providers are targeting specialized niches such as managed security and Industry 4.0 integration. Nearshore delivery adoption is rising in response to tight local talent supply, yet the UK IT services market still favors on-premises proximity for high-regulation verticals such as finance and government.

United Kingdom IT Services Market Trends and Insights

AI-led Digital Transformation Wave

The United Kingdom now ranks as the world's third-largest AI economy and is targeting annual productivity gains of 1.5% through AI deployment. Despite enthusiasm, only 16% of manufacturers report adequate AI knowledge, opening consultative opportunities for service providers. Public investment of USD 4 billion and USD 14 billion in private commitments form a durable pipeline for AI-centric engagements. Accenture alone secured USD 1.4 billion in generative-AI bookings during Q2 FY25, signaling robust enterprise appetite. Government-designated AI Growth Zones-beginning with Culham, Oxfordshire-will require extensive systems integration and cloud capacity. Together, these factors generate a sustained uplift in the UK IT services market.

Cloud-first Government Procurement Policies

The cloud-first mandate, highlighted by G-Cloud 14's catalog of 46,000 services from 4,000 suppliers, is reshaping public-sector procurement. Framework savings of USD 2.3 billion since 2012 validate economic benefits and stimulate SME participation. The forthcoming USD 16 billion Technology Services 4 competition represents the largest single opportunity for vendors. Cloud uptake extends into strategic partnerships under the Digital and Technologies Sector Plan, blurring lines between procurement and innovation. Private-sector spillovers are visible as regulated industries replicate public-sector standards, reinforcing double-digit growth in platform services across the UK IT services market.

High Wage Inflation in Tech Talent Pool

Tech salaries escalated 7-10% in 2024, with 76% of employers citing acute skill shortages. The April 2025 National Insurance hike from 13.8% to 15% inflate employer costs. Post-Brexit workforce attrition of 300,000 EU professionals leaves 600,000 vacancies that cost the economy USD 63 billion annually. Firms offset gaps by expanding nearshore and automation strategies, yet elevated labor costs compress margins and temper growth in the UK IT services market.

Other drivers and restraints analyzed in the detailed report include:

- Acute Cyber-threat Environment

- Convergence of OT-IT in UK Manufacturing

- Near-term Macroeconomic Slowdown

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud and platform services represented 28.15% of the UK IT services market share in 2025, a leadership position supported by G-Cloud 14's widened catalog and ongoing migration of legacy estates to the public cloud. The UK IT services market size for this segment is projected to compound steadily on the back of the USD 16 billion Technology Services 4 framework. Simultaneously, managed security services are forecast to post a 9.38% CAGR to 2031, reflecting mandatory compliance under the Cyber Security and Resilience Bill. IT consulting remains resilient thanks to enterprise AI programs, while IT outsourcing and BPO experience balanced growth amid automation.

Cross-pollination between cloud migration and security hardening underpins provider revenue expansion. As agencies replace on-premise systems, bundled managed-security contracts accompany platform deals, magnifying wallet share. NHS tenders worth USD 1.4 billion illustrate how sector-specific frameworks pull along ecosystem suppliers. The UK IT services market, therefore, rewards vendors that combine hyperscale know-how with zero-trust architectures.

Large enterprises controlled 64.25% of the UK IT services market size in 2025, leveraging substantial budgets for multi-cloud rollouts, generative-AI pilots, and regulatory modernization. Despite dominance, their growth rate moderates as transformation roadmaps mature. In contrast, the SME cohort is projected to expand at a 8.98% CAGR to 2031, propelled by the SME Digital Adoption Taskforce's 10-step action plan. UK IT services market share among SMEs remains modest, yet the economic value potential-USD 78.1 billion in AI-enabled productivity gains-creates a fertile addressable base.

Service models must adjust to shorter sales cycles and outcome-based pricing preferred by smaller firms. Regional AI innovation hubs, tax credits, and cloud marketplaces lower entry barriers, allowing providers to develop repeatable packages. Accordingly, the UK IT services market is witnessing a rise in subscription-oriented solutions tailored to micro-enterprises outside London.

The UK IT Services Market Report is Segmented by Service Type (IT Consulting and Implementation, IT Outsourcing, Business Process Outsourcing, and More), End-User Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Deployment Model (Onshore Delivery, Nearshore Delivery, and More), and End-User Vertical (BFSI, Government and Public Sector, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture plc

- IBM UK Ltd.

- Capgemini SE

- Tata Consultancy Services (TCS) UK

- Infosys Ltd. UK

- Cognizant Technology Solutions UK

- HCL Technologies UK

- Wipro Ltd. UK

- Fujitsu Services Ltd.

- DXC Technology UK

- CGI IT UK Ltd.

- Sopra Steria Ltd.

- Computacenter plc

- Softcat plc

- Kainos Group plc

- BJSS Ltd.

- Endava plc

- Version 1 Software UK Ltd.

- FDM Group plc

- PA Consulting Group

- Civica Ltd.

- NTT DATA UK Ltd.

- Capita IT Services

- Rackspace Technology UK

- Mastek (UK) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-led Digital Transformation Wave

- 4.2.2 Cloud-first Government Procurement Policies

- 4.2.3 Acute Cyber-threat Environment

- 4.2.4 Convergence of OT-IT in UK Manufacturing

- 4.2.5 Rise of Green-IT Mandates (Sustainability Targets)

- 4.2.6 Brexit-Driven Regulatory Complexity

- 4.3 Market Restraints

- 4.3.1 High Wage Inflation in Tech Talent Pool

- 4.3.2 Near-term Macroeconomic Slowdown

- 4.3.3 Data-Sovereignty Concerns with Offshore Delivery

- 4.3.4 Fragmented SME Adoption Outside London

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Evaluation of Critical Regulatory Framework

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Competitive Rivalry

- 4.8.2 Threat of New Entrants

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Bargaining Power of Buyers

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 IT Consulting and Implementation

- 5.1.2 IT Outsourcing (ITO)

- 5.1.3 Business Process Outsourcing (BPO)

- 5.1.4 Managed Security Services

- 5.1.5 Cloud and Platform Services

- 5.2 By End-User Enterprise Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By Deployment Model

- 5.3.1 Onshore Delivery

- 5.3.2 Nearshore Delivery

- 5.3.3 Offshore Delivery

- 5.4 By End-user Vertical

- 5.4.1 BFSI

- 5.4.2 Manufacturing

- 5.4.3 Government and Public Sector

- 5.4.4 Healthcare and Life-Sciences

- 5.4.5 Retail and Consumer Goods

- 5.4.6 Telecom and Media

- 5.4.7 Logistics and Transport

- 5.4.8 Energy and Utilities

- 5.4.9 Other End-user Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 IBM UK Ltd.

- 6.4.3 Capgemini SE

- 6.4.4 Tata Consultancy Services (TCS) UK

- 6.4.5 Infosys Ltd. UK

- 6.4.6 Cognizant Technology Solutions UK

- 6.4.7 HCL Technologies UK

- 6.4.8 Wipro Ltd. UK

- 6.4.9 Fujitsu Services Ltd.

- 6.4.10 DXC Technology UK

- 6.4.11 CGI IT UK Ltd.

- 6.4.12 Sopra Steria Ltd.

- 6.4.13 Computacenter plc

- 6.4.14 Softcat plc

- 6.4.15 Kainos Group plc

- 6.4.16 BJSS Ltd.

- 6.4.17 Endava plc

- 6.4.18 Version 1 Software UK Ltd.

- 6.4.19 FDM Group plc

- 6.4.20 PA Consulting Group

- 6.4.21 Civica Ltd.

- 6.4.22 NTT DATA UK Ltd.

- 6.4.23 Capita IT Services

- 6.4.24 Rackspace Technology UK

- 6.4.25 Mastek (UK) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment